|

시장보고서

상품코드

1692497

오산화니오브 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Niobium Pentoxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

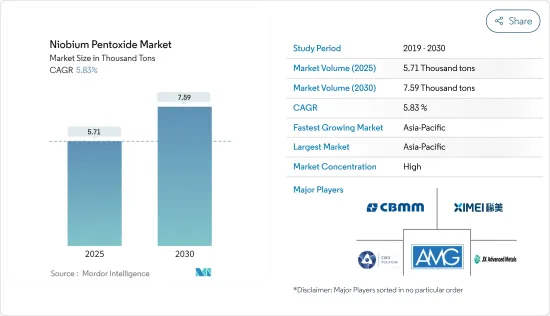

세계의 오산화니오브 시장 규모는 2025년 5,710톤으로 예측되며, 예측 기간 중(2025-2030년) CAGR 5.83%로 확대되어, 2030년에는 7,590톤에 달할 것으로 예측되고 있습니다.

오산화니오브 시장은 COVID-19에 의한 후퇴에 직면했습니다.

주요 하이라이트

- 단기적으로는 광학산업에 있어서의 오산화니오브 수요 증가와 제조업에 있어서의 고품질강 수요 증가가 조사 대상 시장 수요를 견인하는 주된 요인입니다.

- 그러나 오산화 니오브의 급성 노출에 의한 건강 문제에 대한 우려가 시장의 성장을 방해할 것으로 예측됩니다.

- 그럼에도 불구하고 바이오 메디컬 분야 수요 증가는 이 시장에 새로운 기회를 가져올 것으로 기대됩니다.

- 아시아태평양은 중국과 인도 수요가 대부분을 차지하고 세계 시장을 독점할 것으로 예측됩니다.

오산화 니오브 시장 동향

제조업에 의한 고품질강 수요 증가

- 오산화니오브의 동향의 원동력이 되고 있는 것은 제조업에 의한 고품질 강 수요의 급증입니다.

- 오산화니오브은 고강도 저합금(HSLA)강의 강도와 인성을 강화해, 건설, 수송, 에너지 분야에서 널리 이용되고 있습니다.

- 스테인리스 스틸에서는 오산화니오브는 내식성을 높여, 식품 가공, 화학 가공, 의료기기 등의 분야에 도움이 됩니다.

- 게다가 석유 및 가스 수송에 불가결한 파이프라인 강을 강화합니다.

- 세계철강협회(worldsteel)에 따르면 세계의 조강 생산량은 2023년 11월의 1억 4,490만 톤에서 2023년 12월에는 1억 3,570만 톤으로 감소했습니다. 하지만 2024년 7월에는 1억 5,280만 톤으로 회복했습니다. 그러나 2023년 7월부터는 4.7% 감소해 업계의 과제가 부각되었습니다.

- 게다가 중국, 일본, 미국 등의 국가에서의 철강 생산 능력의 강화는 세계의 철강 생산량을 한층 더 촉진해, 그것에 의해 연구 시장의 성장을 지지하고 있습니다.

- 세계철강협회에 따르면 2024년 7월 일본의 철강 생산량은 710만톤으로 2023년 같은 달부터 3.8% 감소했습니다.

- 세계 제4위의 조강 생산국인 미국은 2024년 7월 생산량을 6.9Mt로 보고해 2.1%의 소폭 증가가 되었습니다.

- 독일은 긍정적인 동향을 나타내, 2024년 7월의 추정 생산량은 4.8% 증가의 3.1 Mt가 되었습니다.

- 브라질이 가장 높은 성장률을 보였으며 2024년 7월 생산량은 3.1톤으로 11.6%의 경이적인 성장률을 보였습니다.

- 2023년, 남아프리카의 조강 생산량은 약 4,871.0킬로톤에 이르렀고, 전년 대비 약 10.64%의 성장을 나타냈습니다.

- 철강은 건설이나 철도로부터 자동차 제조나 소비재에 이르기까지, 다양한 분야에 불가결한 것입니다 지난 10년간, 인도를 중심으로 하는 개발도상국의 공업화가 철강 수요를 대폭 밀어 올렸습니다.

- 이러한 역학을 생각하면, 오산화니오브 시장은 향후 수년에 크게 성장할 가능성이 있습니다.

아시아태평양이 시장을 독점할 전망

- 아시아태평양이 오산화 니오브 시장을 독점하고 예측 기간 중에 가장 급성장하는 지역이 됩니다.

- 오산화니오브와 그 유도체는 철강 생산에서 중요한 역할을 합니다. 니오브를 첨가하면 철강의 강도가 향상되고 고온 산화 및 부식에 대한 내성이 향상됩니다. 니오브는 또한 연성 취성 전이 온도를 낮추고 용접 특성과 성형성을 향상시킵니다. 특히 고급 구조용 강재, 고강도 저합금(HSLA) 강재 및 스테인리스 강 제조에 필수적입니다.

- 니오브를 농축한 HSLA강은 자동차나 건설 분야에서 주로 사용되고 있습니다.

- 인도에서는 인도 자동차 공업회(SIAM)의 데이터에 의하면, 2024년 1월부터 3월까지 승용차, 상용차, 삼륜차, 사륜차의 생산 대수는 739만대에 달했습니다.특히 승용차는 114만대, 상용차는 26만 8,000대였습니다.

- 2024년 인도에서는 합리적인 가격의 주택이 70% 증가할 것으로 예상되고 있습니다. 부동산법, GST, REIT라고 하는 최근의 개혁은 인가를 신속화해, 건설 업계를 강화하는 것으로, 시장의 성장을 가속할 것을 목적으로 하고 있습니다.

- 중국은 세계 유수의 철강 생산국이며, 그 생산량은 국내외 시장에 공급되고 있습니다. 세계 철강협회의 데이터에 따르면, 중국은 최대 생산국의 지위를 유지했지만, 2024년 7월의 생산량은 9.0% 감소해, 합계 8,290만 톤(Mt)이 되었습니다.

- BigMint에 따르면, 인도의 철강 생산량은 전년 대비 6% 가까이 증가하고, 2024/2025년 말(2025년 3월기)에는 1억 5,200만 톤에 이를 것으로 예측되고 있습니다.

- 니오브 합금은 건설, 특히 구조 부품이나 내하중 부품에 있어서도 매우 중요합니다.

- 플라스틱 수출 촉진위원회의 데이터에 따르면, 인도는 2023년 12월 안경과 고글의 월간 수출액으로 최고를 기록했습니다.

- Boeing의 Commercial Outlook(2023-2042)에 따르면, 중국에서는 2042년까지 약 8,560기의 항공기가 새롭게 납품될 것으로 예상되고 있습니다.

- 오산화 니오브는 그 높은 표면적, 뛰어난 전기 전도성, 안정성, 내구성에 의해 고성능 슈퍼커패시터의 개발에 있어서의 주요한 기업로서 대두해 왔습니다.

- 중국국가에너지국의 데이터에 따르면 2023년에는 31기가와트 이상의 에너지저장시스템이 새롭게 설치되어 2024년에는 36기가와트에 이를 것으로 예측되고 있습니다.

- 이러한 역학을 고려하면, 아시아태평양의 오산화 니오브 시장은 예측 기간 중에 안정된 성장을 이룰 것으로 보입니다.

오산화 니오브 산업 개요

오산화 니오브 시장은 통합 된 성질을 가지고 있습니다. 주요 기업(특별한 순서 없음)에는 CBMM, Ximei Resources Holding Limited, JSC Solikamsk Magnesium Plant, AMG, JX Advanced Metals Corporation 등이 포함됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 광학산업에서 오산화니오브 수요 증가

- 제조업에서 고품질강 수요 증가

- 기타 촉진요인

- 억제요인

- 오산화니오브의 급성 노출에 의한 건강 문제에 대한 우려

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 등급

- 공업용 등급(순도 99.0%-99.8%)

- 3N

- 4N

- 용도

- 니오브 금속

- 광학 유리

- 슈퍼커패시터

- 초합금

- 세라믹

- 기타 용도

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 합병, 인수, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- AMG

- CBMM

- Chengdu Huarui Industrial Co., Ltd.

- F&X Electro-Materials Limited

- Hebei Suoyi New Material Technology Co., Ltd.

- JSC Solikamsk Magnesium Plant

- JX Advanced Metals Corporation

- Kurt J. Lesker Company

- Merck KGaA

- Mitsui Mining & Smelting Co. Ltd.

- MPIL

- Taki Chemical Co., Ltd.

- XIMEI Resources Holding Limited

제7장 시장 기회와 앞으로의 동향

- 바이오메디컬 분야 수요 증가

- 기타 기회

The Niobium Pentoxide Market size is estimated at 5.71 thousand tons in 2025, and is expected to reach 7.59 thousand tons by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

The niobium pentoxide market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to see significant growth in the upcoming years.

Key Highlights

- Over the short term, the growing demand for niobium pentoxide in the optics industry and the increasing demand for high-quality steel from the manufacturing sector are the major factors driving the demand for the market studied.

- However, concerns about health issues caused by acute exposure to niobium pentoxide are expected to hinder the market's growth.

- Nevertheless, the growing demand from the biomedical sector is expected to create new opportunities for the market studied.

- Asia-Pacific region is expected to dominate the market across the world, with the majority of demand coming from China and India.

Niobium Pentoxide Market Trends

Increasing Demand for High-quality Steel from the Manufacturing Sector

- The manufacturing sector's surging demand for high-quality steel is driving the rising trend of niobium pentoxide. Its incorporation in steel production enhances strength, toughness, and corrosion resistance, solidifying its role as a vital alloying element across diverse steel applications.

- Niobium pentoxide bolsters the strength and toughness of high-strength, low-alloy (HSLA) steel, which is widely utilized in the construction, transportation, and energy sectors.

- In stainless steel, niobium pentoxide enhances corrosion resistance, benefiting sectors like food processing, chemical processing, and medical equipment.

- Additionally, it strengthens pipeline steel, which is crucial for oil and gas transportation.

- According to the World Steel Association (worldsteel), global crude steel production dipped to 135.7 million tonnes (Mt) in December 2023 from 144.9 million tonnes (Mt) in November 2023. However, July 2024 saw a rebound to 152.8 million tonnes (Mt). Despite this, it represented a 4.7% decline from July 2023, highlighting the industry's challenges. However, as emerging economies intensify their infrastructure and construction initiatives, steel demand is set to recover in the coming years.

- Additionally, bolstered steel production capacities in nations like China, Japan, and the United States have further fueled global steel output, thereby supporting the growth of the market studied.

- As per the World Steel Association, Japan's steel production in July 2024 stood at 7.1 Mt, marking a 3.8% decline from the same month in 2023. Year-to-date figures show a production of 49.8 Mt, reflecting a 2.8% year-on-year drop.

- The United States, ranked as the fourth-largest producer of crude steel globally, reported a production of 6.9 Mt in July 2024, witnessing a modest increase of 2.1%. However, the year-to-date production figures were at 46.9 Mt, indicating a decline of 1.8%, as per the World Steel Association.

- Germany showcased a positive trend, producing an estimated 3.1 Mt in July 2024, which is a 4.8% increase. Year-to-date, Germany's production reached 22.5 Mt, marking a notable 4.5% rise, according to data from the World Steel Association.

- Brazil led the pack with the highest growth, producing 3.1 Mt in July 2024, an impressive increase of 11.6%. Year-to-date, Brazil's production stood at 19.4 Mt, up by 3.3%, as reported by the World Steel Association.

- In 2023, South Africa's crude steel production reached approximately 4,871.0 kilotons, marking a growth rate of about 10.64% from the previous year. This surge in production, as reported by the World Steel Association (worldsteel), underscored the country's steel sector and niobium pentoxide market.

- Steel is integral to various sectors, from construction and railroads to automotive manufacturing and consumer goods. Over the last decade, industrialization in developing nations, especially India, has significantly boosted steel demand.

- Given these dynamics, the niobium pentoxide market is poised for substantial growth in the coming years.

Asia Pacific Region is Expected to Dominate the Market

- Asia-Pacific is set to dominate the niobium pentoxide market, emerging as the fastest-growing region during the forecast period. This growth is driven by rising demands across various applications, such as niobium metal, optical glass, supercapacitors, superalloys, and ceramics, especially in countries like China, India, South Korea, Japan, and several Southeast Asian nations.

- Niobium pentoxide and its derivatives play a crucial role in iron and steel production. Adding niobium enhances steel's strength and boosts its resistance to high-temperature oxidation and corrosion. Niobium also lowers the ductile-brittle transition temperature and enhances welding properties and formability. It's particularly vital in producing high-grade structural steel, high-strength low alloy (HSLA) steels, and stainless steel.

- HSLA steels, enriched with niobium, find primary applications in the automotive and construction sectors. Notably, around 80% of all automotive sheet steel grades are micro-alloyed with niobium, ensuring vehicles are fuel-efficient, safe, and durable.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three wheelers, two wheelers and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million and 268 thousand units, respectively.

- In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST, and REITs, aim to expedite approvals and strengthen the construction industry, driving market growth.

- China stands as the globe's leading producer of iron and steel, with its output serving both domestic and international markets. As per the data from the World Steel Association, while China retained its title as the largest producer, it saw a 9.0% dip in output for July 2024, totaling 82.9 million tonnes (Mt). Year-to-date figures show China's production at 613.7 Mt, reflecting a 2.2% drop from 2023.

- According to BigMint, India's steel production is projected to grow by nearly 6% year-on-year, reaching 152 million tons by the close of FY2024/2025 (ending March 2025). The bulk of this projected output is anticipated to stem from steel mills utilizing blast furnaces.

- Niobium alloys are also pivotal in construction, especially for structural and load-bearing components. China, leading the global construction arena with 20% of worldwide investments, is set to spend nearly USD 13 trillion on buildings by 2030, signaling a robust market outlook.

- Data from the Plastics Export Promotion Council highlights that India achieved its highest monthly export of spectacles and goggles in December 2023, a milestone not seen in 60 months. The Indian optical market currently grapples with challenges like low-cost competition, reliance on imported lenses, and swiftly evolving consumer preferences. In 2023, the market for contact lenses in India was valued at approximately USD 164.30 million.

- According to the Boeing's Commercial Outlook (2023-2042) anticipates around 8,560 new aircraft deliveries in China by 2042. This surge in deliveries is expected to elevate the demand for niobium pentoxide in manufacturing aircraft components, particularly engine blades.

- Niobium pentoxide is emerging as a key player in developing high-performance supercapacitors, owing to its high surface area, excellent electrical conductivity, stability, and durability..

- Data from China's National Energy Administration indicates that in 2023, the country installed over 31 gigawatts of new energy storage systems, with projections reaching 36 gigawatts by 2024. Endorsed by Chinese leadership, these new energy storage solutions encompass lithium-ion batteries, supercapacitors, and flow batteries.

- Given these dynamics, the niobium pentoxide market in the Asia-Pacific region is poised for steady growth during the forecast period.

Niobium Pentoxide Industry Overview

The niobium pentoxide market is consolidated in nature. The major players (not in any particular order) include CBMM, Ximei Resources Holding Limited, JSC Solikamsk Magnesium Plant, AMG, and JX Advanced Metals Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Niobium Pentoxide in the Optics Industry

- 4.1.2 Increasing Demand for High-quality Steel from the Manufacturing Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Concerns about Health Issues Caused by Acute Exposure to Niobium Pentoxide

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Grade

- 5.1.1 Industrial Grade (purity: 99.0% to 99.8%)

- 5.1.2 3N

- 5.1.3 4N

- 5.2 Application

- 5.2.1 Niobium Metal

- 5.2.2 Optical Glass

- 5.2.3 Supercapacitors

- 5.2.4 Superalloys

- 5.2.5 Ceramics

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AMG

- 6.4.2 CBMM

- 6.4.3 Chengdu Huarui Industrial Co., Ltd.

- 6.4.4 F&X Electro-Materials Limited

- 6.4.5 Hebei Suoyi New Material Technology Co., Ltd.

- 6.4.6 JSC Solikamsk Magnesium Plant

- 6.4.7 JX Advanced Metals Corporation

- 6.4.8 Kurt J. Lesker Company

- 6.4.9 Merck KGaA

- 6.4.10 Mitsui Mining & Smelting Co. Ltd.

- 6.4.11 MPIL

- 6.4.12 Taki Chemical Co., Ltd.

- 6.4.13 XIMEI Resources Holding Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from the Biomedical Sector

- 7.2 Other Opportunities