|

시장보고서

상품코드

1692521

급성 호흡곤란 증후군(ARDS) 치료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 동향 예측(2025-2030년)Global Acute Respiratory Distress Syndrome (ARDS) Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

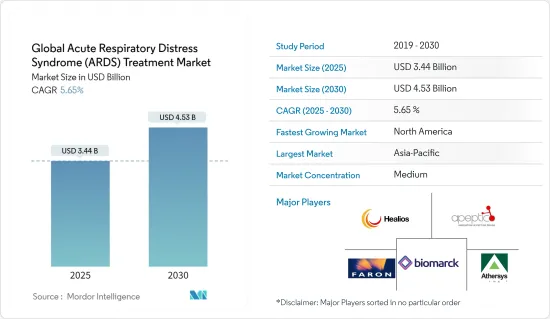

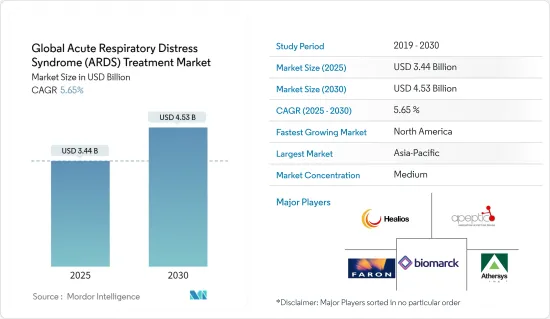

세계의 급성 호흡곤란 증후군 치료 시장 규모는 2025년에 34억 4,000만 달러로 추정되고, 2030년에는 45억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 5.65%를 나타낼 전망입니다.

중증 감염 COVID-19 환자의 임상 데이터에 따르면 폐 부종의 방사선학적 증거는 COVID-19 환자에서 급성 폐 손상(ALI) 증상이 저산소혈증 및 ARDS로 진행될 수 있음을 보여줍니다. 2021년 12월 폐렴에 발표된 “COVID-19의 급성 호흡곤란 증후군 : 가능한 기전 및 치료 관리”라는 제목의 연구에 따르면 입원 환자의 약 1/3(33%)이 ARDS를 경험하는 것으로 나타났습니다. 또한 중환자실에 입원한 COVID-19 환자의 약 3/4(또는 75%)에서 ARDS가 나타납니다. COVID-19에 걸린 ARDS 환자는 예후가 나쁘고 사망률이 높습니다.

급성 호흡곤란 증후군(ARDS) 시장은 급성 폐 손상의 유병률 및 발생률 증가, 광범위한 ARDS 위험 요인, ARDS를 앓고 있는 COVID-19 환자 수 증가 등의 요인에 의해 주도되고 있습니다. 급성 호흡곤란증후군(ARDS)의 글로벌 시장도 생활습관, 대기오염, ARDS를 유발하는 사고와 관련된 질병의 유병률 등의 요인으로 인해 성장할 것으로 예상됩니다. '급성 호흡곤란 증후군'이라는 제목의 연구에 따르면 급성 호흡곤란 증후군은 성인의 역학, 병태생리, 병리 및 병인"이라는 제목으로 2022년 6월에 발표된 마크 D 시겔의 연구에 따르면 미국에서는 연간 약 190,000건의 ARDS증례가 보고되고 있습니다. 환자 연령이 높아질수록 발생률이 증가하여 15-19세의 경우 10만 명당 16명에서 75-84세의 경우 10만 명당 306명으로 증가했습니다. 또한 노인 인구의 증가는 시장 성장을 뒷받침합니다. 예를 들어, 유엔 경제사회국의 '세계 인구 고령화 2020 하이라이트' 보고서에 따르면 2020년 전 세계 65세 이상 인구는 7억 2,700만 명에 달한다고 합니다. 이 인구는 2050년에는 두 배 이상 증가하여 약 15억 명에 달할 것으로 예상됩니다. 고령 인구는 호흡기 및 기타 질병에 걸릴 위험이 높기 때문에 치료의 필요성이 높아져 시장 성장을 견인할 것으로 예상됩니다.

또한 의료 지출 증가와 시장 참여자들의 전략은 글로벌 급성 호흡곤란증후군(ARDS) 시장의 성장 기회를 제공합니다. 예를 들어, 2020년 6월 NeuroRx는 릴리프 테라퓨틱스와 협력하여 미국 식품의약국이 코로나19와 관련된 급성 폐 손상 및 급성 호흡곤란 증후군 치료를 위한 RLF-100(아비프타딜)의 연구를 위해 NeuroRx에 패스트 트랙 지정을 부여했다고 발표했습니다. 또한 2020년 11월, 노바티스는 급성 호흡곤란 증후군 치료를 위한 레메스템셀-L의 개발, 판매, 제조를 위해 메소블라스트와 전 세계 독점 라이선스 및 협력 계약을 체결했다고 발표했습니다.

이와 같이 앞서 언급 한 모든 요인은 예측 기간 동안 시장 성장을 촉진 할 것으로 예상되지만 치료 및 장치와 관련된 높은 비용과 규제 합병증은 시장 성장을 제한 할 수 있습니다.

급성 호흡곤란 증후군 치료 시장 동향

최종 사용자 부문 별 병원 및 클리닉은 예측 기간 동안 견조한 성장을 할 전망

병원 및 클리닉은 수술 절차 및 개선 된 치료를위한 첨단 기술 장비를 잘 갖추고 있으며 병원 부문은 ARDS로 인한 병원 입원 건수 증가, 환자 풀 수 증가, 시장 참여자의 신제품 출시로 인해 빠른 성장을 목격하고 있으며 예측 기간 동안 계속 될 것으로 예상되므로 부문의 성장을 주도 할 것으로 예상됩니다.

또한 민간기업에 의한 병원 수 증가도 시장 성장을 가속할 것으로 예측됩니다. 이 수는 2,946으로, 2022년에는 2,960으로 증가했습니다. 그 결과, ARDS 환자의 치료에 이용할 수 있는 침대 수가 증가하고, 병원 수 증가가 예측 기간 동안 같은 부문의 성장을 지원하고 있습니다.

병원 입원 및 중환자실 입원이 증가함에 따라 ARDS 치료의 필요성이 증가하여 시장 성장을 주도하고 있습니다. 2022년 1월 PLOS One 저널에 발표된 급성 호흡곤란증후군 환자의 18.4%가 재입원을 경험한 것으로 나타났습니다. 또한, 2022년 5월 호주보건복지연구원이 발표한 자료에 따르면 2020-2021년 급성 호흡곤란증후군으로 인한 입원 건수는 약 1,180만 건으로 2019-2020년에 비해 6.3% 증가했습니다. 또한 1,180만 건의 입원 중 7.0%는 중환자실(ICU) 입원, 3.8%는 호흡기 질환 입원, 10.3%는 환자가 병원에서 사망한 분리형 입원이었다고 보고했습니다.

따라서, 상기 요인에 의해 이 부문은 예측 기간 동안 견조한 성장률을 나타낼 것으로 예측됩니다.

예측기간 중 북미가 큰 시장 점유율을 차지할 전망

북미는 주요 시장 플레이어의 존재, 제품 승인 증가, 개발 된 의료 시스템 및 급성 호흡곤란 증후군의 높은 유병률로 인해 글로벌 ARDS 치료 시장을 지배했습니다.

2022년 2월 미국 국립의학도서관에 발표된 '급성 호흡곤란 증후군'이라는 제목의 연구에 따르면, 미국에서 ARDS의 발생률은 연간 10만 명당 64.2-78.9건이라고 보고되었습니다. ARDS 사례에 대한 초기 평가에서는 25%가 경증으로, 75%가 중등도 또는 중증으로 분류됩니다. 그러나 경증 사례의 1/3은 중등도 또는 중증 질환으로 발전합니다. 따라서 미국에서 급성 호흡곤란 증후군의 유병률이 증가함에 따라 예측 기간 동안 시장 성장이 뒷받침됩니다.

주요 시장 진출기업의 다양한 다양한 유기적 및 무기적 전략 채택은 시장 성장을 가속화 할 것으로 예상됩니다. 예를 들어, 2020년 12월 미국 식품의약국(FDA)은 코로나바이러스 감염증(COVID-19)으로 인한 급성 호흡곤란증후군(ARDS) 치료를 위해 레메스템셀-L을 패스트 트랙으로 지정했습니다. 또한, 2020년 9월에는 멀티스템 세포 치료제가 미국 식품의약국으로부터 급성 호흡곤란증후군(ARDS) 프로그램에 대한 재생의료 첨단치료제(RMAT) 지정을 받았다고 발표했습니다.

따라서 위의 모든 요인들 덕분에 시장은 높은 성장을 나타낼 것으로 기대됩니다.

급성 호흡곤란 증후군 치료 산업 개요

세계의 급성 호흡곤란 증후군 시장은 경쟁이 치열하며 소수의 선도 기업으로 구성되어 있습니다. Faron Pharmaceuticals, BioMarck Pharmaceuticals, GE Healthcare, Hamilton Company 등의 기업은 급성 호흡곤란 증후군 시장에서 상당한 시장 점유율을 차지합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 급성 호흡곤란 증후군의 유병률 증가

- 흡연, 도시화 및 오염 수준 증가의 높은 유병률

- 노인 인구 증가

- 시장 성장 억제요인

- 불리한 환급 시나리오

- 치료와 관련된 합병증 및 높은 장치 및 치료 비용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 치료별

- 약제 클래스별

- 혈관 수축제

- 기관지 확대약

- 스트로이드 및 항생제

- 진정 및 마비약

- 계면활성제

- 기타

- 디바이스

- 약제 클래스별

- 최종 사용자별

- 병원 및 클리닉

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Faron Pharmaceuticals

- BioMarck Pharmaceuticals

- GE Healthcare

- Hamilton Company

- Athersys

- United Therapeutics

- Apeptico Forschung

- Fisher & Paykel Healthcare Limited

- NRx Pharmaceuticals, Inc.

- HEALIOS KK

- Dragerwerk AG & Co. KGaA

- ALung Technologies, Inc(LivaNova PLC)

제7장 시장 기회와 앞으로의 동향

HBR 25.05.13The Global Acute Respiratory Distress Syndrome Treatment Market size is estimated at USD 3.44 billion in 2025, and is expected to reach USD 4.53 billion by 2030, at a CAGR of 5.65% during the forecast period (2025-2030).

According to the clinical data of COVID-19 patients with severe infection, radiologic evidence of lung edema shows that symptoms of Acute Lung Injury (ALI) can progress to hypoxemia and possibly ARDS in COVID-19 patients. According to the study titled "Acute respiratory distress syndrome in COVID-19: possible mechanisms and therapeutic management" published in the Pneumonia in December 2021, about one-third or (33%) of hospitalized patients experience ARDS. Additionally, ARDS is present in almost 3/4 (or 75%) of COVID-19 patients admitted to the intensive care unit. ARDS patients with COVID-19 have a poor prognosis and a high mortality rate. Thus, the acute respiratory distress market has been significantly impacted by COVID-19.

The market for acute respiratory distress syndrome (ARDS) is being driven by factors such as the rising prevalence and incidence of acute lung injury, a wide range of ARDS risk factors, and an increase in the number of patients with COVID-19 who have ARDS. The global market for acute respiratory distress syndrome (ARDS) is also expected to grow as a result of factors such as the prevalence of diseases linked to lifestyle choices, air pollution, and accidents that cause ARDS. According to the study titled "Acute respiratory distress syndrome: Epidemiology, pathophysiology, pathology, and etiology in adults" by Mark D Siegel published in June 2022, around 190,000 ARDS cases are reported annually in the United States. The incidence rose with patient age, rising from 16 per 100,000 person-years for those aged 15 to 19 to 306 per 100,000 person-years for those aged 75 to 84. Moreover, the growing geriatric population supports market growth. For instance, as per United Nations Department of Economic and Social Affairs report titled 'World Population Ageing 2020 Highlights' mentioned that there were 727 million persons aged 65 years or over in the world in 2020. It is expected that the population is more than double and reaches nearly 1.5 billion in 2050. Since the older population is at high risk of getting respiratory and other illnesses, it is expected to generate the need for treatment, thereby driving the market's growth.

Furthermore, increasing healthcare spending and market participants' strategic initiatives present a growth opportunity for the global acute respiratory distress syndrome (ARDS) market. For Instance, In June 2020, NeuroRx, in partnership with Relief Therapeutics, announced that the United States Food and Drug Administration awarded Fast Track designation to NeuroRx for the investigation of RLF-100 (Aviptadil) for the treatment of acute lung injury/acute respiratory distress syndrome associated with COVID-19. Additionally, in November 2020, Novartis declared that it had entered into an exclusive worldwide license and collaboration agreement with Mesoblast to develop, market, and manufacture remestemcel-L to treat acute respiratory distress syndrome.

Thus, all aforementioned factors are expected to boost the market growth over the forecast period, However, high costs associated with the treatment and devices and regulatory complication may restraint the market growth.

Acute Respiratory Distress Syndrome Treatment Market Trends

Hospital/ Clinics by End User Segment is Expected to Witness Healthy Growth Over the Forecast Period

Hospitals/Clinics are well equipped with advanced technological equipment for surgical procedures and improved treatments and the hospital segment is witnessing rapid growth, owing to the growing number of hospital admission with the ARDS, the increasing number of patient pools, and the launch of new products by the market players are expected to continue over the forecast period, and thus, driving growth in the segment.

The increasing number of hospitals by private players is also expected to propel the growth of the market. The American Hospital Association Statistics 2022 published in January 2022 reported that in 2021, there are 2,946 nongovernment not-for-profit community hospitals, and this number increased to 2,960 in 2022 in the United States. As a result, as the number of beds available increases to treat ARDS patients, thus increasing number of hospitals support the segment growth over the forecast period.

The increasing number of hospital admissions and admissions in the critical care unit creates the need the ARDS treatment and thus drives the growth of the market. According to the study titled "Acute respiratory distress syndrome readmissions: A nationwide cross-sectional analysis of epidemiology and costs of care" published in the PLOS One Journal in January 2022,18.4% of patients with acute respiratory distress syndrome underwent rehospitalization. Moreover, as per data released by the Australian Institute of Health and Welfare in May 2022, there are about 11.8 million hospital admission occurred in 2020-21 which is 6.3% more compared to 2019-20. It also reported that out of 11.8 million admissions, 7.0% of hospitalizations involved a stay in the Intensive Care Unit (ICU), 3.8% of hospitalizations involved respiratory disease and 10.3 % of hospitalizations had a separation mode indicating the patient died in the hospital. Such increasing admission in emergency critical care creates the need for ARDS treatment and is thus expected to drive the growth of the market segment.

Thus, owing to the above factors the segment is expected to show a healthy growth rate over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America dominated the global ARDS treatment market due to the presence of major market players, an increase in product approvals, a developed health care system, and a high prevalence of acute respiratory distress syndrome.

According to the study titled "Acute Respiratory Distress Syndrome" published in the National Library of Medicine in February 2022, reported the incidence of ARDS in the United States range from 64.2 to 78.9 cases per 100,000 people in a year. Initial assessments of ARDS cases place 25% of cases in the mild category and 75% in the moderate or severe category. But one-third of mild cases go on to develop into moderate or severe illnesses. Thus, the growing prevalence of acute respiratory distress syndrome in the United States supports the market growth over the forecast period.

The key market players' adoption of various organic and inorganic strategies is anticipated to accelerate market growth. For instance, in December 2020, the Food and Drug Administration (FDA) granted Remestemcel-L Fast Track designation for the treatment of acute respiratory distress syndrome (ARDS) brought on by coronavirus disease (COVID-19). Additionally, in September 2020, Athersys announced that MultiStem cell therapy was granted Regenerative Medicine Advanced Therapy (RMAT) designation from the United States Food and Drug Administration for the acute respiratory distress syndrome (ARDS) program.

Thus, owing to all above-mentioned factors the market is expected to witness high growth.

Acute Respiratory Distress Syndrome Treatment Industry Overview

The global acute respiratory distress syndrome market is highly competitive and consists of a few major players. Companies like Faron Pharmaceuticals, BioMarck Pharmaceuticals, GE Healthcare, Hamilton Company, and others, hold a substantial market share in the acute respiratory distress syndrome market. Market players are adopting various strategies such as new product launches, partnerships, and collaborations to remain competitive in the marketplace.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Acute Respiratory Distress Syndrome.

- 4.2.2 High Prevalence of Tobacco Smoking, Urbanization, And Growing Levels of Pollution

- 4.2.3 Growing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Unfavorable Reimbursement Scenario

- 4.3.2 Complications Associated with Treatments and High Cost of Devices and Treatments

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Treatment

- 5.1.1 By Drug Class

- 5.1.1.1 Vasoconstrictor

- 5.1.1.2 Bronchodilators

- 5.1.1.3 Streoid and Antibiotics

- 5.1.1.4 Sedative and Paralytic

- 5.1.1.5 Surfactant

- 5.1.1.6 Other

- 5.1.2 Devices

- 5.1.1 By Drug Class

- 5.2 By End User

- 5.2.1 Hospitals/Clinics

- 5.2.2 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Faron Pharmaceuticals

- 6.1.2 BioMarck Pharmaceuticals

- 6.1.3 GE Healthcare

- 6.1.4 Hamilton Company

- 6.1.5 Athersys

- 6.1.6 United Therapeutics

- 6.1.7 Apeptico Forschung

- 6.1.8 Fisher & Paykel Healthcare Limited

- 6.1.9 NRx Pharmaceuticals, Inc.

- 6.1.10 HEALIOS K.K

- 6.1.11 Dragerwerk AG & Co. KGaA,

- 6.1.12 ALung Technologies, Inc ( LivaNova PLC)