|

시장보고서

상품코드

1692522

산업용 정적 장비 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Industrial Static Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

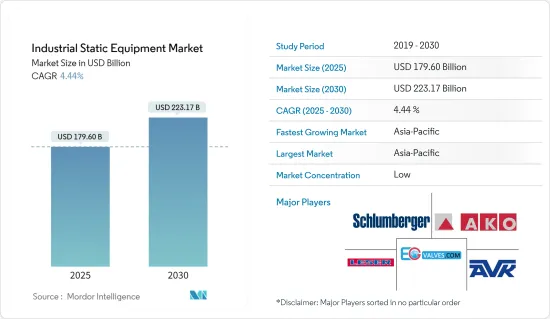

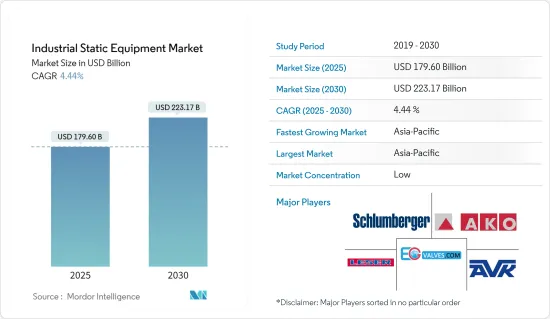

산업용 정적 장비 시장 규모는 2025년에 1,796억 달러로 추정되고, 2030년에는 2,231억 7,000만 달러에 달할 것으로 예측되고, 예측기간(2025-2030년)의 CAGR은 4.44%를 나타낼 전망입니다.

원유 및 기타 탄화수소의 전 세계적인 생산이 눈부시게 발전하면서 석유와 가스의 탐사 및 정제가 증가했습니다.

주요 하이라이트

- 본 조사에 게재되고 있는 시장 수치는 밸브, 용광로, 보일러, 열교환기, 압력 용기 등 유형별 정적 산업 장비의 전체 판매량을 나타냅니다.

- 식음료 산업도 정적 장비에 대한 수요가 더욱 증가할 것으로 예상되는 주요 산업 중 하나입니다.

- 석유 및 가스 산업은 전체 석유 탐사 및 생산 활동이 여러 장소에서 수행되는 여러 공정을 포함하기 때문에 보일러, 용광로, 배관 및 밸브와 같은 정적 산업 장비의 주요 소비자 중 하나입니다.

- COVID-19의 발발은 산업 부문의 성장에 주목할 만한 영향을 미쳤고, 이는 연구 대상 시장의 성장에도 영향을 미쳤습니다.

산업용 정적 장비 시장 동향

급속한 산업화가 시장 성장을 견인

- 산업 부문은 산업 혁명이 시작된 이래로 세계 경제 번영의 원동력이 되어 왔습니다.

- 보일러, 밸브, 열교환기, 용광로 등과 같은 정적 산업 설비는 산업 시설 내에서 운영 목표를 달성하는 데 중추적인 역할을 하는 만큼, 산업 부문 성장과 직접적인 상관관계를 고려할 때 유사한 성장 패턴을 보일 것으로 예상됩니다.

- 산업 부문은 미국, 중국, 일본 등 주요 경제 선진국의 중추적인 역할을 해왔습니다. 예를 들어, 유엔 통계국(UNSD)의 자료에 따르면 미국, 일본, 독일의 GDP에서 제조업이 차지하는 부가가치는 각각 2조 2,272억 달러, 1조 3,036억 달러, 6,973억 달러에 달합니다. 이들 국가가 산업 부문을 강화하기 위해 투자를 늘리고 지원 규정을 마련하고 있기 때문에 예측 기간 동안 정적 산업 장비에 대한 수요도 더욱 증가할 것으로 예상됩니다.

- 또한 아시아태평양 지역은 유리한 정부 규제, 많은 인구, 저렴한 노동력으로 인해 글로벌 기업이이 지역에 기반을 구축하도록 유도함에 따라 산업 부문 성장의 선두 주자가 될 것으로 예상됩니다. 중국, 대만, 인도 등의 국가는 글로벌 기업들이 가장 선호하는 국가 중 하나입니다. 예를 들어, 인도 산업 및 내부 무역 촉진부(DPIIT)에 따르면 2021-2022년에 인도가 유치한 외국인 직접투자(FDI)는 총 587억 7,000만 달러로, 이 중 자동차 산업은 328억 4,000만 달러, 화학 제조 부문은 194억 5,000만 달러의 FDI를 받았습니다. 의약품 및 제약 산업이 받은 FDI는 194억 1천만 달러에 달했습니다.

아시아태평양이 가장 급성장하는 시장이 될 전망

- 아시아태평양 시장은 투자 증가, 인프라 개선 및 LNG 탐사 촉진을 위한 정부 조치 증가, 중국과 인도 등 성장하는 국가에서 활동하는 주요 기업의 존재로 인해 빠르게 발전할 것으로 예상됩니다. 예를 들어, 2021년 1월 구루그람 메트로폴리탄 개발청(GMDA)은 바사이와 단와푸르 주변 10곳에서 물 관리 기술 시범 프로젝트를 시작했습니다. 이 프로젝트의 목표는 도시의 지하 물탱크의 흐름을 모니터링, 제어 및 조절하는 것입니다.

- 중국은 석유 및 가스 탐사에 대한 지출로 인해 아시아태평양 지역에서 석유 및 가스 생산의 선구자입니다. 중국은 가장 많은 석유 굴착 장치를 보유하고 있으며, 그 뒤를 이어 인도도 꾸준히 발전하고 있습니다. 또한, 여러 국가에서 여러 기관이 장비 성능을 향상시키고 업계에 대한 투자를 장려하기 위해 연구 개발 노력을 진행하고 있습니다.

- 아시아태평양에는 세세계 주요 체크 밸브 제조업체의 본거지입니다. 보다 안전한 애플리케이션에 대한 수요 증가와 자동 밸브와 관련된 R&D 노력 증가는 아시아태평양 지역의 산업 발전을 촉진하는 중요한 요인입니다. 또한 산업 연구를 통해 특히 중국에서 에너지 및 전력, 화학을 비롯한 여러 분야에서 밸브의 적용 범위가 넓어졌습니다. 체크 밸브는 에너지 및 전력, 석유 및 가스, 수처리 및 폐수 처리 부문에서 네트워크 전체의 매체 흐름을 조절하고, 이동을 시작, 중지 또는 제어하며 안전하고 효과적인 처리 자동화를 제공하기 위해 사용됩니다.

- 이 지역의 집중된 인구, 상당한 소비자 소득, 대규모 산업, 도시화 증가는 이 지역의 산업용 밸브 확장을 이끄는 중요한 동인입니다. 인도, 중국, 동남아시아 국가들은 이 지역에서 빠르게 성장하는 경제 국가 중 하나입니다. 이 지역의 대도시 인구가 증가함에 따라 현대적이고 향상된 폐수 처리 시설에 대한 수요가 크게 증가하고 있습니다.

- 향상된 물 및 폐수 관리 기술에 대한 수요 증가, 폐수 처리를 위한 정부 노력 증가, 적절한 물 사용에 대한 필요성 증가로 인해 아시아태평양 지역에서 정적 장비에 대한 수요가 증가하고 있습니다.

산업용 정적 장비 산업 개요

산업용 정적 장비 시장은 적당히 높을 것으로 예상되며 예측 기간 동안 동일하게 유지됩니다.

- 2022년 7월, Alfa Laval이 스웨덴의 글로벌 철강 기업인 SSAB와 협력하여 세계 최초로 화석연료를 사용하지 않는 강철로 만든 열교환기를 개발 및 상용화했습니다.

- 2022년 3월, AVK 그룹이 프리미엄 100 게이트 밸브의 새로운 라인업을 발표. 긴 수명과 최대한의 안전성이 요구되는 장소에의 설치에 최적입니다.이것에는 교통량이 많은 도로, 공공시설이나 관광지, 연안 지역, 기름이나 가솔린으로 오염된 지역 등이 포함됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 기술 동향

- 산업 밸류체인 분석

- 시장에 대한 COVID-19의 영향

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자 및 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 급속한 산업화

- 석유 및 가스 탐사 활동 증가

- 시장 성장 억제요인

- 높은 투자 비용과 재생 가능 에너지 발전 원으로의 전환

제6장 시장 세분화

- 유형별

- 밸브

- 게이트, 글러브, 체크

- 볼 밸브

- 버터 플라이

- 플러그

- 압력 릴리프

- 용광로 및 보일러

- 열교환기

- 압력 용기

- 밸브

- 최종 사용자 산업별

- 석유 및 가스

- 발전

- 화학 및 석유 화학

- 상하수도

- 기타 공정 산업

- 기타 개별 산업

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일 : 밸브

- Schlumberger Limited

- AKO Armaturen & Separationstecchink GMBH

- AVK Group

- EG Valves

- Leser GMBH & CO. KG

- Baker Hughes Company

- Emerson Electric CO.

- Flowserve Corporation

- 기업 프로파일 : 열교환기

- Alfa Laval AB

- API Heat Transfer

- Danfoss A/S

- General Electric Company

- Hisaka Works Ltd

- HRS Heat Exchangers

- Johnson Controls International PLC

- 기업 프로파일 : 압력 용기

- Doosan Mecatec (Doosan Corporation)

- IHI Power Services Corp.(IHI Corporation)

- Mitsubishi Heavy Industries Ltd

- Hitachi Zosen Corporation

- Japan Steel Works Ltd

- Shanghai Electric Group Company Limited

- CIMC Enric Holdings Limited

- 기업 프로파일 : 용광로 및 보일러

- Viessmann Group

- Lennox International Inc.

- Baxi(BDR Thermea Group)

- The Fulton Companies

- Worcester Bosch Group(the Bosch Group)

- Ideal Boilers(ideal Heating)

- Burnham Commercial Boilers

제8장 시장 전망

HBR 25.05.13The Industrial Static Equipment Market size is estimated at USD 179.60 billion in 2025, and is expected to reach USD 223.17 billion by 2030, at a CAGR of 4.44% during the forecast period (2025-2030).

The exploration and refining of oil and gas have increased due to the remarkable progress made in the worldwide production of crude oil and other hydrocarbons. With the massive industrialization and urbanization that has resulted from the revolution in a variety of industries, including the automobile, pharmaceutical, telecommunication, and manufacturing, petroleum is now a crucial component of development.

Key Highlights

- The market numbers provided in the study indicate the overall sales of static industrial equipment across types, such as valves, furnaces/boilers, heat exchangers, and pressure vessels. The further market is also segmented into an end-user industry which indicates the sales of several types of static industrial equipment across several industries such as oil and gas, Power generation, Chemical & petrochemical, Water & Wastewater, Other Process industries, and other discrete industries.

- The food and beverage industry is also among the major industries wherein the demand for static equipment is expected to grow further. The increasing consumption of processed and packaged foods globally is one of the major contributors to the growth of the industry. According to the US Census Bureau, total sales for retail and food services from May 2022 through July 2022 were up by 9.2% from the same period last year.

- The oil and gas industry has been among the key contributors to the growth of almost all industries. This was due to the fact that power is required to run any industrial establishment, and until the recent developments in renewable sources, power was used to be fulfilled primarily by oil and gas.

- The oil and gas industry is among the major consumers of static industrial equipment, such as boilers, furnaces, piping, and valves, as the entire oil exploration and production activity involves several processes that are carried out at different places.

- The outbreak of COVID-19 has had a notable impact on the growth of the industrial sector, which in turn impacted the growth of the studied market. According to Eurostat, industrial production in the European Union declined by 7% in 2020. The decline in production activities has had an adverse impact on the demand for major industrial static equipment as major industries put a hold on future expansion activities and investment in establishing new facilities.

Industrial Static Equipment Market Trends

Rapid Industrialization Drives the Market Growth

- The industrial sector has been an engine for the world's economic prosperity since the onset of the industrial revolution. According to the World Bank, the estimated value added by the manufacturing sector to the global economy was around 17.01% in 2021. The growing demand for manufactured products and the role the industrial sector plays in stimulating the growth of other sectors through its outputs are expected to drive the development of the industrial sector during the forecast period.

- As static industrial equipment such as boilers, valves, heat exchangers, furnaces, etc. plays a pivotal role within the industrial establishments to help them achieve their operational targets, they are also expected to follow a similar growth pattern considering their direct co-relation with the industrial sector growth.

- The industrial sector has been the backbone of major economically developed countries such as the United States, China, Japan, etc. For instance, according to the data provided by the United Nations Statistics Division (UNSD), the value added by the manufacturing industry to the GDP of the United States, Japan, and Germany amounted to USD 2,272 billion, USD 1.033.6 billion, and USD 697.3 billion, respectively. As these countries are increasingly investing and framing supportive regulations to bolster the industrial sector, the demand for static industrial equipment is also expected to grow further during the forecast period.

- Additionally, the Asia-Pacific region is expected to be the leader in industrial sector growth, as the favorable government regulations, large populations, and the availability of low-cost labor attract global players to set up their base in the region. Countries like China, Taiwan, India, etc., have been among the favorite destinations of global companies. For instance, According to the Department for Promotion of Industry and Internal Trade (DPIIT), the total foreign direct investment (FDI) received by India in the financial years 2021-22 stood at USD 58.77 billion, of which the automotive industry received FDI worth USD 32.84, chemical manufacturing sector received USD 19.45 billion. The FDI received by the drug and pharmaceutical industry amounted to USD 19.41 billion.

- A similar trend has been observed across other countries as well. For instance, in September 2022, The Malaysian Investment Development Authority (MIDA) announced that the government has attracted approved investment worth USD 27.5 billion in its manufacturing, services, and primary sectors in the first half of 2022.

Asia Pacific is Expected to be the Fastest Growing Market

- The Asia Pacific market is predicted to develop rapidly due to increased investment, increased government measures to enhance infrastructures and promote LNG exploration, and the existence of important firms operating in growing countries, including China and India, in this area. For instance, in January 2021, the Gurugram Metropolitan Development Authority (GMDA) began a trial project for its water management technology in around ten places around Basai and Dhanwapur. The project's goal is to monitor, control, and regulate the flow of the city's underground water tanks. In the subterranean tanks, a flow control valve, an ultrasonic fluid flow meter, and a level meter will be installed as part of the project.

- China is the pioneer in oil & gas production in Asia-Pacific because of its oil & gas exploration expenditure. The nation has the most oil rigs, followed by India, which has also made steady improvements. Furthermore, numerous institutes are conducting research and development initiatives in several nations to increase equipment performance and encourage investment in the industry. For instance, in March 2022, China intends to invest CNY 81.5 billion in upstream exploitation, particularly in the crude oil foundations in the Shunbei and Tahe areas and natural gas resources in Sichuan province and the Interior Mongolia region. Increasing demand for oil & gas exploration will increase the demand for static equipment, boosting the market growth.

- The Asia Pacific area is home to several of the world's major check valve manufacturers. Increasing demand for safer applications and increased R&D efforts linked to automatic valves are some significant factors fueling industry development in the Asia Pacific. Furthermore, industrial research has widened the applicability of valves in many sectors, including energy & power, and chemicals, notably in China. Check valves are employed in the energy & power, oil & gas, and water & wastewater treatment sectors to regulate medium flow throughout the network, commence, stop, or control the movement, and provide secure and effective processing automation.

- The region's concentrated populace, significant consumer income, large-scale industry, and increasing urbanization are important drivers driving the region's industrial valve expansion. India, China, and Southeast Asian countries are among the region's fast-growing economies. Because of the region's growing metropolitan population, there is a strong need for modern and enhanced wastewater treatment facilities.

- The increasing demand for enhanced water and wastewater management techniques, rising government initiatives for treating wastewater, and the growing necessity for appropriate water usage are driving the need for static equipment in the Asia-Pacific region.

Industrial Static Equipment Industry Overview

Industrial Static Equipment Market is expected to be moderately high and remains the same over the forecast period. Major companies like Schlumberger Limited, AKO Armaturen& Separationstecchink GMBH, AVK Group, EG Valves LeserGMBH & CO. KG are also making partnerships and launching new products to retain their market position.

- July 2022 - Alfa Laval collaborated with SSAB, the global Swedish steel company, on developing and commercializing the world's first heat exchanger made of fossil-free steel. The goal is to have the first hydrogen-reduced steel unit ready by 2023. The collaboration is also a significant step toward Alfa Laval's goal of becoming carbon neutral by 2030.

- March 2022 - AVK Group launched a new line of premium 100 gate valves. Premium 100 gate valves offer corrosion and wear resistance. They are ideal for installation in locations where excavation is not feasible and where long life and maximum safety are required. This could include busy roads, public and tourist attractions, coastal areas, or areas contaminated with oil or gasoline.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on The Market

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Industrialization

- 5.1.2 Increasing Oil and Gas Exploration Activities

- 5.2 Market Restraints

- 5.2.1 High Investment Cost and Shift Toward Renewable Energy Generation Sources

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Valves

- 6.1.1.1 Gate, Globe, and Check

- 6.1.1.2 Ball Valves

- 6.1.1.3 Butterfly

- 6.1.1.4 Plug

- 6.1.1.5 Pressure Relief

- 6.1.2 Furnaces/Boilers

- 6.1.3 Heat Exchangers

- 6.1.4 Pressure Vessels

- 6.1.1 Valves

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Power Generation

- 6.2.3 Chemicals and Petrochemicals

- 6.2.4 Water and Wastewater

- 6.2.5 Other Process Industries

- 6.2.6 Other Discrete Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles - Valves

- 7.1.1 Schlumberger Limited

- 7.1.2 AKO Armaturen & Separationstecchink GMBH

- 7.1.3 AVK Group

- 7.1.4 EG Valves

- 7.1.5 Leser GMBH & CO. KG

- 7.1.6 Baker Hughes Company

- 7.1.7 Emerson Electric CO.

- 7.1.8 Flowserve Corporation

- 7.2 Company Profiles - Heat Exchangers

- 7.2.1 Alfa Laval AB

- 7.2.2 API Heat Transfer

- 7.2.3 Danfoss A/S

- 7.2.4 General Electric Company

- 7.2.5 Hisaka Works Ltd

- 7.2.6 HRS Heat Exchangers

- 7.2.7 Johnson Controls International PLC

- 7.3 Company Profiles - Pressure Vessels

- 7.3.1 Doosan Mecatec (Doosan Corporation)

- 7.3.2 IHI Power Services Corp. (IHI Corporation)

- 7.3.3 Mitsubishi Heavy Industries Ltd

- 7.3.4 Hitachi Zosen Corporation

- 7.3.5 Japan Steel Works Ltd

- 7.3.6 Shanghai Electric Group Company Limited

- 7.3.7 CIMC Enric Holdings Limited

- 7.4 Company Profiles - Furnaces/Boilers

- 7.4.1 Viessmann Group

- 7.4.2 Lennox International Inc.

- 7.4.3 Baxi (BDR Thermea Group)

- 7.4.4 The Fulton Companies

- 7.4.5 Worcester Bosch Group (the Bosch Group)

- 7.4.6 Ideal Boilers (ideal Heating)

- 7.4.7 Burnham Commercial Boilers