|

시장보고서

상품코드

1692581

중동 및 아프리카의 건축용 접착제 및 실란트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Middle East & Africa Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

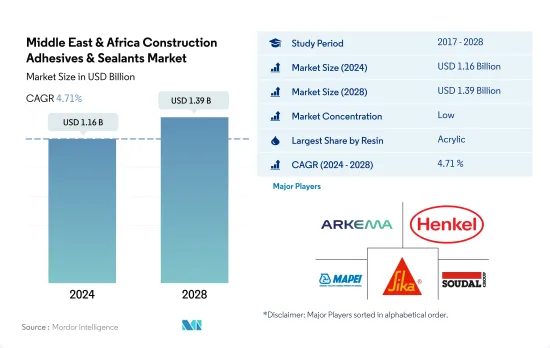

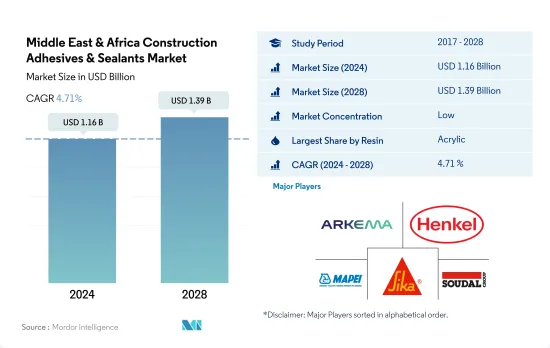

중동 및 아프리카 건축용 접착제 및 실란트 시장 규모는 2024년에 11억 6,000만 달러로 추정되고, 2028년에는 13억 9,000만 달러에 이르를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR 4.71%로 성장할 것으로 예측됩니다.

사우디아라비아의 접착제 및 실란트 소비 증가로 향후 몇 년 동안에도 소비량 1위 자리를 유지할 전망

- 폴리우레탄 및 아크릴 수지 기반 접착제 및 실란트는 2017-2021년에 다른 수지 유형 중에서 가장 많이 사용되었습니다. 이들은 강력한 결합력과 구조용 접착제로서의 적용 가능성으로 인해 예측 기간(2022-2028년) 동안 가장 많이 사용되는 수지 유형이 될 것으로 예상됩니다.

- 중동 및 아프리카 지역의 2020년 건축용 접착제 및 실란트에 대한 전반적인 수요 감소는 코로나19 팬데믹으로 인해 전국적인 봉쇄, 공급망 중단, 사회적 거리두기 의무 규정 등으로 인한 지역 내 전반적인 경기 침체에 기인한 것으로 볼 수 있습니다.

- 중동 및 아프리카에서는 2017-2021년 동안 건축용 접착제 및 실란트에 대한 수요가 예측 기간(2022-2028년) 동안 4%의 연평균 성장률로 증가했습니다. 수요는 6%의 비율로 증가할 것으로 예상됩니다.

- 사우디아라비아는 건축용 접착제 및 실란트에 대한 전 세계 수요에서 가장 큰 비중을 차지했습니다.

이 지역의 친환경 건물 건설 활동 증가가 성장에 크게 기여할 것으로 예상

- 2020년 건설 생산량이 4.4% 감소한 것은 코로나19 팬데믹으로 인해 전국적인 봉쇄, 공급망 중단, 사회적 거리두기 의무 규정 등이 발생했기 때문입니다.

- 2021년에는 중동 및 아프리카의 건설 활동 증가로 인해 건축용 접착제 및 실란트에 대한 수요가 증가했습니다. 사우디아라비아는 5,000억 달러 규모의 미래형 메가시티 '네옴' 프로젝트, 2022년 완공 예정인 홍해 프로젝트 1단계, 5개 섬에 걸쳐 3,000개의 객실을 갖춘 초호화 호텔, 2개의 내륙 리조트, 키디야 엔터테인먼트 시티, 초호화 웰니스 관광지인 아마알라 등 다양한 건설 프로젝트를 시행하고 있습니다. 이러한 프로젝트는 예측 기간 동안 건축용 접착제 및 실란트에 대한 수요를 견인할 것으로 보입니다.

- 중동 및 아프리카 지역도 향후 몇 년 동안 전 세계 친환경 건물의 성장에 중요한 역할을 할 것으로 예상됩니다. MENA 지역 네트워크의 그린 빌딩 협의회는 이 지역의 건물이 사람들에게 높은 삶의 질을 제공하고 환경에 미치는 부정적인 영향을 최소화하며 경제적 이익을 극대화할 수 있도록 현장의 도전과 기회에 대응하고 있습니다. 따라서 친환경 건물 건설 활동이 증가함에 따라 중동 및 아프리카 접착제 및 실란트 시장은 2022-2028년 예측 기간 동안 볼륨 기준 3.4%, 가치 기준 5.01%의 연평균 성장률을 기록할 것으로 예상됩니다.

중동 및 아프리카 건축용 접착제 및 실란트 시장 동향

건설 산업 활성화를 위한 탄탄한 인구와 우호적인 정부 정책

- 건설 산업은 아프리카 경제의 핵심 동력이 되고 있으며 GDP의 10-15%를 차지합니다.

- 건설 산업은 2018년과 2019년에 각각 2.38%와 2.32%의 성장률을 기록했습니다. 그러나 2020년에는 코로나19 팬데믹으로 사우디아라비아, 아랍에미리트 등의 국가에서 건설 활동이 제한되면서 건설 시장이 2019년 같은 기간에 비해 6.81% 위축되었습니다. 2021년에는 중동과 아프리카 국가들이 코로나19 확산을 잘 통제하면서 건설 시장이 성장률을 회복했습니다.

- 중동 및 북아프리카(MENA)에는 현재 3억 5,000만명 이상이 살고 있으며, 그 인구 증가는 급속한 도시화가 특징입니다. 이는 건물에 대한 수요가 많다는 것을 의미하며, 분쟁으로 인한 인구 이동이라는 난제 때문에 더욱 복잡해집니다. 따라서 중동 및 아프리카 건설 산업은 예측 기간(2022-2028년) 동안 2.7%의 연평균 성장률(CAGR)로 증가할 것으로 예상됩니다.

중동 및 아프리카 건축용 접착제 및 실란트 산업 개요

중동 및 아프리카 건설 접착제 및 실란트 시장은 세분화되어 있으며 상위 5개 기업이 18.51%를 점유하고 있습니다. 이 시장의 주요 업체는 Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG 및 Soudal Holding N.V.(알파벳순)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 건축 및 건설

- 규제 프레임워크

- 사우디아라비아

- 남아프리카

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 수지

- 아크릴

- 시아노아크릴레이트

- 에폭시

- 폴리우레탄

- 실리콘

- VAE 및 EVA

- 기타

- 기술

- 핫멜트

- 반응성

- 실란트

- 용매

- 수성

- 국가명

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Arkema Group

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- MAPEI SpA

- Sika AG

- Soudal Holding NV

- Wacker Chemie AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 억제요인, 기회

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Middle East & Africa Construction Adhesives & Sealants Market size is estimated at 1.16 billion USD in 2024, and is expected to reach 1.39 billion USD by 2028, growing at a CAGR of 4.71% during the forecast period (2024-2028).

Saudi Arabia's growing consumption of adhesives & sealants to maintain its position at the top in terms of consumption even for the next few years

- Polyurethane and acrylic resin-based adhesives and sealants were the most used among other resin types in 2017-2021. They are expected to be the most used resin types during the forecast period (2022-2028) because of their strong bonds and their applicability as structural adhesives. In the Middle East and Africa, 67% of acrylic-based construction adhesives are manufactured in water-borne technology, and polyurethane-based products are manufactured majorly in sealant technology.

- In the Middle East & Africa region, the decrease in overall demand for construction adhesives and sealants in 2020 can be attributed to the overall economic slowdown in the region caused due to COVID-19 pandemic, which led to nationwide lockdowns, supply chain disruption, mandatory social distancing regulations, etc. Thus, the construction adhesives and sealants contracted by 7.04%% in 2020. It was restored by 5.22% in 2021.

- In the Middle East and Africa, during the historic period (2017-2021), demand for construction adhesives and sealants increased by a CAGR of 4% during the forecast period (2022-2028). The demand is expected to increase at a rate of 6%. Among all the resin types, silicone resin-based adhesives and sealants are expected to register the largest CAGR of around 6% during the forecast period (2022-2028).

- Saudi Arabia occupied the largest share of the global demand for construction adhesives and sealants. In 2021, the demand generated from Saudi Arabia was 81.6 million kilograms. In 2028, the demand is expected to reach 100.6 million kilograms with a CAGR of 6.9%. Polyurethane, acrylic, and silicon resin-based adhesives and sealants products are expected to occupy more than 50% of the total demand generated by the Saudi Arabian construction industry in 2022.

A major boost to the growth forecasted to be contributed by the rising green building construction activities in the region

- In 2020, the decline in construction output by 4.4% was due to the COVID-19 pandemic, which led to nationwide lockdowns, supply chain disruption, mandatory social distancing regulations, etc. These factors led to declining demand for adhesives and sealants required for construction in 2020. The decline was the highest in South Africa because of the country's construction market decline.

- The demand for construction adhesives and sealants grew in 2021 because of the rising construction activities in Middle East & Africa. Saudi Arabia has implemented various construction projects, including a USD 500 billion futuristic mega-city 'Neom' project, the Red Sea Project - Phase 1, which is due to be completed in 2022, and luxury and hyper-luxury hotels that may comprise 3,000 rooms across five islands, and two inland resorts, Qiddiya Entertainment City, and Amaala - the uber-luxury wellness tourism destination. Such projects are likely to drive the demand for construction adhesives and sealants over the forecast period.

- The Middle East & Africa region is also set to be critical for the growth of green buildings globally over the next few years. Green Building Councils in the MENA Regional Network are responding to challenges and opportunities on the ground, ensuring that the region's buildings provide a high quality of life for people, minimize negative impacts on the environment, and maximize economic benefits. Thus, due to rising green building construction activities, the Middle East & African adhesives and sealants market is projected to record a CAGR of 3.4% by volume and 5.01% by value during the forecast period 2022-2028.

Middle East & Africa Construction Adhesives & Sealants Market Trends

Robust population and favorable government policies to boost the construction industry

- The construction industry is becoming a key driver for African economies, accounting for 10-15% of GDP. Development in the region is attracting investment from all over the world, which is further creating opportunities and boosting the workforce in the construction of residential, commercial, institutional, and industrial buildings.

- The construction industry registered a growth rate of 2.38% and 2.32% in 2018 and 2019, respectively. However, in 2020, the construction market contracted by 6.81% compared to the same period in 2019, as the COVID-19 pandemic negatively affected the construction market by restricting construction activities in countries like Saudi Arabia and the United Arab Emirates. In 2021, the construction market regained growth rate as the Middle East and African nations have done well in controlling the COVID-19 outbreak. As a result, key construction sectors recorded moderate growth, unlike other comparable markets which have witnessed low to negative growth.

- The Middle East and North Africa (MENA) is currently home to over 350 million people, and its population growth has been characterized by rapid urbanization. This is projected to continue, with the urban population expected to double from 2010 to 2050, from 200 million to nearly 400 million. This means a large demand for buildings, complicated by the challenges of conflict-induced displacement of people. Thus, the Middle East & Africa Construction industry is expected to increase at a CAGR of 2.7% during the forecast period (2022-2028).

Middle East & Africa Construction Adhesives & Sealants Industry Overview

The Middle East & Africa Construction Adhesives & Sealants Market is fragmented, with the top five companies occupying 18.51%. The major players in this market are Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Saudi Arabia

- 4.2.2 South Africa

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema Group

- 6.4.2 Dow

- 6.4.3 H.B. Fuller Company

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Huntsman International LLC

- 6.4.6 Illinois Tool Works Inc.

- 6.4.7 MAPEI S.p.A.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms