|

시장보고서

상품코드

1692585

중동 및 아프리카의 차량용 접착제 및 실란트 시장 : 점유율 분석, 산업 동향, 통계, 성장 동향 예측(2025-2030년)Middle East & Africa Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

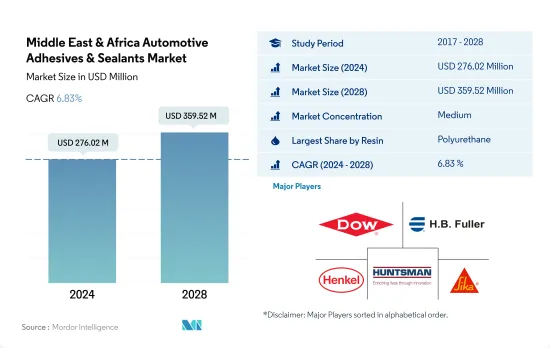

중동 및 아프리카의 차량용 접착제 및 실란트 시장 규모는 2024년에 2억 7,602만 달러로 추정되고, 2028년에는 3억 5,952만 달러에 이를 것으로 예측되며, 예측 기간(2024-2028년)의 CAGR은 6.83%를 나타낼 것으로 예측됩니다.

전기자동차의 도입과 수요가 시장 성장의 상승 요인

- 중동 및 아프리카 자동차 산업의 성장은 자동차용 접착제 및 실란트에 대한 수요 증가로 이어졌습니다. 2020년 전 세계 자동차 생산량의 0.58%를 차지한 남아공 등 아프리카 주요 국가의 자동차 생산량이 증가했으며, 2022-2028년 예측 기간 동안 전기자동차 도입 및 수요로 인해 크게 성장할 것으로 예상됩니다.

- 2020년 코로나19 팬데믹은 경기 침체와 가치 사슬 붕괴로 인해 중동과 아프리카의 자동차 산업에 심각한 영향을 미쳤습니다. 그러나 사우디아라비아의 수입 관세 15% 인하, 중동 국가의 유가 하락 등 정부의 정책 지원으로 자동차 수요가 빠르게 회복되면서 2021년에는 차량용 접착제 및 실란트에 대한 수요가 증가했습니다.

- 자동차 산업에서 주로 사용되는 수지는 에폭시계, 폴리우레탄계, 아크릴계로 자동차의 전체 구조를 구성하는 세라믹, 플라스틱, 유리, 금속, 복합재 등 다양한 피착재와 폭넓은 호환성을 갖기 때문에 자동차 산업에서 주로 사용됩니다. 폴리우레탄 수지는 자동차 제조 시 폴리우레탄 반응성(PUR) 접착제로 사용됩니다.

- VAE 및 EVA 접착제는 중동 및 아프리카 자동차 산업에서 가장 빠르게 성장하는 기술입니다. 이러한 접착제는 용매 기반 접착제보다 핫멜트 접착제의 증가 추세로 인해 예측 기간(2022-2028년) 동안 8.24%의 CAGR로 성장할 것으로 예상됩니다.

부피가 큰 금속 프레임을 대체하는 자동차 산업의 기술 개발이 시장 성장을 가속

- 현대자동차와 같은 중동 및 아프리카의 주요 자동차 회사들은 연비 향상과 비용 절감을 위해 차량 경량화를 위해 노력하고 있습니다. 이를 위해 부피가 큰 금속 프레임과 용접 조인트, 나사, 볼트 등의 접합 부품을 대체하기 위해 자동차용 접착제와 실란트가 사용되고 있습니다.

- 2020년 차량용 접착제 및 실란트의 매출과 수요가 급격히 감소한 것은 코로나19 팬데믹의 영향으로 전반적인 경기 침체와 가치 사슬에 혼란을 일으켰기 때문입니다. 아프리카의 승용차 판매량은 2019년 85만 대에서 2020년 65만 대로 감소했습니다.

- 시장 규모는 해당 지역의 1인당 소득과 인구에 따라 결정됩니다. 따라서 인구 통계에 따라 사하라 이남 지역, 북아프리카, 나머지 중동 국가가 75% 이상을 차지하며, 이 지역의 차량 수가 다른 지역보다 더 많습니다. 차량 대수는 차량 제조에 필요한 차량용 접착제 및 실란트의 수와 정비례합니다.

- 남아공은 전 세계 자동차 생산량의 0.58%를 차지하는 이 지역 최대 자동차 제조업체로서 시장 점유율의 거의 5분의 1을 차지하고 있습니다.

중동 및 아프리카의 차량용 접착제 및 실란트 시장 동향

금리와 연료비 감소가 산업 성장을 뒷받침

- 지역 자동차 시장에서 승용차가 차지하는 비중은 해당 지역의 1인당 소득을 나타내는 지표입니다. 자동차 산업의 수익은 2017년부터 2019년까지 아태지역의 경기 침체로 인해 감소했습니다. 그러나 팬데믹 이후 2021년에는 엄청난 성장 잠재력을 기록했습니다. 일본 자동차 제조업체인 도요타가 중동 및 아프리카에서 가장 많은 승용차를 판매하며 시장 점유율 10.2%를 차지했습니다.

- 아랍에미리트, 이란, 사우디아라비아, 쿠웨이트, 카타르, 바레인 등 중동의 원유 부국들은 현재 유럽과 아시아 자동차 제조업체로부터 훨씬 높은 비용을 들여 대부분을 수입하고 있기 때문에 고급 자동차 생산 허브가 되기 위해 노력하고 있습니다. 2019년 중동 지역의 자동차 판매량은 사우디아라비아가 2019년에는 7,257만 2,000대가 되었습니다.

- 코로나19 팬데믹은 주로 아프리카 지역의 자동차 산업에 영향을 미쳤습니다. 이는 아프리카 지역 전체 자동차 시장의 매출 감소로 이어졌습니다.

중동 및 아프리카의 차량용 접착제 및 실란트 산업 개요

중동 및 아프리카의 차량용 접착제 및 실란트 시장은 적당히 통합되어 있으며 상위 5개 기업이 47.51%를 점유하고 있습니다. 이 시장의 주요 업체는 다우, HB 풀러 컴퍼니, 헨켈 AG & Co. KGaA, 헌츠맨 인터내셔널 LLC, 시카 AG(알파벳 순으로 정렬)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 자동차

- 규제 프레임워크

- 사우디아라비아

- 남아프리카

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 수지

- 아크릴

- 시아노아크릴레이트

- 에폭시

- 폴리우레탄

- 실리콘

- VAE 및 EVA

- 기타

- 기술

- 핫멜트

- 반응성

- 실란트

- 용매

- UV 경화형 접착제

- 수성

- 국가명

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- PPG Industries, Inc.

- Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 억제요인, 기회

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Middle East & Africa Automotive Adhesives & Sealants Market size is estimated at 276.02 million USD in 2024, and is expected to reach 359.52 million USD by 2028, growing at a CAGR of 6.83% during the forecast period (2024-2028).

Introduction and demand for electric vehicles in the region to create upswings for market growth

- The growth in the Middle East & African automotive industry has led to the growth of demand for automotive adhesives and sealants. There was an increase in automobile production in major countries of Africa, such as South Africa, which accounted for 0.58% of global vehicle production in 2020 and is expected to grow significantly because of the introduction and demand for electric vehicles in the forecast period 2022-2028. This trend is expected to boost the demand for adhesives and sealants required for automobile manufacture over the forecast period 2022-2028.

- The COVID-19 pandemic in 2020 severely affected the automotive industry in the Middle East and Africa because of economic slowdowns and value chain disruptions. However, government support in the form of policies such as a 15% reduction in import duties in Saudi Arabia and lower fuel prices in Middle East countries led to a rapid recovery in demand for automobiles, which increased the demand for automotive adhesives and sealants in 2021.

- The majorly used resins in the automotive industry are epoxy-based, polyurethane-based, and acrylic-based because of their wide compatibility with different substrates such as ceramics, plastics, glass, metals, and composites, which comprise the overall structure of an automobile. Polyurethane resin is used as polyurethane reactive (PUR) adhesives in manufacturing automobiles.

- VAE/EVA adhesives are the fastest-growing technology in the Middle East & African automotive industry. It is expected that these adhesives will register a CAGR of 8.24% during the forecast period (2022-2028) due to the rising trend of hot-melt adhesives over solvent-borne adhesives.

Technological developments in automotive industry to replace bulky metallic frames to aid market growth

- The major automotive companies in the Middle East & Africa, such as Hyundai, are working on making the vehicles light in weight so as to improve fuel efficiency and as cost-cutting measures. To achieve this, automotive adhesives and sealants are used to replace bulkier metallic frames and joinery components such as welding joints, screws, and bolts. This technology development will lead to an increase in demand for automotive adhesives and sealants in mentioned period of 2022-2028.

- The abrupt reductions in revenue and demand for automotive adhesives and sealants in 2020 are due to the impact of the COVID-19 pandemic, which caused an overall economic slowdown and value chain disruptions. Passenger vehicle sales in Africa decreased from 850,000 vehicular units in 2019 to 650,000 vehicular units in 2020. This growth was recovered in 2021 because of government policies that were meant to support the automotive industry, as it covers the major portion of the GDP of a nation.

- The size of the market is determined by the per capita income and population of the region. So based on demographics, more than 75% is covered by countries in the sub-Sahara region, Northern Africa, and the rest of the Middle East countries, which is a larger number of vehicles in the region than that of the rest. The vehicle's count is directly proportional to the automotive adhesives and sealants required to manufacture the same.

- South Africa contains nearly one-fifth of the market share as it is the largest manufacturer of automobiles in the region, which comprise 0.58% of global automobile production.

Middle East & Africa Automotive Adhesives & Sealants Market Trends

Lower interest rates and fuel rates to aid the industry's growth

- The share of passenger vehicles in a regional automotive market is an indicator of the per capita income in the region. The revenue in the automotive industry declined from 2017 to 2019 owing to a recession in the region. However, post-pandemic, the market recorded tremendous growth potential in 2021. Japanese automobile manufacturer Toyota sold the maximum number of passenger vehicles in the Middle East & Africa, accounting for 10.2% of the market share. The Middle East & African automotive industry is expected to grow in the forecast period 2022-2028 but at a slower pace.

- The crude oil-rich countries in the Middle East, such as UAE, Iran, Saudi Arabia, Kuwait, Qatar, and Bahrain, are trying to become production hubs for luxury cars as currently, they are importing the majority of them from European and Asian automotive manufacturers at significantly higher costs. The sales of automobiles in the Middle East were the highest in Saudi Arabia, amounting to 72,572 thousand units of vehicles in 2019. Car imports dropped by 18.4% in 2018 compared to 2017.

- The COVID-19 pandemic impacted the automotive industry, majorly in the African region. Toyota, the largest market share holder in the region, registered a dip in sales of passenger vehicles from 900 thousand units in 2019 to 620 thousand units in 2020. This led to a decrease in the revenue of the whole automotive market in the region. However, government initiatives such as lower auto interest rates and cheaper fuel rates in the Middle East region are expected to lead to the growth of the automotive sector in the forecast period 2022-2028.

Middle East & Africa Automotive Adhesives & Sealants Industry Overview

The Middle East & Africa Automotive Adhesives & Sealants Market is moderately consolidated, with the top five companies occupying 47.51%. The major players in this market are Dow, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Automotive

- 4.2 Regulatory Framework

- 4.2.1 Saudi Arabia

- 4.2.2 South Africa

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 PPG Industries, Inc.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms