|

시장보고서

상품코드

1693370

프랑스의 접착제 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)France Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

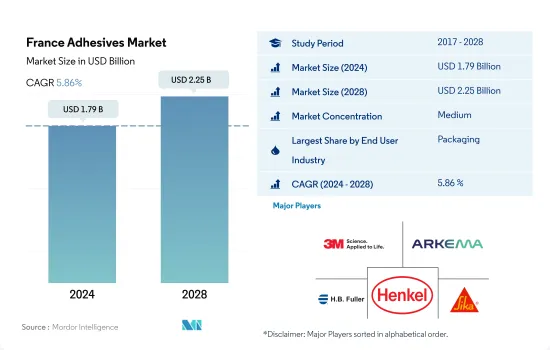

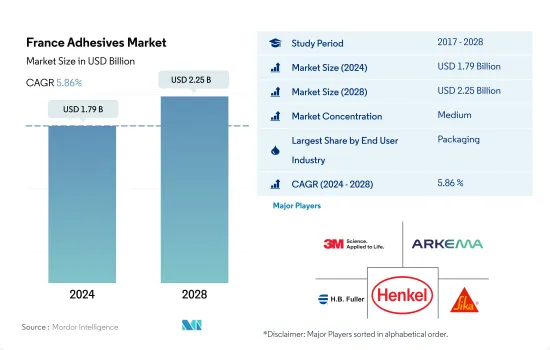

프랑스의 접착제 시장 규모는 2024년에 17억 9,000만 달러로 추정되고, 2028년에는 22억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR은 5.86%를 나타낼 전망입니다.

의료비 지출 증가로 인한 접착제 수요 증가

- 프랑스에서는 포장, 의료, 건설과 같은 최종 사용자 산업이 접착제 시장에서 가장 높은 시장 점유율을 차지하고 있습니다. 프랑스에서 연질 포장은 상당한 성장세를 보였습니다.

- 접착제는 플라스틱, 금속, 종이 및 판지 포장재를 접착하는 데 중요하기 때문에 프랑스 포장 산업에서 주로 소비됩니다. 수성 접착제는 이러한 용도에 필요한 저렴한 비용과 높은 접착 강도로 인해 업계에서 많이 소비되고 있습니다.

- 프랑스에서는 건축용 접착제 또한 널리 사용되고 있습니다. 유럽연합 위원회는 에너지 효율이 높고 탄소 발자국이 적은 건물 건설에 막대한 자금을 할당하는 '차세대 EU 회복 계획'을 발표했습니다. 이는 새로운 건물의 건설과 오래된 건물의 리노베이션으로 이어질 것으로 예상됩니다. 프랑스의 건설 부문은 6.65 %의 연평균 성장률을 기록 할 것으로 예상되며, 이는 예측 기간 동안 접착제 수요 증가로 이어질 것으로 예상됩니다.

- 프랑스의 의료비 지출은 주변 국가에 비해 훨씬 높습니다. 2019년 세계은행이 제공한 데이터에 따르면 유럽의 1인당 평균 의료비 지출은 3,858달러인 반면, 프랑스의 경우 1인당 4,491달러입니다. 그러나 새로운 기술의 도입으로 수요가 급격히 증가하면서 2021년에는 의료기기 시장 규모가 430억 달러에 달할 것으로 예상됩니다.

프랑스의 접착제 시장 동향

프랑스의 저렴하고 가벼운 포장 동향 증가는 연질 및 경질 플라스틱 포장 수요를 견인

- 프랑스의 1인당 GDP는 4만 4,750달러로, 2022년의 성장률은 전년 대비 2.9%였습니다.

- 2020년 프랑스 경제는 코로나19 팬데믹의 영향으로 둔화세를 보였습니다. 이는 공급망 중단, 노동력 부족, 거의 3개월 동안의 국가 봉쇄로 인해 발생했습니다.

- 유럽에서 포장재 생산량은 연간 4,000억 달러에 달하며, 이 중 13%가 프랑스에서 생산됩니다. 프랑스의 포장 산업은 플라스틱 포장(38%)과 종이 및 판지(29%) 포장에 의해 주도되고 있으며, 주로 식품 포장, 음료, 건강 관리 및 미용 제품에 사용됩니다. 프랑스는 유럽 전체 목재 포장의 20%를 차지하는 목재 포장의 선도적인 생산국입니다.

- 독일은 프랑스 포장 산업의 최대 고객으로, 2019년 9억 2,000만 유로의 무역 적자를 기록했습니다. 프랑스에서 저렴하고 가벼운 포장재가 증가하는 추세는 향후 몇 년 동안 유연하고 단단한 플라스틱 포장재에 대한 수요를 견인할 것으로 예상됩니다.

2035년까지 자동차 순배출량 제로와 더불어 전기차 등록 증가가 자동차 생산을 촉진할 것으로 보입니다.

- 프랑스의 자동차 산업은 다른 주요 유럽 국가에 비해 훨씬 더 나은 성과를 거두었습니다.

- 2020년 자동차와 소형 상용차 생산 대수는 2019년 217만 5,350대에 비해 131만 6,371대가 되어 39.5%의 감소를 기록했습니다.

- 2021년 프랑스의 신규 플러그인 전기자동차 등록 대수는 31만 5,000여 대로 2020년 대비 62%의 성장률을 기록하며 프랑스 내 전기자동차 부문의 수요를 증가시켰습니다.

- 프랑스 자동차 업계는 2035년부터 내연기관 자동차 생산을 금지하기로 한 유럽 의회의 투표를 만장일치로 비난했습니다.

프랑스의 접착제 산업 개요

프랑스의 접착제 시장은 적당히 통합되어 있으며 상위 5개 기업이 41.15%를 점유하고 있습니다. 이 시장의 주요 업체는 3M, Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG(알파벳 순으로 정렬)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 신발 및 가죽

- 포장

- 목공 및 목공예

- 규제 프레임워크

- 프랑스

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 신발 및 가죽

- 의료

- 포장

- 목공 및 목공예

- 기타

- 기술

- 핫멜트

- 반응성

- 용매

- UV 경화형 접착제

- 수성

- 수지

- 아크릴계

- 시아노아크릴레이트

- 에폭시

- 폴리우레탄

- 실리콘

- VAE 및 EVA

- 기타

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- Bolton Adhesives

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI SpA

- Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 억제요인, 기회

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The France Adhesives Market size is estimated at 1.79 billion USD in 2024, and is expected to reach 2.25 billion USD by 2028, growing at a CAGR of 5.86% during the forecast period (2024-2028).

Increase in healthcare expenditure to drive the demand for adhesive

- In France, end-user industries, like packaging, healthcare, construction, share the highest market share in the adhesives market. Flexible packaging experienced substantial growth in France. As cheap and lightweight packaging gains popularity in France, it encourages manufacturers to use flexible packaging for different products.

- Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper & cardboard packaging applications. Waterborne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength which is required in these applications. It is seen that nearly 87 thousand tons of water-borne adhesives are consumed in the packaging industry of the country during 2021.

- In France, construction adhesives are also widely used. The European Commission launched the 'Next Generation EU Recovery Plan', in which a major chunk of funds is allocated for the construction of buildings that are energy efficient and have a lesser carbon footprint. This is expected to lead to the construction of newer buildings and the renovation of older buildings. The construction sector in France is expected to register a CAGR of 6.65%, which is expected to lead to an increase in the demand for adhesives in the forecast period.

- Healthcare expenditure in France is much higher compared to its neighboring countries. The average health expenditure in Europe is USD 3,858 per capita, whereas, in France, it is USD 4,491 per capita, as per the data provided by the World Bank in 2019. However, the medical device market reached USD 43 billion by 2021 due to a rapid increase in demand with the adoption of new technologies. This is likely to drive the market for adhesives in the country.

France Adhesives Market Trends

Rising trend of cheap and lightweight packaging in France drives the demand for flexible and rigid plastic packaging

- France had a GDP of USD 44,750 per capita, with a growth rate of 2.9% Y-o-Y in 2022. The packaging industry sector contributed around 0.68% of the country's GDP. France has the third-largest packaging industry in Europe. The factors affecting the French packaging industry are trade exchanges, employment, wine production, government policy support, etc.

- The country's economy observed a slowdown in 2020 because of the impact of the COVID-19 pandemic. The production volume was reduced by 4.77% in the same year compared to 2019. This happened due to supply chain disruptions, labor shortages, and a lockdown in the country for nearly three months. The economic recovery in the country started as international borders opened in 2021, resulting in a regular supply of raw materials for production, which increased by 4,100 tons in 2021.

- In Europe, packaging production reached USD 400 billion annually, of which 13% is produced in France. The packaging industry in the country is dominated by plastic packaging (38%) and paper & paperboard (29%) packaging, which is majorly used in food packaging, beverages, healthcare, and beauty products. France is a leading producer of wooden packaging, accounting for 20% of the total European wooden packaging.

- Germany is the largest customer of the French packaging industry, with a trade deficit of EUR 920 million in 2019. The rising trend of cheap and lightweight packaging in France is expected to drive the demand for flexible and rigid plastic packaging in the coming years. Hence, it may lead to the growth of the packaging industry in the country. However, declining wine production in the country may hinder packaging products in the future.

In addition to net-zero vehicle emissions by 2035, electric vehicle registrations growth is likely to propel the automotive production

- The automotive industry in France has fared much better compared to other major European economies. Automotive vehicle production experienced continuous growth till 2018 and further exhibited a decline of 8.3% in 2019, as the automotive market was negatively affected by the COVID-19 pandemic.

- In 2020, the country produced 1,316,371 cars and light commercial vehicles compared to 2,175,350 vehicles produced during 2019, recording a decline of 39.5%, as production came to a halt in 2020 due to the COVID-19 pandemic. The pandemic forced the temporary shutdown of manufacturing units across different parts of the country. Limited raw material supply added to the challenges faced by the automobile sector.

- In 2021, the country's new plug-ins electric vehicle registration stood at over 315,000, registering a growth rate of 62% compared to 2020, enhancing the demand of the electric vehicle segment in France. Along with it, electric vehicles registered a 21.4% market share in March 2022, up from 16.1% Y-o-Y.

- The French car industry has unanimously condemned the European Parliament's vote to ban the production of combustion engine cars from 2035. The country plans to achieve net-zero vehicle emissions by 2035, which is likely to drive the automotive vehicle market in the country over the forecast period.

France Adhesives Industry Overview

The France Adhesives Market is moderately consolidated, with the top five companies occupying 41.15%. The major players in this market are 3M, Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 France

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Bolton Adhesives

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록