|

시장보고서

상품코드

1693384

태국의 접착제 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Thailand Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

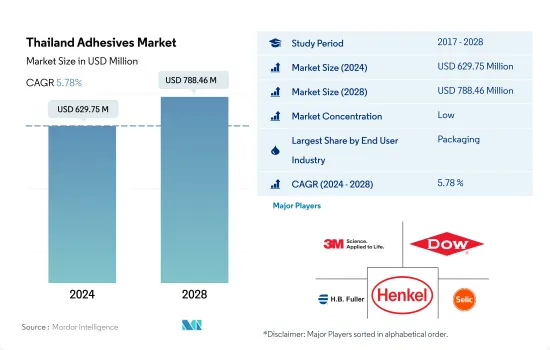

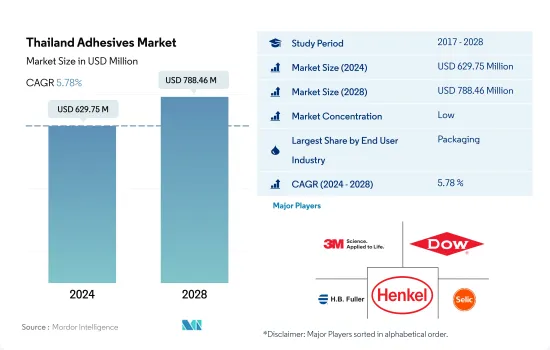

태국의 접착제 시장 규모는 2024년에 6억 2,975만 달러에 달했고, 2028년에는 7억 8,846만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR 5.78%로 성장할 전망입니다.

태국의 자동차 산업은 이 나라에서 접착제 수요의 전반적인 성장에 중요한 역할을 합니다.

- 2020년의 접착제 소비량은 COVID-19의 대유행에 의해 2019년 대비 약 11.6% 감소했습니다. 태국에서는 3개월 가까이 폐쇄가 계속되어 공급 체인의 혼란과 노동력 부족이 생겼습니다.

- 접착제는 플라스틱, 금속, 종이 및 골판지 포장 용도의 접착에 중요한 역할을 하기 때문에 국내 포장 산업에서 주로 소비되고 있습니다. 수성 접착제는 이러한 응용 분야에서 필요한 저렴한 비용과 높은 결합 강도 때문에 업계에서 많이 소비됩니다. 태국의 포장 산업에서는 2021년에 약 2만 6,000톤의 수성 접착제가 소비되었습니다. 2022년부터 2028년까지 이 부문의 연평균 성장률은 2.37%를 보일 것으로 예측됩니다.

- 자동차산업은 태국의 접착제 2위 소비자입니다. 이 나라의 자동차 생산능력은 168만대에 달하고, 전년대비 18% 증가했기 때문에 자동차 접착제 시장은 2021년 16.62% 성장했습니다. 국제 시장에서의 태국의 자동차 수출 수요가 향후 몇 년간의 자동차용 접착제 수요를 견인할 것으로 예측됩니다.

태국 접착제 시장 동향

식품, 화장품 및 기타 산업에서 플라스틱 포장 수요 증가가 포장 산업을 견인

- 태국은 2022년에 1인당 7,450달러의 GDP를 기록했으며, 전년 대비 성장률은 3.3%였습니다.

- 2020년 COVID-19 팬데믹으로 인해 태국 경제는 2019년에 비해 4.74% 감소했습니다. 그러나 2021년에 국제 국경이 개방된 것에 따른 국내 경기 회복에 의해 생산에 필요한 원료의 정기적인 공급이 시작되어 2021년에는 7,900톤 증가했습니다.

- 태국은 세계의 플라스틱 포장 시장의 주요 제조국 중 하나입니다.

- 태국 포장 산업에서 바이오플라스틱의 사용량은 증가하고 있습니다.

ASEAN 국가의 자동차 생산 대수의 50.1% 가까이가 태국 자동차 산업을 견인할 것으로 보인다.

- 태국의 자동차 산업은 지난 50년간 눈부신 성장을 이루었습니다. 태국은 아세안 지역에서 가장 큰 자동차 생산국입니다. 2020년 생산 대수는 142만 7,074대로, ASEAN 전체의 50.1%를 차지하고 있습니다.

- 2019년 자동차 생산 대수는 약 201만 3,710대를 기록했지만, 2020년에는 142만 7,074대로 격감해, COVID-19의 유행에 의해 약 29%의 감소한 수치입니다. 2019-2021년에 걸친 자동차 생산 대수의 변동은 약-16%였지만, 2020-2021년에 걸쳐 변동은 약-1%를 기록했습니다.

- 태국은 세계 11위, ASEAN에서는 1위의 자동차 생산국이며 밸류체인이 확립되어 있기 때문에 ASEAN의 EV센터가 될 준비가 되어 있습니다. 태국의 EV 재고는 현지 수요에 부응하여 꾸준히 증가하고 있습니다. 더 중요한 점은 태국의 유명 기업 여러 회사가 국내 EV 충전 인프라에 적극적으로 투자함으로써 미래 수요 증가에 대한 확신이 높아지고 있음을 보여줍니다. 충전소과 같은 EV 인프라를 늘리는 정부 및 민간 기관의 노력은 태국의 EV 생태계가 빠르게 발전하고 있음을 시사합니다.

태국 접착제 산업 개요

태국의 접착제 시장은 세분화되어 상위 5개사에서 29.77%를 차지하고 있습니다. 이 시장의 주요 기업은 3M, Dow, HB Fuller Company, Henkel AG & Co. KGaA, Selic Corp Public Company Limited 등입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 양말 피혁

- 포장

- 목공 및 가구 제조

- 규제 프레임워크

- 태국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 양말와 가죽

- 의료

- 포장

- 목공 및 가구 제조

- 기타

- 기술

- 핫멜트

- 반응성

- 용제계

- UV 경화형 접착제

- 수성

- 수지

- 아크릴계

- 시아노아크릴레이트

- 에폭시

- 폴리우레탄

- 실리콘

- VAE?EVA

- 기타

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Arkema Group

- Dow

- DUNLOP ADHESIVES(THAILAND) CO., LTD.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Selic Corp Public Company Limited.

- Sika AG

- Star Bond(Thailand) Company Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 억제요인, 기회

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Thailand Adhesives Market size is estimated at 629.75 million USD in 2024, and is expected to reach 788.46 million USD by 2028, growing at a CAGR of 5.78% during the forecast period (2024-2028).

Thailand's Automotive industry having a significant role in the overall growth of adhesive's demand in the country

- The consumption of adhesives declined in 2020 by about 11.6% compared to 2019 due to the COVID-19 pandemic, which severely affected the consumption of adhesives in Thailand owing to the closedown of the manufacturing sites and reduction in demand. The lockdown in the country for nearly three months resulted in supply chain disruptions and labor shortages. However, consumption registered growth in 2021 with a positive growth rate of about 10% due to steady demand from the manufacturing sector.

- Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper and cardboard packaging applications. Water-borne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength, which is required in these applications. Nearly 26 thousand tons of water-borne adhesives were consumed in the Thai packaging industry in 2021. Solvent-borne adhesives are the fastest-growing technology in the packaging industry, and the segment is expected to register a CAGR of 2.37% from 2022 to 2028.

- The automotive industry is the second-largest consumer of adhesives in Thailand. The automotive adhesives market grew by 16.62% in 2021, as the country's total vehicle manufacturing capacity reached 1.68 million units, up by 18% from the previous year. The rising demand for Thailand's automotive exports in the international market is expected to drive the demand for automotive adhesives over the coming years. The automotive export value reached USD 41.43 billion in 2021.

Thailand Adhesives Market Trends

Growing demand for plastic packaging in food, cosmetics, and other industries will propel the packaging industry

- Thailand registered a GDP of USD 7,450 per capita with a growth rate of 3.3% Y-O-Y in 2022. The packaging industry contributes a share of around 1.91 of the country's GDP. Trade exchange, employment, labor charges, government policy support, etc., affect the Thai packaging industry.

- The country observed an economic slowdown in 2020 because of the COVID-19 pandemic. Production volume declined by 4.74% in the same year compared to 2019. This happened due to supply chain disruptions, labor shortages, and a lockdown in the country for nearly three months. However, because of economic recovery in the country in line with international borders being opened in 2021, the regular supply of raw materials began for production, which increased by 7,900 ton in 2021.

- Thailand is one of the major manufacturing countries in the global plastic packaging market. The plastic packaging industry reaches USD 5 billion annually, the highest among other types of packaging. Around 28% of the country's plastic production is used in plastic packaging products. This packaging is majorly used in food, healthcare, cosmetics, and many other types of products in Thailand.

- The usage of bioplastics in the packaging industry of Thailand is increasing. The government has also prioritized the bioplastic industry's development through policies such as the Plastic Waste Management Roadmap (2018-2030). GC and Cargill are two multinational biopolymer companies that have announced plans to invest USD 20 billion in establishing new bioplastic plants in Thailand.

Nearly 50.1% share of the overall automotive production among the ASEAN countries is likely to drive the industry in Thailand

- The Thai automobile sector has grown tremendously over the last 50 years. The country is constantly advancing its next-generation automotive industry to follow the S-Curve promotion with better value-added production, and it also aims for the automotive industrial policy to be aligned with the environmental protection policy. Thailand is the largest auto producer in the ASEAN region. In 2020, production totaled 1,427,074 units, accounting for 50.1% of total ASEAN production. This was followed by Indonesia (690,150 units, or approximately 24.2%) and Malaysia (485,186 units, or approximately 17.0%).

- In 2019, the country recorded about 20.13,710 units of vehicles produced, which drastically reduced to 14,27,074 units in 2020, accounting for a decline of about 29% owing to the COVID-19 pandemic. As a result, the variation in automotive production between 2019 and 2021 amounted to about -16%, whereas between 2020 and 2021, the variation was recorded at about -1%.

- Thailand, ranked as the 11th largest automotive producer in the world and the first in ASEAN, is poised to become ASEAN's EV center, owing to its well-established value chain, which provides the industry with top-notch quality products at a competitive price. Thailand's EV stock has been steadily increasing in response to local demand. More importantly, several well-known Thai corporations have been actively investing in EV charging infrastructure around the country, indicating rising confidence in future demand increases. Efforts by governmental and private sector institutions to increase EV infrastructure, such as charging stations, suggest that Thailand's EV ecosystem is developing rapidly.

Thailand Adhesives Industry Overview

The Thailand Adhesives Market is fragmented, with the top five companies occupying 29.77%. The major players in this market are 3M, Dow, H.B. Fuller Company, Henkel AG & Co. KGaA and Selic Corp Public Company Limited. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 DUNLOP ADHESIVES (THAILAND) CO., LTD.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 Selic Corp Public Company Limited.

- 6.4.9 Sika AG

- 6.4.10 Star Bond (Thailand) Company Limited

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록