|

시장보고서

상품코드

1693395

스페인의 실란트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Spain Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

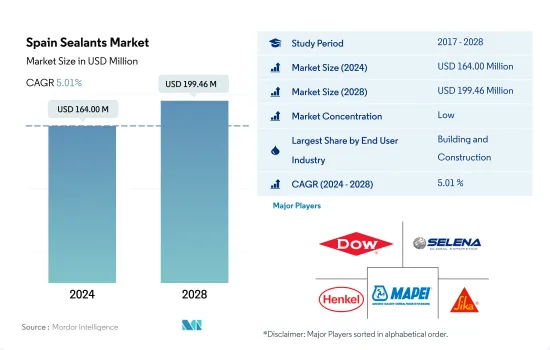

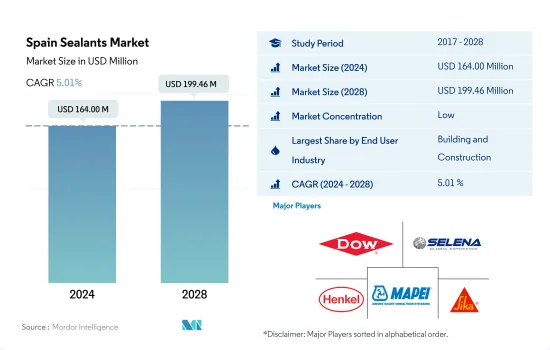

스페인의 실란트 시장 규모는 2024년 1억 6,400만 달러, 2028년에는 1억 9,946만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR 5.01%로 성장할 것으로 예측됩니다.

신규 건설 및 인프라 개발이 시장 성장을 견인

- 스페인의 실란트 시장은 방수, 내후성 실링, 균열 실링, 조인트 실링 등, 건축 및 건설 활동에 있어서의 실란트의 다양한 용도에 의해 건설 업계가 주요한 견인역이 되어, 기타 최종사용자 업계가 뒤를 이었습니다. 게다가, 건축용 실란트는 내용 연수가 길고, 다양한 기재에 간단히 도포할 수 있도록 설계됐습니다. 스페인의 건설 산업은 2019년에 해당 국가의 GDP의 약 5.7%를 기록했습니다. 이러한 동향은 가까운 미래에도 계속되어 실란트 수요를 서서히 증가시킬 가능성이 높습니다.

- 전기 장비 제조에서는 다양한 실란트가 포팅 및 보호 용도에 사용됩니다. 센서나 케이블의 씰 등에 사용됩니다. 스페인의 전자기기 시장은 무선 전자기기의 인기와 웨어러블 가젯의 급속한 보급으로 큰 성장을 기록했습니다. 이것은 다른 최종 사용자 부문에서 실란트 수요를 촉진합니다. 게다가 기관차 및 DIY 산업에서의 실란트의 다양한 용도는 2028년까지 필요한 실란트 수요를 끌어올릴 것으로 보입니다.

- 실란트는 의료 및 자동차 산업에서 다양한 용도가 있습니다. 실란트는 의료기기 부품의 조립 및 씰과 같은 의료용으로 사용됩니다. 자동차 산업은 다양한 기재에 실란트의 큰 적용성을 보여 주며, 주로 엔진과 자동차 가스켓에 사용됩니다. 스페인은 최근 이러한 분야에서 유망한 성장을 기록하고 있으며 앞으로 몇 년 동안 계속 될 것으로 보입니다. 그러므로 이러한 추세는 2028년까지 실란트 수요를 증대시킬 것으로 보입니다.

스페인 실란트 시장 동향

저렴한 주택용으로 10억 유로 상당의 국가 복구 및 부흥 계획(NRRP) 등의 투자가 건설 업계를 견인

- COVID-19 팬데믹이 스페인 건설 부문에 미치는 영향은 엄청났습니다. 건설 업계는 타격을 받아 2020년 1-3월 투자액은 9.6% 감소했습니다. 운송 및 호텔 부문의 2020년 1분기 건설활동 생산고는 11% 감소를 기록했습니다.

- 건설 시장을 회복시키기 위해 스페인 정부는 2022년 12월 31일까지 연장을 포함한 국가 주택 계획 2018-2021의 수정을 도입했습니다. 건설 시장은 2021년에 힘차게 회복해 약 24.9%의 성장을 이루게 되었습니다.

- 스페인 정부는 2021-2026년 국가 부흥 탄력계획(NRRP) 하에 저렴한 가격으로 에너지 효율이 높은 임대주택 건설에 10억 유로를 할당했습니다.

- 스페인의 건설 업계의 전망은 일반적으로 양호합니다. 공공 인프라에 대한 투자, 디지털화, 에너지 효율이 높은 주택의 개축, 유럽 연합(EU)의 자금 원조에 의한 그린인 순환형 경제등이, 향후의 업계의 성장을 뒷받침할 것으로 예상됩니다.

EV 수요 증가와 240억 유로에 해당하는 공적 및 민간 e모빌리티 투자로 자동차 수요 증가

- 스페인은 독일에 이어 유럽 2위의 자동차 생산국입니다.

- 이 나라의 자동차 생산은 최근 몇년간 거의 일정합니다.

- 2021년 1-3분기 자동차 생산 대수는 2020년 1-3분기 대비 4% 증가하여 159만 2,277대에 달했습니다. 이 나라의 자동차 산업은 예측 기간 동안 완만한 수요가 될 것 같습니다. 그러나 2021년 동국의 자동차 생산 대수는 약 209만 8,133대로 2020년보다 8% 감소했습니다. 반도체 칩 부족과 공급망의 제약이 이 나라의 자동차 생산량에 악영향을 미쳤습니다.

- 자동차 생산 대수 부족은 최근 악화되고 있어 2022년에는 생산 대수가 18% 증가해 강력한 회복이 전망됩니다. 스페인의 전기자동차 시장은 공급업체의 전자 이동성으로의 전환을 지원하는 차세대 EU 기금의 혜택을 받아야 합니다. 또한 스페인 정부는 향후 3년간 240억 유로에 해당하는 공적 및 민간 전자 이동성 투자를 발표하고 있습니다.

스페인 실란트 산업 개요

스페인 실란트 시장은 세분화되어 상위 5개 기업에서 35.13%를 차지하고 있습니다. 이 시장 주요 기업은 Dow, Grupa Selena, Henkel AG & Co. KGaA, MAPEI SpA, Sika AG(알파벳순)가 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 규제 프레임워크

- 스페인

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 헬스케어

- 기타 최종 사용자 산업

- 수지

- 아크릴

- 에폭시

- 폴리우레탄

- 실리콘

- 기타 수지

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Dow

- Grupa Selena

- Henkel AG & Co. KGaA

- Industrias Quimicas del Adhesivo, SA-Quiadsa

- MAPEI SpA

- QS Adhesives & Sealants SL

- RPM International Inc.

- Sika AG

- Soudal Holding NV

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업의 개요

- 개요

- Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 저해요인, 기회

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Spain Sealants Market size is estimated at 164.00 million USD in 2024, and is expected to reach 199.46 million USD by 2028, growing at a CAGR of 5.01% during the forecast period (2024-2028).

New construction and infrastructure development to lead the market growth

- The Spain sealants market is majorly driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction industry of Spain registered around 5.7% of the country's GDP in 2019. During COVID-19, the construction output was reduced by 19.5% in 2020, sustained in 2021 owing to increasing construction investment and home maintenance activities in the country. Such trends will likely continue in the near future and gradually increase sealants demand.

- A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Spanish electronics market registered significant growth, mostly due to the growing popularity of wireless electronic devices and the rapid adoption of wearable gadgets. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, a range of applications of sealants in the locomotive and DIY industries will boost the demand for required sealants by 2028.

- Sealants have diverse applications in the healthcare and automotive industries. Sealants are used in healthcare applications, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, mostly used for engines and car gaskets. Spain has registered promising growth in these sectors in recent times and is likely to continue in the upcoming years. Thus, such a trend will augment the demand for sealants by 2028.

Spain Sealants Market Trends

Investments including National Recovery and Resilience Plan (NRRP) worth EUR 1 billion for affordable housing to lead the construction industry

- The impact of the COVID-19 pandemic was huge on the Spanish construction sector. The construction industry pummeled and observed a decline of 9.6% in investments in the first three months of 2020. Construction activity output in the transport and hotel sector registered a decline of 11% in Q1 2020.

- To revive the construction market, the Spanish government introduced amendments to the State Housing Plan 2018-2021, including the program's extension until December 31, 2022. The country also receives financial support from the European Investment Bank (EIB) for developing and constructing social housing. The Spanish construction market was to rebound strongly in 2021 and grow about 24.9% in 2021. As of June 2021, the EIB signed an agreement to support Barcelona City Council in constructing nearly 490 new public rental homes with an investment of EUR 36.2 million.

- Under its 2021-2026 National Recovery and Resilience Plan (NRRP), the Spanish government allocated EUR 1 billion to construct affordable and energy-efficient rental housing. Thus, the construction market in the country is expected to register a 2% CAGR during the forecast period (2022-2028).

- The general outlook for the Spanish construction industry is favorable. Future industry growth is anticipated to be fueled by investments in public sector infrastructure, digitalization, energy-efficient housing renovations, and a green circular economy, all funded by the European Union.

Increasing EVs demand and government investment of public and private e-mobility investments worth EUR 24 billion to boost the automotive demand

- Spain is the second-largest automobile producer in Europe, after Germany. Spanish automotive suppliers produced EUR 35,822 million worth of products in 2019, of which 60% were exported inside and outside the European region.

- Automobile production in the country has been almost constant in the past few years. In 2019, the country produced about 28,22,355 units, registering a meager growth rate of 0.1% over 2018. The country produced about 22,68,185 units of vehicles in 2020. Automotive vehicle production contracted by 18.6% in 2020 as the COVID-19 pandemic halted the supply chain.

- In the first three quarters of 2021, automotive production increased by 4% over Q1-Q3 of 2020 and reached 1,592,277 vehicles. The country's automotive industry is likely to witness moderate demand during the forecast period. However, in 2021, the country produced about 2,098,133 vehicles, which was a decline of 8% from 2020. The semiconductor chip shortage and supply chain restrictions negatively affected the production of automotive vehicle units in the country.

- The automotive production shortfalls have recently worsened, and a strong rebound is expected in 2022, with output increasing by 18%. The Spanish electric vehicles market should benefit from the Next Generation EU fund, which supports suppliers in their shift toward e-mobility. Additionally, the Spanish government has announced public and private e-mobility investments worth EUR 24 billion over the coming three years.

Spain Sealants Industry Overview

The Spain Sealants Market is fragmented, with the top five companies occupying 35.13%. The major players in this market are Dow, Grupa Selena, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Spain

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Dow

- 6.4.3 Grupa Selena

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Industrias Quimicas del Adhesivo, S.A. - Quiadsa

- 6.4.6 MAPEI S.p.A.

- 6.4.7 QS Adhesives & Sealants SL

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms