|

시장보고서

상품코드

1693520

2차 다량 영양소 비료 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Secondary Macronutrients Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

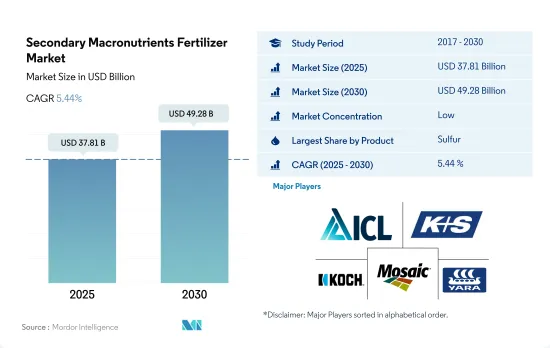

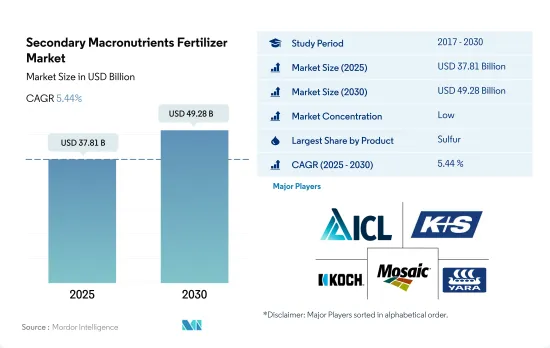

2차 다량 영양소 비료 시장 규모는 2025년에 378억 1,000만 달러로 추정되고, 2030년에는 492억 8,000만 달러에 이를 전망이며, 예측 기간인 2025-2030년 CAGR 5.44%로 성장할 것으로 예측됩니다.

유황비료의 채용은 다른 2차 다량 영양소보다 더 많습니다.

- 2021년 유황은 세계의 2차 다량 영양소 비료 시장의 42.6%를 차지했습니다. 2021년 유럽의 유황 시장 금액은 약 11억 9,000만 달러였습니다. 이 시장에 있어서, 특수 황비료의 시장 점유율은 약 49.4%, 종래형 황비료의 시장 점유율은 약 50.1%였습니다. 특수 황비료의 채택률은 다른 2차 다량 영양소보다 높습니다. 특수 황비료 시장은 예측 기간 종료까지 18억 2,000만 달러에 이를 것으로 예상됩니다.

- 마그네슘은 2021년에 세계의 2차 다량 영양소 비료 시장의 48.9%를 차지했습니다. 농작물이 88.8%로 가장 큰 점유율을 차지하고, 그 다음으로 잔디 및 관상용 작물이 3.9%, 원예 작물이 7.3%의 점유율을 차지했습니다. 비료를 가장 많이 소비하는 작물은 밀과 옥수수로 총 토지면적의 40.0%를 차지했습니다.

- 칼슘은 세계의 2차 다량 영양소 비료 시장의 총액의 8.4%를 차지하고, 2021년에는 약 5억 3,870만 달러를 차지했습니다. 아시아 태평양 지역은 칼슘비료 시장을 독점하여 세계 칼슘비료 시장의 약 41.1%를 차지하고 2021년에는 2억 2,160만 달러를 기록했습니다. 칼슘 비료 시장에서 아시아 태평양 지역의 우위는 주로 토양의 산성화에 의한 것으로, 칼슘이나 마그네슘 등의 염기성 양이온이 상실되어 철이나 알루미늄 착체와 같은 산성 원소로 대체되고 있습니다.

- 작물의 재배 면적이 감소하고 있기 때문에 보다 높은 생산성이 요구되고 있어 2차 다량 영양소 비료 수요는 예측 기간 중에 성장할 것으로 예상됩니다.

기후 변화와 토양의 pH 수준 변화가 시장을 견인할 가능성

- 2차 다량 영양소 비료의 시용은 작물의 수량에 플러스의 영향을 줍니다. 칼슘, 마그네슘, 유황의 수요는 근대적인 고수량 작물 시스템과 연동되어 증가하고 있으며, 식물의 생산성에 있어서 매우 중요한 역할을 담당하고 있는 것으로 밝혀지고 있습니다.

- 아시아태평양은 세계의 2차 다량 영양소 비료 시장을 독점하고 있으며, 2022년에는 그 39.2%를 차지했습니다. 이 지역에서는 유황이 63.5%로 대부분의 점유율을 차지하고 마그네슘의 30.0%가 뒤를 이었습니다. 아시아태평양 지역에서는 쌀이 주요 곡물 작물이며 세계 생산과 소비의 90%를 차지하고 있습니다. 이 지역의 토양은 황이 부족하기 때문에 중요한 미량 원소인 황은 식물의 성장과 수확량을 높이기 위해 시비에 의해 보충됩니다.

- 2022년 세계의 2차 다량 영양소 비료 시장에서는 유럽이 26.9%의 점유율로 2위 자리를 확보했습니다. 유황은 시장 금액의 67.4%를 차지했으며, 2022년 2차 다량 영양소 비료 1위로 올라섰습니다. 러시아는 시장 점유율 19.2%로 유럽 시장의 지배적 기업으로 떠올랐습니다.

- 2022년 남미의 2차 다량 영양소 비료 시장은 세계 시장의 11.5%의 점유율을 차지했습니다. 최근의 가뭄과 열파가 이 지역 토양에서의 영양분 이용 가능성을 방해하고 이러한 결핍에 대항하기 위해 2차 다량 영양소 비료의 채택을 촉진했습니다.

- 2차 다량 영양소는 각 영양소가 특정 대사 과정에 영향을 미치는 것으로 식물의 영양 균형을 유지하는데 있어서 매우 중요한 역할을 하고 있습니다. 최적화된 식물영양의 중요성이 점점 인식됨에 따라 이 역동적인 움직임이 앞으로 수년간 시장의 성장을 촉진할 것으로 보입니다.

세계의 2차 다량 영양소 비료 시장 동향

증가하는 식량 수요를 충족시키기 위한 농업 부문에 대한 압력 증가는 농작물의 재배 면적을 증가시킬 것으로 예상됩니다.

- 세계의 농업 부문은 현재 많은 과제에 직면하고 있습니다. 유엔에 따르면 세계 인구는 2050년까지 90억 명을 넘을 수 있습니다. 이 인구 증가는 노동력 부족과 도시화 진전에 따른 농지 축소로 이미 생산량 저하를 겪고 있는 농업 부문에 과대한 부담을 줄 가능성이 있습니다. 유엔 식량농업기구에 따르면 2050년까지 세계 인구의 70%가 도시에 살게 될 것으로 예상되고 있습니다. 세계적으로 경지가 감소하고 있기 때문에 농가는 작물 수확량을 늘리기 위해 더 많은 비료를 이용해야 합니다.

- 아시아태평양은 세계에서 가장 큰 농산물 생산지입니다. 농업은 이 지역의 경제에 필수적이며, 전체 노동 인구의 약 20%를 고용하고 있습니다. 농작물이 이 지역을 지배하고 있으며, 전체 작물 면적의 95% 이상을 차지하고 있습니다. 쌀, 밀, 옥수수가 이 지역에서 생산되는 주요 농작물로 2022년 총 재배 면적의 약 24.3%를 차지했습니다.

- 북미는 세계 제2위의 경작 가능 지역입니다. 그 농장에서는 농작물을 중심으로 다양한 작물이 재배되고 있습니다. 특히 옥수수, 면화, 쌀, 콩, 밀은 미국 농무부가 강조하고 있듯이 저명한 밭농사 작물입니다. 2022년 미국은 북미 작물 재배 면적의 46.2%를 차지했습니다. 그러나 이 나라는 2017-2019년 작부 면적이 크게 감소한 것을 목격했는데, 이는 주로 텍사스와 휴스턴 등의 지역에서 심각한 홍수를 겪은 악환경 때문입니다.

유황은 식물 내에서 이동하지 않기 때문에 성장 초기부터 수확까지 안정적인 공급이 필요하며 공급이 부족하면 수율이 제한될 수 있습니다.

- 2022년 농작물에 있어서의 2차 다량 영양소의 세계 평균 시용량은 33.73kg/ha였습니다. 같은 해의 칼슘 시용량은 약 39.20kg/헥타르, 마그네슘 시용량은 약 34.51kg/헥타르, 황 시용량은 27.47kg/헥타르였습니다. 칼슘은 다른 필수 영양소의 흡수를 돕습니다. 마그네슘은 식물의 성장과 개화를 촉진하는 뛰어난 효소 활성제입니다. 식물이 필요로 하는 2차 다량 영양소는 소량으로 1차 영양소로는 대체할 수 없습니다.

- 2022년의 평균 유황 시용량은 옥수수 및 메이즈가 34.33kg/ha로 가장 많았고, 이어서 면화가 29.72kg/ha, 유채/카놀라가 27.57kg/ha였습니다. 유황은 식물체 내에서 이동하지 않기 때문에 생육 초기부터 수확까지 안정적인 공급이 필요합니다. 생육의 어느 단계에서나 유황이 부족하면 수확량의 저하로 이어집니다. N, P, K의 요구량은 거의 충족되었기 때문에 다른 영양소의 부족이 나타나기 시작했습니다. 황은 N, P, K에 이어 네 번째로 중요한 양분이지만, 보통은 소량밖에 필요하지 않습니다.

- 남미, 중동 및 아프리카, 아시아태평양이 2차 다량 영양소의 주된 소비국으로, 평균 시비량이 가장 많아, 2022년에는 각각 39.27kg/ha, 32.79kg/ha, 32.74kg/ha를 차지했습니다. 2차 다량 영양소는 식물에게 중요한 영양소이며, 보다 견고한 세포벽을 지지하고 타박상을 줄여주며, 농작물 질병을 예방하기 위해 생산자는 2차 다량 영양소의 중요성을 인정하고 있습니다. 2차 다량 영양소는 1차 다량 영양소보다 수확량을 제한하지는 않지만 작물은 생산성을 최적화하기 위해 2차 다량 영양소를 필요로 합니다.

2차 다량 영양소 비료의 산업 개요

2차 다량 영양소 비료 시장은 세분화되어 있으며 주요 5개사에서 10.61%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. ICL Group Ltd, K+S Aktiengesellschaft, Koch Industries Inc., The Mosaic Company and Yara International ASA.(알파벳순 정렬)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 주요 작물의 작부 면적

- 농작물

- 원예작물

- 평균 양분 시용률

- 2차 다량 영양소

- 농작물

- 원예작물

- 2차 다량 영양소

- 관개 설비가 있는 농지

- 규제 프레임워크

- 밸류체인 및 유통 채널 분석

제5장 시장 세분화

- 유형별

- 스트레이트

- 2차 영양소

- 칼슘

- 마그네슘

- 유황

- 스트레이트

- 적용 모드별

- 시비

- 잎면 살포

- 토양

- 작물 유형별

- 농작물

- 원예작물

- 잔디 및 관상용

- 지역별

- 아시아태평양

- 호주

- 방글라데시

- 중국

- 인도

- 인도네시아

- 일본

- 파키스탄

- 필리핀

- 태국

- 베트남

- 기타 아시아태평양

- 유럽

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 기타 유럽

- 중동 및 아프리카

- 나이지리아

- 사우디아라비아

- 남아프리카

- 튀르키예

- 기타 중동 및 아프리카

- 북미

- 캐나다

- 멕시코

- 미국

- 기타 북미

- 남미

- 아르헨티나

- 브라질

- 기타 남미

- 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Coromandel International Ltd.

- Deepak fertilizers & Petrochemicals Corporation Ltd

- Grupa Azoty SA(Compo Expert)

- Haifa Group

- ICL Group Ltd

- KS Aktiengesellschaft

- Koch Industries Inc.

- The Mosaic Company

- Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Secondary Macronutrients Fertilizer Market size is estimated at 37.81 billion USD in 2025, and is expected to reach 49.28 billion USD by 2030, growing at a CAGR of 5.44% during the forecast period (2025-2030).

The adoption of sulfur fertilizer is more than other secondary macronutrients

- In 2021, sulfur accounted for 42.6% of the global secondary macronutrient fertilizer market. In 2021, the value of the European sulfur market was about USD 1.19 billion. In this market, specialty sulfur fertilizer accounted for a market share of approximately 49.4%, and conventional sulfur fertilizer accounted for about 50.1%. The adoption of specialty sulfur fertilizer is higher than that of other secondary macronutrients. The specialty sulfur fertilizer market is anticipated to reach USD 1.82 billion by the end of the forecast period.

- Magnesium accounted for 48.9% of the global secondary macronutrient fertilizer market in 2021. Field crops accounted for a maximum share of 88.8%, followed by turf and ornamental crops and horticulture crops, holding shares of 3.9% and 7.3%, respectively. The largest fertilizer-consuming crops are wheat and corn, accounting for a total of 40.0% of the land area.

- Calcium recorded 8.4% of the total value of the global secondary macronutrient fertilizer market, accounting for about USD 538.7 million in 2021. The Asia-Pacific region dominated the calcium fertilizer market and accounted for about 41.1% of the global calcium fertilizer market's value, registering USD 221.6 million in 2021. The dominance of the Asia-Pacific region in the calcium fertilizer market is mainly due to the acidification of soils, which means the loss of base cations, such as calcium and magnesium, and replacement with acidic elements, like iron and aluminum complexes.

- The demand for secondary macronutrient fertilizer is anticipated to grow during the forecast period, as the need for higher productivity is increasing due to the decline in the area under the cultivation of crops.

Climate changes and fluctuation in pH levels in soils may drive the market

- Applying secondary macronutrient fertilizers impacts crop yields positively. The demand for calcium, magnesium, and sulfur has risen in tandem with modern high-yield crop systems, underscoring their pivotal role in plant productivity.

- Asia-Pacific dominates the global secondary macronutrient fertilizer market, capturing 39.2% of its value in 2022. Within the region, sulfur claims the majority share at 63.5%, trailed by magnesium at 30.0%. Rice is the major grown cereal crop in Asia-Pacific, with the region accounting for 90% of global production and consumption. Given the region's sulfur-deficient soils, sulfur, a crucial trace element, is supplemented through fertilization to enhance plant growth and yield.

- Europe secured the second-largest share of the global secondary macronutrient fertilizer market in 2022, with a share of 26.9%. Sulfur, commanding a hefty 67.4% of the market's value, emerged as the leading secondary macronutrient fertilizer in 2022. Russia, with a 19.2% market share, emerged as the dominant player in Europe's market landscape.

- In 2022, the South American secondary macronutrient fertilizer market held an 11.5% share of the global market. Recent droughts and heat waves disrupted nutrient availability in the region's soils, driving up the adoption of secondary macronutrient fertilizers to counteract these deficiencies.

- Secondary macronutrients play a pivotal role in maintaining balanced plant nutrition, with each nutrient influencing specific metabolic processes. This dynamic is poised to fuel the growth of the market in the coming years as the importance of optimized plant nutrition becomes increasingly recognized.

Global Secondary Macronutrients Fertilizer Market Trends

The rising pressure on the agriculture sector to meet the growing demand for food is expected to increase the area under field crop cultivation

- The global agricultural sector is currently facing many challenges. According to the United Nations, the world population may exceed 9 billion by 2050. This population growth may overburden the agricultural sector, which is already experiencing an output loss due to a lack of laborers and the shrinkage of agricultural fields caused by rising urbanization. According to the Food and Agriculture Organization, 70% of the global population is expected to live in cities by 2050. Due to the global loss of arable land, farmers now need to utilize more fertilizers to increase crop yields.

- Asia-Pacific is the world's largest producer of agricultural products. Agriculture is critical to the region's economy, as it employs about 20% of the total available workforce. Field crop cultivation dominates the region, accounting for more than 95% of the total crop area. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 24.3% of the total crop area in 2022.

- North America ranks as the second-largest arable region across the world. Its farms cultivate a diverse range of crops, with a focus on field crops. Notably, corn, cotton, rice, soybean, and wheat are the prominent field crops, as highlighted by the USDA. In 2022, the United States commanded 46.2% of North America's crop cultivation area. However, the country witnessed a significant drop in crop acreage between 2017 and 2019, primarily due to adverse environmental conditions, leading to severe flooding in regions like Texas and Houston.

A steady supply of sulfur is required from early growth stages until harvest as it is immobile in plants, and any shortage in supply can limit the yield

- The global average application rate of secondary macronutrients in field crops was 33.73 kg/ha in 2022. In the same year, the calcium application rate was about 39.20 kg/hectare, magnesium was about 34.51 kg/hectare, and sulfur application rate was 27.47 kg/hectare. Calcium aids in the absorption of other essential nutrients. Magnesium is an excellent enzyme activator that promotes plant growth and flowering. Plants require only a small amount of secondary macronutrients that cannot be replaced by any primary nutrients.

- In 2022, corn/maize recorded the highest average sulfur application rate of 34.33 kg/ha, followed by cotton at 29.72 kg/ha and rapeseed/canola at 27.57 kg/ha. A steady supply of sulfur is required from early growth stages until harvest as it is immobile in plants. At any stage of growth, a shortage of sulfur can lead to lower yields. As N, P, and K requirements have mostly been met, deficits of other nutrients have started to appear. Sulfur is the fourth most crucial nutrient after N, P, and K but is usually only needed in low quantities.

- South America, the Middle East & Africa, and Asia-Pacific were the major consumers of secondary macronutrients, with the highest average nutrient application rates, accounting for 39.27 kg/ha, 32.79 kg/ha, and 32.74 kg/ha, respectively, in 2022. Growers acknowledged the importance of secondary macronutrients because they are crucial nutrients for plants, support stronger cell walls, lower bruising, and prevent disease in field crops. Although secondary macronutrients are less yield-limiting than primary macronutrients, crops need them at a rate that will optimize productivity.

Secondary Macronutrients Fertilizer Industry Overview

The Secondary Macronutrients Fertilizer Market is fragmented, with the top five companies occupying 10.61%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Koch Industries Inc., The Mosaic Company and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Secondary Macronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Secondary Macronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Straight

- 5.1.1.1 Secondary Macronutrients

- 5.1.1.1.1 Calcium

- 5.1.1.1.2 Magnesium

- 5.1.1.1.3 Sulfur

- 5.1.1 Straight

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest of Europe

- 5.4.3 Middle East & Africa

- 5.4.3.1 Nigeria

- 5.4.3.2 Saudi Arabia

- 5.4.3.3 South Africa

- 5.4.3.4 Turkey

- 5.4.3.5 Rest of Middle East & Africa

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Rest of South America

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Coromandel International Ltd.

- 6.4.2 Deepak fertilizers & Petrochemicals Corporation Ltd

- 6.4.3 Grupa Azoty S.A. (Compo Expert)

- 6.4.4 Haifa Group

- 6.4.5 ICL Group Ltd

- 6.4.6 K+S Aktiengesellschaft

- 6.4.7 Koch Industries Inc.

- 6.4.8 The Mosaic Company

- 6.4.9 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms