|

시장보고서

상품코드

1693545

프랑스의 항공 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)France Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

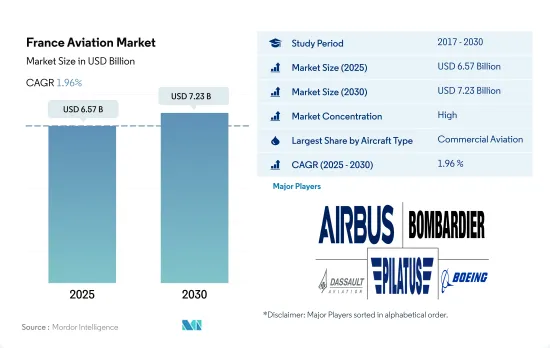

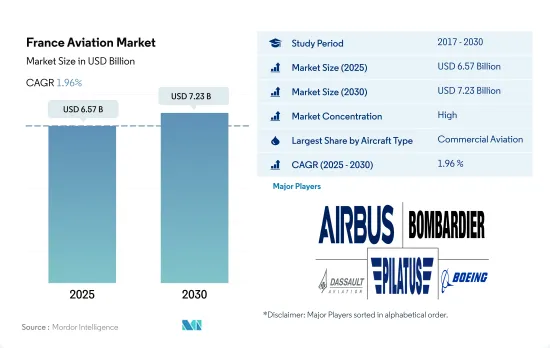

프랑스 항공 시장 규모는 2025년에 65억 7,000만 달러, 2030년에는 72억 3,000만 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 1.96%를 나타낼 전망입니다.

대기업 OEM의 존재와 민간기, 일반기, 군용기 조달 증가가 시장 성장을 견인

- 프랑스는 그 규모와 지리적 위치, 에어프랑스와 Airbus와 같은 산업 플래그십 기업의 존재로 인해 트래픽 측면에서 유럽에서 가장 크고 가장 중요한 항공 시장 중 하나입니다., 2021년에 민간 항공 부문에서 22기, 일반 항공 부문에서 7기의 비즈니스 제트기와 45기의 헬리콥터가 조달되어 2020년 대비 민간 항공 부문이 23% 증가, 일반 항공 부문이 13% 증가했습니다.

- 프랑스의 항공우주산업은 현재 시장의 불확실성과 프랑스 정부의 항공우주지원계획을 통해 기술의 대폭적인 전환을 경험하고 있으며, 이것이 프랑스에서의 이 부문의 성장을 견인하고 있습니다.

- 납품은 생산 정지나 락 다운의 영향을 받고 있지만, 이 부문은 플러스를 유지하고 있습니다. 프랑스의 일반 항공 시장은 민간 공항의 인프라 정비에 중점을 두게 되어, 국내의 부유층이 증가하고 있기 때문에 예측 기간 중에 확대할 가능성이 있습니다.

- 2020년의 COVID-19 발생시에는 비즈니스 제트의 납품이 감소했습니다.

프랑스 항공 시장 동향

국내 여행자 수요 증가가 항공 여객 수송을 견인

- 프랑스 발착 여객수로는 유럽이 최대 시장이며, 아프리카, 북미가 그 다음으로 많습니다. 유럽발 승객은 약 5,830만 명으로 전체의 71.3%를 차지했으며, 아프리카에서 프랑스에 도착한 승객은 970만 명(11.8%), 북미에서 도착한 승객은 490만 명(5.9%)이었습니다.

- 프랑스의 항공 여객 수는 2022년에 0.02% 증가했습니다. 비행 시간이 길어지면 연료 소비량이 증가하고, 특정 노선에서는 운항 비용이 급상승할 가능성이 있습니다. 항공기 승객에게 불편을 끼쳐 비행이 완전히 취소될 위험이 높아지기 때문에 승객의 신뢰를 저하시킬 가능성이 있습니다.

- 마찬가지로 프랑스의 주요 공항에서는 2020년 승객 수가 68% 이상 감소했습니다.

지정학적 위협이 국방비 증가의 원동력

- 이 나라의 국방비는 2021-2022년에 걸쳐 0.6% 급증했고, 2022년에는 536억 달러에 달했습니다. 2022년, 프랑스는 독일에 이어 유럽 제3위의 국방 지출국이었습니다.

- 프랑스 경제는 팬데믹의 영향을 받아 시정 및 여행 제한으로 경제 활동이 축소되었음에도 불구하고 프랑스 정부는 안보 능력을 확보하기 위해 2021년 국방비를 급증시켰습니다. 프랑스에서는 LPM으로 알려진 군사 계획법 2019-2025)은 국방 조치 가이드 라인과 국가 자원을 정의합니다. 여기에는 2022년까지 프랑스 국방 예산이 약 14억 7천만 달러 증가한 데 이어 2023년까지 33억 9천만 달러 증가하는 것이 포함됩니다.

- 프랑스의 국방비는 다른 유럽 국가와 주요 군사대국의 국방비에 비해 2,000년 이후 14.5%나 급증하고 있습니다. 독일의 국방비 지출은 그 이후로 21.6% 급증했습니다. 영국의 국방비는 20% 증가, 중국은 495% 증가, 미국은 61% 증가입니다. 프랑스 국방비 지출은 새로운 무기와 장비를 조달하고 기존 무기를 업그레이드하여 군대를 현대화하는 것을 강조합니다. 프랑스 정부는 2개의 주요 프로그램에 자금을 할당하고 있습니다. 즉, 프랑스-독일-스페인 미래형 전투 항공 시스템(FCAS)(약 3억 2,522만 달러)과, 차세대 전차 프로그램인 주력 지상 전투 시스템(MGCS)으로 6,567만 달러입니다.

프랑스 항공 산업 개요

프랑스 항공 시장은 상당히 통합되어 있으며 상위 5개 기업에서 103.51%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 항공 여객 수송량

- 항공화물 수송량

- 국내총생산

- 수입 여객 킬로(rpk)

- 인플레이션율

- 액티브 플릿 데이터

- 국방 지출

- 개인 부유층(hnwi)

- 규제 프레임워크

- 밸류체인 분석

제5장 시장 세분화

- 항공기 유형

- 민간 항공기

- 서브 항공기 유형별

- 화물기

- 여객기

- 바디 유형별

- 협폭동체 항공기

- 와이드 바디 기계

- 일반 여객기

- 서브 항공기 유형별

- 비즈니스 제트

- 바디 유형별

- 대형 제트기

- 소형 제트기

- 중형 제트기

- 피스톤 고정익기

- 기타

- 군용기

- 서브 항공기 유형별

- 고정익기

- 바디 유형별

- 다용도 항공기

- 훈련용 항공기

- 수송기

- 기타

- 회전익기

- 바디 유형별

- 멀티미션 헬리콥터

- 수송용 헬리콥터

- 기타

- 민간 항공기

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Airbus SE

- Bombardier Inc.

- Dassault Aviation

- Embraer

- Leonardo SpA

- Pilatus Aircraft Ltd

- Robinson Helicopter Company Inc.

- Textron Inc.

- The Boeing Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The France Aviation Market size is estimated at 6.57 billion USD in 2025, and is expected to reach 7.23 billion USD by 2030, growing at a CAGR of 1.96% during the forecast period (2025-2030).

Presence of Major OEMs and the Rising Procurement of Commercial, General, and Military Aircraft Drive the Market Growth

- France is one of the largest and most important aviation markets in Europe in terms of traffic due to its size and geographic location and the presence of some of the industry's flagships, such as Air France and Airbus. In terms of deliveries, 22 aircraft were procured in the commercial aviation segment, while seven business jets and 45 helicopters were procured in the general aviation segment in 2021, a 23% rise for commercial aviation and a 13% rise for general aviation from 2020.

- The French aerospace industry is experiencing a significant shift in technology due to the current market uncertainty and the French government's aerospace assistance plan, which is driving the growth of this sector in France. The military aviation sector has benefitted due to the increasing government investment in R&D and the procurement of advanced fighter jets, helicopters, and transport and training aircraft from the local players.

- Though the deliveries have been affected by a halt in production and lockdowns, this segment remained positive. The general aviation market in France could expand over the forecast period due to an increasing emphasis on improving the infrastructure of private airports and the increasing number of HNWIs in the country.

- During the COVID-19 outbreak in 2020, there was a decline in business jet deliveries. However, the piston fixed-wing, turboprop, and helicopter segments remained strong in terms of aircraft deliveries. In 2021, all these segments exceeded the pre-pandemic deliveries.

France Aviation Market Trends

Increased demand from domestic travelers is driving the air passenger traffic

- Europe is the biggest market for passenger flows to and from France, followed by Africa and North America. About 58.3 million passengers traveled from Europe (71.3% of the total), 9.7 million passengers reached France from Africa (11.8%), and 4.9 million passengers arrived from North America (5.9%). The contribution of the overall air transportation and its allied industries, such as airlines, to the French GDP, is around USD 87 billion.

- Air passenger numbers in France increased by 0.02% in 2022. Longer flights will cause an increase in fuel consumption and can result in a sharp increase in operating costs for certain routes. The increasing fuel costs will particularly impact airlines, therefore resulting in increased costs to passengers through higher ticket prices. Re-routing and longer flights may also cause inconvenience for air passengers, with an increased risk of flights being canceled completely and may decrease passenger confidence. The unpredictability of the situation in Ukraine is likely to be a major challenge for airlines in France and further delay the recovery in air passenger numbers.

- In 2021, the airport had a passenger movement of around 482,676 p.a. Similarly, another major airport in France had a drop of over 68% in passenger traffic during 2020. The recovery in passenger traffic with ease in travel restrictions was witnessed by the major French airlines. In 2021, around 35.8 million passengers were carried by Air France-KLM. The overall air passenger traffic is anticipated to surge during the forecast period.

Geopolitical threats are the driving factor for rising defense expenditure

- The country's defense expenditure surged by 0.6% from 2021 to 2022, with USD 53.6 billion in 2022. The defense expenditure of the country was 1.9% of the GDP. In 2022, France was the third-largest country in terms of defense expenditure in Europe after Germany. During 2017-2022, the country's defense expenditure surged by around 9%.

- Despite the French economy being impacted by the pandemic, which led to reduced economic activities due to imposed lockdowns and travel restrictions, the French government surged its defense expenditure in 2021 to ensure its security capabilities. The Military Programming Law 2019-2025, known as LPM in France, defines the defense policy guidelines and the resources for the country. It includes an increase in France's defense budget by around USD 1.47 billion by 2022, followed by an increase of USD 3.39 billion by 2023. The LPM has allotted a total of USD 334 billion to defense expenditures between 2019 and 2025.

- France's defense spending has surged by 14.5% since 2000 compared to the defense expenditures of other European nations and major military powers. For instance, Germany's defense expenditure has surged by 21.6% since then. The United Kingdom's defense expenditure surged by 20%, China's by 495%, Russia's by 183%, and the United States' by 61%. The French defense expenditure emphasizes the modernization of the armed forces by procurement of newer arms and equipment and the upgradation of the existing ones. The French government is allocating funds for two major programs, namely, the Franco-German-Spanish Future Combat Air System or FCAS (around USD 325.22 million) and the Main Ground Combat System, or MGCS, a next-generation tank program (USD 65.67 million).

France Aviation Industry Overview

The France Aviation Market is fairly consolidated, with the top five companies occupying 103.51%. The major players in this market are Airbus SE, Bombardier Inc., Dassault Aviation, Pilatus Aircraft Ltd and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-net-worth Individual (hnwi)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 By Sub Aircraft Type

- 5.1.1.1.1 Freighter Aircraft

- 5.1.1.1.2 Passenger Aircraft

- 5.1.1.1.2.1 By Body Type

- 5.1.1.1.2.1.1 Narrowbody Aircraft

- 5.1.1.1.2.1.2 Widebody Aircraft

- 5.1.2 General Aviation

- 5.1.2.1 By Sub Aircraft Type

- 5.1.2.1.1 Business Jets

- 5.1.2.1.1.1 By Body Type

- 5.1.2.1.1.1.1 Large Jet

- 5.1.2.1.1.1.2 Light Jet

- 5.1.2.1.1.1.3 Mid-Size Jet

- 5.1.2.1.2 Piston Fixed-Wing Aircraft

- 5.1.2.1.3 Others

- 5.1.3 Military Aviation

- 5.1.3.1 By Sub Aircraft Type

- 5.1.3.1.1 Fixed-Wing Aircraft

- 5.1.3.1.1.1 By Body Type

- 5.1.3.1.1.1.1 Multi-Role Aircraft

- 5.1.3.1.1.1.2 Training Aircraft

- 5.1.3.1.1.1.3 Transport Aircraft

- 5.1.3.1.1.1.4 Others

- 5.1.3.1.2 Rotorcraft

- 5.1.3.1.2.1 By Body Type

- 5.1.3.1.2.1.1 Multi-Mission Helicopter

- 5.1.3.1.2.1.2 Transport Helicopter

- 5.1.3.1.2.1.3 Others

- 5.1.1 Commercial Aviation

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Dassault Aviation

- 6.4.4 Embraer

- 6.4.5 Leonardo S.p.A

- 6.4.6 Pilatus Aircraft Ltd

- 6.4.7 Robinson Helicopter Company Inc.

- 6.4.8 Textron Inc.

- 6.4.9 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms