|

시장보고서

상품코드

1693558

중동 및 아프리카의 비료 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Middle East & Africa Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

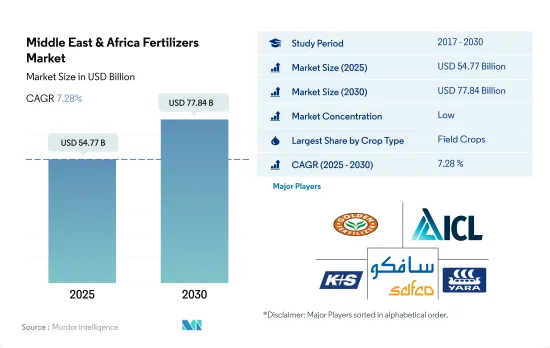

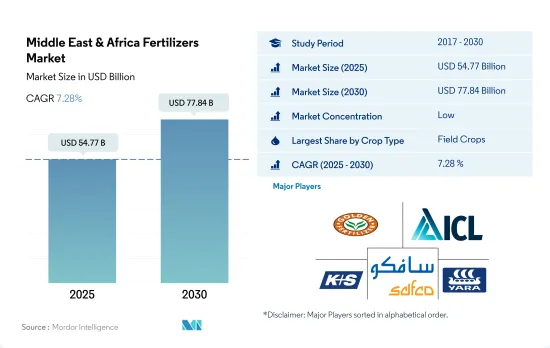

중동 및 아프리카의 비료 시장 규모는 2025년 547억 7,000만 달러로 추정되며, 2030년에는 778억 4,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 7.28%로 성장할 전망입니다.

밭작물이 재배 면적의 넓이로 시장을 독점

- 비료 시장 전체의 CAGR은 2023-2030년간 7.0%를 나타낼 것으로 추정됩니다. 농업은 아프리카에서 가장 중요한 경제활동입니다.

- 아프리카는 경작 가능한 토지가 있기 때문에 농업 생산의 중요한 중심지로 간주되고 있습니다. 그러나, 아프리카의 경작지의 6.0%밖에 관개되고 있지 않습니다.

- 중동에서는 주로 밀과 보리 등의 주식 작물이 재배되고 있습니다. 또 아프리카에서는 토마토, 마늘, 양배추, 피망, 오크라, 가지, 오이 등 다양한 야채를 자랑합니다. 특히 토마토와 양파는 북아프리카의 해안 지역에서 풍부하게 재배되고 있습니다.

- 농업 섹터는 경제 및 사회개발에 있어서 매우 중요한 역할을 하고 있지만, MENA 지역의 정책 입안자나 이해 관계자로부터는 충분한 관심을 모으고 있지 않습니다.

인구 증가와 식량 안보에 대한 우려는 이 지역의 비료 사용을 통해 해결되어야 하며 시장의 원동력이 되고 있습니다.

- 이 지역의 비료 시장은 인구 증가, 식량 안보의 필요성, 집약적 농법의 채용, 지역의 토양에 있어서의 영양 부족 등의 요인에 의해 추진되고 있습니다.

- 광대한 경작지가 있는 아프리카는 대륙에서 가장 인구가 많은 지역입니다.

- 나이지리아는 아프리카 비료 시장을 선도하고 2022년에는 12.7%의 점유율을 차지했습니다.

- 중동은 농업에 불리한 기후 조건인 것으로 알려져있으며 국내 수요를 충족시키기 위해 비료의 수입에 크게 의존하고 있습니다.

- 비료는 경제적 이익을 가져오고, 지속적으로 수량을 증가시킬 수 있지만, 입수 가능한 양에 한계가 있거나, 환경 조건이 나쁘거나 하는 과제가 있기 때문에 그 사용량은 증가의 일도를 따르고 있습니다. 이 지역에서는 인구 증가의 요구에 대응해, 식량 안보를 확보하는 것이 더욱 급선무이며 시장의 성장을 더욱 밀어붙이고 있습니다.

중동 및 아프리카 비료 시장 동향

바람과 물에 의한 침식으로 천수지와 관개지 모두 악화되어, 이 지역의 작물 재배의 과제가 되고 있습니다.

- 중동 및 아프리카에서는 옥수수, 쌀, 사탕수수, 콩 등의 농작물이 보통 4월에서 5월 사이에 심어져 9월에서 10월에 수확됩니다. 토지와 수자원은 부족하고, 천수 관개의 토지는 바람이나 물에 의한 침식으로 열화하고 있어 지속 불가능한 농법에 의해 한층 더 악화하고 있습니다. 2022년, 농작물의 재배면적은 2억 4,900만 헥타르에 달했으며, 2017년부터 3.9% 증가했습니다. 밀의 재배 면적도 현저한 증가를 나타내, 2017-2022년까지 4.6% 증가했습니다.

- 아프리카에서는 나이지리아가 사탕수수 생산량의 최상위에 서서 약간의 차이로 에티오피아가 뒤를 잇습니다. 사탕수수는 가뭄이나 샘물에 강하고, 다양한 토양 조건에 적응하기 위해, 중동이나 아프리카의 건조지대에서는 식량과 소득의 안정에 적합한 작물이 되고 있습니다.

- 이 지역의 인구는 지난 10년간 23% 이상 급증했습니다.

건조한 기후는 토양의 질소 고갈을 가속화하고 농업 생산성에 중요한 영양소가 되었습니다.

- 질소, 인, 칼륨은 식물의 성장에 필수적인 주요 영양소입니다. 질소와 인은 식물 조직의 주요 성분인 단백질과 핵산에 필수적입니다.

- 구체적으로 중동 및 아프리카 농작물에서 질소, 인, 칼륨의 평균 시용량은 각각 234.8kg/헥타르, 127.4kg/헥타르, 161.0kg/헥타르 중동 및 아프리카에서는 밀, 수수, 쌀, 옥수수 등 주요 농작물이 주로 재배되고 있습니다. 2022년 이러한 작물? ㅐ한 일차 영양분의 평균 시용량은 각각 144.5kg/헥타르, 162.9 kg/헥타르, 152.6 kg/헥타르, 245.24 kg/헥타르였습니다.

- 1차 영양소 중 중동 및 아프리카에서의 소비량은 질소가 압도적으로 많아 2022년에는 170만 톤에 달할 전망입니다. 이 우위성은 이 지역의 밭 작물 면적이 크고 전체의 약 95.0%를 차지하고 있기 때문으로, 그 결과 1차 영양소에 대한 수요가 높은 것에 의한 자급 자족을 중시해, 수입에 대한 의존도를 낮추는 것이, 이 지역에 있어서의 농작물 시장의 성장을 뒷받침하고 있습니다.

중동 및 아프리카 비료 산업의 개요

중동 및 아프리카 비료 시장은 단편화되었으며 상위 5개 기업에서 7.92%를 차지합니다. 이 시장 주요 기업은 Golden Fertilizer Company Limited, ICL Group Ltd, K+S Aktiengesellschaft, SABIC Agri-Nutrients Co.,Yara International ASA입니다(알파벳순).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 주요 작물의 작부 면적

- 밭 작물

- 원예 작물

- 평균 양분 시용률

- 미량 영양소

- 밭 작물

- 원예 작물

- 1차 영양소

- 밭 작물

- 원예 작물

- 2차 다량 영양소

- 밭 작물

- 원예 작물

- 미량 영양소

- 관개 농지

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 유형

- 복합형

- 스트레이트

- 미량 영양소

- 붕소

- 구리

- 철

- 망간

- 몰리브덴

- 아연

- 기타

- 질소

- 질산암모늄

- 우레아

- 기타

- 인산

- DAP

- MAP

- SSP

- TSP

- 기타

- 칼륨

- MoP

- SoP

- 기타

- 2차 영양소

- 칼슘

- 마그네슘

- 유황

- 형태

- 기존

- 특수

- CRF

- 액체 비료

- SRF

- 수용성

- 시비 모드

- 시비

- 엽면 살포

- 토양

- 작물 유형

- 밭작물

- 원예작물

- 잔디 및 관상용

- 생산국

- 나이지리아

- 사우디아라비아

- 남아프리카

- 튀르키예

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Foskor

- Gavilon South Africa(MacroSource, LLC)

- Golden Fertilizer Company Limited

- ICL Group Ltd

- KS Aktiengesellschaft

- Kynoch Fertilizer

- SABIC Agri-Nutrients Co.

- Safsulphur

- Unikeyterra Chemical

- Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Middle East & Africa Fertilizers Market size is estimated at 54.77 billion USD in 2025, and is expected to reach 77.84 billion USD by 2030, growing at a CAGR of 7.28% during the forecast period (2025-2030).

Field crops dominated the market owing to their larger cultivation area

- The overall fertilizer market is estimated to register a CAGR of 7.0% from 2023 to 2030. Agriculture is by far the single most important economic activity in Africa. It provides employment for about two-thirds of the continent's working population, and for each country, it contributes an average of 30-60% of the gross domestic product and 30.0% of the value of exports.

- Africa is regarded as a key center of agricultural production because of the availability of arable land. However, only 6.0% of cultivated land in Africa is irrigated. In 2018, Sub-Saharan Africa's average fertilizer consumption stood at 17.0 kg of nutrients per hectare, significantly lower than the global average of 135.0 kg/ha.

- The Middle East predominantly cultivates staple crops like wheat and barley. Additionally, Egypt and Saudi Arabia lead in the production of rice, maize, lentils, chickpeas, vegetables, and fruits. Africa, on the other hand, boasts a diverse vegetable range, including tomatoes, onions, cabbages, peppers, okra, eggplants, and cucumbers. Notably, tomatoes and onions thrive in abundance along North Africa's coastal regions. Africa's notable beverage crops encompass tea, coffee, cocoa, and grapes.

- While the agricultural sector plays a pivotal role in economic and social development, it has not garnered sufficient attention from policymakers and stakeholders in the MENA region. Despite its modest GDP contribution, agriculture holds strategic importance for sustainable development in MENA countries, which is expected to fuel the fertilizers market in the coming years.

The growing population and concern regarding food security need to be addressed through fertilizer use in the region, drive the market

- The fertilizer market in the region is being propelled by factors such as a growing population, the need to ensure food security, the adoption of intensive agricultural practices, and nutrient deficiencies in regional soils. It is projected to witness a value CAGR of 7.0% during 2023-2030.

- Africa, with its vast arable land, boasts the highest population on the continent. For instance, the Sub-Saharan African region is home to 13% of the global population and controls roughly 20% of the world's agricultural land. However, the region grapples with significant food insecurity, largely due to its increasing reliance on fertilizers.

- Nigeria leads the fertilizer market in Africa, commanding a share of 12.7% in 2022. With over 70 blending plants and major urea production facilities, the country is poised to become a fertilizer powerhouse, even competing globally in the urea market. This surge in production has led to cost reductions and increased availability, driving higher adoption rates among farmers.

- The Middle East, known for its unfavorable climatic conditions for farming, heavily relies on fertilizer imports to meet its domestic needs. Consequently, the region witnesses a comparatively higher adoption of fertilizers to cater to both domestic and international demands.

- While fertilizers offer economic benefits and can boost yields sustainably, their usage is on the rise due to challenges like limited availability and adverse environmental conditions. The region's imperative to address the needs of a growing population and ensure food security further fuels the market's growth.

Middle East & Africa Fertilizers Market Trends

Deterioration of both rain-fed and irrigated lands due to erosion caused by wind and water will pose a challenge in cultivating crops in the region.

- In the Middle East and Africa, field crops such as corn, rice, sorghum, and soybeans are typically planted between April and May and harvested from September to October. The agricultural sector in this region faces significant challenges. Land and water resources are scarce, and both rain-fed and irrigated lands are deteriorating due to erosion from wind and water, exacerbated by unsustainable farming practices. Field crops dominate the agricultural landscape, occupying around 90% of the total agricultural land in the region. In 2022, the cultivation area for field crops reached 249 million hectares, marking a 3.9% increase from 2017. Corn alone commands a significant share, covering 17.8% of the total field crop area. Wheat cultivation also saw a notable increase, with a 4.6% increase from 2017 to 2022. Specifically, the corn cultivation area in the region reached 44.3 million hectares in 2022.

- In Africa, Nigeria takes the lead as the top sorghum producer, closely followed by Ethiopia. Sorghum, a staple cereal crop, dominates the agricultural landscape in Nigeria, accounting for 50% of the total cereal output and occupying approximately 45% of the land dedicated to cereal production. Sorghum's resilience to drought and waterlogging, coupled with its adaptability to diverse soil conditions, makes it a preferred choice for food and income security in the drier regions of the Middle East and Africa.

- The region's population has surged by over 23% in the past decade. While food imports are projected to rise due to limited production capacity, the agricultural industry has shown consistent growth, paralleled by an expansion in cultivated land.

The arid climate leads to a faster depletion of nitrogen in the soil, making it a crucial nutrient for agricultural productivity.

- Nitrogen, phosphorous, and potassium are primary nutrients crucial for plant growth. Nitrogen and phosphorous are integral to proteins and nucleic acids, key components of plant tissue. Meanwhile, potassium significantly influences the quality of harvested crops. Field crops, on average, receive an application rate of 174.4 kg per hectare for these primary nutrients.

- Specifically, the average application rates for nitrogen, phosphorous, and potassium in field crops across the Middle East & Africa stood at 234.8 kg/hectare, 127.4 kg/hectare, and 161.0 kg/hectare, respectively. The Middle East & Africa predominantly cultivate major field crops like wheat, sorghum, rice, and corn. In 2022, the average application rates for primary nutrients in these crops were 144.5 kg/hectare, 162.9 kg/hectare, 152.6 kg/hectare, and 245.24 kg/hectare, respectively.

- Of the primary nutrients, nitrogen dominates consumption in the Middle East & Africa, reaching 1.7 million metric tons in 2022. Nitrogen is the most crucial nutrient for crop yields, and given the prevalent deficiency of nitrogen in regional soils, it has become the most widely applied fertilizer. This dominance is driven by the region's substantial field crop area, comprising around 95.0% of the total, and the resulting high demand for primary nutrients. This emphasis on self-sufficiency and reducing import reliance underscores the growing market for field crops in the region.

Middle East & Africa Fertilizers Industry Overview

The Middle East & Africa Fertilizers Market is fragmented, with the top five companies occupying 7.92%. The major players in this market are Golden Fertilizer Company Limited, ICL Group Ltd, K+S Aktiengesellschaft, SABIC Agri-Nutrients Co. and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Urea

- 5.1.2.2.3 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

- 5.5 Country

- 5.5.1 Nigeria

- 5.5.2 Saudi Arabia

- 5.5.3 South Africa

- 5.5.4 Turkey

- 5.5.5 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Foskor

- 6.4.2 Gavilon South Africa (MacroSource, LLC)

- 6.4.3 Golden Fertilizer Company Limited

- 6.4.4 ICL Group Ltd

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Kynoch Fertilizer

- 6.4.7 SABIC Agri-Nutrients Co.

- 6.4.8 Safsulphur

- 6.4.9 Unikeyterra Chemical

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms