|

시장보고서

상품코드

1693576

유럽의 일반 항공 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe General Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

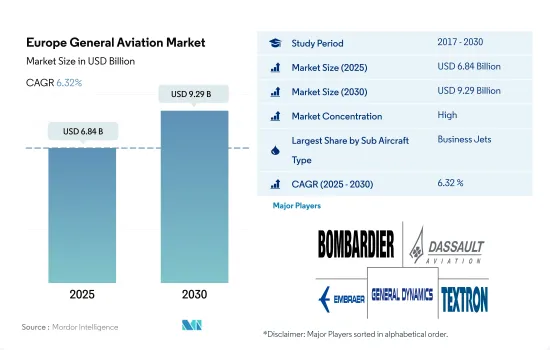

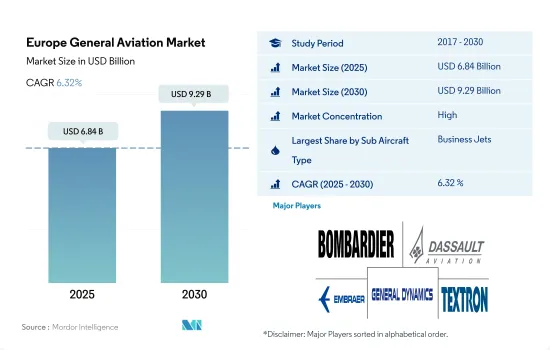

유럽의 일반 항공 시장 규모는 2025년 68억 4,000만 달러로 추정되고, 2030년에는 92억 9,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR 6.32%를 나타낼 것으로 예측됩니다.

팬데믹 후 출장 비행 시간이 증가해 비즈니스 제트에 대한 높은 수요가 발생합니다.

- 비즈니스 제트기는 유럽의 경영진이나 기업에 소규모 공항에 직접 액세스하여 민간 항공편과 관련된 시간이 많이 소요되는 프로세스를 피합니다. 2022년 12월 현재, 유럽은 세계의 비즈니스 제트기 보유 대수의 약 16%를 차지하고 있습니다.

- COVID-19의 유행은 이 지역의 비즈니스 제트기 납품에 악영향을 미쳤으며, 2020년에는 2021년 대비 26% 감소했습니다.

- 납입 실적에서는 2017년부터 2022년까지 대형 제트기 부문이 53%의 점유율을 차지했고 소형 제트기가 35%, 중형 제트기가 12%였습니다. 2022년 12월 현재 유럽의 비즈니스 제트기 보유 대수에서는 Cessna가 30%를 차지하고, Bombardier가 19%, Dassault가 14%로 이어졌습니다. 이 지역에서 UHNWI의 급증은 비즈니스 제트 부문을 뒷받침할 것으로 예상됩니다.

이 지역의 비즈니스 항공 수요는 유럽 일반 항공 부문을 지원할 것으로 예상됩니다.

- 유럽에서는 개인 여행과 출장에 개인 제트기와 헬리콥터를 선호하는 HNWI와 UHNWI가 증가하여 일반 항공 부문의 항공기 조달에 공헌했습니다. 2022년 유럽의 UHNWI 수는 2021년 대비 5% 증가했습니다. 2017년부터 2022년까지 세계의 HNWI 인구의 67%를 나타내고, 초부유층의 3번째의 대폭적인 증가를 기록했습니다.

- 2021년, 에어차터 서비스 제공업체는 기업 항공의 신규 회원이 급증함에 따라 유럽 전역에서 높은 수요를 목격했습니다. 2021년 상반기의 신규 회원수가 2020년 상반기와 비교해 약 53%의 성장을 기록했습니다.

- 유럽의 주요 전세 서비스 제공업체에 따르면 2021년 말에 수요가 크게 증가했으며 2019년 트래픽 수준을 초과할 수 있었습니다. 2021년 8월 이후 2019년에 비해 약 20-30% 증가하고 있습니다.

- 현재의 운항기재에 대해서는 독일이 유럽 비즈니스 제트기의 약 18%를 차지하는 주요국이 되고 있습니다.

유럽 일반 항공기 시장 동향

HNWI 인구 증가는 시장의 주요 성장 촉진요인으로

- HNWI(부유층)와 UHNWI(초부유층)는 개인 여행이나 출장을 위해 프라이빗 제트를 소유하는 경우가 많습니다. 2022년 유럽의 UHNWI 수는 2021년에 비해 5% 증가했습니다. 유럽은 2017년부터 2022년까지 세계의 HNWI 인구의 67%를 나타내고, 초부유층의 3번째의 큰 증가를 기록했습니다.

- HNWI의 수와 자산 측면에서 유럽이 주도적인 지위를 차지하는 것은 주로 독일, 프랑스, 영국에 기인합니다. HNWI 인구는 독일이 350만명으로 가장 많았고, 이어 프랑스가 307만명, 영국이 290만명이었습니다. HNWI 인구의 성장이 가장 적은 것은 러시아로, 2%를 기록했습니다. 이것은 과거 10년간, 부유층이 매년 러시아 국외에 유출하고 있기 때문에 러시아가 현재 직면하고 있는 문제가 나타난 것입니다. 세계 경제, 특히 인플레이션과 금융시장에 리스크를 가져왔습니다. 그러나 시장은 예측기간 중에 회복될 것으로 예상됩니다.

유럽 일반 항공 산업 개요

유럽의 일반 항공 시장은 상당히 통합되어 있으며 상위 5개사에서 74.10%를 차지하고 있습니다. 이 시장 주요 기업은 Bombardier Inc., Dassault Aviation, Embraer, General Dynamics Corporation, Textron Inc.입니다(알파벳순).

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 부유층(HNWI)

- 규제 프레임워크

- 밸류체인 분석

제5장 시장 세분화

- 서브 항공기 유형

- 비즈니스 제트

- 대형 제트기

- 소형 제트기

- 중형 제트기

- 피스톤 고정익기

- 기타

- 비즈니스 제트

- 국가명

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 튀르키예

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Airbus SE

- Bombardier Inc.

- Cirrus Design Corporation

- Daher

- Dassault Aviation

- Diamond Aircraft

- Embraer

- General Dynamics Corporation

- Leonardo SpA

- PIAGGIO AERO INDUSTRIES SpA

- Pilatus Aircraft Ltd

- Robinson Helicopter Company Inc.

- Tecnam Aircraft

- Textron Inc.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe General Aviation Market size is estimated at 6.84 billion USD in 2025, and is expected to reach 9.29 billion USD by 2030, growing at a CAGR of 6.32% during the forecast period (2025-2030).

Increase In Business Travel Flight Hours After The Pandemic Generated A High Demand For Business Jets

- Business jets offer European executives and corporations direct access to smaller airports and avoid the time-consuming processes associated with commercial flights. These jets enable busy executives to maximize their productivity and reduce travel-related disruptions. As of December 2022, Europe accounted for around 16% of the global business jet fleet. Germany led the region with 18% of the total European business jet fleet, followed by the United Kingdom and France, with around 12% and 7%, respectively.

- The COVID-19 pandemic adversely impacted business jet deliveries in the region, with a decline of 26% in 2020 compared to 2021. There has been a shift toward private flying as a safer mode of transportation among the HNWI population in the region, aiding in procuring business jets. However, the market gradually recovered from the pandemic, and in 2022, the region recorded 34% growth compared to 2020.

- In terms of deliveries, during 2017-2022, the large jet segment dominated the region with 53% of the share, followed by light and mid-size jets with 35% and 12%, respectively. During the same period, the OEM that delivered most of the business jets was Embraer, with 11% of the total jets delivered in the region, followed by Cessna with 10% of jets delivered, Bombardier delivered 9% of the jets, and Gulfstream delivered 7% of the jets. Cessna was the leading OEM, with 30% of the current operational fleet size, followed by Bombardier and Dassault, with 19% and 14%, respectively, in the European business jet fleet as of December 2022. The surge in UHNWI individuals in the region is expected to aid the business jet segment. Around 1,244 aircraft are expected to be delivered between 2023 and 2030

The Demand For Business Aviation In The Region Is Expected To Aid The European General Aviation Sector

- The rise of HNWIs and UHNWIs, who prefer private jets and helicopters for personal or business travel in Europe, aided in the procurement of aircraft in the general aviation sector. From 2017 to 2022, the HNWI population in the region increased by 67%. The surge in the HNIW population has also aided in the growth of the general aviation sector in the region. In 2022, the number of UHNWIs in Europe increased by 5% compared to 2021. This was because the Eurozone utilities, tech stocks, and luxury goods sectors performed well, registering solid gains. Europe recorded the third significant rise in the ultra-wealthy population, which recorded 67% of the global HNWI population during 2017-2022.

- In 2021, air charter service providers witnessed high demand across Europe with the surge in new memberships for business aviation. For instance, in 2021, a major Europe-based air charter service provider, VistaJet, registered a growth of around 53% in new memberships during H1 2021 compared to H1 2020. Out of the new memberships, more than 50% belong to the European region.

- According to the major charter service providers in Europe, demand increased significantly toward the end of 2021 and managed to surpass 2019 levels of traffic. Business aviation traffic has been approximately 20-30% more than in 2019 since August 2021. Due to such strong demand, charter jet service companies are expanding their fleets to meet the growing demand.

- Regarding the current operational fleet, Germany is the leading country with around 18% of the European business jet fleet. The United Kingdom and France accounted for approximately 11% and 9%, respectively, of the European fleet as of December 2022. During 2023-2030, around 5,062 general aviation aircraft are expected to be delivered.

Europe General Aviation Market Trends

Rise in the HNWI population acting as the major growth driver for the market

- HNWIs and UHNWIs often own private jets for personal or business travel. Europe is home to a multitude of scenic and exclusive destinations that may not be easily accessible through commercial flights. Business jets provide the opportunity for HNWIs to fly directly to remote locations, avoiding congested airports and time-consuming connections. In 2022, the number of UHNWIs in Europe increased by 5% compared to 2021. This was because the Eurozone utilities, tech stocks, and luxury goods sectors performed well, registering solid gains. Europe recorded the third significant rise in the ultra-wealthy population, which recorded 67% of the global HNWI population during 2017-2022.

- The leading position of Europe in terms of the number and assets of HNWIs is mainly attributed to Germany, France, and the United Kingdom. In 2022, these three countries alone recorded 67% of the total HNWIs in Europe. Germany led the HNWI population with 3.5 million HNWIs, followed by France with 3.07 million and the United Kingdom with 2.9 million. The United Kingdom attracts a steady stream of high-net-worth individuals from Africa, Asia, and the Middle East. Russia saw the least growth in the HNWI population, which recorded 2%. This was because well-off people have been moving out of Russia every year for the past 10 years, a sign of the current issues the country is facing. The crisis in Ukraine posed risks to the global economy, especially to inflation and financial markets. However, the market is expected to recover during the forecast period. In 2030, the HNWI population is expected to grow by 18.4 million.

Europe General Aviation Industry Overview

The Europe General Aviation Market is fairly consolidated, with the top five companies occupying 74.10%. The major players in this market are Bombardier Inc., Dassault Aviation, Embraer, General Dynamics Corporation and Textron Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 High-net-worth Individual (hnwi)

- 4.2 Regulatory Framework

- 4.3 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Aircraft Type

- 5.1.1 Business Jets

- 5.1.1.1 Large Jet

- 5.1.1.2 Light Jet

- 5.1.1.3 Mid-Size Jet

- 5.1.2 Piston Fixed-Wing Aircraft

- 5.1.3 Others

- 5.1.1 Business Jets

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Italy

- 5.2.4 Netherlands

- 5.2.5 Russia

- 5.2.6 Spain

- 5.2.7 Turkey

- 5.2.8 UK

- 5.2.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Cirrus Design Corporation

- 6.4.4 Daher

- 6.4.5 Dassault Aviation

- 6.4.6 Diamond Aircraft

- 6.4.7 Embraer

- 6.4.8 General Dynamics Corporation

- 6.4.9 Leonardo S.p.A

- 6.4.10 PIAGGIO AERO INDUSTRIES S.p.A

- 6.4.11 Pilatus Aircraft Ltd

- 6.4.12 Robinson Helicopter Company Inc.

- 6.4.13 Tecnam Aircraft

- 6.4.14 Textron Inc.

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록