|

시장보고서

상품코드

1693596

GRC 클래딩 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)GRC Cladding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

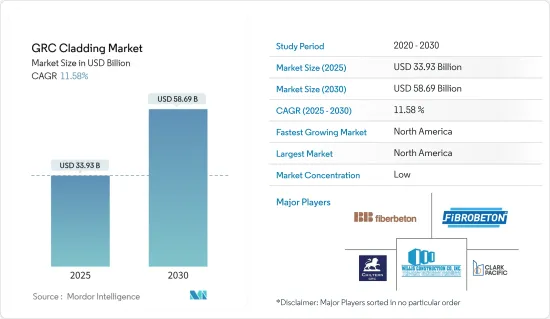

세계의 GRC 클래딩 시장 규모는 2025년 339억 3,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 11.58%로 확대되어, 2030년에는 586억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 유리 섬유 강화 콘크리트(GRC)는 주로 건축 구조물의 근교 패널로서 사용되는 경량 클래딩 패널입니다. 섬유로 보강된 콘크리트는 일반적인 콘크리트와 비교해 환경 개선으로 이어진다고 자주 소개됩니다.

- GRC 클래딩 시장은 그린 빌딩(LEED 평가)의 중시의 고조에 의해 견인되고 있어 뛰어난 기계적 특성이 시장 성장의 원동력이 될 것으로 기대되고 있습니다.

- 미국과 영국은 시멘트의 배합이 연소의 위험을 감수할지 어떨지에 대해 엄격한 가이드라인을 정하고 있습니다.

- GRC는 폴리머와 섬유의 특수 배합에 의해 불침투성, 내후성, 난연성이 뛰어나기 때문에 내화성과 불연성에 효과적입니다.

- GRC는 다른 재료에 없는 다양한 장점이 있습니다. GRC는 가볍고, 보다 유연하며, 내구성이 뛰어나고, 내화성이 뛰어난 진정한 대체 시멘트입니다.

- GRC는 그 성질상, 락울을 도포하는 것으로 차열, 차수, 차음 효과를 발휘합니다. 이 특성에 의해 극단적인 기상 조건의 지역에서는 수요가 높아질 가능성이 있습니다.

- 클래딩 패널과 같은 대형 GRC 제품은 스프레이를 사용하여 제조됩니다.

- 급속히 현재화하고 있는 기후 변화에 의한 긴급사태를 받고, 주택건축물의 내진성을 향상시키기 위해, 캐나다 국가조사위원회는 국가건축기준법(2025년)에 극단적인 기상현상에 견디는 기후 변화에 강한 건축물의 가이드라인을 도입했습니다.

GRC 클래딩 시장 동향

상업 공간 수요 급증이 시장을 견인

최근 조사에 따르면 사무실 공간 수요는 2024년 말까지 12-18% 증가할 것으로 예상됐습니다.

최근의 은행 위기는 상업용 부동산에 긴 그림자를 떨어뜨리고 있습니다. 곤경과 은행의 파탄이 서로 보강한다는 '파멸의 루프' 시나리오가 우려되고 있습니다. 부동산 시장 대부분이 상승세를 보이고 있기 때문에 이는 이상하게 보일 수도 있습니다. 그러나 어느 한 쪽을 무너뜨릴 수 없기 때문입니다. 대체 대출과 사모펀드가 화제가 되고 있지만, 은행 대출의 인하는 향후 수년간 상환이 필요한 거액의 부채를 생각하면 득책이 아닙니다.

미국 시장에는 경기 순환이나 구조적인 문제 등 많은 과제가 있지만, 다른 지역의 사무실 가동률에 대해서는 낙관시할 수 있는 이유가 많습니다. 예를 들어, 유럽에서는 사무실의 평균 가동률이 2022년 43%에서 55%로 회복되었으며 주 중반 가동률은 COVID-19 이전의 평균(70%)에 가깝습니다. 많은 아시아태평양 시장(서울, 도쿄 등)에서 사무실 가동률은 유행 전 수준으로 거의 돌아왔습니다. 아시아태평양에서는 고품질 건물공급이 제한되어 있기 때문에 공실률이 낮게 유지되고 임대료가 상승하고 있습니다.

인도에서는 2023년 1분기 공급이 전년 동기 대비 23% 감소했음에도 불구하고 상업공간 공급은 회복되었으며 2023년 3분기에는 약 4,700만-4,900만 평방 피트에 달할 것으로 예측됐습니다. 순흡수량을 바탕으로 2023년 공급량은 유행 전 2017년부터 2019년의 평균을 초과할 것으로 예측됐습니다. 2024년 공급량은 연률 22% 증가한 5,800만-6,000만 평방 피트로 예측됐습니다. 품질에 대한 도피는 기관 투자자 소유자와 기존 개발자 빌딩에 대한 수요의 양극화를 촉진합니다.

북미가 시장을 독점할 전망

창고 및 유통업은 상업 분야 중에서도 수요가 높고, 최근에는 미국의 상업 투자의 절반 이상을 차지하기까지 증가하고 있습니다.

오피스 시장이 계속 활발해지고 있는 가운데, 향후의 리싱 활동은 가장 인기가 높은 서브 마켓이나 클래스 A빌딩의 소규모 공간에 집중할 가능성이 높습니다. 대형 점포는 공간을 집약하고 전자상거래와 인프라에 대한 투자를 진행하고 있습니다.

헬스케어의 건설 지출은 2023년까지 높은 수준을 유지했으며, 대규모 병원 확장과 외래 환자 및 의료 사무실 수요 회복이 그 원동력이 되었습니다. 대규모 프로젝트는 최근 인구 역학 변화, 용량, 유지 보수 요구, 의료 서비스에 영향을 미치는 신기술(웨어러블 및 원격 의료 등)에 의해 지원되었습니다.

대규모의 신설시설에서는 프로젝트의 스케줄과 예산을 합리화하기 위해 조립식과 모듈화가 점차 진행될 것으로 예상되고 있으며, 이와는 대조적으로 전문의료시설과 간호시설(SCH)은 여전히 자원에 큰 제약을 받고 있으며, 건설활동이 제한되고 있습니다.

교회의 폐쇄는 개관을 웃도는 페이스로 진행되고 있어 개축이나 재이용의 새로운 기회가 태어나고 있습니다. 인프라와 교통기관에 대한 투자는 가장 경쟁이 치열한 시장의 일부로, 오락 및 레크리에이션 시설의 건설에의 지출을 지지하는 것으로 예상됩니다.

GRC 클래딩 산업 개요

본 보고서에서는 GRC 클래딩 시장에서 사업을 전개하는 주요 국제 기업을 다루고 있습니다.

GRC 코팅재 시장의 주요 기업은 UltraTech Cement Ltd, Clar Pacific, BB Fiberbeton, Asahi Building-wall, Willis Construction Co. Inc., Loveld, Fibrobeton, GB Architectural Cladding Products Ltd, Ibstock Telling, BCM GRC Limited 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 성과

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학과 인사이트

- 시장 개요

- 시장 성장 촉진요인

- 시장을 견인하는 주택 부문 수요 증가

- 도시화의 진전이 시장을 견인

- 시장 성장 억제요인

- 시장 성장을 방해하는 임대료 증가

- 시장 기회

- 시장을 견인하는 건설 업계의 성장

- 공급체인/가치체인 분석에 대한 통찰

- 업계의 매력도 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 정부의 규제와 대처

- 기술 동향

- 시장에 대한 COVID-19의 영향

제5장 시장 세분화

- 용도별

- 상업건설

- 주택건설

- 인프라 건설

- 지역별

- 아시아태평양

- 북미

- 유럽

- 남미

- 중동 및 아프리카

제6장 경쟁 구도

- 시장 집중도 개요

- 기업 프로파일

- UltraTech Cement Ltd

- Clark Pacific

- BB Fiberbeton

- ASAHI BUILDING-WALL CO. LTD

- Willis Construction Co. Inc.

- Loveld

- Fibrobeton

- GB Architectural Cladding Products Ltd

- Ibstock Telling

- BCM GRC Limited

- 기타 기업

제7장 시장의 미래

제8장 부록

JHS 25.05.09The GRC Cladding Market size is estimated at USD 33.93 billion in 2025, and is expected to reach USD 58.69 billion by 2030, at a CAGR of 11.58% during the forecast period (2025-2030).

Key Highlights

- Glass-reinforced concrete cladding (GRC) is a lightweight cladding panel primarily used as fascia panels in building structures. Concrete, reinforced with fibers, is often presented as an environmental improvement compared to typical concrete.

- The GRC cladding market is driven by the increased emphasis on green buildings (LEED ratings), and superior mechanical characteristics are expected to drive the market's growth. In the United Kingdom, building regulations state that the materials used for external wall construction or wall cladding should not be a medium for spreading fire.

- The United States and the United Kingdom have stringent guidelines on whether cement formulations can run the risk of combustion. This increased the need for a more fire-resistant material for wall cladding.

- GRC is effective at fire resistance and incombustibility because the mix's special blend of polymers and fibers makes it impermeable, weather-resistant, and fire-retardant.

- GRC has many different advantages that come with its use over other materials. It is a genuinely amazing cement alternative that is lighter, stronger, more flexible, more durable, and fire-resistant.

- Due to its nature, GRC, water, and sound insulation provide thermal insulation by applying rock wool. This property may lead to increased demand in regions with extreme weather conditions.

- Larger GRC products, like cladding panels, are manufactured using a spray. Sprayed GRC is generally stronger than premix vibration-cast GRC.

- In the wake of the rapidly emerging climate change emergency and to help improve resiliency in residential buildings, the National Research Council, Canada, has introduced guidelines in the National Building Code (2025) for climate-resilient construction to withstand extreme weather events.

GRC Cladding Market Trends

The Surge in the Demand for Commercial Spaces is Driving the Market

According to a recent study, the demand for office space will increase by 12-18% by the end of 2024. The growth is expected to be driven by the current fiscal year, the gradual return of office tenants, and the improving macroeconomic environment.

The recent banking crisis has cast a long shadow on commercial real estate. Unburdened by the regulations of their larger 'systemically important' peers, US regional banks have been aggressively lending against commercial property. This raises the specter of a 'doom-loop' scenario, where real estate woes and banking failures reinforce each other. This may seem far-fetched, as much of the real estate market continues to outperform. However, this is because neither can bring the other down. For all the talk of alternative lenders and private equity, a pullback on bank lending (which continues to account for 50% to 60% of total commercial real estate lending) is ill-advised, given the massive amounts of debt that will need to be repaid over the next several years. Refinancing has already been challenging, and it is only likely to become more so as credit standards tighten.

While there are many challenges to the US market in terms of cyclicality and structural issues, there are many reasons to be optimistic about office occupancies in other regions. For example, in Europe, average office occupancies recovered to 55% compared to 43% in 2022, and midweek rates are now close to the pre-COVID-19 average (70%). In many Asia-Pacific markets (Seoul, Tokyo, etc.), office attendance is almost back to where it was before the pandemic. In Asia-Pacific, a limited supply of high-quality buildings keeps vacancy low and pushes up rents.

In India, despite a year-over-year decline of 23% in supply in Q1 2023, the supply of commercial spaces was projected to pick up and reach around 47-49 million square feet by Q3 2023. Based on net absorption, the 2023 supply was projected to be above the average of 2017-2019 before the pandemic. In 2024, supply is projected to grow by 22% yearly to 58-60 million square feet. A flight to quality drives demand polarization toward institutional owners and established developer buildings.

North America is Expected to Dominate the Market

Warehouse and distribution, a commercial segment, is in high demand and has increased in recent years to account for more than half of US commercial investment.

As the office market continues to boom, future leasing activity will likely focus on smaller spaces in the most sought-after submarkets and class-A buildings. Big-box stores are consolidating their space and investing in e-commerce offerings and infrastructure.

Healthcare construction spending remained high through 2023, driven by large-scale hospital expansions and outpatient and medical office demand recovery. Large-scale projects were supported by recent changes in demographics, capacity, maintenance needs, and new technologies that affect health services (such as wearables and telehealth).

Large-scale new facilities are expected to increasingly use prefabrication and modularization to streamline project schedules and budgets. In contrast, specialty care and nursing home (SCH) facilities remain heavily constrained by resources, limiting construction activity.

Churches are closing at a faster rate than they are opening, which is creating new opportunities for renovation or repurposing. Investments in infrastructure and transportation will support spending on the construction of amusement and recreational facilities in some of the most competitive markets.

GRC Cladding Industry Overview

The report covers major international players operating in the GRC cladding market. The market is highly fragmented, with large companies claiming significant market share. Key players engage in collaborations, innovations, business expansion, awards and recognition, and other strategies to improve their offerings and remain competitive.

Some of the key players in the GRC cladding market are UltraTech Cement Ltd, Clark Pacific, BB Fiberbeton, Asahi Building-wall Co. Ltd, Willis Construction Co. Inc., Loveld, Fibrobeton, GB Architectural Cladding Products Ltd, Ibstock Telling, BCM GRC Limited, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand in the Residential Segment Driving the Market

- 4.2.2 Increasing Urbanization Driving the Market

- 4.3 Market Restraints

- 4.3.1 Increasing Rents Hindering the Growth of the Market

- 4.4 Market Opportunities

- 4.4.1 Growing Construction Industry Driving the Market

- 4.5 Insights into Supply Chain/Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Government Regulations and Initiatives

- 4.8 Technological Trends

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Commercial Construction

- 5.1.2 Residential Construction

- 5.1.3 Infrastructure Construction

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.2 North America

- 5.2.3 Europe

- 5.2.4 South America

- 5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 UltraTech Cement Ltd

- 6.2.2 Clark Pacific

- 6.2.3 BB Fiberbeton

- 6.2.4 ASAHI BUILDING-WALL CO. LTD

- 6.2.5 Willis Construction Co. Inc.

- 6.2.6 Loveld

- 6.2.7 Fibrobeton

- 6.2.8 GB Architectural Cladding Products Ltd

- 6.2.9 Ibstock Telling

- 6.2.10 BCM GRC Limited*

- 6.3 Other Companies