|

시장보고서

상품코드

1693651

유럽의 전기자동차 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

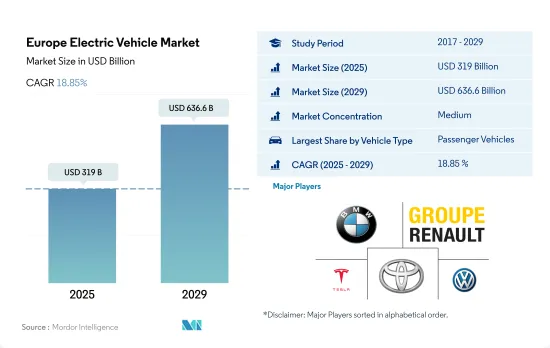

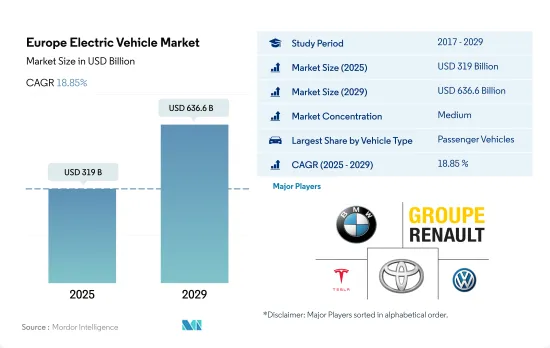

유럽의 전기자동차 시장 규모는 2025년에 3,190억 달러로 추정되고, 2029년에는 6,366억 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2029년) CAGR은 18.85%를 나타낼 전망입니다.

물류, 공급망, 인프라, 건설 부문의 성장과 대중교통 서비스의 증가는 유럽 전기차 시장을 강화하고 있습니다.

- 상업용 차량에 대한 수요는 향후 몇 년 동안 크게 증가할 것으로 예상됩니다. 이러한 성장의 주요 동인으로는 물류, 공급망, 인프라, 건설 부문이 있습니다.

- 유럽 전역에서 현대자동차와 H2 에너지의 파트너십과 같은 신제품 출시와 전략적 협업이 전기 트럭 판매를 촉진할 것으로 보입니다. 현대자동차는 2019년 9월 스위스와 유럽에서 친환경 수소 생태계를 육성한다는 비전을 가지고 현대 하이드로젠 모빌리티(HHM)를 설립했습니다. HHM은 2025년까지 1,600대의 연료전지 전기 대형 트럭을 도입한다는 야심찬 목표를 세웠습니다.

- 2021년 독일 대중교통 부문의 전기 버스 수는 전년 689대에서 60% 급증한 1,269대를 기록하며 거의 두 배로 증가했습니다. 이 중 586대는 배터리 전기 차량이었으며, 연료 전지를 사용하거나 다른 기술을 활용한 차량은 소수에 불과했습니다. 또한 독일의 현지 운송 회사와 정부 기관은 2025년까지 3,000대 이상의 전기 버스를 추가할 계획을 가지고 있습니다.

유럽의 전기자동차 시장은 인센티브, 인프라, 소비자 선호도에 따라 국가별로 차이가 있는 것이 특징입니다.

- 유럽은 전 세계에서 가장 큰 전기자동차 제조업체 중 하나입니다. 또한 전 세계적으로 전기 모빌리티를 가장 빠르게 도입하고 있는 국가 중 하나입니다. 전기자동차의 경우, 2023년 유럽에서 새로 등록된 전체 자동차 중 8.3%가 완전 전기 승용차로 가장 큰 비중을 차지할 것으로 예상됩니다.

- 신제품 출시와 새로운 브랜드의 진입이 유럽 승용차 시장을 견인할 것으로 예상됩니다. 2022년 2월, 중국 자동차 제조업체인 Xpeng이 스웨덴의 전기 승용차 시장에 첫 전기차인 P7과 P5 세단을 출시했습니다. 2022년 6월, 미국 자동차 제조업체 포드는 2030년까지 유럽에서 전기자동차만 생산 및 판매하겠다고 발표했습니다.

- 배터리 전기자동차에 2,950유로의 보조금을 지급하고 중고 배터리 전기자동차에 약 2,000유로의 보조금을 지급할 예정입니다. 하지만 차량 가격은 최소 12,000유로에서 최대 45,000유로여야 합니다.

유럽의 전기자동차 시장 동향

환경 문제, 정부 지원, 탈탄소화 목표가 유럽 전기자동차 수요와 판매를 촉진합니다.

- 유럽 국가의 전기차 수요와 판매량은 지난 몇 년 동안 크게 성장했습니다. 독일은 2021년 대비 2022년 전기차 판매량이 22% 증가했으며, 영국은 2021년 대비 2022년 18.40%의 증가율을 보였습니다. 환경에 대한 관심 증가, 엄격한 정부 규범, 연비, 낮은 유지비, 탄소 배출 없음, 정부의 보조금 등 전기자동차의 장점은 유럽 국가에서 전기자동차가 성장하는 데 기여하는 요인 중 일부입니다.

- 유럽 국가에서는 전기 상용차, 특히 경트럭에 대한 수요가 점차 증가하고 있습니다. 또한 여러 국가의 정부도 전기자동차 도입을 지원하고 있습니다. 2021년 11월, 영국 정부는 2040년까지 모든 대형 차량을 무공해 차량으로 만들겠다는 공약을 발표했습니다. 이러한 요인으로 인해 영국 내 전기 상용차 판매량은 2021년 대비 2022년에 23.17% 증가했으며, 여러 국가에서 유사한 정책이 시행되면서 유럽 전역에서 전기 상용차에 대한 수요가 증가하고 있습니다.

- 유럽 국가들의 차량 전기화는 향후 몇 년 동안 엄청난 성장을 이룰 것으로 예상됩니다. 탈탄소화를 위한 각국 정부의 노력이 유럽 내 전기 상용차 시장을 견인할 것으로 예상됩니다. 예를 들어, 2022년 1월 독일 교통부 장관은 2030년까지 1,500만 대의 전기차를 도로에 배치하겠다는 목표를 발표했습니다.

유럽의 전기자동차 산업 개요

유럽의 전기자동차 시장은 적당히 통합되어 있으며 상위 5개 기업이 43.69%를 점유하고 있습니다. 이 시장의 주요 업체는 Bayerische Motoren Werke AG, Groupe Renault, Tesla Inc., Toyota Motor Corporation and Volkswagen AG (알파벳 순 정렬)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 인구

- 1인당 GDP

- 차량 구매를 위한 소비자 지출(CVP)

- 인플레이션율

- 자동차 대출 금리

- 공유 차량 서비스

- 전기화의 영향

- EV 충전소

- 배터리 팩 가격

- Xev 신모델 발표

- 중고차 판매

- 연료 가격

- OEM 생산 통계

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 차량 부문

- 상용차

- 승용차

- 해치백

- 다목적 차량

- 세단

- SUV

- 이륜차

- 연료 카테고리

- BEV

- FCEV

- HEV

- PHEV

- 국가명

- 오스트리아

- 벨기에

- 체코 공화국

- 덴마크

- 에스토니아

- 프랑스

- 독일

- 아일랜드

- 이탈리아

- 라트비아

- 리투아니아

- 노르웨이

- 폴란드

- 러시아

- 스페인

- 스웨덴

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Audi AG

- Bayerische Motoren Werke AG

- Groupe Renault

- Hyundai Motor Corporation

- Kia Corporation

- Mercedes-Benz

- Tesla Inc.

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Car AB

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Electric Vehicle Market size is estimated at 319 billion USD in 2025, and is expected to reach 636.6 billion USD by 2029, growing at a CAGR of 18.85% during the forecast period (2025-2029).

The growing logistics, supply chain, infrastructure, and construction sectors and the rise in public transportation services are bolstering the European EV market

- The demand for commercial vehicles is set to witness a significant uptick in the coming years. Key drivers of this growth include the logistics, supply chain, infrastructure, and construction sectors. Additionally, a rise in public transportation services is bolstering the demand for buses. However, the sales of commercial vehicles experienced a downturn in 2020, largely due to the impact of the pandemic. The market swiftly rebounded in 2021, with Europe's Climate Plan playing a pivotal role. As Europe aims to ban diesel-powered vehicles by 2030, a notable shift is expected to be witnessed among business consumers toward electric commercial vehicles.

- Across Europe, the introduction of new products and strategic collaborations, such as the partnership between Hyundai Motor Company and H2 Energy, are poised to drive sales of electric trucks. This collaboration produced Hyundai Hydrogen Mobility (HHM) in September 2019 with a vision to foster a green hydrogen ecosystem in Switzerland and Europe. HHM has set an ambitious target of introducing 1,600 fuel-cell electric heavy-duty trucks by 2025. Such initiatives are expected to fuel the sales of heavy electric trucks in Europe from 2024 to 2030.

- In 2021, the number of electric buses in Germany's public transport sector nearly doubled, with new registrations surging by 60% to reach 1,269, up from 689 in the previous year. Of these, 586 were battery electric vehicles, while only a handful was fuel cell-powered or utilized other technologies. Furthermore, both local transport companies and government bodies in Germany have plans to add over 3,000 e-buses by 2025. Similar trends in other European nations are poised to propel the overall commercial vehicle market in Europe from 2024 to 2030.

The European electric vehicles market is characterized by country-level variations, reflecting differing incentives, infrastructure, and consumer preferences

- Europe is one of the largest electric vehicle manufacturers globally. Globally, it has one of the fastest adoptions of electric mobility. In terms of electric vehicles, sales of electric passenger cars accounted for the largest share of 8.3% of all newly registered cars across the region in 2023, which were fully electric. Gasoline-powered vehicles are expected to be banned by 2030 and 2035 in most countries, providing a boost to the sales of electric vehicles.

- The launch of new products and the entry of new brands are expected to drive the market for passenger cars in Europe. In February 2022, the Chinese automaker Xpeng entered Sweden's electric passenger cars with its debut electric cars, P7 and P5 sedans. In June 2022, the American automaker Ford announced that it would produce and sell only electric cars in Europe by 2030. The company plans to invest USD 11.4 billion in producing an electric car at a manufacturing plant in Valencia, Spain.

- Several government efforts in terms of rebates and subsidies are increasing the adoption of electric vehicles in various European countries. For instance, in 2023, a subsidy of EUR 2,950 was made eligible for new battery electric cars and a subsidy of around EUR 2,000 for used battery electric cars. However, the price of the vehicles should be a minimum of EUR 12,000 and a maximum of EUR 45,000. Such advantages attract customer attention to these vehicles, which is expected to enhance the demand for various types of electric vehicles in European countries from 2024 to 2030.

Europe Electric Vehicle Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Electric Vehicle Industry Overview

The Europe Electric Vehicle Market is moderately consolidated, with the top five companies occupying 43.69%. The major players in this market are Bayerische Motoren Werke AG, Groupe Renault, Tesla Inc., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.2 Passenger Vehicles

- 5.1.2.1 Hatchback

- 5.1.2.2 Multi-purpose Vehicle

- 5.1.2.3 Sedan

- 5.1.2.4 Sports Utility Vehicle

- 5.1.3 Two-Wheelers

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Audi AG

- 6.4.2 Bayerische Motoren Werke AG

- 6.4.3 Groupe Renault

- 6.4.4 Hyundai Motor Company

- 6.4.5 Kia Corporation

- 6.4.6 Mercedes-Benz

- 6.4.7 Tesla Inc.

- 6.4.8 Toyota Motor Corporation

- 6.4.9 Volkswagen AG

- 6.4.10 Volvo Car AB

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms