|

시장보고서

상품코드

1693701

교육 보안 : 시장 점유율 분석, 산업 동향·통계, 성장 예측(2025년-2030년)Education Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

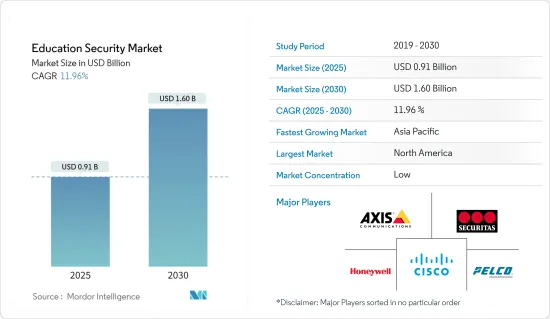

교육 보안 시장 규모는 2025년에 9억 1,000만 달러, 2030년에는 16억 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 11.96%를 나타낼 전망입니다.

보안 시스템은 병, 화재, 괴롭힘, 도난, 공격 및 내부 및 외부 공격으로부터 학생과 교사를 보호하기 위해 설계되었습니다. 시청 시스템은 합리적인 가격으로 실시간 정보를 제공합니다. 심각한 보안 사건이 발생하면 이러한 솔루션은 학생과 직원을 보호하고 일상적인 규율 문제를 처리하기 위해 가장 가까운 경찰서에 신고합니다.

각 국의 교육시설의 구조에는 큰 차이가 있어 폭력방지와 개입에 대한 접근과 지원에 영향을 미칩니다.

게다가 학교, 단과 대학, 대학에서의 견고한 보안 대책의 필요성에 대한 의식의 고조에 힘입어 교육 섹터는 최근 큰 변모를 이루고 있습니다. 안전이 최우선 과제가 되면서, 교육 기관들은 학생, 교직원, 그리고 자산을 보호하기 위해 첨단 보안 솔루션을 점점 더 많이 도입하고 있습니다. 또한, 교육 보안의 성장을 뒷받침하는 정부 원조의 확대나, 인프라의 확장 증가는 보안 시스템을 강화해, 예측 기간 중 시장 성장에 크게 기여하는 것으로 예측됩니다.

예를 들어, 2024년 2월, 조지아 대학은 730만 달러 상당의 새로운 캠퍼스 시큐리티 대책을 발표했습니다. 이 패키지에는 경찰 부문의 예산을 20% 증액해, 보다 경쟁력이 있는 급여에 의해 경관의 채용과 정착을 높이는 것이 포함되어 있습니다. 이 패키지에는 방범 카메라와 조명의 증설, 추가 번호판 판독기, 블루 라이트 콜 시스템 구현도 포함되어 있습니다.

공공 감시와 관련된 조달 비용과 프라이버시에 대한 우려는 교육 보안 시장의 성장을 크게 억제하고 있습니다.

팬데믹은 시장에 악영향을 미쳤고, 일부 교육기관은 전 세계적으로 폐쇄되었습니다. 자동화 된 솔루션 수요가 높아지고 있습니다. COVID-19의 영향으로부터 회복하기 위해서 세계적으로 교육 시설의 건설이 증가했고 예측 기간중 시장 성장률에 플러스의 영향을 주는 것으로 분석되고 있습니다.

교육 보안 시장 동향

고등교육시설이 큰 성장을 이룰 전망

ID 액세스 관리 및 방문자 관리 시스템과 같은 요구는 고등 교육 캠퍼스에서 지지를 받고 있으며 시장 성장 기회를 창출하고 있습니다.

Identisys, Honeywell, Pelco Products Inc.와 같은 공급업체는 대학 및 대학의 고유한 요구에 맞게 맞춤형 솔루션을 제공하며, 교육 기관용 보안 솔루션 시장 도입을 촉진하고 있습니다.

또한 시장 공급업체는 학생과 직원이 스마트폰을 가상 ID 카드 및 액세스 키로 사용할 수 있도록 하는 모바일 자격 증명 솔루션과 같은 첨단 기술을 도입하여 물리적 카드의 필요성을 없애고 다중 요소 인증을 통해 보안을 강화하고 있습니다.

예를 들면, 아미티 대학에서는 스마트 카드, 생체 인증 리더, IP 카메라, 화재 경보 시스템에 의한 보안 솔루션을 도입하고 있어, 캠퍼스에 있어서 교육 보안 솔루션의 필요성을 나타내고 있습니다. 또한, 학생은 캠퍼스에 액세스하기 위해서 칩 대응 스마트 카드를 휴대하고 있어, 카페테리아나 서점 등에서 전자 지갑으로서 사용할 수 있습니다. 이는 캠퍼스, 학생, 교직원의 보안 필요성을 완화하고 시장 성장을 촉진합니다.

대학 구내에 설치된 모든 IoT를 동시에 관리하고 더 나은 관리를 위한 통합 보안 솔루션과 오픈소스 플랫폼의 필요성으로 시스템 통합 및 관리 서비스가 고등 교육 부문의 교육 보안 시장을 견인하고 있습니다.

고등교육 분야의 교육 보안 솔루션 시장은 현저한 기술 진보를 기록하고 있으며, 보안 리스크를 관리 및 검출하기 위해 인공지능(AI) 대응 솔루션을 통합하여 시장 성장을 지원하고 있습니다.

북미가 큰 시장 점유율을 차지할 전망

북미의 교육 보안 시장은 지난 몇 년간 학교에서 총기 난사 사건 증가, 새로운 초등 및 고등 교육 시설의 건설, 교육 예산 증가, 이 지역에서 사업을 전개하는 벤더에 의한 혁신적인 솔루션의 발매 등에 기인하는 보안 수요 증가가 주요 요인이 되고 있습니다. Cisco Systems Inc.와 Honeywell Security Group 같은 주요 기업들이 위치해 있어, 이 지역의 교육 보안 시장을 더욱 확대하고 있습니다.

미국과 캐나다는 이 지역의 캠퍼스 및 학교 보안 시장에서 가장 높은 성장을 이루고 있습니다.

예를 들어, 2024년 1월, 펜실베니아의 학교는 1억 5,500만 달러의 안전 및 보안 자금을 받을 권리를 얻었지만, 그 중 9,000만 달러는 정신건강 상담자와 자원에 대한 신규 투자에 맞추어지고 있습니다. 학교 안전 자금은 조쉬 샤피로 지사의 최우선 계산에 포함되었습니다. 학교 안전 및 보안 자금은 학교 안전 및 보안(SS&S) 위원회를 통해 펜실베니아 위원회(PCCD)를 통해 제공됩니다.

게다가 이 지역에서 진행 중인 인프라 개발과 건설 활동은 새로 건설되는 교육 시설의 보안에 보안 솔루션을 채택하는 성장 기회를 창출할 것으로 기대되고 있습니다. 2024년 2월 AUCSO는 회원사들을 위한 중요한 벤치마킹 데이터를 수집하기 위해 맞춤형 리스크, 회복탄력성 및 보안 관리 솔루션인 ISARR와 파트너십을 발표했습니다.

게다가 물리적 보안 시스템에 대한 주목이 높아지는 가운데, 교육 시설은 허가된 개인을 부지 내에 넣고, 허가되지 않은 개인을 부지 밖에 낼 수 있는 학교나 대학의 캠퍼스 보안 솔루션을 도입하는 것이 필수가 되고 있습니다.

이에 따라 북미 시장은 제품 출시 증가, 정부 및 교육 당국의 학교 보안 보조금 증가, 지역 전체 교육 시설 건설 증가 등 교육 보안 시장에서 큰 점유율을 차지하는 것으로 분석되고 있습니다.

교육 보안 시장 개요

교육 보안 시장은 Cisco Systems Inc., Honeywell International Inc., Axis Communications AB, Genetec Inc.와 같은 주요 기업들이 참여하고 있습니다. 이러한 시장 리더는 기능성을 높이기 위해 다양한 전략을 실시하여 타사와의 차별화에 성공하고 있습니다. 전략적 파트너십(기타 서비스, 특전, 제품 번들, 유통 제공), 더 큰 할인 제공 등이 포함되어 있으며, 이러한 공급업체는 시장에서 제공하는 제품을 크게 차별화합니다.

브랜드 아이덴티티의 강도는 시장에서의 영향력과 밀접하게 연결되어 있습니다. 확립된 브랜드는 고성능의 대명사이기 때문에 옛부터 기업은 경쟁 우위를 유지할 수 있을 것으로 예측됩니다.

2024년 2월 OmnilERT는 3세대 AI 시각 총기 감지 시스템을 출시했습니다. Omnilert Gun Detect는 현재 수십만 개의 학교, 대학, 병원 캠퍼스, 소매점 및 상업시설, 기타 조직 시설 및 캠퍼스의 안전을 확보하고 있습니다.

2024년 4월 보쉬의 총기 감지 시스템은 비디오와 음성 AI를 결합한 다층적인 접근법으로 학교 입구에서 총기를 감지합니다. PRO 시각 총기 검지 기능을 탑재한 시스템의 2대의 Flexidome 카메라가 즉시 학교 직원에게 통지합니다. 총기가 보이지 않을 경우, 두 번째 단계인 지능형 오디오 분석 기능을 갖춘 Flexidome panorama 5100i 카메라가 총성을 감지하고 분류하며, 총성이 발생한 방향을 정확하게 예측합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- COVID-19 팬데믹 시장에 대한 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 실시간 감시에 대한 수요 증가

- 비용 효율적인 보안 솔루션과 중요한 인프라 정비에 대한 수요 증가

- 시장 성장 억제요인

- 보안 솔루션의 조달 비용과 공중 감시와 관련된 프라이버시에 대한 우려가 시장 성장에 영향

제6장 시장 세분화

- 서비스별

- 경비

- 고용 전 스크리닝

- 보안 컨설팅

- 시스템 통합 및 관리

- 알람 감시 서비스

- 기타 비공개 보안 서비스

- 시설별

- 초등 및 중등 교육 시설

- 고등교육시설

- 기타 교육 시설

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Cisco Systems Inc.

- Honeywell International Inc

- Pelco Inc.(Motorola Solutions Inc.)

- Securitas Technology(Securitas AB)

- Axis Communications AB

- Genetec Inc.

- Verkada Inc.

- Hangzhou Hikvision Digital Technology Co. Ltd

- Silverseal Corporation

- Bosch Sicherheitssysteme GmbH(Robert Bosch GMBH)

- SEICO Inc.

- AV Costar

- Kisi Incorporated

- Siemens AG

제8장 투자 분석

제9장 시장 전망

SHW 25.05.15The Education Security Market size is estimated at USD 0.91 billion in 2025, and is expected to reach USD 1.60 billion by 2030, at a CAGR of 11.96% during the forecast period (2025-2030).

Security systems are designed to protect students and teachers from diseases, fires, harassment, theft, aggression, and attacks from internal and external forces. More security spending is needed to develop technology innovation in education facilities. Video surveillance systems are affordable and provide real-time information. In case of significant security incidents, these solutions alert the nearer law enforcement offices to protect students and staff and handle routine discipline issues.

Significant differences in the structure of educational establishments in different countries affect the approach and support for violence prevention and intervention. Substantial differences also exist in the level of student and teacher learning standards, quality of teaching, support for teachers, and infrastructure across countries with development, poverty, or underdeveloped status. Moreover, the increase in the market for education safety is driven by a variety of security systems and services.

Moreover, the education sector has witnessed a significant transformation in recent years, driven by the increased awareness of the need for robust security measures in schools, colleges, and universities. With safety becoming a top priority, educational institutions increasingly use advanced security solutions to protect students, staff, and property. In addition, the growing government aid to boost education security growth and the increasing expansion of infrastructure are set to strengthen the security systems and significantly contribute to the market's growth during the forecast period.

For instance, in February 2024, the University of Georgia announced new campus security measures worth USD 7.3 million. The package includes a 20% budget increase for the police department to increase officer recruitment and retention through more competitive salaries. The package also includes additional security cameras and lighting, additional license plate readers, and the implementation of a Blue Light Call System.

Procurement costs and privacy concerns related to public surveillance significantly restrain the growth of the Education Security Market. The market is expected to overcome these challenges only by implementing a well-balanced approach.

The pandemic had a negative impact on the market, with several education institutions shut down globally. However, in the recovery, education security served additional purposes, and in the post-COVID-19 environment, the demand for automated solutions in education security has risen. The growing construction of education facilities globally to recover from the impact of COVID-19 is analyzed to positively impact the market growth rate during the forecast period.

Education Security Market Trends

Higher Education Facilities are Expected to Witness Major Growth

The need for identity access management and visitor management systems, among others, is gaining traction in higher education campuses, creating market growth opportunities.

Market vendors, such as Identisys, Honeywell, and Pelco Products Inc., provide customized solutions to universities and colleges designed for their unique needs, driving the market adoption of education security solutions. For instance, IdentiSys, an education security solution provider, offers customized security systems, streamlined identification processes, advanced access control, integrated visitor management, and mobile credentials for university campuses.

Additionally, market vendors are introducing advanced technologies, such as mobile credential solutions to allow students and staff to use their smartphones for virtual ID cards and access keys, eliminating the need for physical cards and enhancing security through multi-factor authentication, driving the market growth of educational security solutions in higher educational institutions due to its ease in providing digital access control system.

For instance, Amity University implemented security solutions through smart cards, biometric readers, IP cameras, and fire warning systems, which shows the need for education security solutions on campuses. Additionally, students carry a chip-enabled smart card to access the campus, which can be used as an e-wallet in the cafeteria, book shops, etc., easing the security needs of the campus, students, and staff and fueling the market growth.

System integration and management services are driving the educational security market in higher education departments due to the need for integrated security solutions and an open-source platform to simultaneously manage all the IoTs installed on university premises for better management. This service offers a single dashboard solution to the user to control, monitor, and manage their security needs, which can be customer-managed and vendor-managed.

The higher education sector's market for education security solutions has been registering significant technological advancement and integrating artificial intelligence (AI)-enabled solutions to manage and detect security risks, supporting market growth.

North America is Expected to Hold Significant Market Share

The education security market in North America is primarily driven by the increased demand for security owing to the increased shooting attacks in schools in the past few years, construction of new primary and higher education facilities, growth in the education budget coupled with innovative solutions launches by the market vendors operating in the region. Additionally, the region is home to some of the major players, such as Cisco Systems Inc. and Honeywell Security Group, which further expand the education security market in the region.

The United States and Canada have experienced the highest growth in the region's campus and school security market, primarily because of rising education security spending caused by high construction costs for educational facilities and increased demand for surveillance cameras. Various schools and higher education institutions in the country are upgrading their security measures by investing substantial funding. This, in turn, drives the growth of the education security market in the region.

For instance, in January 2024, Pennsylvania schools were entitled to USD 155 million in safety and security funds - USD 90 million of which is earmarked for new investments in mental health counselors and resources. School safety funding is a top priority for Governor Josh Shapiro and was included in the state budget for the 23-24 school year. The School Safety and Security funding is made available through the Pennsylvania Commission (PCCD) through the School Safety and Security (SS&S) Committee. PCCD has approved a funding framework that allows schools to leverage over USD 155 million dollars in federal and state funding for a variety of investments.

Furthermore, the region's ongoing infrastructure development and construction activities are expected to create growth opportunities for adopting security solutions for the security of newly constructed educational facilities. For instance, in February 2024, AUCSO announced a partnership with ISARR, A Customized Risk, Resilience and Security Management Solution, to collect critical benchmarking data for its members. This partnership builds on the existing relationship between ISARR and AUCSO (ISARR has been a major supporter of AUCSO over the past four years).

Further, with a greater focus on physical security systems, it's becoming vital that educational facilities implement school and college campus security solutions that can allow authorized individuals onto their sites and keep unauthorized individuals out. Education authorities in the country are investing heavily to expand educational institutions' video surveillance systems, access control systems, and door-locking systems.

Therefore, the North American market is analyzed to hold a significant share in the education security market owing to the growing product launches, increasing school security funding by the government and educational authorities, and growth in educational facilities construction across the region.

Education Security Market Overview

The Education Security market features key players such as Cisco Systems Inc., Honeywell International Inc., Axis Communications AB, and Genetec Inc. These market leaders have successfully set themselves apart by implementing various strategies to enhance functionality. These strategies include remote access, wireless capabilities, strategic partnerships (offering additional services, benefits, product bundling, and distribution), and providing deeper discounts. As a result, these vendors have significantly differentiated their offerings in the market.

The strength of their brand identity is closely tied to their influence in the market. Established brands are synonymous with high performance, so long-standing players are anticipated to maintain a competitive advantage. Due to their extensive market reach and capacity to offer advanced products, the competitive rivalry in this sector is expected to remain intense.

February 2024: OmnilERT launched its 3rd generation AI Visual Gun Detection System. This state-of-the-art system is packed with cutting-edge innovations designed to take the industry to the next level with Omnilert's visual gun detection solution. As the only solution to deliver the combination of Detection, Verification, Activation and Notification Omnilert Gun Detect now secures hundreds of thousands of school, college, and hospital campuses, as well as retail and commercial properties and other organizational facilities and campuses.

April 2024: Bosch's gun detection system combines video and audio AI with a multi-tiered approach to detect guns at school entrances. When someone brandishing a gun walks into a school's entrance, the system's two Flexidome cameras, equipped with IVA PRO visual gun detection, immediately notify school staff. If a gun isn't visible, the second layer, the Flexidome panorama 5100i camera, with intelligent audio analytics, detects and classifies the shot while accurately predicting the direction from which it came. The near-infrared camera-based system enhances safety while providing a smooth flow and welcoming environment to support learning.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Real-time Surveillance

- 5.1.2 Growing Demand for Cost-effective security solutions and significant Infrastructure Developments

- 5.2 Market Restraints

- 5.2.1 The Security Solutions Procurement Costs and Privacy Concerns Related to Public Surveillance Impact the Growth of the Market

6 MARKET SEGMENTATION

- 6.1 By Services

- 6.1.1 Guarding

- 6.1.2 Pre-Employment Screening

- 6.1.3 Security Consulting

- 6.1.4 Systems Integration & Management

- 6.1.5 Alarm Monitoring Services

- 6.1.6 Other Private Security Services

- 6.2 By Facilities

- 6.2.1 Primary & Secondary Facilities

- 6.2.2 Higher Education Facilities

- 6.2.3 Other Educational Facilities

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Honeywell International Inc

- 7.1.3 Pelco Inc. (Motorola Solutions Inc.)

- 7.1.4 Securitas Technology (Securitas AB)

- 7.1.5 Axis Communications AB

- 7.1.6 Genetec Inc.

- 7.1.7 Verkada Inc.

- 7.1.8 Hangzhou Hikvision Digital Technology Co. Ltd

- 7.1.9 Silverseal Corporation

- 7.1.10 Bosch Sicherheitssysteme GmbH (Robert Bosch GMBH)

- 7.1.11 SEICO Inc.

- 7.1.12 AV Costar

- 7.1.13 Kisi Incorporated

- 7.1.14 Siemens AG