|

시장보고서

상품코드

1693726

미국 및 유럽의 광섬유 케이블 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)United States And European Fiber Optic Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

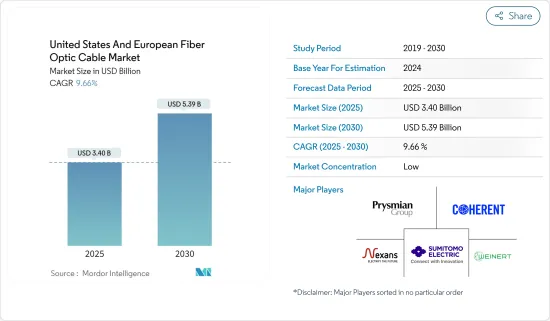

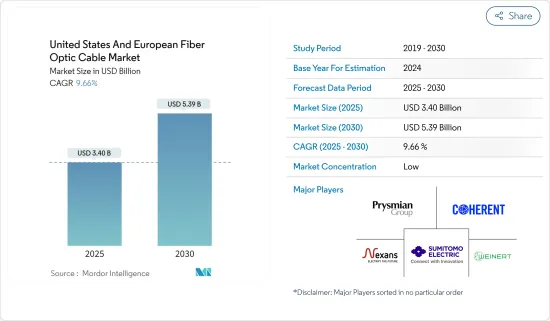

미국과 유럽의 광섬유 케이블 시장 규모는 2025년에 34억 달러로 추정되며, 예측 기간(2025-2030년) 동안 9.66%의 연평균 복합 성장률(CAGR)로 2030년에는 53억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 5세대 네트워크와 광섬유 인프라의 진화가 산업 전반의 디지털 혁신을 주도하고 있습니다. 광섬유 케이블은 구리선 케이블보다 보안, 신뢰성, 대역폭, 안전성이 우수합니다. 광섬유 케이블과 구리선의 차이점은 광섬유 케이블이 구리선을 통해 정보를 전달하는 전자 펄스가 아닌 광섬유선을 통해 정보를 전달하는 광 펄스를 이용한다는 점입니다.

- 온라인 거래와 가상 회의가 증가함에 따라 기업은 경쟁력을 유지하기 위해 5G와 광섬유 케이블이 필요합니다. 예를 들어, 유럽중앙은행에 따르면 소비자의 비정기 결제에서 온라인 결제가 차지하는 비중은 2019년 6%에서 2022년 17%까지 증가했습니다. 따라서 이러한 추세를 지원하기 위해서는 초고속 인터넷과 같은 견고한 인프라가 필요하며, 이는 조사 대상 시장에 기회를 창출할 것으로 예측됩니다.

- 또한, 광섬유 케이블은 조명 및 장식, 데이터 전송, 수술, 기계 검사 등 다양한 산업 응용 분야에 비용 효율적이고 편리하며 간편한 솔루션입니다. 또한 재택근무 및 하이브리드 근무 모델 증가는 미국과 유럽 전역에서 FTTH의 필요성을 증가시키고 있습니다.

- 데이터 트래픽 증가, 특히 인터넷 프로토콜(IP) 증가로 인해 높은 네트워크 대역폭에 대한 수요가 급증하고 있습니다. 유명 서비스 제공업체들은 6-9개월마다 백본 대역폭이 두 배로 증가하고 있다고 보고하고 있습니다. 인터넷 트래픽 증가로 인해 대역폭은 6-9개월마다 두 배로 증가하고 있습니다.

- 미국과 유럽 시장의 광섬유 통합 인프라의 확장은 특히 통신 산업에서 광섬유 케이블에 대한 수요를 크게 증가시켰습니다. 광섬유 네트워크와 광섬유 와이어도 광대역 설비에 의해 크게 개선되었습니다. 이러한 아키텍처에는 FTTH, FTTP, FTTC, FTTB, FTTH, FTTC, FTTB가 포함됩니다.

- 개발도상국의 광섬유 생산자의 연결 수요 증가는 큰 비즈니스 전망을 제공합니다. 그러나 무선 솔루션에 대한 수요 증가와 광섬유 케이블 설치의 어려움과 같은 요인은 시장 성장에 몇 가지 운영상의 어려움을 가져옵니다.

- 또한, 미국과 유럽 양 지역이 코로나 이후 경기 침체를 겪고 있는 것처럼 거시경제적 요인도 조사 시장의 성장에 큰 영향을 미칩니다. 또한 러시아와 우크라이나의 전쟁, 미국과 중국의 갈등과 같은 지정학적 문제도 시장의 지속적인 성장에 어려운 환경을 조성하고 있습니다.

미국 및 유럽 광섬유 케이블 시장 동향

광섬유 및 5G 구축에 대한 투자 증가가 시장을 주도하고 있습니다.

- 미국과 유럽 시장은 선진 통신 기술을 가장 먼저 도입한 국가 중 하나이며, 현재도 그 추세가 지속되고 있습니다. 발달된 생태계의 존재와 디지털 기술의 높은 소비자 보급률 등의 요인으로 인해 산업 이해관계자들이 광섬유 및 통신 인프라에 대한 투자를 늘리고 있습니다. 예를 들어, 통신 서비스 제공업체인 코닝은 최근 2023년 애리조나 주 최초의 광섬유 네트워크를 설계할 계획을 밝혔습니다.

- 예를 들어, CommScope는 광섬유 기술 혁신의 선두주자로서 가장 까다로운 네트워크를 위한 고성능 광섬유 연결의 경계를 넓히고 있습니다. 이 회사는 또한 산업 표준을 설정하고 있기 때문에 회사의 광섬유 배선 시스템은 항상 요구 사항을 초월합니다.

- 미국과 유럽 시장에서의 5G 도입이 진행되고 있는 것도 조사 대상 시장의 성장을 가속하고 있습니다. 예를 들어, Ericsson은 최근 2025년까지 독일에서 3.5GHz(5G)를 구축할 것이라고 발표했으며, 3.5GHz 대역의 5G 네트워크는 2023년 42%에서 2025년에는 독일 전체의 43%를 차지할 것으로 예측됩니다. 그러나 2025년에 커버되는 지역은 독일 지리적 지역의 7%에 불과할 것으로 예측됩니다.

- 마찬가지로 미국 국립과학재단(NSF)은 미국의 중요 인프라와 정부 사업자가 언제 어디서나 안전하게 통신할 수 있도록 5G 솔루션의 가속화에 주력하고 있습니다. 예를 들어, 2022년 9월 NSF는 미 국방부와의 파트너십을 발표했으며, 1,200만 달러의 투자로 NSF는 2022년 컨버전스 액셀러레이터 프로그램에 16개 팀을 선정했습니다. 이들 팀은 'Track G: Securely Operating Through 5G Infrastructure'에 선정되었습니다. Track G는 미국 연방정부 및 군을 위한 5G 통신을 개발하기 위한 기술 발전을 촉진합니다.

- 미국에 본사를 둔 네트워크 및 통신 솔루션 제공업체인 애드트랜은 패시브 광 네트워크 기술을 채택한 풀 파이버 네트워크를 구축하여 기업 및 가정에 기가비트 액세스 및 인프라 백홀을 제공합니다. SDX 6330 10Gb/s 콤보 패시브 광 네트워크 파이버 액세스 플랫폼을 발표했습니다. 이 플랫폼을 통해 서비스 제공 업체는 비용 효율적이고 신속하게 기업과 가정을 광섬유 기반 광대역으로 연결할 수 있습니다. 이 새로운 솔루션은 업계에서 가장 높은 포트 밀도를 제공하며, 400Gbit/s의 업링크를 지원하는 광 회선 단말기의 선구자입니다.

- 또한 데이터 소비 증가는 데이터 연결을 지원하는 새로운 광섬유 케이블 네트워크에 대한 투자를 촉진함으로써 연구 시장에도 기회를 창출하고 있습니다. 예를 들어, 2022년 11월 스웨덴의 연결 제공 업체인 아렐리온(Arelion)은 멕시코와 미국 텍사스 사이를 통과하는 두 개의 대용량 광섬유 경로를 건설할 계획을 발표했습니다. 새로운 고밀도 파장 분할 다중화 경로는 대용량 및 확장 가능한 대역폭 전송에 대한 수요 증가에 대응하고 미국, 아시아 및 유럽 OTT 공급업체의 멕시코 국내 시장에 대한 액세스를 단순화합니다.

통신 최종 사용자 산업이 큰 시장 점유율을 차지합니다.

- 광섬유 케이블(OFC)은 통신 인프라의 중요한 구성 요소입니다. 지난 10년간 광섬유는 특히 통신사의 강력한 대역폭 요구에 부응하여 전송 매체의 선택이 되고 있습니다. 조사 대상 지역에는 AT&T, Verizon, Sprint, Vodafone Group과 같은 주요 통신사가 존재하며, 세계 및 지역적 입지를 강화하기 위해 광섬유 네트워크를 지속적으로 확장하고 있습니다.

- 인터넷, 전자상거래, 컴퓨터 네트워크, 멀티미디어(음성, 데이터, 비디오) 등 다양한 소스에서 발생하는 데이터 트래픽의 급증은 이러한 방대한 양의 정보를 처리하기 위해 더 높은 대역폭을 관리할 수 있는 전송 매체가 필요함을 보여줍니다. Eurostat에 따르면, 유럽연합(EU)의 일일 인터넷 사용자 비율은 2028년 74.07%였으나 2022년에는 84%로 증가할 것으로 예상하고 있습니다. 상대적으로 무한한 대역폭을 가진 광섬유 케이블은 이 문제에 대한 중요한 해결책 중 하나이기 때문에 수요는 앞으로도 높은 수준으로 유지될 것으로 예측됩니다.

- 통신 네트워크에서 광섬유 케이블은 셀 타워, 데이터센터, 인터넷 서비스 제공 업체 등 서로 다른 네트워크 노드를 연결하여 서로 다른 위치에서 대량의 데이터를 교환 할 수 있도록합니다. 광섬유 케이블은 고속 인터넷 연결, 화상회의, 온라인 게임, 클라우드 컴퓨팅 등 첨단 통신 기술 개발에도 적합합니다. 따라서 미국과 유럽에서 5G 네트워크의 확장이 시장 기회를 촉진할 것으로 예측됩니다.

- 또한, 광섬유 케이블은 안전성, 확장성, 무제한의 대역폭 가능성으로 인해 실시간 데이터 수집 및 전송에 크게 의존하는 5G, 빅데이터, IoT와 같은 진화한 기술에 대응하는 대역폭 수준을 지원하기 위해 선택되었습니다. 5G의 시작과 함께 네트워크 용량이 향상되고 지연 시간이 단축될 것으로 예측됩니다.

- 인터넷은 광섬유 케이블이 데이터 및 통신 산업에서 널리 사용되는 것처럼 조사 대상 지역 시장 기회를 촉진하는 조사 대상 지역에서 급격한 변화와 급성장 기술 중 하나입니다. 예를 들어, Ericsson에 따르면, 조사 대상 지역의 스마트폰 당 데이터 트래픽은 계속 증가하고 있으며, 예를 들어 북미의 경우 스마트폰 당 데이터 트래픽은 2021년 13GB/월에서 2028년 58GB/월로 증가할 것으로 예측됩니다. 마찬가지로 서유럽에서는 2021년 16GB/월에서 2028년 56GB/월로 증가할 것으로 예측됩니다.

미국과 유럽의 광섬유 케이블 산업 개요

미국과 유럽의 광섬유 케이블 시장은 세분화되어 있으며, Nexans SA, Prysmian Group, Weinert Industries AG, Coherent Corporation, Sumitomo Corporation과 같은 주요 기업들이 참여하고 있습니다. 시장 진출기업들은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 확보하기 위해 파트너십, 인수, 합병 등의 전략을 채택하고 있습니다.

- 2023년 3월 - 세계 네트워크 연결 솔루션 기업인 CommScope는 미국 전역의 광대역 구축을 가속화하고 더 많은 지역 사회와 소외된 지역을 연결하기 위해 광섬유 케이블 생산을 확대한다고 발표했습니다. 회사측에 따르면, 이번 조치로 미국 내 광섬유 케이블 생산량이 증가하여 서비스 미달 지역에 대한 광대역 보급을 가속화할 수 있다고 합니다. 또한, 이 회사의 HeliARC 회선은 연간 50만 가구의 FTTH 구축을 지원할 수 있을 것으로 예상하고 있습니다.

- 2023년 3월 - 유럽연합은 디지털 10년을 위한 2030 정책 프로그램에 따라 건물에 광섬유 케이블 설치 의무를 발표했습니다. 새로운 규정에 따라, 신규 계약 건물 및 대규모 개보수 중인 건물은 패시브 인프라(미니 덕트)와 건물 내 광섬유 배선(광섬유 케이블)을 아파트/유닛 내 네트워크 종단점까지 확보해야 합니다. 준비된)' 건물에 대한 인증 제공도 계획하고 있습니다. 이러한 추세는 광섬유 케이블 수요를 촉진할 것으로 예측됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 주요 거시경제 테마 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 시장이 해결해야 할 과제

제6장 시장 세분화

- 최종사용자 산업별

- 통신

- 전력 유틸리티

- 방위 및 군

- 산업

- 의료

- 기타

- 국가별

- 미국

- 독일

- 오스트리아 및 스위스

제7장 경쟁 구도

- 기업 개요

- Nexans SA

- Prysmian Group

- Weinert Industries AG

- Coherent Corporation

- Sumitomo Corporation

- Corning Inc.

- Finisar Corporation

- Leoni AG

- Folan

- Molex LLC

- Fujikura Ltd

- Sterlite Technologies

- Furukawa Electric Co. Ltd

- Smiths Interconnect(Smiths Group PLC)

제8장 산업용 광섬유 현황

제9장 시장 전망

LSH 25.05.20The United States And European Fiber Optic Cable Market size is estimated at USD 3.40 billion in 2025, and is expected to reach USD 5.39 billion by 2030, at a CAGR of 9.66% during the forecast period (2025-2030).

Key Highlights

- The evolution of fifth-generation networks & fiber optic infrastructure has driven digital transformation across industries. Optic fiber cable presents better security, reliability, bandwidth, and security than copper cables. The distinction between a fiber optic cable and a copper wire is that the fiber optic cable utilizes light pulses to transfer information down the fiber lines rather than electronic pulses to transmit information through the copper lines.

- With increasing online transactions & virtual meetings, companies need 5G and optic fiber cable to remain competitive. For instance, according to the European Central Bank, online payments share in consumers' non-recurring payments increased to 17% in 2022 from just 6% in 2019. Hence, to support such trends robust infrastructure such as high-speed internet is required which is anticipated to create opportunities in the studied market.

- Furthermore, fiber optic cables are cost-effective, convenient, & easy solutions for numerous industrial applications, like lighting and decorations, data transmission, surgeries, and mechanical inspections. The growing work-from-home & hybrid work model also drives the need for FTTH throughout the United States and Europe.

- Data traffic growth, specifically Internet Protocol (IP), drives the surge in need for high network bandwidth. Prominent service providers registered bandwidth doubling on their backbones every six to nine months. Due to growing internet traffic, bandwidth doubles every 6 to 9 months.

- The expansion of fiber-integrated infrastructure in the US and the European market has also immensely raised the need for fiber-optic cables, particularly in the telecom industry. Fiber-optic networks and fiberoptic wires have also greatly improved owing to broadband installations. These architectures include FTTH, FTTP, FTTC, & FTTB.

- The increase in the need for connectivity in developing nations for fiber-optic producers offers significant business prospects. Yet factors like the advancement in wireless solution demand & the difficulty of deploying fibreoptic cables provide several operational difficulties for the market's growth.

- Macroeconomic factors also influence the studied market's growth significantly as both the United States and the European regions have been witnessing economic downturns post-covid. Furthermore, geopolitical issues such as the Russia-Ukraine war, and the US-China disputes also creates a challenging environment for an uninterrupted growth of the market.

US & European Fiber Optic Cable Market Trends

Rising Investment in Fiber Optic and 5G Deployment Drives the Market

- The US and European markets have been among the early adopters of advanced telecom technologies and continue to remain so. Factors such as the presence of developed ecosystems and higher consumer penetration of digital technologies support encourage the industry stakeholders to increase investments in fiber optic and telecom infrastructure. For instance, Corning, the telecom service provider, recently disclosed plans to design Arizona's first fiber network in 2023, anticipated to serve over 100,000 residences.

- Additionally, the studied regions also have the presence of some of the biggest fiber optic cable companies who continue to expand their regional presence; for instance, CommScope is among the leaders in fibreoptic innovation and drives the boundaries of high-performance fiber connectivity for the most challenging networks. Since the company also sets industry standards, its fiber-optic cabling systems always transcend requirements.

- The growing deployment of 5G in the US and European markets also favors the studied market's growth. For instance, Ericsson, recently stated that the 3.5 GHz (5G) roll-out will be conducted in Germany by 2025. The 3.5 GHz 5G network would constitute 43% of the total German population by 2025, up from 42%, which is anticipated in 2023. However, only 7% of the geographical region in Germany is expected to be covered in 2025.

- Similarly, the US National Science Foundation (NSF) concentrates on accelerating 5G solutions to support US critical infrastructure and government operators to communicate securely anytime and anywhere. For instance, in September 2022, NSF announced a partnership with the Department of Defense Office. With an investment of USD 12 million, NSF selected 16 teams for the Convergence Accelerator program in 2022. These teams were chosen for "Track G: Securely Operating Through 5G Infrastructure". Track G promotes technology advancement to develop 5G communications for the US federal government & military.

- Adtran, the US-based networking & communications solutions provider, enables the building of full-fiber networks employing passive optical network technologies that provide gigabit access to businesses and homes and for infrastructure backhaul. In January 2023, the company established its SDX 6330 10 Gbit/s combo passive optical network fiber access platform, which allows service providers to cost-effectively and quickly connect businesses & homes with fiber-based broadband. The new solution provides the highest port density in the industry and is the foremost optical line terminal incorporated with 400 Gbit/s uplinks.

- Furthermore, the growing data consumption is also creating opportunities in the studied market by driving investment in new optical fiber cable networks which supports the data connectivity. For instance, in November 2022, Arelion, a Swedish connectivity provider, unveiled a plan to create two high-capacity fiber optic routes through Texas between Mexico & the United States. The new dense wavelength division multiplexing routes will meet the increasing demand for high-capacity, scalable bandwidth transport & simplify access to Mexico's local markets for over-the-top suppliers in the United States, Asia, and Europe.

Telecommunication End-user Industry Holds Significant Market Share

- Optical fiber cable (OFC) is a vital building block in the telecommunication infrastructure. Over the last decade, fiber optics have been catering to forceful bandwidth needs, especially from telecommunication companies, and have become the choice of transmission medium. The Studied regions have the presence of some of the biggest telecommunication companies, such as AT&T, Verizon, Sprint, Vodafone Group, etc., who are continuously expanding their optical fiber network to increase their global and regional presence, which creates opportunities in the studied market.

- The eruption of data traffic from different sources, like the internet, e-commerce, computer networks, and multimedia (voice, data, and video), has shown the requirement for a transmission medium capable of managing higher bandwidth to handle such vast amounts of information. According to Eurostat, the share of daily internet users in the European Union had increased to 84% in 2022, compared to 74.07% in 2028. As fiber-optic cables, with comparatively infinite bandwidth, are among the key solutions to this problem, the demand is anticipated to remain high.

- In telecommunication networks, fiber optic cables join different network nodes, like cell towers, data centers, and internet service providers, allowing the exchange of extensive amounts of data between different locations. Fiber-optic cables also have suitable for developing high-speed internet connections & other advanced communication technologies such as video conferencing, online gaming, and cloud computing. Hence, the expanding 5G network footprint in the United States and the European region is anticipated to drive opportunities in the studied market.

- Moreover, owing to their security, scalability, and the unlimited bandwidth potential to handle the vast amount of backhaul traffic being generated, fiber-optic cables are also being selected to support the bandwidth levels catering to evolved technologies like 5G, Big Data and IoT that rely heavily on real-time data gathering and transfer. The launch of 5G is predicted to improve the capacity and lower latency straight to networks.

- The internet has been one of the significantly transformative and fast-growing technologies in the studied regions which is driving opportunities in the studied market as optical fiber cables are widely used in the data and the telecommunication industry. For instance, according to Ericsson, datatraffic per smartphone continues to grow in the studied regions, for instance, in North America, data traffic per smartphone is anticipated to growth from 13 GB/month in 2021 to 58 GB/month in 2028. Similarly, in Western Europe, it is anticipated to grow from 16GB/month in 2021 to 56GB/month by 2028.

US & European Fiber Optic Cable Industry Overview

The United States and European fiber optic cable market is fragmented, with major players like Nexans SA, Prysmian Group, Weinert Industries AG, Coherent Corporation, and Sumitomo Corporation. Players in the market are embracing strategies like partnerships, acquisitions, and mergers to enhance their product offerings and gain sustainable competitive advantage.

- March 2023 - CommScope, a global network connectivity solution, announced expansions to its fiber-optic cable production to accelerate broadband rollout across the U.S., connecting more communities and underserved areas. According to the company, this initiative will increase fiber-optic cable output in the U.S., hastening broadband deployment to underserved communities. Additionally, the company's HeliARC lines are expected to support 500,000 homes per year in FTTH deployments.

- March 2023 - European Eunion announced obligations to equip buildings with fiber-optic cables in line with its 2030 policy program for the digital decade. As per the new regulation, it will be mandatory to keep passive infrastructure (mini ducts) and in-building fiber wiring (fiber optic cables) in newly contracted buildings or buildings undergoing major renovations, up to the network termination point in the apartment/unit. EU is also planning to provide certification to the buildings that are 'fiber ready. Such trends are anticipated to drive the demand for fiber optic cables.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of Key Macro-economic themes

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Increased Data Traffic Creates the Demand for Fiber Optic Cable Network

- 5.1.2 Rising Investment in Fiber Optic and 5G Deployment

- 5.2 Market Challenges

- 5.2.1 Rising Demand For Wireless Solutions and Complex Installation Process

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Telecommunication

- 6.1.2 Power Utilities

- 6.1.3 Defence/military

- 6.1.4 Industrial

- 6.1.5 Medical

- 6.1.6 Other End-user Industries

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Germany

- 6.2.3 Austria and Switzerland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nexans SA

- 7.1.2 Prysmian Group

- 7.1.3 Weinert Industries AG

- 7.1.4 Coherent Corporation

- 7.1.5 Sumitomo Corporation

- 7.1.6 Corning Inc.

- 7.1.7 Finisar Corporation

- 7.1.8 Leoni AG

- 7.1.9 Folan

- 7.1.10 Molex LLC

- 7.1.11 Fujikura Ltd

- 7.1.12 Sterlite Technologies

- 7.1.13 Furukawa Electric Co. Ltd

- 7.1.14 Smiths Interconnect (Smiths Group PLC)