|

시장보고서

상품코드

1693816

전력기기 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Power Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

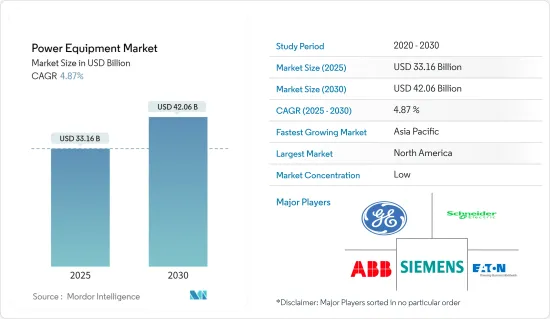

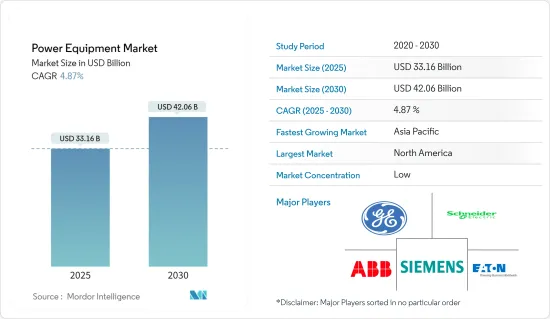

전력기기 시장 규모는 2025년에 331억 6,000만 달러에 이르고, 예측기간(2025-2030년)의 CAGR은 4.87%를 나타내, 2030년에는 420억 6,000만 달러에 달할 것으로 예상됩니다.

COVID-19는 2020년 시장에 부정적인 영향을 미쳤습니다.

주요 하이라이트

- 중기적으로는 인구 증가와 인프라 개발에 의한 에너지 수요 증가가 예상되고, 그 결과 예측 기간 중의 전력기기 수요가 증가합니다.

- 한편, 높은 운전·보수 비용이 시장 성장의 방해가 될 것으로 예측됩니다.

- 신재생에너지와 스마트그리드의 인프라 개척을 위한 기술 투자 증가는 전력기기 시장에 큰 기회를 가져올 것으로 예측됩니다.

전력기기 시장 동향

발전이 시장을 독점할 전망

- 인구 증가, 도시화, 공업화를 배경으로 세계의 전력 수요는 증가하고 있습니다.

- 또한 태양광 발전, 풍력 발전, 수력 발전, 지열 발전 등 재생 가능 에너지 발전에 대한 주목이 높아지고 있는 것도 발전 설비의 우위성을 높이고 있습니다.

- 예를 들어, 2022년 6월, 베스타스 AS는 EnBW의 900MW He Dreiht 해상 풍력 발전 프로젝트를 위해 64기의 V235-15.0MW 풍력 터빈을 공급하는 계약을 획득했습니다.

- 세계 각국의 정부도 시책, 인센티브, 재생 가능 에너지 발전 목표를 실시하고 있으며, 특히 재생 가능 에너지 부문의 발전 설비 수요를 더욱 밀어 올리고 있습니다.

- 이에 따라 재생가능에너지의 설비용량은 세계적으로 증가하고 있습니다.

- 따라서 에너지 수요 증가, 재생 가능 에너지에 대한 주목, 정부의 대처, 발전에 의해 발전은 전력기기 시장 중에서 지배적인 부문으로서 부상하고 있습니다.

아시아태평양이 현저한 성장을 이룰 전망

- 아시아태평양에는 세계 인구의 상당한 비율이 집중되어 있어 수많은 대도시가 있습니다.

- 아시아태평양은 가까운 미래에 전력기기의 유력한 시장으로 대두해 오는 것으로 예측됩니다.

- BP Statistical Review of World Energy에 따르면 2021년 동지역의 발전량은 13,994.4 TWh로 2020년 대비 8.4%, 2011-2021년 사이에 4.7% 증가했습니다.

- 또한 이 지역의 정부는 발전·배전 인프라에 유리한 시책, 이니셔티브, 투자를 실시함으로써 중요한 역할을 하고 있습니다.

- 예를 들어 중국 정부는 2022년 고비사막지대에 총용량 450기가와트의 태양광발전소와 풍력발전소를 건설한다는 야심적인 계획을 발표했습니다.

- 이러한 진보는 효율적이고 지속 가능한 전력 관리를 가능하게 하고, 전력기기 시장에서의 이 지역의 우위성을 높이고 있습니다.

- 아시아태평양은 급속한 경제 성장, 도시화, 정부의 이니셔티브, 신재생에너지 도입, 인프라 개척, 산업 수요, 기술의 진보에 의해 전력기기 시장을 독점하는 태세를 갖추고 있습니다.

전력기기 산업 개요

세계의 전력기기 시장은 반고체화되어 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 시장 규모와 수요 예측(-2028년, 단위:달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 인구 증가 및 인프라 개발

- 성장 억제요인

- 높은 운용 및 보수비용

- 성장 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 설비 유형

- 발전기

- 변압기

- 스위치 기어

- 회로 차단기

- 전원 케이블

- 기타 기기

- 발전원

- 화석연료

- 태양열

- 풍력

- 원자력

- 수력

- 최종 사용자

- 주거

- 산업 및 상업

- 유틸리티

- 용도

- 발전

- 송전

- 배전

- 지역, 시장 규모 및 수요 예측(-2028년, 지역별)

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 프랑스

- 영국

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 호주

- 일본

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- General Electric Company

- Siemens AG

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Toshiba Corporation

- Honeywell International Inc.

- Bharat Heavy Electricals Limited

- Crompton Greaves Ltd.

- Larsen & Toubro Limited

- Fuji Electric Co., Ltd.

- Rockwell Automation, Inc.

- ABB Ltd.

제7장 시장 기회와 앞으로의 동향

- 신재생에너지와 스마트그리드 인프라 개발에 대한 기술 투자 증가

The Power Equipment Market size is estimated at USD 33.16 billion in 2025, and is expected to reach USD 42.06 billion by 2030, at a CAGR of 4.87% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. Presently, the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, increasing population growth and infrastructure development are expected to increase energy demand, consequently increasing the demand for power equipment during the forecasted period.

- On the other hand, high operations and maintenance costs are expected to hinder market growth.

- Nevertheless, the increasing technological investments in developing renewable energy and smart grid infrastructure are expected to create huge opportunities for the power equipment market.

Power Equipment Market Trends

Power Generation Expected to Dominate the Market

- The global electricity demand is rising, driven by population growth, urbanization, and industrialization. As a result, power generation equipment plays a critical role in meeting this escalating demand and ensuring a consistent electricity supply.

- Moreover, the expanding focus on renewable energy sources, such as solar, wind, hydro, and geothermal power, further contributes to the dominance of power generation equipment. The transition towards cleaner and more sustainable energy necessitates specialized power generation equipment like solar panels, wind turbines, and hydroelectric generators.

- For instance, in June 2022, Vestas AS won a contract to supply 64 V235-15.0 MW wind turbines for EnBW's 900 MW He Dreiht offshore wind project. Vestas has also entered into an agreement with Cadeler for the transportation and installation of the turbines, which is planned to start in Q2 2025.

- Governments worldwide are also implementing policies, incentives, and renewable energy targets, further boosting the demand for power generation equipment, particularly in the renewable energy sector.

- This has led to an increase in renewable energy installed capacity globally. According to the International Renewable Energy Agency, in 2022 the global renewable energy installed capacity was 3371.8 GW, compared to 3077.23 GW in 2021, registering a growth rate of more than 9.5% between 2021 and 2022.

- Therefore, with increasing energy demand, the focus on renewable energy, government initiatives, and power generation, power generation emerges as the dominant segment within the power equipment market.

Asia-Pacific to Witness Significant Growth

- Asia-Pacific houses a significant proportion of the global population and has numerous major cities. In the coming years, the region is expected to witness a surge in power demand due to the expanding access to electricity among millions of new customers. This escalating demand can be attributed to rapid population growth and the ongoing process of industrialization.

- The Asia-Pacific region is poised to emerge as a prominent market for power equipment in the foreseeable future. The main drivers are the increasing use of renewable energy sources, rising power consumption, increased access to electricity, and ongoing improvements to power grid infrastructure. Key countries such as China, India, Japan, and Australia are anticipated to play pivotal roles in shaping the power equipment market within the region.

- According to the BP statistical review of world energy, the electricity generation in the region was 13,994.4 TWh in 2021, an increase of 8.4% compared to 2020 and 4.7% between 2011 and 2021.

- Additionally, governments in the region are playing a crucial role by implementing favorable policies, initiatives, and investments in power generation and distribution infrastructure. This commitment to energy security, renewable energy promotion, and improved electricity access further propel the demand for power equipment in Asia-Pacific.

- For instance, the Chinese government unveiled its ambitious plan in 2022 to construct solar and wind energy power plants with a total capacity of 450 gigawatts in the Gobi desert regions. This initiative aims to propel the nation towards achieving its renewable energy target by 2030.

- These advancements enable efficient and sustainable power management, enhancing the region's prominence in the power equipment market.

- Asia Pacific is therefore poised to dominate the power equipment market due to rapid economic growth, urbanization, government initiatives, the deployment of renewable energy sources, infrastructure development, industrial demand, and technological advancements.

Power Equipment Industry Overview

The global power equipment market is semi-consolidted. Some of the key players in this market (in no particular order) are General Electric Company, Schneider SE, ABB Ltd., Eaton Corporation, and Siemens AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Population Growth and Infrastructure Development

- 4.5.2 Restraints

- 4.5.2.1 High Operational and Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Equipment Type

- 5.1.1 Generator

- 5.1.2 Transformer

- 5.1.3 Switchgears

- 5.1.4 Circuit Breakers

- 5.1.5 Power Cable

- 5.1.6 Other Equipment Types

- 5.2 Power Generation Source

- 5.2.1 Fossil Fuel Based

- 5.2.2 Solar

- 5.2.3 Wind

- 5.2.4 Nuclear

- 5.2.5 Hydro

- 5.3 End-User

- 5.3.1 Residential

- 5.3.2 Industrial and Commercial

- 5.3.3 Utility

- 5.4 Application

- 5.4.1 Power Generation

- 5.4.2 Transmission

- 5.4.3 Distribution

- 5.5 Geography [Market Size and Demand Forecast till 2028 (for regions only)]

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Australia

- 5.5.3.4 Japan

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Nigeria

- 5.5.4.4 South Africa

- 5.5.4.5 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Chile

- 5.5.5.4 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 General Electric Company

- 6.3.2 Siemens AG

- 6.3.3 Schneider Electric SE

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 Eaton Corporation plc

- 6.3.6 Toshiba Corporation

- 6.3.7 Honeywell International Inc.

- 6.3.8 Bharat Heavy Electricals Limited

- 6.3.9 Crompton Greaves Ltd.

- 6.3.10 Larsen & Toubro Limited

- 6.3.11 Fuji Electric Co., Ltd.

- 6.3.12 Rockwell Automation, Inc.

- 6.3.13 ABB Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technological Investments in Developing Renewable Energy and Smart Grid Infrastructure