|

시장보고서

상품코드

1693826

불소수지 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

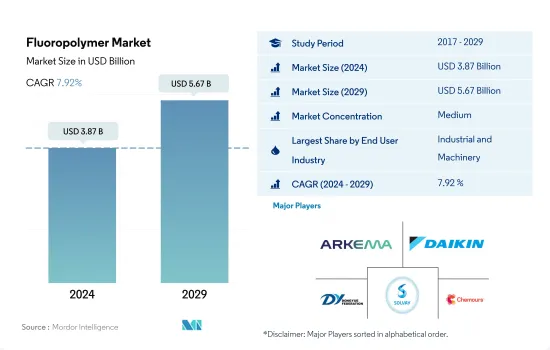

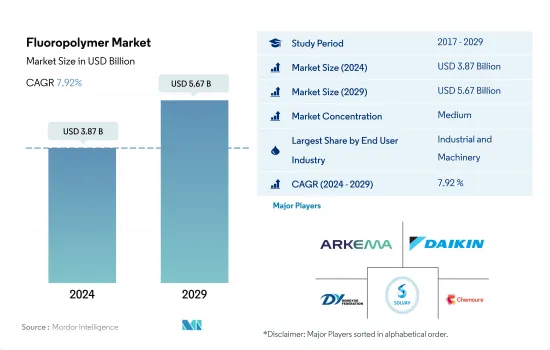

불소수지 시장 규모는 2024년에 38억 7,000만 달러에 달했고, 2029년에는 56억 7,000만 달러에 이르고, 예측기간(2024-2029년)의 CAGR은 7.92%를 나타낼 것으로 예상됩니다.

전기차 수요 증가가 시장 확대에 크게 기여

- 불소수지는 고온과 부식 환경에 견디는 고성능 플라스틱입니다.

- 2022년 세계의 불소수지 시장에서는 양적으로는 산업 및 기계설비산업이 최대 시장 점유율을 차지했습니다. 아시아태평양과 북미의 급속한 도시화로 중건설기기와 전동공구 수요가 증가하고, 이들 지역이 최대의 소비지가 되어, 2022년의 세계의 불소수지 시장 매출 점유율은 각각 51.59%와 28.37%를 차지했습니다.

- 전기 및 전자산업은 불소수지의 세계 제2위의 소비자입니다. 이것은 기업이 재택근무 모델을 채용해, 소비자가 홈 오피스를 짓는 것으로, 노트북, 휴대폰, 스마트 디바이스등의 전자기기 수요가 높아지고 있기 때문입니다. 아시아태평양은 이 부문에 있어서의 불소수지의 최대 소비국에서

- 자동차산업은 가장 급성장하고 있는 부문이며, 예측기간(2023-2029년)의 CAGR은 금액 기준으로 12.31%를 나타낼 것으로 보입니다.

예측기간 동안에도 아시아태평양이 우위를 유지

- 중국, 일본, 한국, 미국, 캐나다 등 주요국 덕분에 아시아태평양과 북미는 불소수지의 주요 소비국 중 하나가 되어 2022년에는 합계로 수량 기준으로 약 81.5%의 점유율을 차지했습니다.

- 아시아태평양은 불소수지의 최대 소비국이며, 예측 기간 동안 금액 기준으로 CAGR 9.06%를 나타내고, 가장 급성장하는 부문이 될 전망입니다. 쇼어 수출의 회복으로 중국의 공작기계와 설비에 대한 수요가 세계적으로 높아지고 있습니다.

- 북미는 아시아태평양에 이은 급성장 지역이며, 예측 기간 (2023-2029) 중에 금액 기준으로 CAGR 8.69%를 나타낼 것으로 예측되고 있습니다. 미국은 자동차 산업으로 인해이 지역에서 불소 중합체의 주요 소비자 중 하나이며, 예측 기간 동안 가치 측면에서 11.60%의 CAGR을 나타낼 것으로 예상됩니다. 이 지역의 자동차 생산 대수 증가는 향후 불소수지 수요를 끌어올릴 것으로 예측됩니다.

세계의 불소수지 시장 동향

전자 산업의 기술 진보가 성장을 가속할 가능성

- 전자제품에 있어서의 기술 혁신의 급속한 페이스가 새롭고 고속의 전기 및 전자제품에 대한 일관된 수요를 촉진하고 있습니다. 세계의 전기 및 전자 시장은 예측 기간 동안 6.61%의 연평균 성장률을 기록할 것으로 예상됩니다.

- 2018년 아시아태평양은 중국, 한국, 일본, 인도, ASEAN 국가의 급속한 산업화로 강력한 경제 성장을 보였습니다. 이 성장을 견인한 것은 팬데믹(세계적 대유행)의 사이, 사람들이 실내 대기를 강요당했기 때문에 리모트 워크나 홈 엔터테인먼트용의 소비자용 전자 기기 제품에 대한 수요였습니다.

- 디지털화, 로봇공학, 가상현실, 증강현실, IoT(사물인터넷), 5G연결 등 첨단기술에 대한 수요는 예측기간 동안 확대될 것으로 예측됩니다. 는 예측기간 중에 상승할 것으로 예측됩니다.

불소수지 산업 개요

불소수지 시장은 적당히 통합되어 있으며 상위 5개사에서 42.38%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 포장

- 수출입 동향

- 불소수지 무역

- 규제 프레임워크

- 아르헨티나

- 호주

- 브라질

- 캐나다

- 중국

- EU

- 인도

- 일본

- 말레이시아

- 멕시코

- 나이지리아

- 러시아

- 사우디아라비아

- 남아프리카

- 한국

- 아랍에미리트(UAE)

- 영국

- 미국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 산업 및 기계

- 포장

- 기타

- 하위 수지 유형

- 에틸렌테트라플루오로에틸렌(ETFE)

- 플루오르화 에틸렌-프로필렌(FEP)

- 폴리테트라플루오로에틸렌(PTFE)

- 폴리비닐플루오라이드(PVF)

- 폴리비닐리덴 플루오라이드(PVDF)

- 기타 하위 수지

- 지역

- 아프리카

- 국가별

- 나이지리아

- 남아프리카

- 기타 아프리카

- 아시아태평양

- 국가별

- 호주

- 중국

- 인도

- 일본

- 말레이시아

- 한국

- 기타 아시아태평양

- 유럽

- 국가별

- 프랑스

- 독일

- 이탈리아

- 러시아

- 영국

- 기타 유럽

- 중동

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 북미

- 국가별

- 캐나다

- 멕시코

- 미국

- 남미

- 국가별

- 아르헨티나

- 브라질

- 기타 남미

- 아프리카

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Arkema

- Daikin Industries, Ltd.

- Dongyue Group

- Gujarat Fluorochemicals Limited(GFL)

- Kureha Corporation

- Sinochem

- Solvay

- The Chemours Company

- Zhejiang Juhua Co., Ltd.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Fluoropolymer Market size is estimated at 3.87 billion USD in 2024, and is expected to reach 5.67 billion USD by 2029, growing at a CAGR of 7.92% during the forecast period (2024-2029).

Rising electric vehicles demand to majorly benefit the market expansion

- Fluoropolymers are high-performance plastics that can withstand high temperatures and corrosive environments. Due to their non-adhesive and low-friction properties, they are suitable for applications in various end-user industries like aerospace, electronics, and telecommunications.

- In terms of volume, the industrial and machine equipment industry occupied the largest market share in the global fluoropolymers market in 2022. Fluoropolymers, like PVDF, PVF, and ETFE, are widely used to manufacture structural equipment, valves, fittings, pipes, and tubing. Owing to the rapid urbanization in Asia-Pacific and North America, the demand for heavy construction equipment and power tools increased, making these regions the largest consumers while generating 51.59% and 28.37% of revenue shares, respectively, in the global fluoropolymer market in 2022.

- The electrical and electronics industry is the second-largest consumer of fluoropolymers globally. This can be attributed to companies adopting work-from-home models and consumers setting up home offices, raising the demand for electronic gadgets like laptops, mobiles, and smart devices. Asia-Pacific is the largest consumer of fluoropolymers in this sector, accounting for 59.89% of the global fluoropolymer revenue in the electrical and electronics industry.

- The automotive industry is the fastest-growing sector and is likely to witness a CAGR of 12.31% in terms of value during the forecast period (2023-2029). The rising demand for PVDF resin in lithium-ion batteries used in electric vehicles is expected to increase the consumption of fluoropolymer resins.

Asia-Pacific to remain dominant during the forecast period

- Owing to the major countries such as China, Japan, South Korea, the United States, and Canada, Asia-Pacific and North America are among the major consumers of fluoropolymers, combinedly holding a share of around 81.5% by volume in 2022.

- Asia-Pacific is the largest consumer of fluoropolymer resins and is expected to register a CAGR of 9.06%, by value, during the forecast period, making it the fastest-growing segment as well. Countries like China and Japan are at the forefront of the utilization of fluoropolymers occupying 58.73% and 18.55%, respectively, of the total fluoropolymer market share in terms of revenue. China's industrial and machinery is the major consumer of fluoropolymers in the country. Rapid urbanization and restoration of offshore exports have increased the demand for Chinese machine tools and equipment globally. As a result, the country has an increasing demand for fluoropolymers. For instance, the revenue of fluoropolymers in the region from the industrial machinery segment is expected to amount to around USD 796.3 million in 2023.

- North America is the second-fastest-growing region after Asia-Pacific and is predicted to register a CAGR of 8.69% in terms of value during the forecast period [2023-2029]. The United States is among the major consumers of fluoropolymers in the region owing to its automotive industry, which is predicted to register a CAGR of 11.60% in terms of value during the forecast period. The rising vehicle production in the region is expected to drive the demand for fluoropolymers in the future. For instance, vehicle production in the region is projected to reach 18 million units by 2029 from 14.5 million units in 2022.

Global Fluoropolymer Market Trends

Technological advancements in electronics industry may foster the growth

- The rapid pace of technological innovation in electronic products is driving the consistent demand for new and fast electrical and electronic products. In 2022, the global revenue of electrical and electronics stood at USD 5,807 billion, with Asia-Pacific holding a 74% market share, followed by Europe with a 13% share. The global electrical and electronics market is expected to record a CAGR of 6.61% during the forecast period.

- In 2018, the Asia-Pacific region witnessed strong economic growth owing to rapid industrialization in China, South Korea, Japan, India, and ASEAN countries. In 2020, due to the pandemic, there was a slowdown in global electrical and electronics production due to the shortage of chips and inefficiencies in the supply chain, which led to a stagnant growth rate of 0.1% in revenue compared to the previous year. This growth was driven by the demand for consumer electronics for remote working and home entertainment as people were forced to remain indoors during the pandemic.

- The demand for advanced technologies, such as digitalization, robotics, virtual reality, augmented reality, IoT (Internet of Things), and 5G connectivity, is expected to grow during the forecast period. Global electrical and electronics production is expected to register a growth rate of 5.9% in 2027. As a result of technological advancements, the demand for consumer electronics is expected to rise during the forecast period. For instance, the global consumer electronics industry is projected to witness a revenue reach of around USD 904.6 billion in 2027, compared to USD 719.1 billion in 2023. As a result, technological development is projected to lead the demand for electrical and electronic products during the forecast period.

Fluoropolymer Industry Overview

The Fluoropolymer Market is moderately consolidated, with the top five companies occupying 42.38%. The major players in this market are Arkema, Daikin Industries, Ltd., Dongyue Group, Solvay and The Chemours Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 EU

- 4.3.7 India

- 4.3.8 Japan

- 4.3.9 Malaysia

- 4.3.10 Mexico

- 4.3.11 Nigeria

- 4.3.12 Russia

- 4.3.13 Saudi Arabia

- 4.3.14 South Africa

- 4.3.15 South Korea

- 4.3.16 United Arab Emirates

- 4.3.17 United Kingdom

- 4.3.18 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.3 Polytetrafluoroethylene (PTFE)

- 5.2.4 Polyvinylfluoride (PVF)

- 5.2.5 Polyvinylidene Fluoride (PVDF)

- 5.2.6 Other Sub Resin Types

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Nigeria

- 5.3.1.1.2 South Africa

- 5.3.1.1.3 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Japan

- 5.3.2.1.5 Malaysia

- 5.3.2.1.6 South Korea

- 5.3.2.1.7 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Russia

- 5.3.3.1.5 United Kingdom

- 5.3.3.1.6 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Saudi Arabia

- 5.3.4.1.2 United Arab Emirates

- 5.3.4.1.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Daikin Industries, Ltd.

- 6.4.4 Dongyue Group

- 6.4.5 Gujarat Fluorochemicals Limited (GFL)

- 6.4.6 Kureha Corporation

- 6.4.7 Sinochem

- 6.4.8 Solvay

- 6.4.9 The Chemours Company

- 6.4.10 Zhejiang Juhua Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록