|

시장보고서

상품코드

1693922

일본의 데이터센터 서버 시장(2025-2030년) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측Japan Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

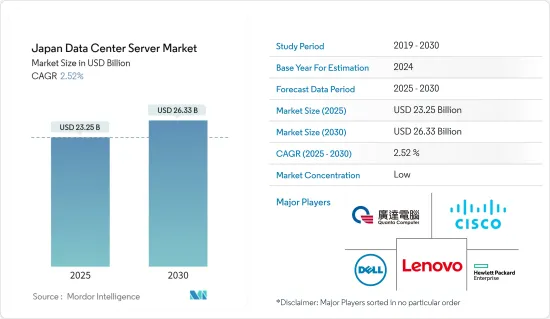

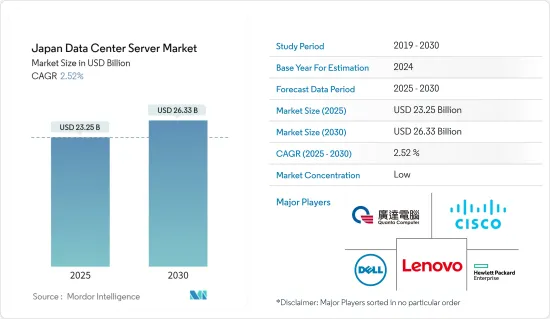

일본의 데이터센터 서버 시장 규모는 2025년에 232억 5,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 2.52%로 성장하여 2030년에는 263억 3,000만 달러에 달할 것으로 예측됩니다.

일본의 데이터센터 수요는 급증하고 있으며 비즈니스 시장으로서의 매력도 높아지고 있습니다. 환경 문제에 대한 대처, 지방 데이터센터에 대한 정부의 지원, 산업 구조의 변화, 기술의 진보에 의한 라이프스타일의 변화 등이 일본의 데이터센터 시장에서 중요한 역할을 하고 있으며, 그 결과 서버 시장 수요가 커지고 있습니다.

주요 하이라이트

- 시장 성장의 주요 촉진요인은 일본 지역의 하이퍼스케일 구축 수요의 확대입니다. 오사카의 강점은 환경, 신에너지, 제약, 제조업 등 다양한 산업이 집적되어 있다는 점에 있습니다. 이 활기찬 에코시스템은 하이퍼스케일 데이터센터와 세계의 지속 가능성과 기술 진보를 추진하는 산업 간의 독특한 연계를 키우고 있습니다. 인구 880만명인 오사카부의 GDP는 3,600억 달러로 노르웨이의 경제 규모에 필적합니다.

- 일본은 인터넷의 보급이라는 점에서 가장 선진적인 경제국 중 하나로 널리 간주되고 있습니다. 광대역 가입자 수는 4,380만명으로, 그 중에서 FTTH 가입자 3,660만명, CATV 인터넷 가입자 650만명, 모바일 광대역 가입자수(4G와 5G)는 1억 8,400만명입니다.

- 클라우드 데이터센터의 에너지 효율은 2050년까지 탄소 배출량 제로를 목표로 하는 일본 정부의 목표를 달성하기 위해 일본의 이산화탄소 배출량을 절감하는 데 중요한 역할을 할 수 있습니다.

- 클라우드 기술이 일본에 가져오는 이점과 혁신의 촉진이나 기존과는 다른 비즈니스 모델의 육성에 긍정적인 효과를 가져오는 것을 인식한 일본 정부는 나라를 더욱 디지털화하는 광범위한 계획의 일환으로서 클라우드를 추진하기 위한 수많은 이니셔티브를 내세우고 있습니다.

- 서버를 구축하려면 먼저 개별 부품을 구입해야 하며 서버를 조립하고 필요한 소프트웨어를 설치해야 합니다.

일본 데이터센터 서버 시장 동향

블레이드 서버의 폼 팩터 부문이 크게 성장할 것으로 예상

- 블레이드 서버는 컴퓨터 및 시스템 네트워크 내에서 데이터를 호스팅하고 전달하는 데 사용되는 소형 컴퓨터입니다. 컴퓨터, 애플리케이션, 프로그램 및 시스템 간의 링크 역할을 합니다. Cloudscene에 따르면 2023년 9월 기준 일본에는 218곳의 데이터센터가 존재했습니다. 블레이드 서버는 일반적으로 공간과 전력을 최대한 활용하고 효율화해야 하므로 대규모 데이터센터에서 사용됩니다.

- 일본에는 대규모 데이터센터 시설로 확인된 데이터센터가 40여곳 있으며, 향후 수년간 증가할 것으로 예측됩니다. 일본 정부는 해저 케이블의 육지 기지를 분산시키고 육지 지점을 다양화함으로써 전국에 여러 개의 새로운 데이터센터를 건설할 계획입니다. 해저 케이블은 주로 일본의 동태평양 측에 부설되어 있으며, 그 대부분은 도쿄나 시마 등 특정 지역에 집중하고 있습니다. 정부는 다른 지역에 육지 기지를 분산시켜 경제적 안전성을 강화할 방침입니다. 이로 인해 새로운 집중 지역에서 대형 DC 부문이 크게 성장하여 블레이드 서버 수요를 높일 수 있습니다.

- 수도권에서는 토지와 전력에 제약이 있어 건설비용이 상승하고 신규 개발이 지연될 수 있어 국내외 진입기업과의 경쟁이 격화되고 있습니다. DC 건설 회사는 일본의 부족한 토지에 새로운 데이터센터를 건설하기 위해 투자하고 있지만 수요가 높기 때문에 이러한 데이터센터는 높은 컴퓨팅 파워를 가질 가능성이 높습니다. 이러한 상황에서 블레이드 서버의 장점은 블레이드 서버의 제한된 컴퓨팅 컴포넌트를 통해 고객은 더 많은 서버를 더 작은 랙 영역에 설치하여 밀도를 높일 수 있다는 것입니다.

- 일본과 같은 일부 아시아 국가들은 110V 전원 인프라를 지원하지 않으므로 미국에서 실현할 수 있는 전력 밀도를 달성할 수 없습니다. 하지만 이 전력 밀도를 지원하려면 BladeSystem C3,000 및 IBM BladeCenter S와 같은 특별한 냉각 솔루션이 필요합니다.

- 또한 블레이드 서버는 고성능 처리를 위해 설계되었습니다. 랙 서버와 달리 블레이드 서버는 핫스왑이 가능합니다.

- 블레이드 서버 기술의 과거, 현재, 미래를 이해하는 것은 일본의 모든 규모의 조직에 있어서, IT 인프라에 관한 충분한 정보에 근거한 의사 결정을 실시하기 위해서 필수적입니다.

IT 및 통신은 최종 사용자 산업으로서 급성장

- 일본의 정보통신기술(ICT) 부문은 혁신의 최전선에 있으며 눈부신 진보를 이룩하여 미래를 위한 환경을 만들어 내고 있습니다.

- 일본의 ICT 시장의 성장은 주로 소비자용 전자기기, 군사, 농업, 건설 등 다양한 부문에서 사물인터넷(IoT) 기기의 이용 확대에 의해 견인되고 있습니다. Sony, Panasonic, Fujitsu, NEC, Toshiba(Toshiba)와 같은 세계 유수의 ICT 기업이 있으며, ICT 허브로서의 일본의 성장에 중요한 역할을 하고 있습니다.

- 일본의 ICT 시장은 시민 참여, 자기 평가, 온라인 정부 서비스에 대한 피드백 등 지역 전자 정부 프로젝트에 초점을 맞춘 E-일본 전략의 급속한 확대로 성장할 것으로 예측됩니다.

- 일본은 ICT 인프라, 통신기술, 교육, 의료 등 질 높은 인프라와 서비스 외에도 비즈니스와 사회의 안정성이 높습니다.

- 스마트 시티는 소사이어티 5.0을 실현하기 위한 일본 정부의 주요 이니셔티브 중 하나입니다. 'Smart City Public-Private Partnership platform'은 민관 파트너십을 촉진하고 지역 프로젝트를 개발하기 위해 지방에 분산된 디지털 환경을 대체합니다.

- 또한 일본의 통신회사는 6G에 투자하고 있습니다. 2023년 3월 시점에서 일본 국내의 5G 계약수는 약 6,980만건을 돌파하였습니다.

- 이와 같이 하이테크 기업에 의한 전체적인 투자 증가에 따라 IT산업의 개발을 개선하기 위한 정부의 대처나 국내 데이터센터의 성장이 일본의 서버 시장을 밀어 올릴 것으로 예측됩니다.

일본 데이터센터 서버 산업 개요

일본의 데이터센터 서버 시장은 Dell Technologies Inc., Hewlett Packard Enterprise, Cisco Systems Inc., Lenovo Group Limited, Quanta Computer Inc. 등의 대기업이 존재하고 있으며, 매우 세분화되어 있습니다.

- 2023년 12월 - Fujitsu는 주로 서버와 스토리지 솔루션을 중심으로 하는 하드웨어 사업의 경영을 더욱 강화하기 위해 이 전략에 따른 하드웨어 사업의 전문 회사를 일본에서 설립한다고 발표했습니다.

- 2023년 8월 - Hewlett Packard Enterprise는 phoenixNAP가 Ampere Computing의 에너지 효율이 우수한 프로세서를 채용한 클라우드 네이티브 HPE ProLiant RL300 Gen11 서버로 베어 메탈 클라우드 플랫폼을 확대한다고 발표하였습니다.

- 2023년 7월 - Fujitsu는 새로운 서버 BS2,000 SE730/SE730B를 발표하였습니다. 최신 SE세대 서버는 대용량의 데이터를 관리하기 위한 하이엔드 성능의 플랫폼으로서 평가되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 서포트

목차

제1장 서론

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 산업 밸류체인 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 신규 데이터센터 건설 증가, 인터넷 인프라 개발

- 클라우드와 IoT 서비스 채용 증가

- 시장의 과제

- 고액의 초기 투자

- COVID-19의 영향 평가

제6장 시장 세분화

- 폼 팩터별

- 블레이드 서버

- 랙 서버

- 타워용 서버

- 최종 사용자별

- IT 및 통신

- BFSI

- 정부기관

- 미디어 엔터테인먼트

- 기타

제7장 경쟁 구도

- 기업 프로파일

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- Cisco Systems Inc.

- Lenovo Group Limited

- Quanta Computer Inc.

- Super Micro Computer Inc.

- Huawei Technologies Co. Ltd

- Fujitsu Limited

- NEC Corporation

- IBM Corporation

제8장 투자 분석

제9장 시장 기회와 미래 동향

CSM 25.05.15The Japan Data Center Server Market size is estimated at USD 23.25 billion in 2025, and is expected to reach USD 26.33 billion by 2030, at a CAGR of 2.52% during the forecast period (2025-2030).

Japan's demand for data centers is proliferating and becoming more attractive as a business market. Environmental initiatives, government support for local data centers, changes in industrial structure, and changing lifestyles due to technological advancements all play a significant role in the Japanese data center market, resulting in major demand for the server market.

Key Highlights

- The major driver for the market growth is the growing demand for hyperscale construction in the Japanese region. Osaka's strength lies in its diverse concentration of industries, encompassing environmental, new energies, pharmaceuticals, and manufacturing sectors. This vibrant ecosystem fosters a unique coaction between hyperscale data centers and industries driving global sustainability and technological advancement. With a population of 8.8 million, Osaka Prefecture has a GDP of USD 360 billion, similar to the size of Norway's economy.

- Japan is widely regarded as one of the most advanced economies in terms of Internet penetration. As of 2023, Japan's Internet usage rate (individuals) was 82.9%, and the development rate of optical fiber was 99.3%. The number of broadband subscribers was 43.8 million, which includes 36.6 million FTTH subscribers and 6.5 million CATV Internet subscribers, while the number of mobile broadband subscribers (4G and 5G) was 184 million.

- The energy efficiency of cloud data centers can play a crucial role in reducing Japan's carbon footprint to achieve the Japanese government's goal of net-zero carbon emissions by 2050.

- Having recognized the benefits cloud technologies can provide to the country and their positive effect on encouraging innovation and fostering non-conventional business models, the Japanese government has been launching numerous initiatives to promote the cloud as part of the broader plans to digitalize the country further.

- To build a server, one must buy individual components first. They have to assemble the server and install the necessary software. It is resource-intensive to customize, own, and maintain a server. It is well-suited for long-term projects and knowledge-building within the company.

Japan Data Center Server Market Trends

Blade Server Form Factor Segment is Expected to Witness Significant Growth

- A blade server is a small computer used to host and distribute data within a network of computers and systems. It acts as a link between computers, applications, programs, and systems. According to Cloudscene, as of September 2023, there were 218 data centers in Japan. A blade server is typically used in larger data centers due to the need to maximize space and power utilization and efficiency, have high computing needs, and support higher thermal and electrical loads.

- There are close to 40 data centers in Japan that are identified as extensive data center facilities and are expected to increase in the coming years. The Japanese government plans to build several new data centers nationwide by decentralizing landing bases for submarine cables to diversify landing points. Submarine cables are laid mainly on Japan's eastern Pacific Ocean side, with many concentrated in certain areas, such as Tokyo and Shima. The government intends to disperse landing bases in other areas and strengthen economic security. This may lead to significant growth in the large DC segments in newer concentrated areas, boosting the demand for blade servers.

- Constraints on land and power in the greater Tokyo area result in higher construction costs, possible delays for new developments, and fierce competition from domestic and foreign players. DC construction companies are investing in new data centers to build new data centers on scarce land in Japan, but as the demand is high, these data centers are likely to have high computing power. The advantage of blade servers in this situation is that, due to the limited computing components of blade servers, customers can fit more servers into a smaller rack area to increase the density.

- Some Asian countries, such as Japan, do not support 110 V power infrastructure. As a result, they are unable to achieve the power density enjoyed in the United States. For example, a 3-phase 220V power data center in the United States can support a 15 kW rack. However, special cooling solutions are needed to support this power density. Blades are not a viable solution in cases where power is restricted to 110V, no matter the vendor. An exception to this would be a departmental solution, such as the HP BladeSystem C3000 or IBM BladeCenter S.

- Further, blade servers are designed for high-performance processing. Unlike rack servers, blade servers can be hot-swapped. This means that one can remove and replace a blade server in a cluster without powering down the whole cluster. This significantly reduces downtime when an administrator needs to swap out a blade server or move a blade server out of the cluster for maintenance.

- Understanding blade server technology's past, present, and future is essential for organizations of all sizes in Japan to make informed decisions regarding their IT infrastructure. Due to their compact design, high performance, and scalability, blade servers are expected to remain a key component of that infrastructure for many years as they continue to evolve and evolve with the ever-evolving world of technology.

IT and Telecommunication to be the Fastest Growing End-user Industry

- Japan's Information and Communications Technology (ICT) sector is at the forefront of innovation, driving remarkable progress and creating a future-proof environment. The ICT sector opens up a world of possibilities by utilizing state-of-the-art technologies while facing the challenges that define its growth.

- The growth of the Japanese ICT market is mainly driven by the growing use of Internet of Things (IoT) devices across various sectors, such as consumer electronics, military, agriculture, and construction. Japan is home to some of the most prominent ICT organizations in the world, such as Sony, Panasonic, Fujitsu, NEC, and Toshiba (Toshiba), which are playing an important role in the growth of Japan as an ICT hub. The increasing government spending on maintaining the top-of-the-line and advanced infrastructure and the proper implementation of many modernization and improvement projects contribute to the market's expansion.

- Japan's ICT market is expected to grow due to the rapid expansion of E-Japan's strategy, which focuses on local e-government projects, such as citizen participation, self-assessment, and feedback on online government services.

- Japan has a high level of stability in business and society, as well as high-quality infrastructure and services such as ICT infrastructure, communication technology, education, healthcare, and more. The Japanese government is taking steps to support the private sector's digital transformation and the emergence of small and medium-sized enterprises (SMEs).

- Smart Cities are one of the Japanese government's key initiatives to bring Society 5.0 to life. The 6th Strategic Technology Infrastructure (STI) plan set a goal of 100 initiatives10 to be implemented by 2025 with the participation of 1000+ organizations from local government, regional organizations, and private enterprises. The "Smart City Public-Private Partnership platform" will replace the local and dispersed digital landscape to promote public-private partnerships and develop regional projects. Specific initiatives include centralizing the MyNumber (citizens ID) system and developing database registry standards by 2030.

- Further, the telecom companies in Japan are investing in 6G. The 6G system will not only outperform 5G, but it will also offer high speed, high capacity, low latency, new high-frequency bands (above 100 GHz), extend communication coverage to the sky, sea, and space, and provide ultra-low power consumption and ultra-low-cost communications. According to the Ministry of Internal Affairs and Communications, about 69.8 million 5G subscriptions were counted in Japan as of March 2023. In June 2022, NEC (NEC), Fujitsu (Fujitsu), and Nokia (Nokia) joined forces to test new mobile communication technologies to launch 6G services commercially by 2030.

- Thus, with the overall increase in investment by tech companies, government initiatives to improve the IT industry development and growth in data centers in the country would boost the server market in Japan.

Japan Data Center Server Industry Overview

The Japan data center server market is highly fragmented with the presence of major players like Dell Technologies Inc., Hewlett Packard Enterprise, Cisco Systems Inc., Lenovo Group Limited, and Quanta Computer Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023 - Fujitsu announced the launch of a dedicated company for the hardware business in Japan in alignment with this strategy and to further strengthen the management of its hardware business, which primarily focuses on servers and storage solutions.

- August 2023 - Hewlett Packard Enterprise announced that phoenixNAP is expanding its Bare Metal Cloud platform with cloud-native HPE ProLiant RL300 Gen11 servers, using energy-efficient processors from Ampere Computing. The expanded services support AI inferencing, cloud gaming, and other cloud-native workloads with enhanced performance and energy efficiency.

- July 2023 - Fujitsu announced a new server, BS2000 SE730/SE730B. The servers of the latest SE generation are a valued platform in the high-end performance range for managing the largest data volumes. The servers offer extremely high availability and serve as an ideal platform for mission-critical applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Construction of New Data Centers, Development of Internet Infrastructure

- 5.1.2 Increasing Adoption of Cloud and IoT Services

- 5.2 Market Challenge

- 5.2.1 High Initial Investments

- 5.3 Assessment of COVID-19 Impact

6 MARKET SEGMENTATION

- 6.1 By Form Factor

- 6.1.1 Blade Server

- 6.1.2 Rack Server

- 6.1.3 Tower Server

- 6.2 By End User

- 6.2.1 IT and Telecommunication

- 6.2.2 BFSI

- 6.2.3 Government

- 6.2.4 Media and Entertainment

- 6.2.5 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Technologies Inc.

- 7.1.2 Hewlett Packard Enterprise

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Lenovo Group Limited

- 7.1.5 Quanta Computer Inc.

- 7.1.6 Super Micro Computer Inc.

- 7.1.7 Huawei Technologies Co. Ltd

- 7.1.8 Fujitsu Limited

- 7.1.9 NEC Corporation

- 7.1.10 IBM Corporation