|

시장보고서

상품코드

1693924

통합시설관리 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 성장 예측Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

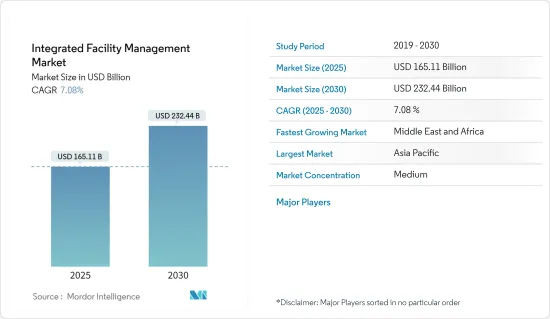

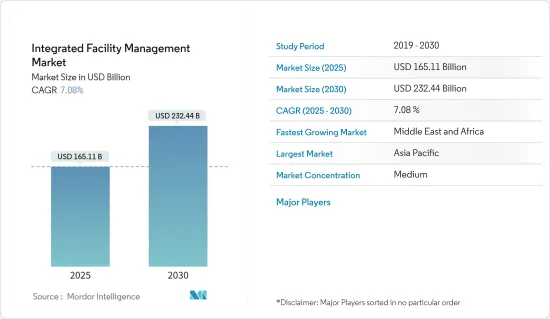

통합시설관리(FM) 시장 규모는 2025년에 1,651억 1,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 7.08%로 성장하여 2030년에는 2,324억 4,000만 달러에 달할 것으로 예측됩니다.

통합시설관리(IFM)는 주로 모든 시설 관리 계약을 하나의 서비스로 관리하는 개념입니다.

주요 하이라이트

- 건설활동의 회복과 함께 친환경 서스테이너블 건축 관행이 중시되고 있는 점이 통합시설관리 시장의 성장 촉진요인으로 분석되고 있습니다.

- 정부의 다양한 대처에 의한 건설 활동의 확대, 도시화의 진전, 선진국과 신흥 경제 제국에서의 상업 건설 프로젝트 증가에 의해 통합시설관리 서비스의 필요성이 최근 몇년 동안 높아지고 있습니다.

- 통합시설관리(IFM)는 사업확대에 의한 입주 요구 증가, 기술 진보에 따른 시설 요구 진화, 비용 효율의 중시 등으로 다양한 부문에서 상업활동이 회복되면서 상승을 경험하고 있습니다.

- 환경 의식의 고조와 비즈니스 관행에 대한 우려로 인해 통합시설관리(IFM)는 계획적인 비즈니스의 추진력으로서 종래의 유지관리의 역할을 넘어서는 개념으로 대두하였습니다.

- 전문적인 인재의 필요성은 세계의 통합시설관리 시장을 발전시키는 데 큰 과제가 되고 있습니다.

통합시설관리 시장 동향

상업 부문이 가장 큰 최종 사용자 부문

- 상업시설은 기업의 IT 및 통신 오피스, 제조업, 기타 서비스 제공업체 등 비즈니스 서비스가 건설 또는 입주하는 오피스 빌딩을 대상으로 합니다. 상업지구는 부동산 회계, 임대, 계약 관리, 조달 관리, 기타 여러 서비스를 필요로 하기 때문에 전문가의 고용이 필요합니다.

- 미국에서는 다양한 소매업이 신규 출점을 하고 존재감을 확대하고 있기 때문에 소프트 FM 서비스 수요가 발생하고 있습니다. IKEA를 보유하고 있는 Ingka Group은 향후 3년간 20억 유로(22억 달러)를 투입해 미국에서 사업을 확대할 계획을 발표했습니다.

- 게다가 CBRE에 따르면 인도와 같은 국가의 소매 섹터는 2023년 중 현저한 성장을 보였으며 국내 주요 도시에서 최고 기록인 710만 평방 피트(2022년 대비 47% 증가)를 기록했습니다. 국내외의 브랜드의 진출에 의해 패션 및 어패럴이 상업 지구의 최대 임대 면적을 차지했습니다.

- Colliers International의 조사에 따르면 부동산 투자자들 사이에서는 2023년에는 사무실과 공업 및 물류시설이 가장 수요가 높은 자산 클래스가 될 것으로 예상되고 있으며, 세계 투자자의 60% 가까이 이러한 유형의 부동산에 대한 투자를 원하고 있습니다.

- 전체적으로, 상업활동의 회복에 의해 가동률의 상승을 관리하고 원활한 사업운영을 확보하면서 기업이 핵심적인 활동에 임할 수 있는 진화한 기술을 채용하기 위한 통합시설관리의 요구가 높아질 것으로 예측됩니다.

아시아태평양이 주요 시장 점유율을 차지

- 아시아태평양에서는 상업시설의 개발이 진행되고 있으며 병원, 공항, 제조 시설, 데이터센터, 교육 기관 등의 인프라 프로젝트에 거액의 투자가 이루어지고 있습니다.

- 중국에서는 많은 시설관리자가 지속 가능 빌딩 관리 수법을 도입하여 직장의 효율화를 촉진하고, 인프라를 개선하여 자산의 수명을 연장하고 있습니다.

- 중국 경제는 특히 상하이와 베이징과 같은 상업 중심지에서 거대한 시장 잠재력을 제공합니다.

- 2023년 12월 중국 자동차 회사 BYD는 한국 자동차 제조업체 KG 모빌리티에 EV용 배터리를 안정적으로 공급하기 위해 4억 1,200만 달러를 투자한다고 발표했습니다. 중국에는 LG Energy Solutions, Samsung SDI, SK On, BYD 등 자동차 시장의 대기업이 진출해 있습니다.

- 유형별로는 MEP(기계, 전기, 배관)와 HVAC(보수 서비스, 기업 자산 관리 등)와 같은 하드 FM이 아시아태평양에서 급속히 인기를 얻고 있습니다. 시설의 열손실을 확실히 절감하여 건물의 에너지 효율을 높이고 시설의 운용 수명을 연장하고자 하는 수요의 증가가 동시장에서의 하드 FM 부문의 성장을 뒷받침하고 있습니다.

- 일본에서는 FM 사업자는 현장의 노동력 부족과 건물과 공조 및 조명 시스템 등의 설비를 포함한 노후화된 시설의 유지관리에 대처해야 합니다.

통합시설관리 산업 개요

통합시설관리 시장은 매우 세분화되어 있으며 Jones Lang LaSalle IP Inc., Sodexo Inc., ISS Facility Service, CBRE Group Inc., Compass Group PLC 등의 주요 기업이 참가하고 있습니다.

- 2023년 12월 - JLL은 텍사스주 달라스, 엘 파소, 샌안토니오, 네바다주 라스베이거스, 오클라호마 시티, 피츠버그, 위스콘신주 밀워키에있는 총 면적 100만 평방 피트에 달하는 35개의 소규모 병원과 응급시설에 통합시설관리, 임대 관리, 재산 관리, 에너지 지속 가능 서비스를 제공할 것을 발표했습니다.

- 2023년 7월 - 위스콘신주를 거점으로 하는 에너지 효율 개선 서비스 공급 기업인 ECM Holding Group, Inc.를 EMCOR, Inc.가 인수하였습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 산업 밸류체인 분석

- 시장에 주는 거시경제 요인의 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 상업활동의 회복이 성장을 견인할 전망

- 지속 가능한 녹색 건축 사례의 중시

- 시장 성장 억제요인

- 전문 인력의 부족

제6장 시장 세분화

- 유형별

- 하드 FM

- 소프트 FM

- 최종 사용자별

- 공공/인프라

- 상업

- 산업용

- 시설

- 기타

- 지역별

- 북미

- 유럽

- 아시아

- 라틴아메리카

- 호주 및 뉴질랜드

제7장 경쟁 구도

- 기업 프로파일

- Jones Lang LaSalle IP Inc.

- Sodexo Inc.

- ISS Facility Service

- CBRE Group Inc

- Compass Group PLC

- Cushman & Wakefield

- AHI Facility Services Inc

- EMCOR Facility Services

- Facilicom

- CBM Qatar LLC.

제8장 투자 분석

제9장 시장 기회와 미래 동향

CSM 25.05.15The Integrated Facility Management Market size is estimated at USD 165.11 billion in 2025, and is expected to reach USD 232.44 billion by 2030, at a CAGR of 7.08% during the forecast period (2025-2030).

An integrated facilities management (IFM) primarily brings all the facility management contracts under a single service. IFM combines complex facilities management and soft FM, such as security, cleaning, and waste management. Bringing all these different services together under a single umbrella can result in better customer service, better coordination between FM services, and consolidated costs to bring everything in under budget.

Key Highlights

- Growing emphasis on green and sustainable building practices coupled with rebounding construction activity are analyzed as drivers for the growth of the integrated facility management market.

- The growing construction activities due to various government initiatives, rising urbanization, and growing commercial construction projects in developed and developing economies have necessitated the need for integrated facility management services in the past few years.

- Integrated facility management (IFM) is experiencing an upswing due to rebounding commercial activity across various sectors due to the increased need for occupancy due to business expansion; evolving facility needs with technology advancements, and a focus on cost-efficiency.

- Augmented environmental awareness and concerned business practices have pushed integrated facility management (IFM) to exceed its conventional maintenance role as planned business drivers. IFM has appeared as a strategic driver within industries, no longer limited to being a cost center.

- The need for specialized talents poses significant challenges to advancing the integrated facility management market worldwide. The talent gap hinders IFM service providers from delivering the potential of their services as IFM involves a broad range of services from complex FM to soft FM, and finding professionals with expertise in these multiple categories is challenging.

Integrated Facility Management Market Trends

Commercial Segment to be the Largest End-user Segment

- Commercial entities cover office buildings constructed or occupied by business services, such as corporate IT and communication offices, manufacturers, and other service providers. Due to the provision of necessary fitments, interiors, and commercial buildings, decoration and management have gained significant importance, driving the commercial sector market. Commercial spaces require property accounting, renting, contract management, procurement management, and several other services, so hiring professionals becomes necessary. Due to such factors, the commercial category has further growth opportunities in the market, and the trend is likely to continue throughout the forecast period.

- Various retail businesses are expanding their presence by opening new stores in the United States, creating demand for soft FM services. For instance, in April 2023, IKEA store owner Ingka Group announced a plan to spend EUR 2 billion (USD 2.2 billion) expanding in the United States over the next three years. With this plan, the company finalized the opening of eight new big IKEA stores and nine smaller stores and upgraded existing stores in the United States, which is IKEA's second-biggest market by sales after Germany.

- Furthermore, the retail sector in countries like India has shown significant growth during 2023, with the highest record of 7.1 million square feet across key cities in the country, which is 47% more than in 2022, according to CBRE. Recently completed mall constructions primarily led to the demand for retail spaces. Fashion and apparel accounted for the largest leasing of commercial spaces with the expansion of domestic and international brands. Retail space growth in malls is witnessing higher consumer traffic, necessitating robust maintenance, cleaning, security, and energy management services.

- According to a survey by Colliers International, among real estate investors, offices and industrial and logistic properties are expected to be the most demanding asset classes in 2023, with nearly 60% of global investors intending to invest in these types of properties. Multifamily real estate came second with 48% of respondents, followed by hotels.

- Overall, rebounding commercial activities are expected to drive the need for integrated facility management to manage increased occupancy and adopt evolving technologies that allow businesses to address core activities while ensuring smooth business operations.

Asia Pacific to Hold Major Market Share

- The Asia-Pacific region is witnessing an increased development of commercial facilities, with significant investments in infrastructure projects such as hospitals, airports, manufacturing facilities, data centers, and educational institutions, which are expected to drive the Integrated FM market growth. Increasing awareness of Integrated FM outsourcing and service integration benefits is expected to fuel the market's development.

- In China, many facilities managers are incorporating sustainable building management techniques to encourage workplace efficiency and improve the infrastructure to increase asset longevity. Integrated Facility Management impacts every aspect of the organization; a facilities manager's position and the plans for strategic business management will become increasingly strategic in the country.

- China's economy offers an enormous market potential, especially in commercial hubs such as Shanghai and Beijing. Increasing government investments in the country's real estate sector would provide growth opportunities to the market. For instance, China's Five-Year Plan (2021- 2025) targets key areas to balance the country's economy.

- In December 2023, China's automotive company, BYD, announced it would invest USD 412 million to supply South Korea's automaker KG Mobility Co. Ltd with a stable supply of EV batteries. The factory is expected to start mass production in 2025. The country is home to big automotive market players, including LG Energy Solutions, Samsung SDI, SK On, and BYD. Their investment in the factory is crucial to advancing the EV ecosystem in the country.

- By type, hard FM such as MEP (Mechanical, Electrical, Plumbing) and HVAC (Maintenance Services, Enterprise Asset Management, and others) is gaining rapid popularity in Asia-Pacific. Growing demands for creating and operating a planned maintenance schedule across all areas of facility management and enhancing the energy efficiency of buildings by ensuring a reduction in heat loss from premises and lengthening a premise's operational lifespans are propelling the growth of the Hard FM segment in the market.

- In Japan, FM businesses must deal with frontline labor shortages and the upkeep of aging facilities, including buildings and equipment like air-conditioning and lighting systems. Improvements in living standards in the country have escalated demand for buildings equipped with sophisticated security features that can be managed more efficiently. This trend has been particularly evident in urban centers and is expected to gain even more momentum in the forecast period.

Integrated Facility Management Industry Overview

The integrated facility management market is highly fragmented, with significant players like Jones Lang LaSalle IP Inc., Sodexo Inc., ISS Facility Service, CBRE Group Inc., and Compass Group PLC. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023 - JLL declared that it would continue to provide Integrated Facilities Management, Lease Administration, Property Management, and Energy and Sustainability Services for 35 small-format hospitals and emergency departments totaling 1 million square feet in Dallas, El Paso, and San Antonio, Texas; Las Vegas, Nev.; Oklahoma City, Okla.; Pittsburgh, Pa.; and Milwaukee, Wis.; in addition to starting to provide Project and Development Services (PDS) for select markets.

- July 2023 - ECM Holding Group, Inc., a Wisconsin-based provider of energy efficiency retrofit services, was acquired by EMCOR Group, Inc. The group believes that adding ECM will further strengthen its position in energy efficiency specialty services and broaden the scope of its nationwide portfolio of bundled energy conservation and sustainability solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rebounding Commercial Activity Expected to Drive Growth

- 5.1.2 Emphasis on Green and Sustainable Building Practices

- 5.2 Market Restrains

- 5.2.1 Lack of Specialized Talents

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hard FM

- 6.1.2 Soft FM

- 6.2 By End -User

- 6.2.1 Public/Infrastructure

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.2.4 Institutional

- 6.2.5 Other End-Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Australia and new Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jones Lang LaSalle IP Inc.

- 7.1.2 Sodexo Inc.

- 7.1.3 ISS Facility Service

- 7.1.4 CBRE Group Inc

- 7.1.5 Compass Group PLC

- 7.1.6 Cushman & Wakefield

- 7.1.7 AHI Facility Services Inc

- 7.1.8 EMCOR Facility Services

- 7.1.9 Facilicom

- 7.1.10 CBM Qatar LLC.