|

시장보고서

상품코드

1693955

원자 시계 시장(2025-2030년) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측Atomic Clock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

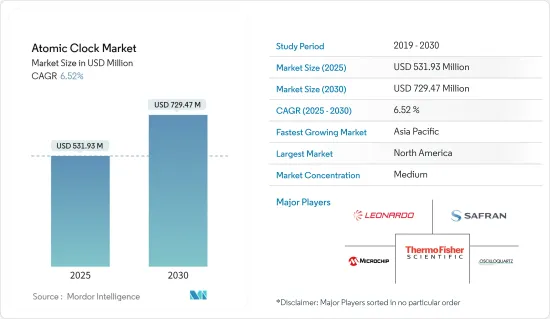

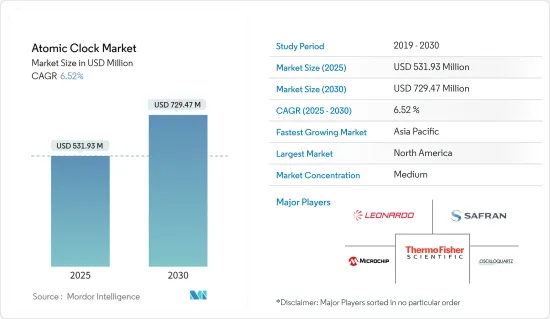

원자 시계 시장 규모는 2025년에 5억 3,193만 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 6.52%로 성장하여 2030년에는 7억 2,947만 달러에 달할 것으로 예측되고 있습니다.

원자 시계 시장은 항공 우주나 군사 부문에서 고정밀 원자시계의 요구가 높아지면서 성장하고 있습니다.

세계 네비게이션과 포지셔닝 시스템의 확대, GPS와 GNSS 시스템에서의 원자 시계의 용도의 상승도 원자 시계 시장의 성장에 박차를 가하고 있습니다.

원자 시계 시장 동향

예측 기간 동안 방위 부문이 시장 점유율을 독점

세계의 군사가 새롭고 정확한 위치 네비게이션 시스템을 통합함으로써 노후화된 항공기의 현대화를 도모하고 있기 때문에 원자 시계는 방위 부문의 최종 사용자로부터 큰 수요가 있습니다.

이와 관련하여 2018년 12월 미국 공군은 네비게이션과 위치 측정의 품질을 높이기 위해 차세대 GPS 수신기를 함대 전체에 통합한다고 발표했습니다. 미 공군 라이프사이클 관리 센터는 F-16 함대에 최신 세대의 디지털 GPS 안티 재밍 수신기(DIGAR)를 제공하기 위해 Rockwell Collins를 선택했습니다.

미국, 독일, 인도, 호주, 아랍에미리트(UAE), 중국 등 많은 국가들은 완전히 새로운 플랫폼보다는 기존의 군용기 플릿의 현대화에 투자하고 있습니다. 이 이니셔티브 하에서 미국 공군 라이프사이클 관리 센터는 Rockwell Collins를 선정해 F-16 항공기의 함대에 최신 세대의 디지털 GPS 안티 재밍 수신기(DIGAR)를 제공했습니다.

항공기 항법 보조 장치의 발전은 기업에게 새로운 시장 기회를 창출할 것으로 예측됩니다. Northrop Grumman Corporation의 All Source Adaptive Fusion 소프트웨어는 범지구적 측위 시스템(GPS) 위성 신호를 사용하지 않고 군용기나 공중 무기 시스템을 유도할 수 있게 합니다.

예측 기간 동안 북미가 최대 시장 점유율을 가질 전망

스톡홀름 국제평화연구소(SIPRI)에 따르면 세계 국방비는 2022년에 2조 달러를 돌파하였고 미국 등 군사대국은 2022년 국방예산을 대폭 추가 편성하였습니다.

미국 공군은 러시아와 중국과의 대국 간 분쟁의 요구에 부응하기 위해 차세대 항공기의 개발과 조달을 지속하고 있습니다. 일본이나 대만과 같은 나라와의 외교 및 군사 관계에서 중국으로부터의 도발적인 군사 행동에 대항하기 위해 항공기의 증강에 거액의 투자가 요구되고 있습니다.

게다가 미국이 중동지역의 군사 분쟁에 관여하고 있는 점이 전투기와 수송기의 조달에 크게 영향을 미치고 있습니다. 미 공군 예산의 대부분은 나라의 군사 행동을 지원하는 신기술의 연구 개발에 할당됩니다. 또한, 우주 부문에의 지출 증가, 상업과 방위 용도의 위성 발사 수 증가, NASA와 SpaceX에 의한 우주 탐사 활동의 확대는 미국 시장에 있어 중요한 부스터이며 북미의 원자 시계 시장을 견인하고 있습니다.

원자 시계 산업 개요

원자 시계 시장은 반고정적이며 세계적으로 사업을 전개하고 있는 참가 기업은 소수입니다. 주요 기업으로는 Thermo Fisher Scientific Inc., Oscilloquartz (Adtran Networks SE), Microchip Technology Inc., Leonardo SpA, Safran 등이 있습니다.

각 회사는 자사 제조 능력, 세계 네트워크, 제품 라인업, 연구 개발 투자, 견고한 고객 기반 등을 무기로 점유율을 획득하고 있습니다. 수요가 증가함에 따라 시장 진출기업을 제품 포트폴리오 확충에 몰두하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 유형

- 루비듐(Rb) 원자 시계

- 세슘(Cs) 원자 시계

- 수소(H) 메이저 원자 시계

- 최종 사용자

- 방위

- 전투기와 헬리콥터

- 무인 차량

- 장갑차

- 휴대용 시스템

- 군함(구축함, 프리깃 등)

- 잠수함

- 초계함

- 우주

- 방위

- 용도

- 모니터링

- 네비게이션

- 전자전

- 텔레메트리

- 통신

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 이탈리아

- 스페인

- 폴란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- IQD Frequency Products Limited

- Leonardo SpA

- Microchip Technology Incorporated

- Oscilloquartz(Adtran Networks SE)

- Stanford Research Systems

- Tekron International Limited

- VREMYA-CH JSC

- Safran

- MacQsimal(CSEM)(accelopment Schweiz AG)

- Thermo Fisher Scientific Inc

제7장 시장 기회와 미래 동향

CSM 25.05.15The Atomic Clock Market size is estimated at USD 531.93 million in 2025, and is expected to reach USD 729.47 million by 2030, at a CAGR of 6.52% during the forecast period (2025-2030).

The atomic clock market's growth is attributed to the increasing need for high-precision atomic clocks in the aerospace and military sectors. Atomic clocks guarantee accurate one-way range measurements, ensuring the user maintains the transmitted GPS signal's phase precision. Developments in quantum computing and quantum communication are expected to create better opportunities for the market.

The expansion of global navigation and positioning systems and the rise of atomic clock applications in GPS and GNSS systems are also fueling the growth of the atomic clock market. However, the high cost of deployment and maintenance may hinder the market's growth during the forecast period.

Atomic Clock Market Trends

Defense to Dominate Market Share During the Forecast Period

The atomic clocks are in huge demand from defense end-users as the global armed forces look to modernize their aging fleet by integrating new and accurate position and navigation systems. Most current-generation aircraft utilize GNSS (GPS) and TACAN positioning and navigation systems, and the demand for new aircraft would also generate parallel demand for atomic clocks during the forecast period.

On this note, in December 2018, the US Air Force announced the fleet-wide integration of next-generation GPS receivers to enhance the quality of navigation and positioning measurements. The US Air Force Life Cycle Management Center selected Rockwell Collins to provide its latest-generation Digital GPS Anti-Jam Receiver (DIGAR) for its fleet of F-16 aircraft. Similar initiatives from various armed forces are anticipated to propel the segment's growth during the forecast period.

Many countries, such as the United States, Germany, India, Australia, the United Arab Emirates, and China, are investing in modernizing their existing fleet of military aircraft rather than acquiring entirely new platforms. For instance, in December 2018, the US Air Force announced that their fighter aircraft would be fitted with next-generation GPS receivers to enhance the quality of navigation and positioning measurements. Under this initiative, the US Air Force Life Cycle Management Center selected Rockwell Collins to provide its latest-generation Digital GPS Anti-Jam Receiver (DIGAR) for its fleet of F-16 aircraft. Similar initiatives from various armed forces are anticipated to propel the segment's growth during the forecast period.

The anticipated advancement of navigational aids for aircraft is expected to create new market opportunities for companies. For instance, Northrop Grumman Corporation's All Source Adaptive Fusion (ASAF) software allows military aircraft and airborne weapon systems to guide them without using Global Positioning System (GPS) satellite signals. Such software, when used with advanced sensor systems, is anticipated to improve the operational efficiencies of the air platforms.

North America is Expected to Have the Largest Market Share During the Forecast Period

The world defense expenditure crossed over USD 2 trillion in 2022, with significant military powers such as the US surging their defense budgets in 2022, according to the Stockholm International Peace Research Institute (SIPRI). US defense spending increased by USD 71 billion from 2021 to 2022, which comprised nearly 40% of global defense expenditures.

The US Air Force continues developing and procuring next-generation aircraft to meet the demands of great power conflicts with Russia and China. The US Air Force comprises 13,247 aircraft that are part of an operational, reserve, and out-of-service fleet. The country's diplomatic and military relations with nations such as Japan and Taiwan have compelled it to drive significant investments into increasing the fleet of aircraft to counter any provocative military action from China successfully.

Furthermore, the US involvement in the military conflict in the Middle Eastern region majorly drove its procurement of attack aircraft and transport aircraft. The Department of Air Force proposed a budget request of USD 194 billion for FY2023, a USD 20.2 billion or 11.7% increase from the FY2022 budget request. A major chunk of this budget will be channeled toward the procurement of new aircraft and research and development of new technologies that can aid the military actions undertaken by the country. Also, the rising expenditure on the space sector, increasing number of satellite launches for commercial and defense applications, and growing space exploration activities from NASA and SpaceX are significant boosters for the US market, which drives the atomic clock market in the North American region.

Atomic Clock Industry Overview

The atomic clock market is semi-consolidated, with a handful of players operating globally. Thermo Fisher Scientific Inc., Oscilloquartz (Adtran Networks SE), Microchip Technology Inc., Leonardo SpA, and Safran are some of the major market players. The market is highly competitive, with players competing to gain the largest market share.

Market players compete, leveraging their in-house manufacturing capabilities, global network footprint, product offerings, research and development investments, and robust client base. Technical capabilities and product features at definite price points are also key market parameters. The increasing demand for accurate positioning and navigation capabilities drives the market players to broaden their product portfolio. With a moderate threat of new entrants, the market's competitive landscape is projected to intensify due to heightened product/service extensions and technological innovations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Rubidium (Rb) Atomic Clock

- 5.1.2 Cesium (Cs) Atomic Clock

- 5.1.3 Hydrogen (H) Maser Atomic Clock

- 5.2 End User

- 5.2.1 Defense

- 5.2.1.1 Combat Aircraft and Helicopters?

- 5.2.1.2 Unmanned Vehicles?

- 5.2.1.3 Armoured Vehicles

- 5.2.1.4 Portable Systems

- 5.2.1.5 Naval Ships (Destroyers, Frigates, etc)

- 5.2.1.6 Submarines?

- 5.2.1.7 Patrol Vessels?

- 5.2.2 Space

- 5.2.1 Defense

- 5.3 Application

- 5.3.1 Surveillance

- 5.3.2 Navigation

- 5.3.3 Electronic Warfare?

- 5.3.4 Telemetry

- 5.3.5 Communication

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Italy

- 5.4.2.6 Spain

- 5.4.2.7 Poland

- 5.4.2.8 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AccuBeat Ltd.

- 6.2.2 Excelitas Technologies Corp.

- 6.2.3 IQD Frequency Products Limited

- 6.2.4 Leonardo S.p.A.

- 6.2.5 Microchip Technology Incorporated

- 6.2.6 Oscilloquartz (Adtran Networks SE)

- 6.2.7 Stanford Research Systems

- 6.2.8 Tekron International Limited

- 6.2.9 VREMYA-CH JSC

- 6.2.10 Safran

- 6.2.11 MacQsimal (CSEM) (accelopment Schweiz AG)

- 6.2.12 Thermo Fisher Scientific Inc