|

시장보고서

상품코드

1693968

애드테크(Ad Tech 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ad Tech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

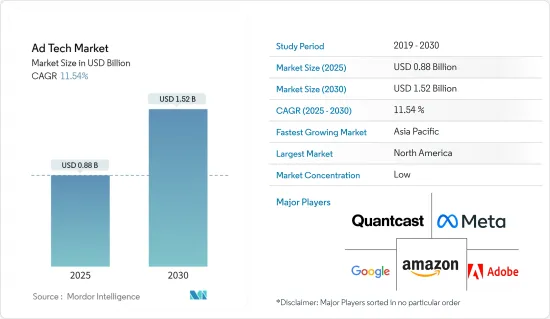

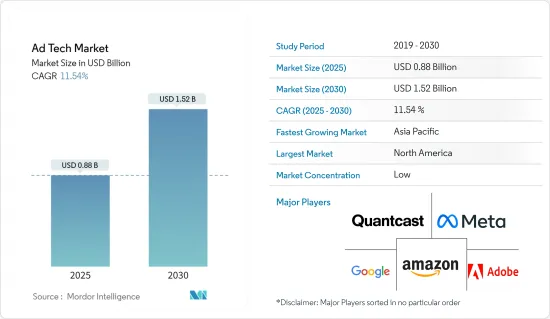

애드테크 시장 규모는 2025년에 8억 8,000만 달러, 2030년에는 15억 2,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 11.54%를 나타낼 전망입니다.

애드테크 시장은 디지털 기기와 인터넷의 이용 확대에 견인되어 지난 몇 년간 큰 성장을 이루어 왔습니다.

주요 하이라이트

- 전통적인 광고에서 온라인 광고로 지속적인 전환은 시장 성장의 주요 원동력이 되고 있습니다.

- 5G 기술은 저지연, 고속 다운로드, 네트워크 효율 향상을 제공하고, 애드테크 수요의 성장에 큰 영향을 미칠 것으로 예측됩니다.

- 온라인 전자상거래 서비스 부문은 또한 유행 기간 동안 크게 성장했습니다. 더 많은 사람들이 온라인 쇼핑과 같은 디지털 서비스를 이용하게 되었고, 이러한 산업 기업들은 잠재고객에게 도달하기 위해 광고비를 늘렸습니다.

- 그러나 애드테크의 프랙티스에 대한 일반 시민의 인식 부족이 규제상의 우려의 증대로 이어지고 있습니다.

- COVID-19의 유행은 광고산업에 큰 변혁을 가져오고, 이러한 변혁의 일부는 광고산업에 장기적인 영향을 미칠 것으로 예측됩니다. 금액을 줄이기 위해 전체 광고 비용이 줄어들고 라디오, 텔레비전 및 인쇄 미디어와 같은 전통적인 미디어 플랫폼에서 특히 눈에 띄며 광고 수입이 급격히 감소했습니다. 사람들이 집에서 보내는 시간이 길어져 디지털 미디어를 이용하게 되었기 때문에 디지털 광고비는 대폭 증가하고 있습니다. 사람이 늘어날수록 계속될 것으로 예측됩니다. 전반적으로 유통은 산업의 데이터 중심 접근 방식과 디지털 광고 채널로의 전환을 촉진하고 이 부문의 미래에 장기적인 영향을 미칩니다.

애드테크 시장 동향

모바일 기기와 스마트폰이 크게 성장

- 휴대기기의 광고는 엔터프라이즈가 타겟팅하는 잠재고객과 연결하고 상호작용할 수 있는 중요한 도구 역할을 합니다. 비즈니스 섹터의 소규모 기업은 이 섹터의 시각적 측면을 활용하여 자사의 제공물과 특징적인 브랜드 ID 확인을 강조하는 매력적인 광고를 모바일 기기에서 만들 수 있습니다.

- 또한 이미지 텍스트 광고, 배너 광고, 클릭 투 콜 광고, 클릭 투 메시지 광고, 클릭 투 다운로드 광고 등 모바일 기기용 광고에는 여러 가지 형태가 있습니다. 또한, 이동성과 용이성을 위해, 사람들은 궁극적으로 노트북이나 데스크톱보다 스마트폰 단말기를 선택합니다. 또한 비슷한 작업을 수행하는 전자의 능력을 통해 모바일 플랫폼은 점점 더 이익을 창출할 것으로 예측됩니다.

- 기업에 힘을 주고 4차 산업혁명에 진출하는 최신 마케팅 전략에는 디지털 광고와 모바일 마케팅이 포함됩니다. 가까운 미래에 온라인 판매로 전환하는 중소기업의 수가 크게 증가하고 스마트폰 사용률이 높아지면서 지상 행사나 전시회가 부족하다는 점을 감안하면 곧 필수적인 광고 채널을 공급하고 온라인 광고 시장에 좋은 영향을 미칠 것으로 입증됩니다.

- Ericsson에 따르면 세계 스마트폰 모바일 네트워크 계약 총수는 최근 약 64억 건에 이르며 예측 기간 동안 77억 건을 돌파할 것으로 예측되고 있습니다. 스마트폰의 모바일 네트워크 계약 수가 가장 많은 국가는 중국, 인도, 미국입니다. 따라서 스마트폰의 모바일 네트워크 계약 수가 세계적으로 증가하고 있기 때문에 이 시장은 같은 부문에서 성장할 충분한 기회를 목격할 것으로 예측됩니다.

- 따라서, 더 많은 고객이 물건을 탐구하고 구매하기 위해 모바일 장치를 사용하기 때문에 모바일 광고는 패션 비즈니스에 더 중요해지고 있습니다. 대상 잠재고객에게 도달하고 상호작용하기 위해 기업은 모바일 광고에 대한 투자를 크게 늘리고 있습니다.

큰 성장이 기대되는 아시아태평양

- 중국의 경제 성장과 기술에 익숙한 인구 증가로 인해 최근 인터넷 소비와 모바일 기기의 보급률이 높아지고 있습니다. 소셜 미디어의 보급에 따라, 이 나라에서는 애드테크 산업이 급성장하고 있습니다. 중국에는 바이두(Baidu), 텐센트(Tencent), 알리바바(Alibaba)와 같은 여러 거대 기술 기업들이 있습니다. 동영상 기반 플랫폼에 대한 선호도가 증가함에 따라 이 지역의 다양한 광고 형식에 대한 수요가 증가하고 있습니다.

- 디지털 혁명과 인터넷 보급률의 상승이 인도의 애드테크 시장을 견인하고 있습니다. 온라인 쇼핑 및 기타 디지털 서비스의 시작, 검색 엔진 및 소셜 미디어 플랫폼을 중심으로 디지털 광고에 대한 수요가 증가함에 따라 인도의 애드테크 산업 기업은 광고 지출을 늘릴 필요가 있습니다.

- 일본의 애드테크 시장은 데이터, 자동화, 인공지능, 프로그래매틱 광고에 대한 투자 증가로 성장할 전망입니다. 새로운 시장 진출 기업의 출현과 혁신은 일본의 애드테크 에코시스템에서 중요한 역할을 하고 있습니다. 일본에서는 모바일 앱 에코시스템이 확대되고 있어 애드테크 기업에게 큰 비즈니스 기회가 되고 있기 때문에 예측 기간 동안 모바일 광고비가 증가할 것으로 예측됩니다. 또한 동영상 광고 게재 플랫폼의 일본 시장 진출도 증가하고 있습니다.

- 호주에서는 디지털과 인터넷의 보급이 진행되고 있으며, 이 지역의 애드테크 시장의 성장을 뒷받침하고 있습니다., 광고 기술 기업에 유리한 성장 기회가 가져올 것으로 기대되고 있습니다.

- 한국에서는 투자 증가, 관민 파트너십, 성장하는 디지털 게임 시장에 의해 마케터가 고도로 인터랙티브한 아웃 오브 홈(OOH) 환경에서 잠재고객을 매료하는 절호의 기회가 가져올 것으로 예측됩니다.

- 크리에이티브한 혁신, 기술적인 채용, 윤리적인 광고에의 헌신이 조합되는 것으로, 세계의 애드테크 시장에 있어서의 뉴질랜드의 지위가 정해집니다.

애드테크 산업 개요

애드테크 시장은 세분화되어 있으며, 대기업과 중소기업 간에 치열한 경쟁이 펼쳐지고 있습니다.

- 2023년 10월 - Meta는 광고주를 위한 최초의 생성형 AI 기능을 발표했으며, 광고주는 AI를 사용하여 배경을 만들고, 이미지를 확대하고, 원본 사본을 기반으로 여러 버전의 광고 텍스트를 생성할 수 있게 되었습니다. 경치를 생성하여 제품 이미지의 외형을 변경하여 광고 소재 자산을 맞춤설정할 수 있습니다.

- 2023년 7월 - 옴니콤은 Google과 제휴하여 Google의 생성형 AI 모델을 자체 애드테크 플랫폼에 통합했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- COVID-19가 산업에 미치는 영향의 평가

- 거시 경제 동향의 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 스마트폰과 소셜미디어의 보급률 상승

- 디지털 광고의 고정밀도, 효과, 비용 효율성

- 시장 성장 억제요인

- 인지도가 낮은 가운데의 클릭봇이나 설치형 하이잭 증가

- 광고의 디지털화

- 퍼블리셔에 의한 고객 데이터에 대한 액세스 증가

- 새로운 수익 스트림 창출

- 추천 엔진을 통한 개인화에 의한 시청 체험의 향상

- 위치 기반 광고

- 소비 패턴에 도움이 되는 고객 행동 분석

- 기술기업과의 파트너십 및 협업 증가

제6장 시장 세분화

- 플랫폼별

- 공급측 플랫폼(SSP)

- 수요측 플랫폼(DSP)

- AdExchange

- 데이터 관리

- 광고 형식별

- 동영상 광고

- 소셜 미디어

- 검색 광고

- 메일

- 기타 광고 형식

- 디바이스 플랫폼별

- 데스크톱

- 모바일 스마트폰

- 기타 디바이스 플랫폼

- 최종 사용자 산업별

- 소매 및 E-Commerce

- 의료

- BFSI

- 서비스(호스피탈리티, 관광, 법률 서비스)

- 통신산업

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 기타 라틴아메리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Google LLC

- Amazon.com, Inc.

- Meta Platform, Inc.

- Quantcast

- Adobe

- Adform A/S

- MediaMath

- Microsoft Corporation

- Zeta Global Holdings Corp.

- Mediaocean

제8장 투자 분석

SHW 25.05.15The Ad Tech Market size is estimated at USD 0.88 billion in 2025, and is expected to reach USD 1.52 billion by 2030, at a CAGR of 11.54% during the forecast period (2025-2030).

The ad tech market has witnessed considerable growth over the past few years, driven by the growing use of digital devices and the Internet. With the increasing adoption of smartphones and social media platforms, digital advertising has become essential to marketing plans for businesses worldwide.

Key Highlights

- The continuous shift from traditional to online advertising is the main driving force behind the market's growth. The proliferation of the Internet and the increase in the number of Internet users has made it possible to reach a larger audience through digital ads. People spend more time online for work, entertainment, and socializing, and advertisers can now reach them online.

- 5G technology is expected to significantly impact ad tech demand growth, offering lower latency, faster download speeds, and improved network efficiency. These advances introduce new opportunities for ad tech companies to provide targeted, innovative, data-driven advertising solutions to enhance user experience.

- The online and e-commerce services sector also significantly boosted during the pandemic. As more people turn to digital services such as online shopping, companies in these industries have increased their advertising spending to reach potential audiences. This has increased the demand for online advertising, especially on search engines and social media platforms.

- However, a lack of public awareness of ad tech practices has led to augmented regulatory concerns. Consumer protection agencies are becoming increasingly concerned about data being used and collected for advertising efforts, leading to strict regulations that threaten the growth of the ad tech industry.

- The COVID-19 pandemic has brought about significant transformations in the advertising industry, and several of these changes are expected to have a long-lasting impact on the sector. With reduced consumer spending and economic uncertainty, many brands have opted to decrease their advertising budgets, leading to an overall decrease in ad spending. This decline has been particularly noticeable in traditional media platforms such as radio, television, and print media, which have experienced a sharp decrease in advertising revenues. On the other hand, as people spend more time at home and engage with digital media, there has been a substantial increase in digital ad spending. This upward trend is predicted to persist even after the pandemic subsides as more individuals become acquainted with e-commerce and digital channels. Overall, the pandemic has augmented the industry's shift to a more data-driven approach and digital advertising channels, with long-term effects for the sector's future.

Ad Tech Market Trends

Mobile Devices and Smartphones to Witness Significant Growth

- Advertising on mobile devices acts as a significant tool for firms to connect with and interact with their target audience. Small firms in the business sector may make use of the visual aspect of the sector to create engaging advertising on mobile devices that highlights their offerings and distinctive brand identities.

- Furthermore, there are several forms of advertising for mobile devices, such as image text and banner ads, click-to-call ads, click-to-message ads, and click-to-download ads. Additionally, due to their mobility and ease, people ultimately choose smartphone devices over laptops or desktops. Also, due to the former's ability to undertake similar tasks, mobile platforms are predicted to become increasingly profitable.

- Modern marketing strategies that would empower firms and bring them into the fourth industrial revolution include digital advertising and mobile marketing. In due course, it would supply the essential advertising channels and prove to produce a good influence on the online advertising market, given the significant number of SMEs transitioning to online sales, rising smartphone usage, and the lack of on-ground events or exhibits in the near future.

- According to Ericsson, the total number of smartphone mobile network subscriptions worldwide reached around 6.4 billion in the recent years and is forecasted to surpass 7.7 billion during the forecast period. China, India, and the United States are the countries with the most significant number of smartphone mobile network subscriptions. Hence, with the rise in the overall number of smartphone mobile network subscriptions worldwide, the market is expected to witness ample opportunities to grow within the market sector.

- Therefore, as more customers use their mobile devices to explore and buy things, mobile advertising is becoming more crucial for the fashion business. In order to reach and interact with their target audience, firms are increasing their investment in mobile advertising significantly.

Asia-Pacific Expected to Witness Major Growth

- China's economic growth and a rising tech-savvy population have resulted in higher penetration of internet consumption and mobile device penetration in recent years. Due to the increased proliferation of social media, the ad tech industry is growing rapidly in the country. China hosts several tech giants such as Baidu, Tencent, and Alibaba. The rising inclination toward video-based platforms has also increased the demand for various advertising formats in the region.

- The digital revolution and growing internet penetration are driving the ad tech market in India. The rise of online shopping and other digital services, as well as increasing demand for digital advertising, especially on search engines and social media platforms, have compelled businesses in the Indian ad tech industry to increase their advertisement spending.

- The ad tech market in Japan is anticipated to grow due to increasing investment in data, automation, artificial intelligence, and programmatic advertising. The emergence of new market players and innovation plays a critical role in the ad tech ecosystem in Japan. Mobile ad spending is projected to increase in Japan during the forecast period, attributed to the country's expanding mobile app ecosystem, representing a massive opportunity for ad tech companies. Japan also has an increased influx of video advertising serving platforms entering the Japanese market.

- The rising digital and internet penetration in Australia is bolstering the growth of the regional ad tech market. The rising adoption of artificial intelligence (AI), machine learning (ML), Virtual reality (VR), and augmented reality (AR) technologies is expected to provide lucrative growth opportunities for advertising technology players. The growing use of social media apps and the rising gaming industry also create numerous options for the ad tech market growth in Australia.

- Increased investments, public-private partnerships, and the ever-growing digital gaming market are projected to provide tremendous opportunities for marketers to attract audiences in highly interactive out-of-home (OOH) environments in South Korea. Programmatic Digital out-of-home advertising is opening up new revenue streams for media owners to drive additional revenues.

- A combination of creative innovation, technical adoption, and a dedication to ethical advertising define New Zealand's position in the global ad tech market. Because of the market's projected expansion and emphasis on regional specifics and legal compliance, New Zealand is positioned to have a significant impact on the changing face of digital advertising.

Ad Tech Industry Overview

The Ad tech market is fragmented, with high competition among large and small companies. Some of the players include Adobe, Google LLC, Amazon.com Inc., Meta Platform Inc., and Quantcast. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023 - Meta launched its first generative AI features for advertisers, allowing them to use AI to create backgrounds, expand images, and generate multiple versions of ad text based on their original copy. The first among the trio of new features allows an advertiser to customize their creative assets by generating multiple different backgrounds to change the look of their product images. Another feature, image expansion, allows advertisers to adjust their assets to fit different aspect ratios required across various products, like Feed or Reels.

- July 2023 - Omnicom has partnered with Google to integrate the latter's generative AI models into its Adtech platform. The integration aims to improve the capabilities of Omnicom's Adtech platform while providing personalized and effective advertising opportunities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 An Assessment of the Impact of COVID-19 on the Industry

- 4.3 Impact of Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in the Adoption of Smartphones and Social Media

- 5.1.2 High Precision, Effectiveness, and Cost Efficiency of Digital Advertising

- 5.2 Market Restraint

- 5.2.1 Rise of Click Bots and Install Hijacks Amid Low Public Awareness

- 5.3 Digital Transformation in Advertising

- 5.3.1 Increased Access of Customer Data for Publishers

- 5.3.2 Generation of New Revenue Streams

- 5.3.3 Better Viewer Experience Through Personalization Through Recommendation Engines

- 5.3.4 Location-Based Advertising

- 5.3.5 Customer Behavior Analytics Helping with Spending Pattern

- 5.3.6 Increasing Partnerships and Collaboration with Technology Companies

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 Supply Side Platform (SSP)

- 6.1.2 Demand Side Platform (DSP)

- 6.1.3 Ad Exchange

- 6.1.4 Data Management

- 6.2 By Ad Format

- 6.2.1 Video Advertising

- 6.2.2 Social Media

- 6.2.3 Search Advertising

- 6.2.4 Email

- 6.2.5 Other Ad Formats

- 6.3 By Device Platforms

- 6.3.1 Desktop

- 6.3.2 Mobile Devices and Smartphones

- 6.3.3 Other Device Platforms

- 6.4 By End-user Industry

- 6.4.1 Retail and E-Commerce

- 6.4.2 Healthcare

- 6.4.3 BFSI

- 6.4.4 Services (Hospitality, Tourism, Legal Services)

- 6.4.5 Telecommunications

- 6.4.6 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Spain

- 6.5.2.5 Italy

- 6.5.2.6 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Australia

- 6.5.3.5 South Korea

- 6.5.3.6 New Zealand

- 6.5.3.7 Rest of Asia-Pacific

- 6.5.4 Middle-East and Africa

- 6.5.4.1 Saudi Arabia

- 6.5.4.2 United Arab Emirates

- 6.5.4.3 South Africa

- 6.5.4.4 Nigeria

- 6.5.4.5 Egypt

- 6.5.4.6 Rest of Middle East and Africa

- 6.5.5 Latin America

- 6.5.5.1 Brazil

- 6.5.5.2 Mexico

- 6.5.5.3 Argentina

- 6.5.5.4 Colombia

- 6.5.5.5 Rest of Latin America

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google LLC

- 7.1.2 Amazon.com, Inc.

- 7.1.3 Meta Platform, Inc.

- 7.1.4 Quantcast

- 7.1.5 Adobe

- 7.1.6 Adform A/S

- 7.1.7 MediaMath

- 7.1.8 Microsoft Corporation

- 7.1.9 Zeta Global Holdings Corp.

- 7.1.10 Mediaocean