|

시장보고서

상품코드

1694017

승무원 산소 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Crew Oxygen Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

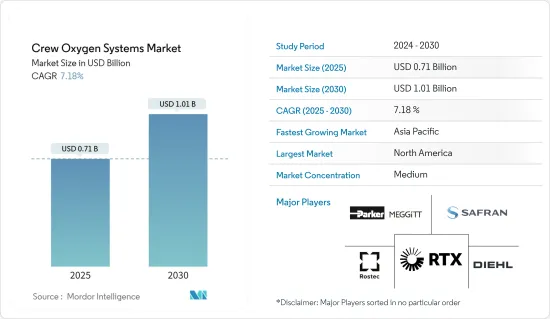

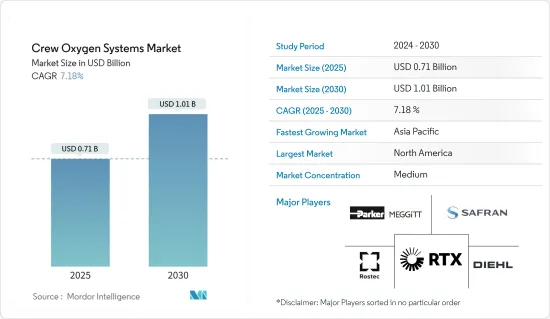

승객용 산소시스템 시장 규모는 2025년에 7억 1,000만 달러, 2030년에는 10억 1,000만 달러에 달할 것으로 예측됩니다. 예측기간(2025-2030년)의 CAGR은 7.18%를 나타낼 전망입니다.

주요 하이라이트

- 전 세계 민간 항공우주 산업의 급성장은 승무원 산소 시스템 시장에 영향을 미치는 주요 요인입니다. 주요 항공사들의 항공기 기단 확장 이니셔티브, 상업용 항공 수요 증가, 군용기 현대화 프로젝트는 승무원 산소 시스템에 대한 수요 증가에 종합적으로 기여하고 있습니다. 항공 여객 수송량 증가는 시장 수요를 충족시키기 위해서 세계에서 보다 많은 항공기 발주에 연결되어 있습니다.

- 게다가 세계 국방군이 항공기술의 진보를 우선하고 있기 때문에 군용 최종 사용자가 수요에 영향을 미치고 있습니다.

- 미국 연방항공국(FAA)과 유럽연합항공안전기관(EASA)이 정한 국제항공안전기준은 승무원 산소시스템 수요에 크게 영향을 미치고 있습니다. 이러한 안전 표준 및 규정 준수 사항은 안전 인증 요건을 포함하여 진화하는 엄격한 규제 상황에 공헌하고 있으며, 중요한 항공기 부품의 설계, 개발, 승인 프로세스를 직접 형성하고 있습니다.

승무원 산소 시스템 시장 동향

예측 기간 동안 산소 저장 시스템이 시장을 독점

- 산소 저장 시스템은 순수한 산소 공급을 저장하거나 생성하고, 산소를 조정하고, 필요에 따라 희석하고, 탑승자 또는 승객에게 분배하도록 설계되었습니다. 산소 시스템은 통상의 운항에 사용되는 일도 있으며, 특정의 상황하에서 보조 산소를 공급하기 위해서 사용되는 일도, 화재, 연기, 가압 상실시에 긴급용 산소를 공급하기 위해서 사용되는 일도 있습니다. .

- 보조 산소 또는 긴급 산소 시스템의 제공 및 사용에 관한 규제는 국제 민간 항공 기관(ICAO)의 표준 및 권장 사례(SARPS)가 제공하는 지침을 기반으로합니다. 항공기와 비가압항공기를 구별하여 더욱 비행을 실시하는 고도에 따른 구체적인 요건을 정하고 있습니다.

- 또한 2023년에는 Boeing과 Airbus가 각각 528대와 735대의 항공기를 인도했으며, 이는 2022년의 480대와 663대와 비교하여 증가한 수치입니다. 공식 A320 생산량은 월 45대이며 2021년 말부터 이 수준을 유지하고 있습니다. 2023년에는 월 평균 48대의 A320을 인도한 반면, 2022년에는 43대를 인도했습니다.

예측기간 중 북미가 시장에서 가장 높은 점유율을 차지

- 북미가 승무원 산소시스템 시장에서 가장 높은 점유율을 차지하고 있는 것은 미국의 높은 항공 수요, 대규모 항공기 보유 대수, 국방비에 대한 상당액의 투자로 인한 것입니다. 보잉은 미국에서 선도적인 항공기 공급업체 중 하나이며 승무원 관련 산소 시스템에 대한 상당한 수요를 창출하고 있습니다. 미국의 항공 산업은 파일럿 부족이라는 과제에 직면하고 있습니다.

- 미국에서는 2017-2022년에 걸쳐 총 1,500대 이상의 신형 여객기가 납품되고, 2023-2029년에는 2,000대 이상의 신형 제트기가 납입될 전망입니다. Aerosystems는 미국의 BoeingB737 및 B787 항공기용 산소 시스템의 주요 공급업체입니다. 미국은 예측 기간 동안 다른 북미 국가에 비해 신규 항공기 납품 수요가 가장 높아질 것으로 예측됩니다.

- 게다가 일반 항공 부문에서는 OEM 기술 혁신을 중시하고 신제품을 출시하고 있습니다. 이 솔루션은 휴대용 산소 시스템, 긴급 강하 장비, 다양한 산소 시스템 액세서리로 구성되어 있습니다.

승무원 산소 시스템 산업 개요

승무원 산소 시스템 시장은 시장에서 중요한 점유율을 가진 소수의 로컬 및 세계 진출기업이 존재하기 때문에 그 성질상 반쯤 통합되어 있습니다.

승무원 산소시스템 시장의 주요 시장 진출기업은 RTX Corporation, Safran, Parker-Meggitt(Parker Hannifin Corporation), Rostec, Diehl Stiftung & Co.KG 등입니다. 또한 주요 OEM은 경량으로 선진적 산소시스템을 개발하기 위해 연구개발에 고도로 투자하고 있습니다. 2023년 6월 사프란(Safran)이 에어리퀴드(Air Liquide)의 어드밴스드 기술의 항공용 산소 및 질소 사업을 인수한다고 발표했습니다. 시장 점유율을 크게 잡는 일부 현지 및 참가 기업과 세계의 참가 기업이 지배적인 존재감을 나타내고 있는 것이 특징입니다.

승무원 산소시스템 시장 진출기업은 RTX Corporation, Safran, Parker-Meggitt(Parker Hannifin Corporation), Rostec, Dehl Stiftung & Co.KG입니다.이 주요 시장 진출 기업은 혁신과 연구 개발에의 헌신을 나타내, 경량으로 고도로 선진적인 산소 시스템의 창조에 엄청난 투자를 실시했습니다.

이 성장 동향은 주요 OEM 업체의 최첨단 산소 시스템 제조를 목표로 한 연구 개발에 적극적으로 참여하고 있음을 보여줍니다. Air Liquide사와의 독점 협상은 그 일례입니다.이 전략적 인수 프로젝트는 사프란 에어로시스템의 목표, 특히 기내 산소 발생 시스템(OBOGS) 부문의 제품 라인업의 강화에 합치하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 성과

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 용도

- 민간항공

- 군용기

- 일반항공

- 컴포넌트

- 산소 마스크

- 산소 저장 시스템

- 산소 공급 시스템

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Cobham Limited

- Safran

- RTX Corporation

- Parker-Meggitt(Parker Hannifin Corporation)

- Rostec

- Aeromedix, LLC

- Aviation Oxygen Etc.

- Aerox Aviation Oxygen Systems, LLC

- Precise Flight, Inc.

- PFW Aerospace GmbH

- Caeli Nova

- Diehl Stiftung & Co. KG

제7장 시장 기회와 앞으로의 동향

SHW 25.05.15The Crew Oxygen Systems Market size is estimated at USD 0.71 billion in 2025, and is expected to reach USD 1.01 billion by 2030, at a CAGR of 7.18% during the forecast period (2025-2030).

Key Highlights

- The rapid growth of the commercial aerospace industry across the globe is a key factor influencing the crew oxygen systems market. Aircraft fleet expansion initiatives by major airlines, the rising demand for commercial aviation, and military aircraft modernization projects collectively contribute to increased demand for crew oxygen systems. The increase in air passenger traffic is leading to more aircraft orders around the world to meet market demand. This, in turn, leads to increased cabin crew strength, thus ultimately leading to a significant rise in demand for crew oxygen systems.

- Moreover, the military end users influence the demand as defense forces worldwide prioritize advancements in aviation technology. The need for sophisticated oxygen systems is driven by evolving military strategies that involve extended flight durations and operations at high altitudes.

- International aviation safety standards, such as those set by the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), significantly influence the demand for crew oxygen systems. These safety standards and compliances, which include safety certification requirements and contribute to an evolving stringent regulatory landscape, directly shape the design, development, and approval processes of critical aircraft components. On the other hand, the high cost associated with the development of oxygen systems hinders the market growth.

Crew Oxygen Systems Market Trends

Oxygen Storage Systems Dominates the Market During the Forecast Period

- Oxygen storage systems are designed to store or generate a supply of pure oxygen and to regulate, dilute as required, and then distribute that oxygen to crew or passengers. Depending upon the type and the role of the aircraft concerned, an oxygen system may be used for normal operations, to provide supplemental oxygen for specific situations, or to provide emergency oxygen in the event of smoke, fire, fumes, or loss of pressurization.

- Regulations for the provision and use of supplemental or emergency oxygen systems are based on the guidance provided by the International Civil Aviation Organization (ICAO) Standards and Recommended Practices (SARPS). The regulations differentiate between pressurized and non-pressurized aircraft and then provide specific requirements based on the altitude at which the flight is to be conducted. For instance, in June 2022, Diehl Aviation built its own emergency oxygen supply generator for onboard passenger aircraft.

- Furthermore, in 2023, in total, Boeing and Airbus delivered 528 and 735 aircraft compared to 480 and 663, respectively, in 2022. The official A320 production rate is 45 aircraft per month and has remained at this level since the end of 2021. On average, the company delivered 48 A320s per month in 2023 compared to 43 in 2022. Thus, an increase in aircraft deliveries will create the market to propel during the forecast period.

North America Holds Highest Shares in the Market During the Forecast Period

- North America holds the highest shares in the crew oxygen systems market, owing to the high demand for air travel in the US, large fleet size, and significant investments in defense spending. The US Department of Transportation (DoT) announced that the air passenger traffic number in 2022 crossed around 854 million. Boeing is among the leading aircraft suppliers in the United States and is responsible for creating significant demand for crew-related oxygen systems. The US airline industry is facing a challenge with the pilot shortage. However, this presents an opportunity for growth and development in the aviation sector. The high demand for travel in the US has created a need for more pilots. Whenever new orders for aircraft are placed, the corresponding demand for oxygen systems is also generated.

- A total of 1500+ new passenger aircraft were delivered in the United States between 2017 and 2022, and a further 2000+ new jets are expected to be delivered to the region during 2023-2029. Carleton Technologies Inc., Collins Aerospace, and Safran Aerosystems were major suppliers of oxygen systems in the United States for Boeing B737 and B787 aircraft. The United States accounted for 80% of the total air passenger traffic in North America in 2022. Therefore, the United States is expected to generate the highest demand for new aircraft deliveries compared to other North American countries over the forecast period. Airlines are looking to expand their fleet size to cater to the growing demand for air travel, which may generate significant demand for crew oxygen systems.

- Furthermore, in the general aviation sector, original equipment manufacturers (OEMs) have emphasized on innovation and launched new products. For instance, in 2023, Aerox, a US-based company, offered aircraft oxygen systems related to turboprop and light jets. These solutions consist of portable oxygen systems, emergency descent gear, and various oxygen system accessories. This is also expected to aid the growth of oxygen systems in the country's general aviation sector.

Crew Oxygen Systems Industry Overview

The crew oxygen systems market is semi-consolidated in nature due to the presence of a few local and global players holding significant shares in the market. The key aerospace players such as The Boeing Company, Bombardier Inc., and Airbus SE shape market dynamics through their aircraft production and technology integration initiatives.

The key market players in the crew oxygen systems market include RTX Corporation, Safran, Parker-Meggitt (Parker Hannifin Corporation), Rostec, and Diehl Stiftung & Co. KG. Furthermore, key OEMs highly invest in research and development to develop lightweight and highly advanced oxygen systems. This growth trend highlights the huge demand for reliable and advanced oxygen systems to support the expanding global fleet. For instance, in June 2023, Safran announced that it had entered into exclusive negotiations with Air Liquide to acquire the aeronautical oxygen and nitrogen activities of Air Liquide's advanced Technologies. This acquisition project would complement Safran Aerosystems' product range especially on-board oxygen generation systems (OBOGS) will enable Safran to become a leading player through systems integration.The crew oxygen systems market exhibits a semi-consolidated structure, characterized by the dominant presence of a select number of local and global players holding substantial market shares. Key aerospace industry leaders, including The Boeing Company, Bombardier Inc., and Airbus SE, play pivotal roles in shaping market dynamics through their influential contributions to aircraft production and technology integration initiatives.

Prominent participants in the crew oxygen systems market comprise RTX Corporation, Safran, Parker-Meggitt (Parker Hannifin Corporation), Rostec, and Diehl Stiftung & Co. KG. These key market players demonstrate a commitment to innovation and research and development, investing significantly in the creation of lightweight and highly advanced oxygen systems. This ongoing emphasis on technological advancement underscores the substantial demand for dependable and cutting-edge oxygen systems to cater to the needs of the expanding global fleet.

This growth trend shows that key original equipment manufacturers (OEMs) are actively engaged in research and development endeavors aimed at producing state-of-the-art oxygen systems. An exemplary instance is the announcement made by Safran in June 2023, revealing exclusive negotiations with Air Liquide to acquire the aeronautical oxygen and nitrogen activities of Air Liquide Advanced Technologies. This strategic acquisition project aligns with Safran Aerosystems' objectives, particularly in enhancing its product range, specifically in the domain of onboard oxygen generation systems (OBOGS). Through this initiative, Safran aims to establish itself as a leading player in the market, leveraging its prowess in systems integration.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters' Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial Aviation

- 5.1.2 Military Aviation

- 5.1.3 General Aviation

- 5.2 Component

- 5.2.1 Oxygen Mask

- 5.2.2 Oxygen storage system

- 5.2.3 Oxygen Delivery system

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Cobham Limited

- 6.2.2 Safran

- 6.2.3 RTX Corporation

- 6.2.4 Parker-Meggitt (Parker Hannifin Corporation)

- 6.2.5 Rostec

- 6.2.6 Aeromedix, LLC

- 6.2.7 Aviation Oxygen Etc.

- 6.2.8 Aerox Aviation Oxygen Systems, LLC

- 6.2.9 Precise Flight, Inc.

- 6.2.10 PFW Aerospace GmbH

- 6.2.11 Caeli Nova

- 6.2.12 Diehl Stiftung & Co. KG