|

시장보고서

상품코드

1694028

중국의 의약품 포장 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)China Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

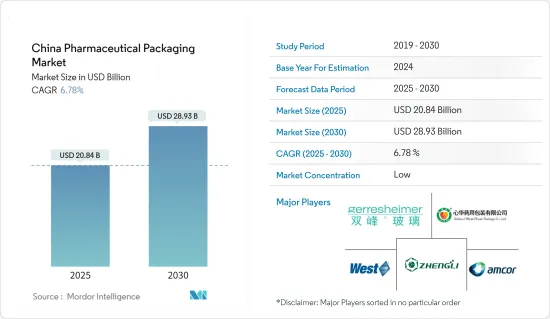

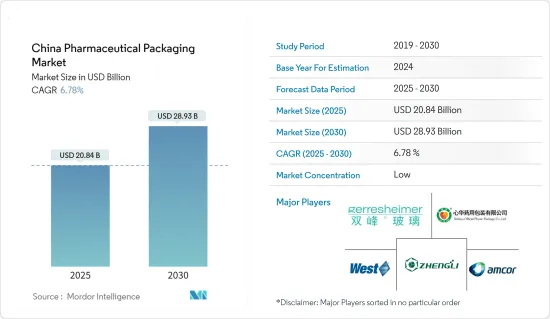

중국의 의약품 포장 시장 규모는 2025년에 208억 4,000만 달러, 2030년에는 289억 3,000만 달러에 이를 것으로 예측되고 있습니다.예측 기간(2025-2030년)의 CAGR은 6.78%를 나타낼 전망입니다.

중국의 의약품 섹터의 성장은 중국의 의약품 포장 기업에 비즈니스 기회를 가져옵니다.

주요 하이라이트

- 중국의 의료산업의 변화를 추진하는 중국 정부의 시책에 의해 의약품 포장 섹터의 개발이 촉진될 것으로 기대됩니다.

- 중국의 의약품 산업은 중국 식품 약품 감독 관리국(CFDA)이나 국가 의약품 감독 관리국(NMPA) 등 당국이 시행하는 엄격한 규제 기준의 틀 안에서 운영되고 있습니다. 포장 설계, 재료 구성, 표시 요건, 안전 프로토콜의 다양한 측면을 포함하고 있습니다. 이 규격의 준수는 양보할 수 없는 것이며, 포장 실무에 있어서 세세한 부분까지 세심한 주의를 지불할 필요가 있습니다.

- 나노기술은 빛, 습기, 산소 등의 환경요인으로부터 의약품을 보호함으로써 의약품의 안정성을 높일 수 있는 나노구조 재료의 개발을 가능하게 합니다. 나노기술은 약물의 상태를 모니터링하여 온도, 습도, 빛에 노출 등의 요인에 대해 실시간으로 피드백을 제공할 수 있는 스마트 포장 솔루션의 개발을 가능하게 합니다.

- 의약품 포장 시장에서는 병, 바이알, 블리스터 팩, 라벨 등의 원료가 포장 자재의 제조에 필수적입니다. 원자재 공급업체는 특히 시장에서 지배적인 위치를 차지하거나 원자재가 부족할 때 상당한 협상력을 발휘합니다. 그들은 이 힘을 이용해, 가격을 인상하거나, 의약품 포장 제조업체에 불리한 조건을 밀어붙일 수가 있습니다.그 결과, 포장 자재의 생산 비용이 상승할 가능성이 있습니다.

- 플라스틱 포장은 경량, 고내구성, 다용도성, 비용 효과 등의 유리한 특성으로 인해 포장 산업에서 엄청난 존재가 되고 있습니다. 중국에서의 재료 포장의 개발에는 풍부한 역사가 있어 확립된 산업 체인으로 성숙해 왔습니다.

중국 의약품 포장 시장 동향

베를린이 창고 총 취급량으로 리드

- 중국의 의약품 유리 앰풀과 바이알 시장은 중국이 의약품 산업의 표준 틀을 확립한 것으로 확대가 전망되고 있습니다. 제약회사는 그 내구성, 비반응성, 투명성, 환경적합성, 다용도성에서 유리제 포장을 채용하는 케이스가 늘고 있습니다.

- 특히 지난 몇 년간의 COVID-19 팬데믹과 관련된 의약품과 예방접종 수요에 의해 바이알과 앰풀 수요가 늘어나고 있습니다.

- CNN에 따르면 2023년 3월 현재 전 세계에서 약 130억 회분의 COVID-19 백신이 투여되고 있으며, 중국 본토는 이 중 약 34억 9,100만 회분을 차지하고 있습니다.

- 선진국에서는 유리 바이알과 앰플이 널리 사용되고 있습니다.

- 마찬가지로 제약과 생명과학의 최종 사용자에 있어서의 바이알과 앰풀 수요도 증가하고 있습니다.

- 2023년 10월, 유리의 개척자인 샷이 차세대 유형 i의 붕규산 유리관을 발표했습니다. 제약 변환기는 회사의 유리 튜브를 사용하여 고품질 바이알, 앰플, 주사기 또는 카트리지를 생산하여 간단하고 복잡한 약물을 보관합니다.

패션 의류 부문이 수익을 이끌

- 접이식 상자는 2 차 포장 제품의 가장 인기있는 유형입니다. 이 판지는 다양한 방법으로 사용할 수 있습니다. 접이식 박스 포장은 빛, 습기, 오염 등의 외부 요인으로부터 의약품을 보호함으로써 의약품의 안전성을 확보합니다.

- 인쇄된 의약품 판지에 대한 수요는 산업의 까다로운 경쟁으로 인해 증가하고 있습니다. 최신 인쇄 의약품 포장 시장의 혁신은 변조 방지 기능과 어린이 증거 기능을 통합하고 있습니다.

- 불충분한 복약 준수의 문제가 만연하고 있어 만성 질환의 합병증이나 의료 지출 증가로 연결되어 있습니다.

- 알약 상자는 재사용 가능한 멀티 컴파트먼트 용기로 특정 시간에 복용하는 약을 넣도록 설계되었습니다. 물집 팩과 달리 전문적인 조치가 필요하지 않으며 환자, 비공식 간병인 또는 의료 제공자가 채울 수 있습니다. 여러 의료 제공업체는 복수의 만성 질환을 앓는 노인을 위해서, 약제 정보를 기재한 2차 포장으로서 블리스터 팩, 알약 박스, 폴딩 카톤의 사용을 추천하고 있습니다.

- 중국의 의약품 시장은 성장 전망과 시장 규모라는 점에서 여전히 가장 중요한 시장 중 하나입니다.

- 국제 당뇨병 연합에 따르면 중국 성인의 당뇨병 유병률은 2045년까지 12.5%가 될 것으로 예측되고 있습니다. 회사는 블리스터를 보호하기 위해 견고하고 다재다능한 종이기 포장을 사용하고 있습니다.

중국 의약품 포장 시장 개요

중국의 의약품 포장 시장은 세계 기업과 중소기업에 의해 매우 세분화되어 있습니다. Gerresheimer Shuangfeng Pharmaceutical Glass (Danyang) Co. Ltd (Gerresheimer AG), West Pharmaceutical Services Inc., Taishan Xinhua Pharmaceutical Packaging Co. Ltd, Ningbo Zhengli Pharmaceutical Packaging, AmcorGroup GMBH 등이 있습니다. 시장 진출 기업은 제품 제공을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 제휴 및 인수 등의 전략을 채택하고 있습니다.

- 2023년 11월 - 지속 가능한 포장 솔루션의 세계 공급자로 알려진 Amco는 의료용 라미네이트 솔루션의 최신 진보를 발표했습니다. 이 제품은 최종 포장의 이산화탄소 배출량을 크게 줄임으로써 의료기기 용도에 필수적인 성능 기준을 충족하는 동시에 환자의 안전성을 손상시키지 않고 지속 가능한 목표를 달성하기 위해 의료 기업을 지원합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 생태계 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 의약품 포장에 관한 산업의 규제와 시책, 기준

- 의약품 포장 산업에서의 최근 혁신과 신제품 개발 동향

- 원료 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 포장에 관한 규제 기준과 위조품에 대한 엄격한 규범

- 혁신적인 차세대 포장 솔루션에 의한 나노기술의 영향

- 시장 성장 억제요인

- 공급기업의 협상력에 의한 원료비용의 변동

제6장 신흥 동향 분석과 주요 성공 요인

제7장 시장 세분화

- 1차 포장별

- 의약품 플라스틱 병

- 병과 항아리

- 물집 포장

- 프리필러블 주사기

- 바이알과 앰풀

- 점적 용기

- 프리필러블 흡입기

- 기타 1차 포장 제품(파우치, 튜브, 캡, 클로저 등)

- 2차 포장별

- 접이식 상자와 카톤(종이 베이스)

- 골판지(종이 베이스)

- 가방 및 파우치(연질)

- 클램쉘(종이플라스틱)

- 기타 2차 포장 제품(트레이, 라벨 등)

제8장 경쟁 구도

- 기업 프로파일

- Gerresheimer Shuangfeng Pharmaceutical Glass(Danyang) Co. Ltd(Gerresheimer AG)

- West Pharmaceutical Services Inc.

- Taishan Xinhua Pharmaceutical Packaging Co. Ltd

- Ningbo Zhengli Pharmaceutical Packaging

- Amcor Group GMBH

- Perlen Packaging(Suzhou) Co. Ltd

- Shandong Pharmaceutical Glass Co. Ltd

- Yuhuan Kang-jia Enterprise Co. Ltd

- Dongguan Fukang Plastic Products Co. Ltd

- JOTOP Glass

- Jiangsu Hanlin Pharmaceutical Packaging

- Hangzhou Xunda Packaging Co., Ltd.

- Luoyang Dirante Pharmaceutical Packaging Material Co. Ltd

- Share of China Pharmaceutical Packaging Companies in Global Market

제9장 투자 전망

제10장 시장의 미래

SHW 25.05.15The China Pharmaceutical Packaging Market size is estimated at USD 20.84 billion in 2025, and is expected to reach USD 28.93 billion by 2030, at a CAGR of 6.78% during the forecast period (2025-2030).

The growth of the Chinese pharmaceutical sector creates business opportunities for the country's pharmaceutical packaging companies. China's pharmaceutical packaging firms are encouraged to develop research and development teams to explore innovative, environmentally friendly, safe, functional, and sustainable packaging materials and products.

Key Highlights

- The Chinese government's policies to advance the transformation of the country's medicine industry are expected to promote the development of the pharmaceutical packaging sector. China is actively upgrading its pharmaceutical packaging facilities and materials and diversifying its pharmaceutical products, bringing new opportunities to pharmaceutical packaging firms.

- The Chinese pharmaceutical industry operates within a framework of stringent regulatory standards enforced by authorities such as the China Food and Drug Administration (CFDA) and the National Medical Products Administration (NMPA). These standards encompass various aspects of packaging design, material composition, labeling requirements, and safety protocols. Compliance with these standards is non-negotiable and requires meticulous attention to detail in packaging practices.

- Nanotechnology enables the development of nanostructured materials that can enhance the stability of drugs by protecting them from environmental factors such as light, moisture, and oxygen. This leads to increased shelf-life and efficacy of pharmaceutical products. Nanotechnology enables the development of smart packaging solutions that can monitor the condition of the drug and provide real-time feedback on factors such as temperature, humidity, and exposure to light. This helps ensure the quality and efficacy of pharmaceutical products throughout their lifecycle.

- In the pharmaceutical packaging market, raw materials such as bottles, vials, blister packs, and labels are essential for manufacturing packaging materials. Suppliers of raw materials wield significant bargaining power, especially when they hold a dominant position in the market or when the raw material is scarce. They can leverage this power to increase prices or impose unfavorable terms on pharmaceutical packaging manufacturers. This, in turn, can lead to higher production costs for packaging materials.

- Plastic packaging has emerged as a formidable player in the packaging industry due to its advantageous properties, such as lightweight, high durability, versatility, and cost-effectiveness. It has widespread application in various industries, including medicine, healthcare, and other sectors requiring packaging support. The development of material packaging in China has a rich history and has matured into a well-established industrial chain. In this chain, the upstream sector comprises raw material suppliers responsible for providing synthetic resins and plastic additives for manufacturing plastic packaging materials.

China Pharmaceutical Packaging Market Trends

Berlin Leads in Total Warehousing Take-up

- The Chinese pharmaceutical glass ampoules and vials market is expected to expand as China has established a standard framework for the pharmaceutical industry. The country is increasingly focusing on the stability of pharmaceutical packaging materials during drug storage and the safety of the packaging when used. Pharmaceutical companies increasingly use glass packaging because of its durability, non-reactivity, transparency, eco-friendliness, and versatility. Additionally, glass vials are in high demand due to increasing investment and R&D in healthcare systems and rising drug spending.

- Notably, the demand for vials and ampoules has grown due to the demand for medications and vaccinations related to the COVID-19 pandemic in the past few years. Manufacturers of pharmaceutical and parenteral packaging have greatly boosted their capacity for production. Millions of vials and ampoules are produced monthly by manufacturers operating at full capacity.

- According to CNN, as of March 2023, approximately 13 billion COVID-19 vaccine doses had been administered globally, with Mainland China accounting for almost 3.491 billion of this total.

- Glass vials and ampoules are becoming more widely used in developed countries. As a result of COVID-19, the healthcare and pharmaceutical sectors are growing in emerging nations, which presents the potential for the Chinese market. Additionally, players operating in the region focus on increasing their production capacity.

- Similarly, the demand for vials and ampoules among end users of pharmaceutical and life sciences is increasing. The market continues to favor these end users for demand variation, so players are concentrating on launching new products.

- In October 2023, the glass pioneer SCHOTT introduced next-generation type I Borosilicate glass tubing. This new product and its associated services will support three key trends in the pharma industry: the development of complex pharmaceuticals, sustainability, and digitalization. Pharmaceutical converters use the company's glass tubing to produce high-quality vials, ampoules, syringes, or cartridges to store simple and complex drugs. In particular, the company sees an increasing demand for biopharmaceutical products in the future, where packaging and materials will need to meet more stringent requirements and regulations.

Fashion and Apparel Segment to Lead in Revenue

- Folding cartons constitute the most popular type of secondary packaging product. These cartons are versatile and can be used in many ways. Folding cartons offer several advantages, including flexibility, rigidity, and easy and cost-effective flat-pack shipping and storage. The folding box packaging ensures the safety of pharmaceutical products by protecting them from external factors like light, moisture, and contamination. This protection helps preserve the potency and integrity of the medications. Implementing radio-frequency identification (RFID) smart labeling technology to prevent product replication in the pharmaceutical industry will also contribute to market expansion.

- The demand for printed pharmaceutical cartons is rising due to the industry's stiff competition. In addition to providing ample space for regulatory information and brand advertising, these cartons also offer more room than small bottles, vials, and containers. The latest printed pharmaceutical packaging market innovation incorporates tamper-evident and child-proof features. These features are achieved through advanced material technology and design, further driving the demand for pharmaceutical printed cartons.

- The problem of inadequate medication adherence is prevalent, leading to an increase in chronic disease complications and healthcare expenditures. Packaging interventions such as pillboxes and blister packs have been widely recommended to address this issue, leading to a growing market for such products.

- Pillboxes are reusable multi-compartment containers designed to hold medications to be consumed at specific times. Unlike blister packs, they do not require professional action and can be filled by patients, informal caregivers, or healthcare providers. Multiple healthcare providers recommend using blister packs, pillboxes, and folding cartons as secondary packaging with medication information for the aging with multiple chronic diseases.

- The Chinese pharmaceutical market is still one of the most important in terms of growth prospects and market size. The expansion of insurance coverage, the aging population, the growing middle class with higher healthcare needs, and chronic diseases are the main reasons for this growth.

- According to the International Diabetes Federation, the forecasted prevalence of diabetes among adults in China will be 12.5 % by 2045. Blister packaging is the most common type of pharmaceutical packaging used in China. Major pharmaceutical companies use sturdy and versatile folding carton packaging to protect the blister. Therefore, with the growth of pharmaceutical blister packaging, there would be a consequent growth in demand for folding cartons.

China Pharmaceutical Packaging Market Overview

The Chinese pharmaceutical packaging market is highly fragmented due to global players and small and medium-sized enterprises. Some of the major players in the market are Gerresheimer Shuangfeng Pharmaceutical Glass (Danyang) Co. Ltd (Gerresheimer AG), West Pharmaceutical Services Inc., Taishan Xinhua Pharmaceutical Packaging Co. Ltd, Ningbo Zhengli Pharmaceutical Packaging, and Amcor Group GMBH. Market players are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2023 - Amcor, a renowned global provider of sustainable packaging solutions, launched its latest advancement in Medical Laminates solutions. This innovative offering facilitates the creation of fully recyclable, all-film packaging within the polyethylene recycling stream. By significantly reducing the carbon footprint of the final package, this new solution meets the performance standards essential for medical device applications while supporting medical companies in advancing their sustainability objectives without compromising patient safety.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Regulations, Policies, and Standards for Pharmaceutical Packaging

- 4.5 Recent Innovations and New Product Development in the Pharmaceutical Packaging Industry

- 4.6 Raw Material Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Regulatory Standards on Packaging and Stringent Norms Against Counterfeit Products

- 5.1.2 Impact of Nanotechnology due to Innovative and New-generation Packaging Solutions

- 5.2 Market Restraints

- 5.2.1 Fluctuations in Raw Material Cost due to Suppliers' Bargaining Power

6 EMERGING TREND ANALYSIS AND KEY SUCCESS FACTORS

7 MARKET SEGMENTATION

- 7.1 By Primary Packaging

- 7.1.1 Pharmaceutical Plastic Bottles

- 7.1.2 Bottles and Jars

- 7.1.3 Blister Packaging

- 7.1.4 Pre-fillable Syringes

- 7.1.5 Vials and Ampoules

- 7.1.6 IV Containers

- 7.1.7 Prefillable Inhalers

- 7.1.8 Other Primary Packaging Products (Pouches, Tubes, Caps, Closures, Etc.)

- 7.2 By Secondary Packaging

- 7.2.1 Folding Boxes and Cartons (Paper-based)

- 7.2.2 Corrugated Shipping Containers (Paper-based)

- 7.2.3 Bags and Pouches (Flexible)

- 7.2.4 Clamshells (Paper and Plastic)

- 7.2.5 Other Secondary Packaging Products (Trays, Labels among Others)

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Gerresheimer Shuangfeng Pharmaceutical Glass (Danyang) Co. Ltd (Gerresheimer AG)

- 8.1.2 West Pharmaceutical Services Inc.

- 8.1.3 Taishan Xinhua Pharmaceutical Packaging Co. Ltd

- 8.1.4 Ningbo Zhengli Pharmaceutical Packaging

- 8.1.5 Amcor Group GMBH

- 8.1.6 Perlen Packaging (Suzhou) Co. Ltd

- 8.1.7 Shandong Pharmaceutical Glass Co. Ltd

- 8.1.8 Yuhuan Kang-jia Enterprise Co. Ltd

- 8.1.9 Dongguan Fukang Plastic Products Co. Ltd

- 8.1.10 JOTOP Glass

- 8.1.11 Jiangsu Hanlin Pharmaceutical Packaging

- 8.1.12 Hangzhou Xunda Packaging Co., Ltd.

- 8.1.13 Luoyang Dirante Pharmaceutical Packaging Material Co. Ltd

- 8.2 Share of China Pharmaceutical Packaging Companies in Global Market