|

시장보고서

상품코드

1835644

바이오프리저베이션 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Biopreservation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

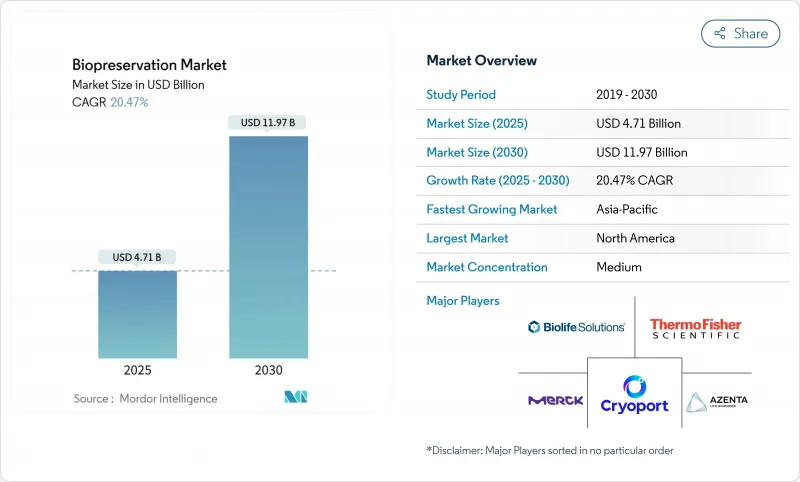

바이오프리저베이션 시장은 2025년 47억 1,000만 달러 규모에 달하고, CAGR 20.47%를 반영하여 2030년에는 119억 7,000만 달러로 확대될 것으로 예측됩니다.

이러한 급성장의 배경에는 개인 맞춤형 의료의 가속화, 첨단 생물학적 제제에 대한 규제 당국의 지원 강화, 백신 시대의 초저온 물류의 전개가 있습니다. 바이오뱅크 재고의 급속한 디지털화와 인공지능 분석은 시료의 유용성을 높이고 장기적인 시료 유지를 촉진하고 있습니다. 이와 함께 극저온 로봇과 예측 모니터링에 대한 투자는 신뢰성을 높이고 수작업으로 인한 실수를 줄여 바이오프리저베이션 시장의 저변을 더욱 넓히고 있습니다. 비결빙성 고분자 매트릭스에서 얼음 결정화 억제제 배지까지, 공급 측면의 기술 혁신은 연구 및 임상 환경 전반에 걸쳐 기술적 깊이를 더하고 새로운 수익원을 개척하고 있습니다.

세계의 바이오 프리저베이션 시장 동향 및 인사이트

헬스케어 및 생명과학 R&D 예산

미국에서는 기업 및 공공 R&D 예산이 연간 2,000억 달러를 넘어섰고, 제약회사는 일관된 품질을 보장하는 전문업체에 샘플 처리를 의뢰하고 있습니다. 디스커버리 생명과학(Discovery Life Sciences)와 같은 기업들은 유세포 분석과 분자 분석을 통합하여 아웃소싱 서비스가 어떻게 시료 처리량을 가속화하고, 사이클 타임을 단축하며, 소모품 및 장비에 대한 새로운 수요를 창출할 수 있는지를 보여주고 있습니다. 강력한 자금 조달은 또한 멀티오믹스 데이터 세트를 마이닝하는 인공지능 모델을 지원하여 바이오프리저베이션 시장에 진입하는 재료의 양과 다양성을 증가시킵니다. 자금 조달이 가능하다면, 높은 초기 설비 비용이 완화되고, 연구 네트워크가 자동화된 에너지 효율이 높은 냉동고와 클라우드 기반 모니터링을 채택할 수 있게 됩니다.

개인 맞춤형 의료를 위한 바이오뱅크

현재 50만 명이 넘는 영국 바이오뱅크와 같은 대규모 이니셔티브는 수동적 보존에서 동적 데이터 통합 플랫폼으로의 전환을 강조하고 있습니다. 브라질의 기관 리포지토리는 정밀 진단을 지원하는 다양하고 종단적인 시료에 대한 전 세계적인 수요를 검증하고 있습니다. 시료의 다양성이 증가함에 따라 통일된 품질 관리 프로토콜이 요구되고 있으며, 이에 따라 고급 배지 및 유리화 장비의 판매가 증가하고 있습니다. 유전체, 단백질체학, 전자의무기록의 데이터가 통합됨에 따라 바이오프리저베이션 시장은 보존 기간을 연장하고 프리미엄 서비스 계약을 촉진하는 반복적인 시료 회수를 통해 이익을 얻을 수 있습니다.

저온 장비의 자본 비용 및 운영 비용

고성능 냉동고의 가격은 15,000-5만 달러이며, 여기에 매년 1대당 3,000-5,000 달러의 전기료가 소요됩니다. 소규모 연구기관에서는 구매와 유지보수에 어려움을 겪고 있으며, 비용에 민감한 지역에서는 도입이 늦어지고 있습니다. 온도 최적화 및 설비 공유를 통해 비용을 절감할 수 있지만, 선행 투자 장벽이 신흥국 바이오프리저베이션 시장의 즉각적인 침투를 억제하고 있습니다.

보고서에서 분석된 기타 촉진 및 억제요인은 다음과 같습니다.

- 병원 기반 병원 내 샘플 보관

- 분산형 임상시험 및 현장 진료 요구 사항

- 보관 중 생존율 저하 위험

부문 분석

장비 판매는 로봇화, 예지보전, 무냉매 기술에 대한 노력을 반영하여 CAGR 22.74%로 가속화되고 있습니다. 바이오프리저베이션 장비 시장 규모는 2025년 17억 8,000만 달러에서 2030년 49억 6,000만 달러로 증가할 것으로 예측됩니다. 초저온 냉동고에는 현재 사물인터넷 센서가 장착되어 있어 사전 예방적 유지보수를 위해 작동 데이터를 전송하는 사물인터넷 센서가 장착되어 있습니다. 자동화된 보관 모듈은 연간 수백만 개의 바이알 병을 선별, 피킹, 재수납할 수 있어 인건비를 절감하고 생물 시료의 추적성을 향상시킬 수 있습니다. 기체상 질소 시스템의 병행 발전은 서리 축적을 억제하고 액체 질소 소비를 줄이며 안전 및 ESG 요구 사항을 모두 충족시킵니다.

소모품 및 액세서리는 샘플량 증가와 함께 꾸준한 성장세를 보이고 있습니다. 미디어와 하드웨어의 통합 솔루션은 고유한 동결 방지제가 자동화 플랫폼이 제공하는 정확한 냉각 프로파일에 최적화되는 수렴 추세를 보이고 있습니다. 이러한 공생은 고객들을 포용하고, 경상 수익의 흐름을 강화하며, 바이오프리저베이션 시장에서 공급업체의 장기적인 회복력을 뒷받침하고 있습니다.

인체조직은행은 여전히 가장 큰 매출을 차지하고 있지만, 줄기세포는 CAGR 23.55%의 높은 성장세를 보이고 있습니다. 제대혈 기반 오미실지의 승인으로 고품질 줄기세포 보존이 임상적으로 유용하다는 것이 입증되었습니다. 현재는 정교한 프로토콜을 통해 줄기세포의 조달부터 해동까지 관리하여 재생수술이나 면역치료를 위한 생존성을 보장하고 있습니다.

장기 이식은 아직 실험적으로 어렵지만, 쥐의 신장 해동과 이식에 성공한 것은 임상 장기 보존을 향한 구체적인 진전을 보여줍니다. DNA, 혈장 및 기타 생물학적 유체는 콜드체인 비용을 절감하고 세계 연구 협력의 폭을 넓히는 상온 고분자 매트릭스의 혜택을 누리고 있습니다. 이러한 생물 시료의 다양화는 최종 시장의 기회를 확대하고 생물 보존 시장의 장기적인 모멘텀을 강조합니다.

생물 보존 시장 보고서는 제품 유형(생물 보존 매체 및 장치(온도 유지 장치, 소모품, 기타)), 생물 시료(인체 조직, 기타), 보존 방법(동결보존, 유리화, 기타), 응용 분야(바이오 뱅킹, 기타), 최종 사용자(바이오 뱅크 및 유전자 은행, 기타), 지역별로 분류되어 있습니다.), 지역별로 분류되어 있습니다. 시장 예측은 금액(USD)으로 제공됩니다.

지역 분석

북미는 2024년 바이오프리저베이션 시장의 38.48%를 차지하며 가장 규모가 큰 지역 점유율을 차지했습니다. 세포 및 유전자 치료의 안전성에 대한 연방 정부의 지침과 안정적인 벤처 자금으로 미국은 극저온 장비 및 특수 물류 공급망의 결절점이 되고 있습니다. 캐나다 컨소시엄과 멕시코의 제조 코리도(Manufacturing Corridor)는 생태계를 보완하고, 국경을 초월한 효율성을 높이고, 시장 접근성을 넓히고 있습니다.

아시아태평양은 23.41%의 연평균 복합 성장률(CAGR)로 명백한 성장 동력입니다. 중국의 바이오의약품 매출은 2029년까지 1조 4,000억 위안이 넘을 것으로 예상되며, 냉동고, 질소발생장치, 모니터링 소프트웨어 등 인프라 수주에 박차를 가할 것으로 보입니다. 일본의 경기 부양책과 세제 혜택은 국내 바이오테크놀러지 시장의 3배 성장을 목표로 첨단 유리응고 키트와 자동 바이오뱅크 모듈의 채택을 가속화할 것입니다. 인도의 계약 제조업체는 생산 연동 인센티브를 활용하여 세계 감사 기준에 부합하는 GMP 콜드체인 창고를 건설하여 보존세포치료제의 새로운 수출 경로를 개척하고 있습니다.

유럽은 성숙하면서도 발전하는 과정에 있습니다. 영국의 1,600만 시료 규모 확대는 국립 바이오뱅크에 대한 정부의 지속적인 지원을 입증하는 것입니다. 독일과 프랑스는 에너지 효율 의무를 통합하고, -70℃ 운영 및 액체 질소 회수 시스템 구축을 장려하고 있습니다. 환경, 사회, 거버넌스 요구사항은 공급업체들이 보다 친환경적인 냉각 기술을 제공하도록 장려하고 있으며, 지역 바이오프리저베이션 시장에서 지속가능성과 성능이 함께 발전할 수 있도록 보장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 밸류체인/공급망 분석

- 규제 상황

- 기술 전망

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모·성장 예측(금액-달러)

- 제품 유형별

- 생물 보존 배지

- 장비

- 온도 유지 장치

- 소모품

- 액세서리 및 모니터링 시스템

- 생물 시료 별

- 세포 및 세포주

- 인체조직

- 장기

- 줄기세포

- 기타 바이오유체(DNA/RNA, 혈장 등)

- 보존 방법별

- 동결보존

- 유리화

- 저체온 보존

- 동결건조

- 용도 분야별

- 바이오뱅크

- 재생의료

- Drug Discovery 및 전임상시험

- 기타 용도

- 최종사용자별

- 바이오뱅크 및 유전자 은행

- 병원 및 이식 센터

- 제약 기업 및 바이오테크놀러지 기업

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 개요

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Azenta US Inc.

- BioLife Solutions Inc.

- Cryoport Inc.

- Cesca Therapeutics Inc.

- Core Dynamics Ltd.

- Custom Biogenic Systems Inc.

- Lifeline Scientific Inc.

- MVE Biological Solutions

- Princeton CryoTech Inc.

- Danaher Corp.

- Sartorius AG

- Eppendorf AG

- STEMCELL Technologies Inc.

- Lonza Group AG

- Bio-Rad Laboratories Inc.

- CryoConcepts LP

제7장 시장 기회와 전망

LSH 25.10.27The biopreservation market reached a valuation of USD 4.71 billion in 2025 and is set to expand to USD 11.97 billion by 2030, reflecting a 20.47% CAGR.

The surge is underpinned by the acceleration of personalized medicine, stronger regulatory support for advanced biologics, and deployment of vaccine-era ultra-low temperature logistics. Rapid digitization of biobank inventories plus artificial-intelligence analytics is increasing specimen utility and encouraging long-term sample maintenance. In parallel, investments in cryogenic robotics and predictive monitoring improve reliability and reduce manual error, further broadening the biopreservation market footprint. Supply-side innovation, ranging from non-cryogenic polymer matrices to ice-recrystallization-inhibitor media, adds technological depth and opens new revenue streams across research and clinical settings.

Global Biopreservation Market Trends and Insights

Healthcare & life-science R&D budgets

Record-high corporate and public R&D allocations now exceed USD 200 billion annually in the United States, prompting pharmaceutical firms to outsource sample handling to specialist providers that guarantee consistent quality. Companies such as Discovery Life Sciences integrate flow cytometry with molecular analytics, illustrating how outsourced services accelerate specimen throughput, reduce cycle times, and stimulate fresh demand for consumables and equipment. Robust funding also supports artificial-intelligence models that mine multi-omic datasets, increasing the quantity and diversity of materials entering the biopreservation market. Capital availability cushions high upfront equipment costs, allowing research networks to adopt automated, energy-efficient freezers and cloud-based monitoring.

Biobanking for personalized medicine

Large-scale initiatives like the UK Biobank, now surpassing 500,000 participants, underscore the shift from passive storage to dynamic data integration platforms. Brazil's institutional repositories follow suit, validating a global appetite for diverse, longitudinal specimens that underpin precision diagnostics. Growing sample diversity demands unified quality control protocols, which translate into higher sales of advanced media and vitrification devices. As genomic, proteomic, and electronic health-record data converge, the biopreservation market benefits from repeat specimen retrievals that extend storage horizons and encourage premium service contracts.

Cryogenic equipment capital & operating costs

High-performance freezers range from USD 15,000-50,000, compounded by electricity expenses of USD 3,000-5,000 per unit each year. Smaller institutes struggle with acquisition and maintenance, delaying adoption in cost-sensitive regions. Though temperature optimization and shared facilities mitigate expenses, the upfront barrier suppresses immediate penetration of the biopreservation market in emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Hospital-based in-house sample storage

- Decentralized trials and point-of-care needs

- Risk of viability loss during preservation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment sales are accelerating at a 22.74% CAGR, reflecting the push toward robotics, predictive maintenance, and cryogen-free technology. The biopreservation market size for equipment is on track to climb from USD 1.78 billion in 2025 to USD 4.96 billion by 2030. Ultra-low temperature freezers now feature internet-of-things sensors that transmit operational data for proactive servicing. Automated storage modules can sort, pick, and re-rack millions of vials annually, cutting labor costs and enhancing biospecimen traceability. Parallel advances in vapor-phase nitrogen systems curb frost accumulation and reduce liquid nitrogen consumption, addressing both safety and ESG requirements.

Consumables and accessories exhibit steady growth alongside rising sample volumes. Integrated media-hardware solutions illustrate a convergence trend, where proprietary cryoprotectants are optimized for precise cooling profiles delivered by automated platforms. This symbiosis locks in customers and strengthens recurring-revenue streams, anchoring long-term resilience for suppliers within the biopreservation market.

Human tissue banks still account for the largest revenue slice, yet stem cells are the star performer with a 23.55% CAGR. Approval of cord-blood-based Omisirge validates the clinical payoff of high-quality stem-cell preservation. Sophisticated protocols now govern everything from sourcing to thaw, ensuring viability for regenerative surgeries and immunotherapies.

Organs remain experimentally challenging, but the successful thaw-and-transplant of a rat kidney demonstrates tangible progress toward clinical organ repositories. DNA, plasma, and other bio-fluids benefit from room-temperature polymer matrices that slash cold chain costs and broaden global research collaboration. This biospecimen diversification magnifies end-market opportunities and underscores the long-run momentum of the biopreservation market.

The Biopreservation Market Report is Segmented by Product Type (Biopreservation Media and Equipment [Temperature-Maintaining Units, Consumables and More), Biospecimen ( Human Tissues and More), Preservation Method (Cryopreservation, Vitrification and More), Application Area (Biobanking and More), End User (Biobanks & Gene Banks, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America continues to command the largest regional stake, holding 38.48% of the biopreservation market in 2024. Federal guidance on cell and gene therapy safety plus steady venture funding make the United States the supply-chain nexus for cryogenic equipment and specialized logistics. Canadian consortia and Mexican manufacturing corridors complement the ecosystem, adding cross-border efficiencies and broadening market access.

Asia-Pacific is the clear growth engine at a 23.41% CAGR. Chinese biopharma revenues are set to exceed CNY 1.4 trillion by 2029, fueling infrastructure orders for freezers, nitrogen generators, and monitoring software. Japan's stimulus packages and tax incentives aim to triple the domestic biotech market, accelerating adoption of advanced vitrification kits and automated biobank modules. India's contract manufacturers leverage Production-Linked Incentives to build GMP cold-chain warehouses that conform to global audit standards, opening new export pathways for preserved cell therapies.

Europe holds a mature yet evolving position. The United Kingdom's 16 million-sample expansion validates sustained government backing for national biobanks. Germany and France integrate energy-efficiency mandates, encouraging deployment of -70 °C operations and liquid-nitrogen recapture systems. Environmental, social, and governance requirements push suppliers to deliver greener cooling technologies, ensuring that sustainability and performance advance together within the regional biopreservation market.

- Thermo Fisher Scientific

- Merck

- Azenta

- BioLife Solutions

- Cryoport Inc.

- Cesca Therapeutics

- Core Dynamics Ltd.

- Custom Biogenic Systems

- Lifeline Scientific

- MVE Biological Solutions

- Princeton CryoTech

- Danaher Corp.

- Sartorius

- Eppendorf

- Stem Cell Technologies

- Lonza Group

- Bio-Rad Laboratories

- CryoConcepts LP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Healthcare & Life-Science R&D Budgets

- 4.2.2 Expansion Of Biobanking For Personalised Medicine

- 4.2.3 Rapid Adoption Of Hospital-Based, In-House Sample Storage

- 4.2.4 Decentralised Trials Driving Point-Of-Care Preservation

- 4.2.5 Repurposed Ultra-Low-Temp Logistics From mRNA Supply Chain

- 4.2.6 Venture Funding Into Cryogenic Robotics & Monitoring

- 4.3 Market Restraints

- 4.3.1 High Capital & Operating Costs Of Cryogenic Equipment

- 4.3.2 Risk Of Cell/Tissue Viability Loss During Preservation

- 4.3.3 Medical-Grade Liquid-Nitrogen Supply-Chain Fragility

- 4.3.4 ESG Pressure On Energy-Intensive Long-Term Storage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Type

- 5.1.1 Biopreservation Media

- 5.1.2 Equipment

- 5.1.2.1 Temperature-Maintaining Units

- 5.1.2.2 Consumables

- 5.1.2.3 Accessories & Monitoring Systems

- 5.2 By Biospecimen

- 5.2.1 Cells & Cell Lines

- 5.2.2 Human Tissues

- 5.2.3 Organs

- 5.2.4 Stem Cells

- 5.2.5 Other Bio-fluids (DNA/RNA, Plasma, etc.)

- 5.3 By Preservation Method

- 5.3.1 Cryopreservation

- 5.3.2 Vitrification

- 5.3.3 Hypothermic Storage

- 5.3.4 Lyophilisation

- 5.4 By Application Area

- 5.4.1 Biobanking

- 5.4.2 Regenerative Medicine

- 5.4.3 Drug Discovery & Pre-clinical Testing

- 5.4.4 Other Applications

- 5.5 By End User

- 5.5.1 Biobanks & Gene Banks

- 5.5.2 Hospitals & Transplant Centres

- 5.5.3 Pharmaceutical & Biotechnology Companies

- 5.5.4 Academic & Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Merck KGaA

- 6.3.3 Azenta US Inc.

- 6.3.4 BioLife Solutions Inc.

- 6.3.5 Cryoport Inc.

- 6.3.6 Cesca Therapeutics Inc.

- 6.3.7 Core Dynamics Ltd.

- 6.3.8 Custom Biogenic Systems Inc.

- 6.3.9 Lifeline Scientific Inc.

- 6.3.10 MVE Biological Solutions

- 6.3.11 Princeton CryoTech Inc.

- 6.3.12 Danaher Corp.

- 6.3.13 Sartorius AG

- 6.3.14 Eppendorf AG

- 6.3.15 STEMCELL Technologies Inc.

- 6.3.16 Lonza Group AG

- 6.3.17 Bio-Rad Laboratories Inc.

- 6.3.18 CryoConcepts LP

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment