|

시장보고서

상품코드

1836435

미국의 약물전달 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United States Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

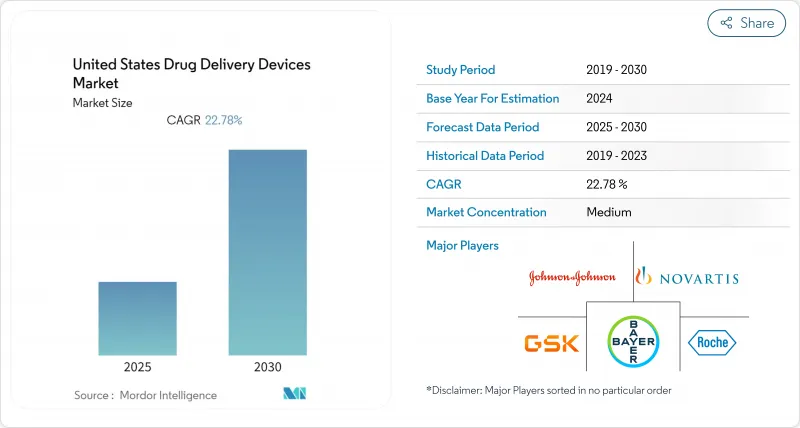

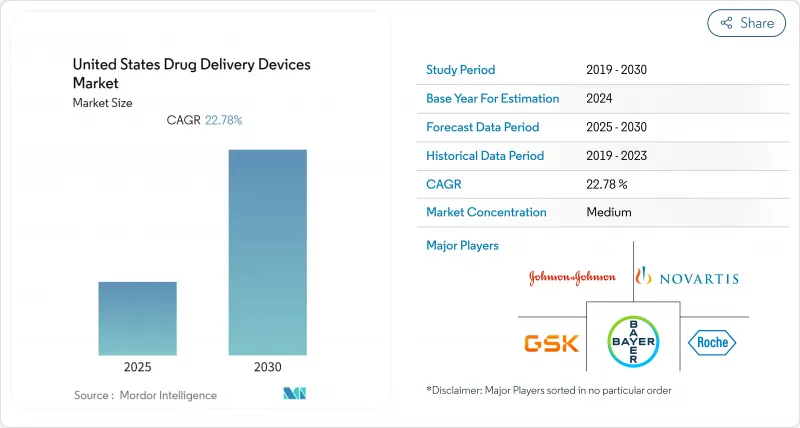

미국의 약물전달 기기 시장은 2025년에 512억 4,000만 달러로 평가되고, 2030년에는 752억 달러에 이르며, CAGR 6.71%를 나타낼 것으로 예측됩니다.

성장의 배경에는 만성 질환 부담 증가, 지속적인 제품 혁신,자가 투여 및 재택 관리를 선호하는 환자 중심 치료에 대한 결정적인 축족이 있습니다. 기존의 스타일은 여전히 적절하지만, 기기 제조업체는 어드히어런스와 실세계 결과를 개선하기 위해 입증된 플랫폼에 연결성, 센서 및 분석을 중첩합니다. 병원은 계속 수요의 핵심을 담당하고 있지만, 상환 동향과 고액의 면책 금액에 의해 외래 진료소나 거실에서의 치료가 증가해, 채널 경제가 재구축되고 있습니다. 경쟁은 생물학적 제제에 대응하는 주사기, 스마트 흡입 시스템, 통원 횟수를 줄이는 온보디 펌프 등으로 격화하고 있습니다. 동시에 FDA의 디지털 헬스 자문위원회는 엄격한 안전 기준을 유지하면서도 소프트웨어 주도형 기기의 피드백 루프를 단축하고, 혁신자에게 기회와 컴플라이언스 비용을 모두 창출하고 있습니다.

미국의 약물전달 기기 시장 동향과 인사이트

높은 환자 부담액과 텔레헬스의 보급이 뒷받침되는 자기 투여 지향의 높아짐

환자의 자기 부담액이 증가함에 따라 간편한 투여 형태에 대한 수요가 가속화되고 있습니다. 원격 의료는 유행에 따라 급증하고 현재도 증가하고 있으며 임상의가 직접 훈련을받지 않고 연결된 펜, 펌프 및 흡입기에 대해 사용자를 안내 할 수 있습니다. 2023년 1,150억 달러의 약제비에 직면한 병원은 입원기간과 약국경비를 줄이기 위해 재택요법을 장려했습니다. 2025년 4월에 FDA가 편두통의 디지털 치료제 CT-132를 인가한 것은 재택 케어로 이행한 소프트웨어 강화형 요법의 기세를 강조하는 것입니다. 지속적인 포도당 모니터링은 당뇨병 치료의 초기 단계부터 시작되며, 개인의 라이프 스타일에 맞는 기기 선택이 가능해져, 자기 관리에 의한 투약에 대한 신뢰가 높아집니다.

확장하는 생물학적 제형 파이프라인은 고급 비경구 전달 플랫폼을 필요로 합니다.

FDA의 승인에 차지하는 고분자 치료제의 비율이 증가하고 점도 제어, 온도 안정성, 정확한 미량 투여를 유지하는 기기가 요구되고 있습니다. 5-10mL의 피하 투여가 가능한 웨어러블 주사기가 임상시험을 개시하고 있어, 수액센터를 대신하는 집에서의 투여가 가능하게 되어 있습니다. 제약 제조업체가 제형의 점도와 환자의 편안함을 비교 검토하는 동안, 초기 기기 전략은 이제 분자 설계에 통합되어 있습니다. 고분자 전문 지식을 가진 수탁 제조업체는 특히 보스턴과 베이 지역의 바이오 클러스터에서 해자를 확장합니다. 아스트라제네카가 파이프라인 업데이트에서 지질 나노입자와 경구 생물학적 제형의 플랫폼을 강조함에 따라 생물학적 제제를 지원하는 시스템에 대한 업계의 주목은 더욱 높아졌습니다.

FDA의 엄격한 시판 전 심사에 의해 배합제 시장 투입까지의 기간이 연장

신약과 기기 조합의 승인주기는 36개월에 달할 수 있으며 벤처기업의 개발자를 괴롭히고 있습니다. 유저피법의 초안은 심사의 합리화를 목표로 하고 있지만, 당분간은 새로운 문서 레이어를 도입하게 될 것으로 보입니다. 기업은 현재 컨셉 설계 초기에 규제 당국의 전문가를 통합하고 있는데, 이는 비용 증가와 연구 개발의 장기화로 이어집니다. 확립된 품질 시스템을 보유한 선도적인 기존 기업은 소규모 진출기업이 문서화의 엄격함과 싸우는 가운데 경쟁 거리를 넓히고 있습니다. FDA의 지도자 교체 및 예산 압박은 심사 순서와 자원 배분에 영향을 미칠 수 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 기술의 진보와 제품 혁신

- 만성질환이 높은 부담

- 디지털 컴패니언 용도에 대한 상환 불확실성

부문 분석

흡입기는 가장 빠른 CAGR 9.13%를 나타내 성장을 지속하고, 미국의 약물전달 기기 시장 전체를 웃돌았지만, 점유율 30.34%를 차지하는 주사기와 주사 바늘에는 아직 미치지 못했습니다. 이 급성장은 추진제 재설계와 천식을 관리하는 2,500만 명의 미국인에게 중요한 올바른 기술을 보장하는 디지털 용량 카운터로 인해 발생합니다. GSK의 저탄소 벤틀린 시제품은 지속가능성을 새로운 차별화 요인으로 자리매김하고 있습니다.

흡입 기술의 기세는 생물 제제의 전신 투여가 가능한 소프트 미스트나 드라이 파우더 플랫폼에 대한 투자에 조타를 끊고 있습니다. 바늘이 없는 주사기는 현재 샤프를 강하게 싫어하는 사용자를 유치하고 있으며, 자동 주사기와 펜은 집에서의 정확한 생물학적 제제 투여를 위해 스프링식의 기구를 활용하고 있습니다. 임베디드 펌프는 2025년 2월에 FDA가 검토한 안과용 삽입제와 같은 장기 치료 틈새를 채웠습니다. 이러한 다양한 모달리티는 미국의 약물전달 기기 시장에서 대응 가능한 기반을 확대하고 단일 기술에 대한 의존도를 저하시킵니다.

주사제는 생물 제제와의 호환성으로 2024년 미국 약물전달 기기 시장 규모의 42.12%의 점유율을 유지했습니다. 그러나, 침투 촉진제, 마이크로니들 패치, 피부층을 통해 펩티드를 전달하는 폴리머 필름에 의해 국소 시스템은 7.88%로 성장하고 있습니다. 편두통용 점비약과 안과용 재충전 가능한 임플란트의 승인은 바늘 이외의 옵션의 확대를 나타냅니다.

경구 투여 형태는 생체이용률 부스터의 기술 혁신에 뒷받침되며, 저분자 화합물에서는 여전히 선호되고 있습니다. 폐 투여법은 전신 적용으로 확산되고, 경피 GLP-1 패치는 비만의 만연을 표적으로 합니다. 이러한 변화는 양식의 위험을 다양화하고 미국의 약물전달 기기 시장 전반에 걸쳐 성장 벡터를 확장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 높은 환자 부담과 텔레헬스의 보급에 의한 자기 투여 지향 증가

- 고급 비경구 전달 플랫폼이 필요한 생물 제제 파이프라인 확대

- 기술의 진보와 제품 혁신

- 만성질환이 높은 부담

- 첨단 접속형 약물전달 기기의 사용 증가

- CMS의 재택 주입 요법 급부금과 병원 재택 프로그램이 휴대용 주입 펌프 수요를 촉진

- 시장 성장 억제요인

- 조합 제품에 대한 FDA의 엄격한 시판 전 심사에 의한 시장 투입 기간의 연장

- 디지털 컴패니언 용도에 대한 상환의 불투명성

- 침침 상해 소송 증가에 의한 배상 책임 보험료의 상승

- 의료 등급의 실리콘 및 특수 폴리머의 지속적인 부족에 의한 기기 제조 스케줄의 혼란

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 기기 유형별

- 흡입기

- 경피 패치

- 주입 펌프

- 주사기 및 바늘

- 주사 펜

- 자동 주사기

- 바늘 없는 주사기

- 이식형 약물전달 기기

- 기타

- 투여 경로별

- 주사제

- 국소제

- 경구제

- 폐흡입제

- 안과용제

- 비강제

- 기타

- 기술별

- 지속/제어 방출 시스템

- 표적/부위 특이적 전달

- 생분해성/생체흡수성 시스템

- 스마트 및 연결형 약물전달 기기

- 바늘 없는 기술

- 용도별

- 당뇨병

- 암

- 심혈관 질환

- 호흡기 질환

- 중추신경계 장애

- 감염성 질환

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 재택 헬스케어

- 클리닉 및 의사 진료실

- 기타

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Becton, Dickinson and Company

- Solventum

- Johnson & Johnson

- Medtronic plc

- West Pharmaceutical Services, Inc.

- Insulet Corporation

- Baxter International Inc.

- Boston Scientific Corporation

- Terumo Corporation

- Gerresheimer AG

- Ypsomed AG

- Tandem Diabetes Care, Inc.

- Antares Pharma(a Halozyme company)

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd.

- Bayer AG

- Sanofi

- GlaxoSmithKline plc

- Eli Lilly and Company

- Novo Nordisk A/S

- AstraZeneca plc

- Teva Pharmaceutical Industries Ltd.

- AptarGroup, Inc.

- CooperSurgical, Inc.

제7장 시장 기회와 전망

KTH 25.10.27The United States drug delivery devices market is valued at USD 51.24 billion in 2025 and is forecast to reach USD 75.20 billion by 2030, expanding at a 6.71% CAGR.

Growth is grounded in the nation's rising chronic-disease burden, continual product innovation, and a decisive pivot toward patient-centric therapy that favors self-administration and home care.[1]Traditional modalities remain relevant, yet device makers are layering connectivity, sensors, and analytics onto proven platforms to improve adherence and real-world outcomes. Hospitals continue to anchor demand, but reimbursement trends and high deductibles are funneling volume into ambulatory clinics and living rooms, reshaping channel economics. Competitive intensity is sharpening around biologics-ready injectors, smart inhalation systems, and on-body pumps that reduce clinic visits. At the same time, the FDA's Digital Health Advisory Committee is shortening feedback loops for software-driven devices while maintaining a stringent safety bar, creating both opportunity and compliance cost for innovators.

United States Drug Delivery Devices Market Trends and Insights

Rise in Self-Administration Preferences Driven by High Patient Deductibles and Telehealth Adoption

Demand for convenient dosing formats is accelerating as patients shoulder higher out-of-pocket costs. Telehealth visits rose sharply during the pandemic and remain elevated, enabling clinicians to coach users on connected pens, pumps, and inhalers without in-person training. Hospitals, facing USD 115 billion in 2023 drug spend, encourage take-home therapies to trim length-of-stay and pharmacy overhead. The FDA's April 2025 clearance of CT-132, a digital therapeutic for migraine, underscores momentum for software-enhanced regimens that transfer care into the home. Continuous glucose monitoring now starts earlier in diabetes journeys, aligning device selection with individual lifestyle and boosting confidence in self-managed dosing.

Expanding Biologics Pipeline Necessitating Advanced Parenteral Delivery Platforms

Large-molecule therapies represent a growing share of FDA approvals, demanding devices that maintain viscosity control, temperature stability, and precise micro-dosing[1]. Wearable injectors capable of 5-10 mL subcutaneous delivery are entering trials, offering at-home alternatives to infusion centers. Early device strategy is now embedded in molecule design as drug makers weigh formulation viscosity against patient comfort. Contract manufacturers with polymer expertise enjoy a widening moat, especially in Boston-area and Bay-area biotech clusters. Industry attention to biologics-ready systems expanded further after AstraZeneca highlighted lipid nanoparticle and oral biologic platforms in its pipeline update.

Stringent FDA Premarket Review for Combination Products Extending Time-to-Market

Approval cycles for novel drug-device combinations can stretch to 36 months, straining venture-backed developers. Draft user-fee legislation aims to streamline reviews but will introduce new documentation layers in the near term. Firms now integrate regulatory specialists early in concept design, adding cost and prolonging R&D. Larger incumbents with established quality systems widen competitive distance as smaller entrants wrestle with documentation rigor. Any leadership turnover or budget pressure at FDA may influence review cadence and resource allocation.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancement and Product Innovation

- High Burden of Chronic Disease

- Reimbursement Uncertainty for Digital Companion Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inhalers record the fastest 9.13% CAGR, outpacing the broader United States drug delivery devices market yet still trailing Syringes and Needles that hold 30.34% share. This surge stems from propellant redesigns and digital dose-counters that assure correct technique, critical for the 25 million Americans managing asthma. GSK's low-carbon Ventolin prototype positions sustainability as a new differentiator.

Momentum in inhalation technology is steering investment into soft-mist and dry-powder platforms capable of systemic delivery of biologics. Needle-free injectors now attract users with strong aversion to sharps, while auto-injectors and pens leverage spring-loaded mechanics for precise biologic dosing at home. Implantable pumps fill long-term therapy niches such as ophthalmology inserts reviewed by the FDA in February 2025. These diverse modalities enlarge the addressable base and reduce single-technology dependence within the United States drug delivery devices market.

Injectables retained 42.12% share of the United States drug delivery devices market size in 2024 due to compatibility with biologics. Yet topical systems grow at 7.88% thanks to permeation enhancers, microneedle patches, and polymer films that deliver peptides through skin layers. Regulatory nods for migraine nasal sprays and ocular refillable implants demonstrate expanding options beyond needles.

Oral dosage formats remain favored for small molecules, supported by innovations in bioavailability boosters. Pulmonary delivery methods broaden into systemic applications, and transdermal GLP-1 patches target the obesity epidemic. Together these shifts diversify modality risk and spread growth vectors across the United States drug delivery devices market.

The United States Drug Delivery Devices Market Report is Segmented by Device Type (Inhalers, Transdermal Patch, and More), Route of Administration (Injectable, Topical, and More), Technology (Sustained/Controlled Release System, Targeted/Site-Specific Delivery, and More), Application (Diabetes, Cancer and More), and End Users (Hospitals, Ascs, and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beckton Dickinson

- Solventum

- Johnson & Johnson

- Medtronic

- West Pharmaceutical Services

- Insulet

- Baxter

- Boston Scientific

- Terumo

- Gerresheimer

- Ypsomed

- Tandem Diabetes Care

- Antares Pharma (a Halozyme company)

- Pfizer

- Roche

- Bayer

- Sanofi

- GlaxoSmithKline

- Eli Lilly and Company

- Novo Nordisk

- AstraZeneca

- Teva Pharmaceutical Industries

- AptarGroup, Inc.

- The Cooper Companies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Self-Administration Preferences Driven by High Patient Deductibles and Telehealth Adoption

- 4.2.2 Expanding Biologics Pipeline Necessitating Advanced Parenteral Delivery Platforms

- 4.2.3 Technological Advancement and Product Innovation

- 4.2.4 High Burden of Chronic Disease

- 4.2.5 Increased Use of Advanced and Connected Drug Delivery Devices

- 4.2.6 CMS Home-Infusion Therapy Benefit and Hospital-at-Home Programs Fueling Demand for Portable Infusion Pumps

- 4.3 Market Restraints

- 4.3.1 Stringent FDA Premarket Review for Combination Products Extending Time-to-Market

- 4.3.2 Reimbursement Uncertainty for Digital Companion Applications

- 4.3.3 Rising Needlestick Injury Litigation Elevating Liability Insurance Premiums

- 4.3.4 Persistent Shortages of Medical-Grade Silicone and Specialty Polymers Disrupting Device Manufacturing Schedules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Inhalers

- 5.1.2 Transdermal Patches

- 5.1.3 Infusion Pumps

- 5.1.4 Syringes & Needles

- 5.1.5 Injection Pens

- 5.1.6 Auto-Injectors

- 5.1.7 Needle-Free Injectors

- 5.1.8 Implantable Drug Delivery Devices

- 5.1.9 Others

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Topical

- 5.2.3 Oral

- 5.2.4 Pulmonary

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.2.7 Others

- 5.3 By Technology

- 5.3.1 Sustained / Controlled Release Systems

- 5.3.2 Targeted / Site-Specific Delivery

- 5.3.3 Biodegradable / Bioresorbable Systems

- 5.3.4 Smart & Connected Drug Delivery Devices

- 5.3.5 Needle-less Technologies

- 5.4 By Application

- 5.4.1 Diabetes

- 5.4.2 Cancer

- 5.4.3 Cardiovascular Diseases

- 5.4.4 Respiratory Diseases

- 5.4.5 Central Nervous System Disorders

- 5.4.6 Infectious Diseases

- 5.4.7 Others

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers (ASCs)

- 5.5.3 Home Healthcare Settings

- 5.5.4 Clinics and Physician Offices

- 5.5.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Becton, Dickinson and Company

- 6.4.2 Solventum

- 6.4.3 Johnson & Johnson

- 6.4.4 Medtronic plc

- 6.4.5 West Pharmaceutical Services, Inc.

- 6.4.6 Insulet Corporation

- 6.4.7 Baxter International Inc.

- 6.4.8 Boston Scientific Corporation

- 6.4.9 Terumo Corporation

- 6.4.10 Gerresheimer AG

- 6.4.11 Ypsomed AG

- 6.4.12 Tandem Diabetes Care, Inc.

- 6.4.13 Antares Pharma (a Halozyme company)

- 6.4.14 Pfizer Inc.

- 6.4.15 F. Hoffmann-La Roche Ltd.

- 6.4.16 Bayer AG

- 6.4.17 Sanofi

- 6.4.18 GlaxoSmithKline plc

- 6.4.19 Eli Lilly and Company

- 6.4.20 Novo Nordisk A/S

- 6.4.21 AstraZeneca plc

- 6.4.22 Teva Pharmaceutical Industries Ltd.

- 6.4.23 AptarGroup, Inc.

- 6.4.24 CooperSurgical, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment