|

시장보고서

상품코드

1836458

정맥 조명기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Vein Illuminator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

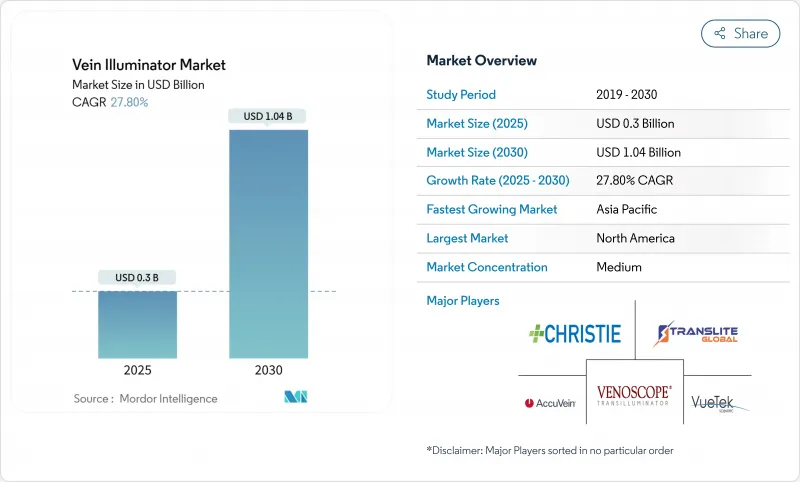

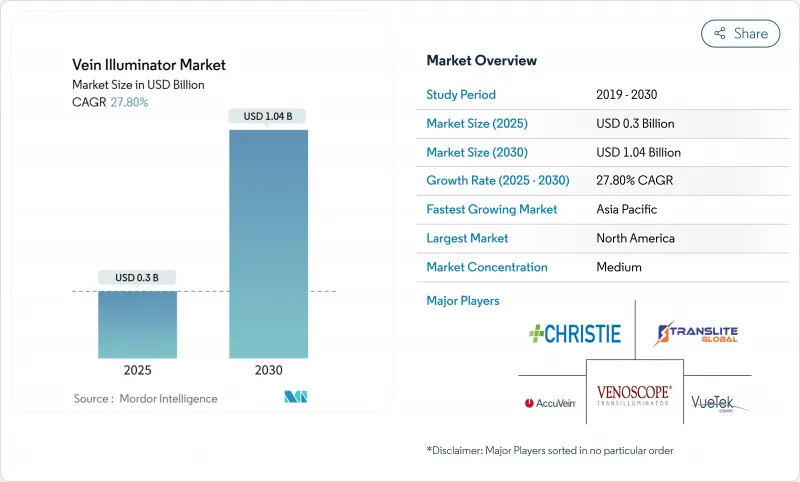

정맥 조명기 시장 규모는 2025년에 3억 달러에 달하고, 예측 기간(2025-2030년)의 CAGR은 27.80%를 나타낼 전망이며, 2030년에는 10억 4,000만 달러에 달할 것으로 예상됩니다.

견고한 성장은 의료 시스템이 초기 정맥 천자의 성공에 중점을 두고 있음을 반영합니다. 수요는 전통적인 정맥촉진의 신뢰성을 저하시키는 고령화와 비만화에 의해 증폭되며, 만성질환 모니터링 증가에 의해 보다 빈번한 채혈이 필요합니다. 근적외선(NIR) 이미징 기술의 향상, 부품 비용 저하, 휴대형 폼 팩터가 더욱 채용을 가속화합니다. 아시아태평양의 의료기기 제조 현지화 추진과 중국의 병원 현대화로 인해 미래 수익은 비용 최적화 시스템에 기울어지고 있습니다. 현지 기업이 저가의 NIR 장비를 도입해 기존 브랜드를 밑돌면서 프리미엄 모델은 AI 지침과 멀티모달 이미징을 탑재하고 있어 경쟁 압력이 강해지고 있습니다.

세계의 정맥 조명기 시장 동향과 인사이트

퍼 스토어 템프 성공률 상승으로 품질 지표 견인

소아과 병동에서의 임상시험에서는 촉진에 의한 40.7%에 비해 AccuVein AV400에서는 퍼스트 스틱의 성공률이 74.1%로 상승하여 치료시간이 169초에서 44초로 단축되었습니다. 의료 시스템의 임원은 이러한 이익을 HCAHPS 환자 경험 점수 상승에 직접 반영하고 메디케어 환불을 결정하고 장비 구매를 전략적 우선순위로 끌어올리고 있습니다. 환자 조사는 응답자의 93%가 직원이 시각화 도구를 사용하는 병원을 더 높게 평가하고 있음을 보여줍니다.

만성 질환의 채혈 증가

당뇨병 환자와 심혈관 질환 환자 사이에서는 HbA1c, 지질, 신장 검사 빈도가 높아지고 정맥 천자의 연간 양이 증가하고 사혈 능력에 부담이 걸리고 있습니다. 혈관 노화 및 약물로 인한 정맥 취약성이 실패의 위험을 증가시키고 있기 때문에 시설은 휴대용 NIR 뷰파인더를 실험실에 장착하여 반복적으로 천자와 소모품 낭비를 줄입니다.

높은 자본 비용과 1대당 장비 비용

프리미엄 NIR 시스템의 가격은 4,000달러에서 27,000달러로 소규모 병원 예산을 압박하고 있습니다. 재활용 광학 부품으로 만들어진 오픈소스 실험 모델은 미화 25달러에서 동등한 정맥 대비를 입증하고 향후 가격 하락을 시사합니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 고령화와 비만 인구가 종래의 방법에 과제

- 환자 체험 KPI를 요구하는 병원의 움직임

- 보험 상환 코드 부족

부문 분석

근적외선 조사는 2024년에 50.3%의 수익을 제어하고 성숙하고 비용 효율적인 플랫폼에서 정맥 조명기 시장을 지원했습니다. 2030년까지 연평균 복합 성장률(CAGR) 31.8%를 나타내는 초음파 강화 유닛은 보다 깊은 이미징과 기존 초음파 카트와의 시너지 효과로 어려운 액세스 환자에서 점유율을 획득합니다. 다중 스펙트럼 하이브리드가 조사를 견인하는 반면, 투과 조명은 더 부드러운 빛 때문에 여전히 소아과의 틈새 분야입니다. 듀얼 모드 VeinCAP 시스템과 같은 특허 출원은 NIR과 확산 하이퍼 스펙트럼 뷰를 제공하는 단일 장치로의 수렴 동향을 보여줍니다. 기능 세트가 확대됨에 따라 공급업체는 정맥의 질을 자동 평가하고 성공 지표를 전자 의료 기록에 기록하는 AI 알고리즘으로 차별화를 도모하고 있습니다.

핸드헬드 및 휴대용 기기는 2024년 매출의 61.2%를 차지했습니다. 웨어러블 및 클립 온 모듈은 CAGR 34.1%를 나타내 상승하고 복잡한 교정 중에 임상의의 손을 자유롭게 하고 교육용으로 스마트 글라스에 비디오를 보냅니다. 탁상형 카트는 혈액은행에 뿌리 깊게 남아 있으며, 탑재된 카메라는 장시간의 채혈에서도 교정된 상태를 유지합니다. IoT 연결은 설계 우선순위를 재정의합니다. 차세대 웨어러블은 Wi-Fi와 고속 스틱 비율을 벤치마킹하는 클라우드 대시보드를 통합하여 기본 조명을 품질 관리 노드로 전환합니다.

정맥 조명기 시장은 기술별(근적외(NIR) 조명, 투과 조명, 기타), 제품 유형별(핸드헬드 휴대용, 탁상용 카트 마운트, 웨어러블·클립온 모듈), 용도별(정맥내 액세스, 채혈·천자 보조, 기타), 최종 사용자별(병원 및 진료소, 헌혈 캠프·혈액 은행, 기타), 지역별

지역 분석

북미는 세련된 인프라와 환자 체험의 성과에 대해 보상을 지불하는 상환 프로그램을 배경으로 2024년 매출에서 37.2%의 주도권을 유지했습니다. 미국 병원에서는 퍼스트 스틱 통계를 품질 대시보드에 통합하여 재주문을 보장합니다. 캐나다의 단일 지불 제도는 단가를 낮추는 주 전체 계약을 선호하며 멕시코의 민간 의료 관광 클리닉은 환자의 편안함 차별화 요인으로 파인더를 도입했습니다.

독일 대학 병원은 멀티 모달 유닛을 시험적으로 도입하고 영국 NHS는 혈관 접근의 안전 목표를 지원하기 위해 대량 가격 협상을 실시합니다. CE 마크의 조화는 국경을 넘은 판매를 원활하게 해, 스칸디나비아나 동유럽으로부터의 신규 참가를 촉구하고 있습니다.

아시아태평양의 정맥 조명기 시장 규모는 CAGR 33.2%를 나타내 세계적인 성장 엔진이 되고 있습니다. 인도의 Production-Linked Incentive(생산 연동 인센티브) 제도는 국내 장비 공장에 보조금을 지급하고 수입에 대한 의존도를 낮추고 있습니다. 중국 병원 업그레이드 프로그램은 간호 효율을 높이는 장비가 필요합니다. 현지 브랜드는 가시화를 점적 키트와 번들로 수입품을 밑돌게 됩니다. 일본의 초고령화 인구와 높은 기기 수준은 고급 듀얼 모드 시스템을 지지하고 한국의 신흥 기업은 재택 주입 서비스용 AI 대응 스마트폰 어댑터를 테스트하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정맥주사와 사혈의 첫회 성공률 상승

- 만성 질환 관련 채혈 증가

- 정맥 접근이 곤란한 고령화 및 비만 인구

- 병원에 의한 환자 체험 KPI의 추진

- AI를 통합한 모바일 정맥 파인더 앱

- 미용 주사에의 채용

- 시장 성장 억제요인

- 높은 자본 비용과 장비 단가

- 상환 코드의 부족

- 낮은 자원 환경에서의 훈련 격차

- 미용전용기기에 대한 규제의 모호함

- 업계 밸류체인 분석

- 규제 상황

- 기술적 전망

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측(금액)

- 기술별

- 근적외선(NIR) 조명

- 투과 조명

- 초음파 증강

- 다중 스펙트럼/하이브리드

- 기타

- 제품 유형별

- 휴대형 및 휴대용

- 탁상형/카트 장착형

- 웨어러블 및 클립온 모듈

- 용도별

- 정맥 내(IV) 접근

- 채혈/정맥 천자 보조

- 경화 요법 및 정맥류 치료

- 응급 및 중환자 치료

- 미용/미적 주사

- 최종 사용자별

- 병원 및 진료소

- 헌혈캠프 및 혈액은행

- 외래수술센터(ASC)

- 재활 및 요양 시설

- 학술 및 연구 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 싱가포르

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AccuVein Inc.

- Christie Medical Holdings Inc.

- TransLite LLC(Veinlite)

- VueTek Scientific LLC

- Venoscope LLC

- Near Infrared Imaging Inc.

- ZD Medical Inc.

- VeinSight(Surmount Electronic)

- Shenzhen Vivolight Medical Device and Technology Co.

- Veincas Medical Ltd.

- SIFSOF LLC

- NextVein LLC

- Infinium Medical Inc.

- B. Braun Medical Inc.

- Koninklijke Philips NV

- Siemens Healthineers AG

- Baxter International Inc.

- GE Healthcare Technologies Inc.

- Osang Healthcare Co., Ltd.

- Kingmaker Biomedical Inc.

- Dhanika Instrument Co.

- Zhongke Micro-Light Medical Equipment Co.

- YSENMED Medical Equipment Co.

- Xavant Medical(Pty) Ltd.

- ALEH Medical Laser and Systems

- FY Medical Devices Co.

제7장 시장 기회와 앞으로의 동향

KTH 25.10.27The Vein Illuminator Market size is estimated at USD 0.3 billion in 2025, and is expected to reach USD 1.04 billion by 2030, at a CAGR of 27.80% during the forecast period (2025-2030).

Robust growth reflects health systems' focus on first-attempt venipuncture success, an outcome now tied to U.S. Medicare's value-based purchasing scores. Demand is amplified by aging and obese populations that make traditional vein palpation unreliable, while rising chronic-disease monitoring requires more frequent blood draws. Technology improvements in near-infrared (NIR) imaging, falling component costs, and portable form factors further accelerate adoption. Asia-Pacific's push to localize medical-device manufacturing and China's hospital modernization are tilting future revenue toward cost-optimized systems. Competitive pressure is intensifying as local firms introduce low-price NIR devices that undercut established brands while premium models layer on AI guidance and multi-modal imaging.

Global Vein Illuminator Market Trends and Insights

Rising First-Attempt Success Rates Drive Quality Metrics

Clinical trials in pediatric units showed first-stick success climbing to 74.1% with AccuVein AV400 compared with 40.7% using palpation, trimming procedure time from 169 seconds to 44 seconds. Health-system executives translate these gains directly into higher HCAHPS patient-experience scores, which shape Medicare reimbursements, elevating device purchases to strategic priorities. Patient surveys reveal 93% of respondents rate hospitals higher when staff employ visualization tools.

Growth in Chronic-Disease Blood Draws

More frequent HbA1c, lipid, and renal tests among diabetic and cardiovascular cohorts raise annual venipuncture volumes, stressing phlebotomy capacity. Aging vasculature and drug-induced vein fragility heighten failure risk, prompting facilities to equip labs with portable NIR finders that cut repeat sticks and consumable waste.

High Capital and Per-Unit Device Costs

Premium NIR systems list between USD 4,000 and USD 27,000, squeezing budgets of small hospitals. Experimental open-source models built from recycled optics have demonstrated comparable vein contrast for USD 25, hinting at future price erosion.

Other drivers and restraints analyzed in the detailed report include:

- Ageing and Obese Populations Challenge Traditional Methods

- Hospital Push for Patient-Experience KPIs

- Lack of Reimbursement Codes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Near-Infrared Illumination controlled 50.3% revenue in 2024, underpinning the vein illuminator market with a mature, cost-efficient platform. Ultrasound-Augmented units, posting 31.8% CAGR to 2030, carve share in difficult-access patients via deeper imaging and synergy with existing ultrasound carts. Transillumination remains a pediatric niche due to softer light, while multispectral hybrids gain research traction. Patent filings such as the dual-mode VeinCAP system illustrate convergence trends toward single devices offering NIR plus diffuse hyperspectral views. As feature sets widen, vendors differentiate on AI algorithms that auto-grade vein quality and log success metrics to electronic health records.

Hand-held and Portable devices occupied 61.2% of 2024 revenue because nurses favor pocketable tools that shift easily between wards. Wearable and Clip-On Modules, climbing at 34.1% CAGR, free clinicians' hands during complex cannulations, and feed video to smart glasses for teaching. Table-top carts persist in blood banks where mounted cameras stay calibrated for long draws. IoT connectivity is redefining design priorities: next-generation wearables integrate Wi-Fi and cloud dashboards that benchmark first-stick rates, transforming basic lights into quality-management nodes.

Vein Illuminator Market is Segmented by Technology (Near-Infrared (NIR) Illumination, Transillumination, and More), Product Type (Hand-Held and Portable, Table-Top/Cart-Mounted, and Wearable and Clip-On Modules), Application (Intravenous (IV) Access, Blood Draw/Venipuncture Assistance, and More), End-User (Hospitals and Clinics, Blood Donation Camps and Blood Banks, and More), and Geography.

Geography Analysis

North America retained 37.2% 2024 revenue leadership on the back of sophisticated infrastructure and reimbursement programs that pay for patient-experience outcomes. U.S. hospitals embed first-stick statistics into quality dashboards, ensuring repeat device orders. Canada's single-payer system favors province-wide contracts that lower per-unit costs, while Mexico's private medical-tourism clinics install finders as patient-comfort differentiators.

Europe's multi-payer environment produces steady uptake; Germany's university hospitals pilot multi-modal units, and the United Kingdom's NHS negotiates bulk pricing to support vascular-access safety goals. CE Mark harmonization smooths cross-border sales and encourages newer entrants from Scandinavia and Eastern Europe.

The vein illuminator market size in Asia-Pacific is expanding at a 33.2% CAGR, making it the global growth engine. India's Production-Linked Incentive scheme subsidizes domestic device plants, reducing import reliance. China's hospital-upgrade program requires equipment that boosts nursing efficiency; local brands undercut imports by bundling visualization with IV kits. Japan's super-aged population and high device standards favor premium dual-mode systems, while South Korea's start-ups test AI-enabled smartphone adapters for home infusion services.

- AccuVein Inc.

- Christie Medical Holdings Inc.

- TransLite LLC (Veinlite)

- VueTek Scientific LLC

- Venoscope LLC

- Near Infrared Imaging Inc.

- ZD Medical Inc.

- VeinSight (Surmount Electronic)

- Shenzhen Vivolight Medical Device and Technology Co.

- Veincas Medical Ltd.

- SIFSOF LLC

- NextVein LLC

- Infinium Medical Inc.

- B. Braun Medical Inc.

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- Baxter International Inc.

- GE Healthcare Technologies Inc.

- Osang Healthcare Co., Ltd.

- Kingmaker Biomedical Inc.

- Dhanika Instrument Co.

- Zhongke Micro-Light Medical Equipment Co.

- YSENMED Medical Equipment Co.

- Xavant Medical (Pty) Ltd.

- ALEH Medical Laser and Systems

- FY Medical Devices Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising first-attempt success rates for IV and phlebotomy

- 4.2.2 Growth in chronic-disease related blood draws

- 4.2.3 Ageing and obese populations with difficult venous access

- 4.2.4 Hospital push for patient-experience KPIs

- 4.2.5 AI-integrated mobile vein-finder apps

- 4.2.6 Adoption in cosmetic/aesthetic injections

- 4.3 Market Restraints

- 4.3.1 High capital and per-unit device costs

- 4.3.2 Lack of reimbursement codes

- 4.3.3 Training gaps in low-resource settings

- 4.3.4 Regulatory ambiguity for aesthetic-only devices

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 Near-Infrared (NIR) Illumination

- 5.1.2 Transillumination

- 5.1.3 Ultrasound-Augmented

- 5.1.4 Multispectral/Hybrid

- 5.1.5 Others

- 5.2 By Product Type

- 5.2.1 Hand-held and Portable

- 5.2.2 Table-Top/Cart-Mounted

- 5.2.3 Wearable and Clip-On Modules

- 5.3 By Application

- 5.3.1 Intravenous (IV) Access

- 5.3.2 Blood Draw/Venipuncture Assistance

- 5.3.3 Sclerotherapy and Varicose Vein Treatment

- 5.3.4 Emergency and Critical Care

- 5.3.5 Cosmetic/Aesthetic Injections

- 5.4 By End-user

- 5.4.1 Hospitals and Clinics

- 5.4.2 Blood Donation Camps and Blood Banks

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Rehabilitation and Nursing Homes

- 5.4.5 Academic and Research Institutions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Malaysia

- 5.5.4.6 Singapore

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AccuVein Inc.

- 6.4.2 Christie Medical Holdings Inc.

- 6.4.3 TransLite LLC (Veinlite)

- 6.4.4 VueTek Scientific LLC

- 6.4.5 Venoscope LLC

- 6.4.6 Near Infrared Imaging Inc.

- 6.4.7 ZD Medical Inc.

- 6.4.8 VeinSight (Surmount Electronic)

- 6.4.9 Shenzhen Vivolight Medical Device and Technology Co.

- 6.4.10 Veincas Medical Ltd.

- 6.4.11 SIFSOF LLC

- 6.4.12 NextVein LLC

- 6.4.13 Infinium Medical Inc.

- 6.4.14 B. Braun Medical Inc.

- 6.4.15 Koninklijke Philips N.V.

- 6.4.16 Siemens Healthineers AG

- 6.4.17 Baxter International Inc.

- 6.4.18 GE Healthcare Technologies Inc.

- 6.4.19 Osang Healthcare Co., Ltd.

- 6.4.20 Kingmaker Biomedical Inc.

- 6.4.21 Dhanika Instrument Co.

- 6.4.22 Zhongke Micro-Light Medical Equipment Co.

- 6.4.23 YSENMED Medical Equipment Co.

- 6.4.24 Xavant Medical (Pty) Ltd.

- 6.4.25 ALEH Medical Laser and Systems

- 6.4.26 FY Medical Devices Co.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment