|

시장보고서

상품코드

1836466

총성 탐지 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Gunshot Detection Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

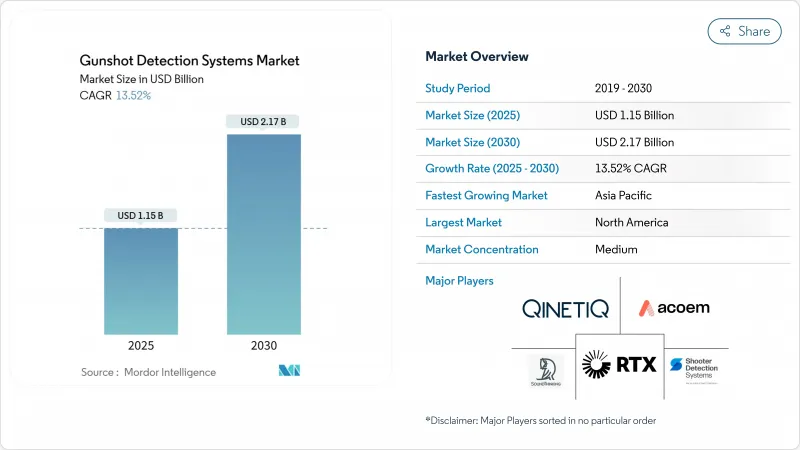

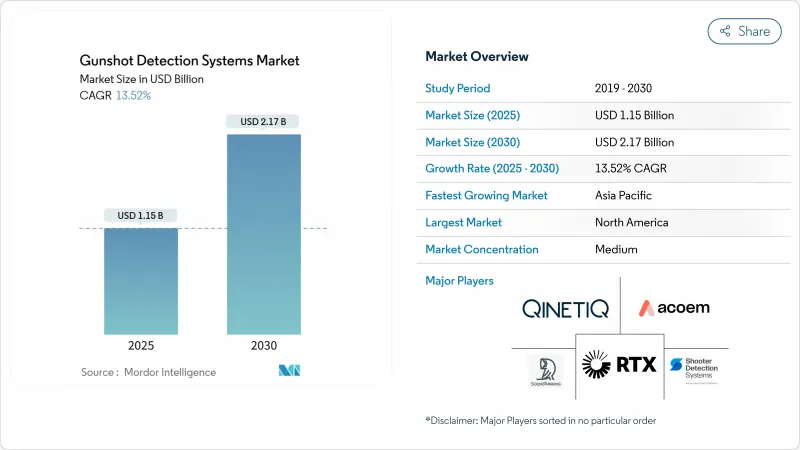

총성 탐지 시스템 시장은 2025년에 11억 5,000만 달러로 평가되고, 2030년에는 21억 7,000만 달러로 확대될 것으로 예측되며, CAGR은 13.52%를 나타낼 전망입니다

보급의 배경은 도시 지역에서 총 난사 사건 증가, 공공 부문의 안정적인 자금 조달, 오경보를 줄이는 이중 센서 플랫폼의 입증된 능력을 포함합니다. 공급자는 하드웨어 판매에서 구독 서비스로 축족을 옮기고 지자체는 상당한 자본 지출 없이 지속적인 업그레이드를 이용할 수 있게 되었습니다. 비디오 분석, 자율적인 무인 항공기 및 실시간 범죄 센터 플랫폼과의 기술 융합은 시장의 대응 가능한 범위를 교육, 중요 인프라 및 전장 인식으로 확장합니다. 북미는 광역 도시로의 전개와 강력한 보조금 파이프라인으로 선도하고, 아시아태평양은 스마트 시티에의 지출과 국내 센서의 혁신을 배경으로 가속하고 있습니다.

세계의 총성 탐지 시스템 시장 동향과 인사이트

대도시에서 총과 관련된 폭력 격화

총 난사 사건이 다발하고 있는 도시는 제1선의 인프라로서 감지 네트워크를 채용하고 있습니다. 미국에서는 2024년 총기로 인한 사망자 4만 886명, 부상자 3만 1,652명을 기록해 5,570억 달러의 경제적 부담이 발생했습니다. 샌프란시스코에서는 총 목소리의 15%만 911을 통해 보고되었으나, 음성 센서가 나머지를 포착하여 1분 이내에 지리적으로 식별된 경고를 파견 대원에게 제공했습니다. 독립적인 임상조사에서도 총창 피해자의 반송시간이 배치 후 4분에서 2분으로 단축되어 생존확률이 향상된 것으로 나타났습니다. 이 혜택은 제곱 마일의 커버 범위를 추가하는 자금 조달 사례를 강화합니다.

확대하는 연방정부와 지자체의 안전기술 보조금

전용 보조금 프로그램은 중규모 관할 구역의 도입 장벽을 낮추고 있습니다. 미국의 일부 주에서는 유치원에서 고등학교까지의 시설에서 AI를 이용한 총을 감지하는 데 보조금을 내고 있습니다. 국가적 기술 평가는 개방형 API와 CAD 통합을 통한 솔루션의 중요성을 강조하고 상호 운용 가능한 공급업체에게 상을 추가로 유도하고 있습니다.

도입 비용의 높이가 보급의 과제

전통적인 네트워크는 매년 1평방 마일당 6만 5,000-9만 5,000달러의 비용이 들기 때문에 대도시를 제외한 전개에는 한계가 있습니다. 반면 ATD-300과 같은 에지 프로세싱 유닛은 서버 부하 및 센서 수를 줄이고 총 소유 비용을 낮춥니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 음향 센서와 적외선 센서의 융합에 의한 정밀도 향상

- 병사의 상황 인식 키트의 근대화

- 증거의 신뢰성과 오경보 우려

부문 분석

옥외 배치는 2024년 수익의 60.26%를 차지했고, 도시 지역에서 포격 인텔리전스의 주요 층으로서의 지위를 굳혔습니다. 광역 메쉬 어레이는 골목, 공원, 간선 도로에 걸친 충격파를 삼각 측량하여 도시 데이터 세트에서 검출된 85%의 보고 갭을 채웁니다. 경보를 감시 카메라에 링크시킴으로써 공동으로 오디오 비주얼에 의한 검증이 가능하게 되고, 순찰대는 60초 이내에 실용적인 증거를 얻을 수 있습니다. 이 통합은 통합된 명령 플랫폼에 이기종 센서를 중첩하는 더 광범위한 스마트 시티 지침을 지원합니다.

실내 솔루션은 교육위원회, 경기장, 기업 캠퍼스에서 증가하는 액티브 슈터 사건에 대응하기 위해 CAGR 11.48%를 나타내 가속화되고 있습니다. 가디언과 같은 음향 및 적외선 듀얼 디바이스는 에코가 많은 복도에서도 99.9%의 현장 정밀도를 달성합니다. 실험실에서 교정된 마이크를 사용한 학교 복도에서의 시험적 연구에서는 분류 정밀도가 99.99%까지 향상되어 폐쇄 공간 성능의 새로운 벤치마크가 되었습니다. 빌딩 자동화 시스템과 경보를 결합하면 잠금 및 대량 알림 채널이 작동하여 초동 대응 이외의 가치도 확대됩니다.

고정설비는 고밀도 지역에 적합하기 때문에 2024년 총성 탐지 시스템 시장 규모의 52.75%를 차지했습니다. 도시 기관은 지속적인 모니터링과 기존의 섬유 백본과의 통합을 높이 평가합니다. 경찰의 감사 데이터에 따르면, 옥외에서 발생한 총소리 중 긴급 회선에 도달한 것은 불과 15%이며, 사일런트 인시던트를 포착하는 고정 노드의 중요성이 부각되고 있습니다.

병사 탑재형 및 휴대형은 국방군이 컴팩트한 상황 인식 기어를 우선하기 때문에 CAGR 15.69%를 나타낼 것으로 예측되고 있습니다. 무게 230g 이하의 어깨걸이형 센서 팩은 무선 헤드셋과 통신하여 시가지 작전에서의 생존성을 향상시킵니다. 차량 탑재형 어레이는 순찰차 및 장갑 운송 차량으로 이동 중 감지를 제공하며 경로 조정을 위해 파견 콘솔에 자동으로 공급됩니다.

총성 탐지 시스템 시장 보고서는 용도(실내 및 실외), 설치(고정, 차량 등), 솔루션(시스템 및 구독 기반 총성 감지 서비스(SaaS)), 최종 사용자(방위 및 군사, 법 집행 기관, 상업 및 중요 인프라 등), 지역(북미, 유럽 및 기타)으로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 40.78%로 최대 점유율을 획득했습니다. 지속적인 총기 사건과 사법 지원 보조금 등 연방 정부 프로그램은 총성 탐지 시스템 시장 확대를 위한 지속적인 지출을 지원하고 있습니다. 뉴욕, 시카고, 샌프란시스코의 실시간 범죄 센터와의 통합은 운영의 성숙을 보여주는 반면, 자선 활동의 자금 흐름은 충분한 서비스를받지 못한 지역으로의 적용을 확대합니다.

유럽은 전개 설계를 형성하는 강력한 프라이버시 보호 프레임 워크가 특징입니다. 공급업체는 데이터 최소화 규칙 및 보존 기간 제한에 대응해야 하며 지속적인 기록보다 에지 처리에 의한 경고를 선호합니다. 영국, 프랑스, 네덜란드의 대도시 경찰은 교통의 요소와 관광지 보호에 중점을 둡니다.

아시아태평양은 중국, 인도, 동남아시아에서 스마트 시티 프로그램이 전개됨에 따라 지역별 CAGR이 9.49%를 나타내 가장 빨라질 것으로 예측되고 있습니다. 국내 센서 제조업체는 정부의 우대 조치의 혜택을 받고 있으며, 도시화의 진전에 의해 확장 가능한 경계 보안 수요가 높아지고 있습니다. 이 지역의 국방부는 미국 및 유럽 전장에서의 경험을 참고로 병사에 장착하는 유형의 것도 시험적으로 도입하고 있습니다.

남미에서는 일부 수도에서 높은 살인 발생률에 직면하고 있으며, 예산이 제한되어 있음에도 불구하고 지자체에 의한 시험 도입이 진행되고 있습니다. 고액의 초기 비용을 회피할 수 있는 정액제 플랜이 인기를 모으고 있습니다. 중동 및 아프리카의 일부는 주로 중요한 에너지 인프라와 대규모 이벤트를 보호하기 위해이 기술을 채택하고 있으며, 종종 신속한 차단을 위해 총성 감지와 무인 감시를 결합합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 대도시의 총과 관련된 폭력의 격화

- 연방 정부 및 지자체의 안전 기술 보조금 증가

- 음향 센서와 적외선 센서의 융합에 의한 정밀도 향상

- 병사의 상황 인식 키트의 근대화

- 보호된 장소의 보험료 할인

- API 대응 피드에 대한 실시간 범죄 센터 수요

- 시장 성장 억제요인

- 멀티노드 전개를 위한 고액의 설비투자와 OPEX

- 증거로서의 신뢰성과 오경고의 우려

- 프라이버시·민사 소송 리스크

- 멀티 센서 드론 플랫폼으로의 예산 이동

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액)

- 용도별

- 실내

- 실외

- 설치별

- 고정형

- 차량 탑재형

- 휴대용/병사 휴대형

- 솔루션별

- 시스템

- 구독형 총성 감지 서비스(SaaS)

- 최종 사용자별

- 국방 및 군사

- 법 집행 기관

- 상업 및 중요 인프라

- 캠퍼스 및 교육 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SoundThinking, Inc.

- Raytheon BBN(RTX Corporation)

- Thales Group

- QinetiQ Group plc

- ASELSAN AS

- ACOEM Group

- Databuoy Corporation

- Microflown AVISA

- Israel Aerospace Industries Ltd.

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- Shooter Detection Systems LLC

- Safety Dynamics, Inc.

- EAGL Technology, Inc.

- Louroe Electronics, Inc.

- Pelco(Motorola Solutions, Inc.)

- AmberBox, Inc.

- Nextivity, Inc.

- Knightscope, Inc

- Omnilert LLC

제7장 시장 기회와 전망

KTH 25.10.27The gunshot detection system market is valued at USD 1.15 billion in 2025 and is forecasted to advance to USD 2.17 billion by 2030, representing a 13.52% CAGR.

Uptake stems from rising urban gun violence, steady public-sector funding, and the proven ability of dual-sensor platforms to cut false alerts. Providers have pivoted from hardware sales to subscription services, giving municipalities access to continuous upgrades without large capital outlays. Technology convergence with video analytics, autonomous drones, and real-time crime-center platforms expands the market's addressable footprint into education, critical infrastructure, and battlefield awareness. North America leads with wide-area city deployments and strong grant pipelines, while Asia-Pacific is accelerating on the back of smart-city spending and domestic sensor innovation.

Global Gunshot Detection Systems Market Trends and Insights

Escalating gun-related violence in major cities

Cities experiencing higher firearm incidents are adopting detection networks as first-line infrastructure. The US recorded 40,886 gun-violence deaths and 31,652 injuries in 2024, creating a USD 557 billion economic burden. Only 15% of gunfire was reported through 911 in San Francisco, but audio sensors captured the remainder, supplying dispatchers with geolocated alerts in under a minute.Independent clinical research also showed transport times for gunshot victims falling from 4 minutes to 2 minutes after deployment, improving survival odds. These benefits strengthen the funding case for additional square-mile coverage.

Growing federal and municipal safety-tech grants

Dedicated grant programs are lowering adoption barriers for mid-sized jurisdictions. Several US states have ring-fenced awards for AI-enabled gun detection in K-12 facilities, alongside city-level allocations that cover subscription fees. A national technology assessment underscored the importance of solutions with open APIs and CAD integration, further steering awards toward interoperable vendors.

High deployment costs challenge widespread adoption

Traditional networks cost USD 65,000-95,000 per square mile each year, limiting roll-out beyond large cities. Subscription models that convert capital to operating expense are gaining traction, while edge-processing units such as the ATD-300 cut server loads and sensor counts, lowering total cost of ownership.

Other drivers and restraints analyzed in the detailed report include:

- Accuracy gains from acoustic and IR sensor fusion

- Modernization of soldier situational-awareness kits

- Evidentiary reliability and false-alert concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Outdoor deployments accounted for 60.26% of 2024 revenue, cementing their status as the primary layer of urban gunfire intelligence. Wide-area mesh arrays triangulate shock waves across alleys, parks, and arterial roads, filling the 85% reporting gap detected in city data sets. Linking alerts to surveillance cameras enables joint audio-visual verification, giving patrols actionable evidence within 60 seconds. This integration supports the broader smart-city mandate to overlay disparate sensors on a unified command platform.

Indoor solutions are accelerating at a 11.48% CAGR as education boards, arenas, and corporate campuses respond to rising active-shooter incidents. Dual acoustic-infrared devices such as Guardian achieve 99.9% in-situ accuracy, even in echo-rich hallways. Pilot studies in school corridors using laboratory-calibrated microphones further improved classification to 99.99% accuracy, setting a new benchmark for enclosed-space performance. Combining alerts with building-automation systems triggers lockdowns and mass-notification channels, extending value beyond first response.

Fixed installations represented 52.75% of the gunshot detection system market size in 2024 due to their suitability for high-density neighborhoods. City agencies value their continuous monitoring and integration with existing fibre backbones. Data from police audits showed only 15% of outdoor gunfire reached emergency lines, highlighting the importance of fixed nodes in capturing silent incidents.

Soldier-mounted and portable formats are projected to log a 15.69% CAGR as defence forces prioritise compact situational-awareness gear. Shoulder-worn sensor packs weighing under 230 grams communicate with radio headsets, improving survivability during urban operations. Vehicle-mounted arrays round out the category, giving patrol cars and armored transports on-the-move detection that feeds automatically into dispatch consoles for route adjustment.

The Gunshot Detection Systems Market Report is Segmented by Application (Indoor and Outdoor), Installation (Fixed, Vehicle, and More), Solution (Systems and Subscription-Based Gunshot Detection Services (SaaS)), End User (Defense and Military, Law Enforcement Agencies, Commercial and Critical Infrastructure, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated the largest share at 40.78% in 2024. Persistent firearm incidents, combined with federal programmes such as the Justice Assistance Grant, underpin continuous spending on the gunshot detection system market expansion. Integration with real-time crime centers in New York, Chicago, and San Francisco demonstrates operational maturity, while philanthropic funding streams expand coverage into underserved neighborhoods.

Europe is characterised by strong privacy frameworks that shape deployment design. Vendors must accommodate data-minimisation rules and limited retention periods, favouring edge-processed alerts rather than continuous recording. Uptake among metropolitan police services in the United Kingdom, France, and the Netherlands focuses on protecting transit hubs and tourist districts.

Asia-Pacific is projected to post the fastest regional CAGR of 9.49% as smart-city programs roll out in China, India, and Southeast Asia. Domestic sensor makers benefit from government incentives, and rising urbanisation heightens demand for scalable perimeter security. Defence ministries in the region are also trialling soldier-mounted variants, borrowing from the US and European battlefield experience.

South America faces high homicide rates in several capitals, which is driving municipal pilots despite constrained budgets. Subscription plans that bypass heavy upfront costs are gaining traction. The Middle East and parts of Africa adopt the technology mainly to safeguard critical energy infrastructure and large-scale events, often bundling gunshot detection with drone surveillance for rapid interdiction.

- SoundThinking, Inc.

- Raytheon BBN (RTX Corporation)

- Thales Group

- QinetiQ Group plc

- ASELSAN A.S.

- ACOEM Group

- Databuoy Corporation

- Microflown AVISA

- Israel Aerospace Industries Ltd.

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- Shooter Detection Systems LLC

- Safety Dynamics, Inc.

- EAGL Technology, Inc.

- Louroe Electronics, Inc.

- Pelco (Motorola Solutions, Inc.)

- AmberBox, Inc.

- Nextivity, Inc.

- Knightscope, Inc

- Omnilert LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating gun-related violence in major cities

- 4.2.2 Growing federal and municipal safety-tech grants

- 4.2.3 Accuracy gains from acoustic and IR sensor fusion

- 4.2.4 Modernization of soldier situational-awareness kits

- 4.2.5 Insurance-premium discounts for protected sites

- 4.2.6 Real-time-crime-centre demand for API-ready feeds

- 4.3 Market Restraints

- 4.3.1 High capex and OPEX for multi-node deployments

- 4.3.2 Evidentiary reliability and false-alert concerns

- 4.3.3 Privacy/civil-liberty litigation risk

- 4.3.4 Budgets shifting to multi-sensor drone platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Indoor

- 5.1.2 Outdoor

- 5.2 By Installation

- 5.2.1 Fixed

- 5.2.2 Vehicle-Mounted

- 5.2.3 Soldier-Mounted/Portable

- 5.3 By Solution

- 5.3.1 Systems

- 5.3.2 Subscription-Based Gunshot Detection Services (SaaS)

- 5.4 By End-User

- 5.4.1 Defense and Military

- 5.4.2 Law Enforcement Agencies

- 5.4.3 Commercial and Critical Infrastructure

- 5.4.4 Campus and Educational Institutions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SoundThinking, Inc.

- 6.4.2 Raytheon BBN (RTX Corporation)

- 6.4.3 Thales Group

- 6.4.4 QinetiQ Group plc

- 6.4.5 ASELSAN A.S.

- 6.4.6 ACOEM Group

- 6.4.7 Databuoy Corporation

- 6.4.8 Microflown AVISA

- 6.4.9 Israel Aerospace Industries Ltd.

- 6.4.10 Rafael Advanced Defense Systems Ltd.

- 6.4.11 Rheinmetall AG

- 6.4.12 Shooter Detection Systems LLC

- 6.4.13 Safety Dynamics, Inc.

- 6.4.14 EAGL Technology, Inc.

- 6.4.15 Louroe Electronics, Inc.

- 6.4.16 Pelco (Motorola Solutions, Inc.)

- 6.4.17 AmberBox, Inc.

- 6.4.18 Nextivity, Inc.

- 6.4.19 Knightscope, Inc

- 6.4.20 Omnilert LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment