|

시장보고서

상품코드

1836515

인조잔디 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Artificial Turf - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

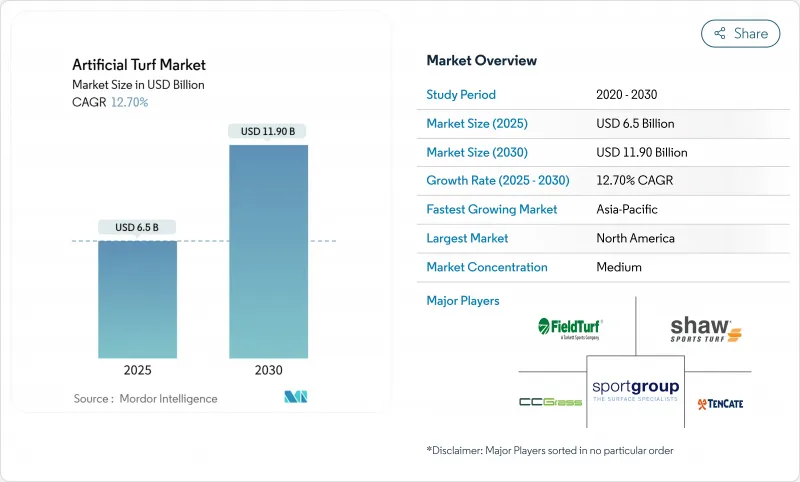

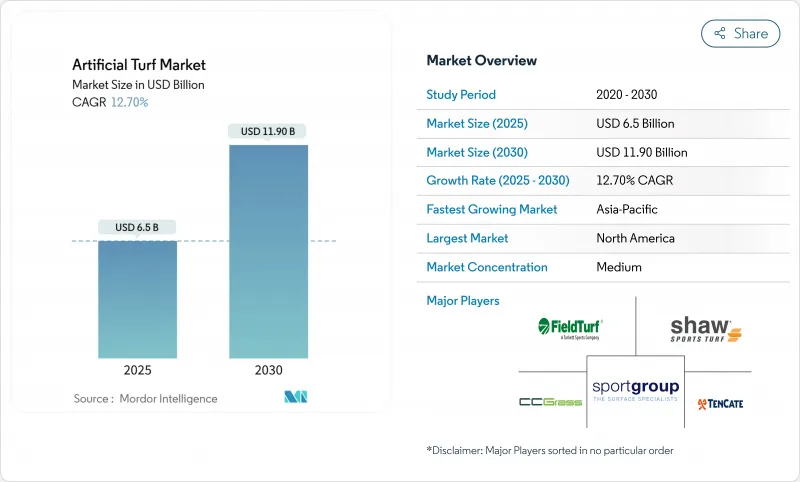

세계의 인조잔디 시장 규모는 2025년 65억 달러로, 2030년에는 119억 달러에 이르고, CAGR 12.7%를 보일 것으로 예측됩니다.

가뭄 위험 증가와 절수법의 의무화로 인해 수요는 스포츠 장소뿐만 아니라 주택, 상업시설, 시민 인프라로 이동하고 있습니다. Tarkett(FieldTurf)와 TenCate Grass와 같은 세계 리더들은 대규모 압출 성형 능력과 조기 재활용 프로그램을 통해 점유율을 보호하고, Shaw Sports Turf, CCGrass, 그리고 늘어나고 있는 지역의 스페셜리스트 집단은 근접성과 가격의 민첩성을 살려 자치체 현재 혁신의 중심은 저가열 섬유화학물질, PFAS 프리 처방, 폐쇄 루프 재활용 파트너십으로 EU의 마이크로플라스틱 규제 강화와 북미의 확대 생산자 책임 제안에 대응하고 있습니다. 바이어는 엔드 오브 라이프 솔루션과 검증된 냉각 성능으로 공급업체를 평가하고 있으며, 시장 전체의 단편화가 계속되는 가운데서도 기술 소유자에게 가격 프리미엄을 주고 있습니다.

세계 인조잔디 시장 동향과 통찰

엄격한 절수 의무

캘리포니아의 AB1572와 콜로라도의 SB24-005는 비 기능적 잔디에서 식수에 의한 관개를 제거하고 기능적이지 않은 잔디의 신설을 금지합니다. 스케줄이 빨라지면 시공업체의 용량이 압박되어 인조잔디의 교체 사이클이 앞당겨지기 때문에 인조잔디 시장은 사실상 팀 시즌 예산이 아니라 공공정책의 캘린더에 고정되게 됩니다. 애리조나, 네바다, 그리고 호주의 일부 지자체는 감소하는 대수층을 보호하기 위해 병행하여 조례의 초안을 시작합니다.

멀티스포츠 스타디움에 도입 확대

엘리트 장소에서는 축구, 축구 및 콘서트를 압축된 일정에서 개최할 수 있는 필드가 점점 더 요구되고 있습니다. Mercedes-Benz Stadium의 2025년 FieldTurf CORE 설치와 SoFi 스타디움의 2026년 월드컵용 하이브리드 터프 파일럿은 대규모 계약으로 차세대 시스템이 가시화됨을 보여줍니다. 이러한 사양의 향상은 2-3회의 입찰 사이클 중에 대학이나 2차 시설로 이행해 각 기함 프로젝트의 수익에 대한 영향력을 배증시킵니다.

마이크로 및 나노플라스틱 오염의 조사

유럽 화학물질청은 스포츠 피치가 연간 1만 6,000톤의 마이크로플라스틱을 배출하고 있는 것으로 추정하고 있으며, 대륙 전체에서 고무 부스러기의 단계적 폐지 기운을 가속화하고 있습니다. 제조업체는 인필 봉쇄를 재설계하여 폴리머 결합형 또는 식물 유래의 대체품을 찾아야 하며, 시스템 비용은 8-12% 상승합니다. 과학적 연구에 의해 기계적 마모에 의한 나노플라스틱 섬유의 탈락이 확인되고, 사양 제한의 강화나 생산자 책임 제도의 확대를 요구하는 논의가 강해지고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 급증하는 주택 및 상업용 조원 수요

- 도시의 열섬 기후 회복 프로젝트

- 높은 초기 설치 비용

부문 분석

스포츠는 2024년 인조잔디 시장의 42.7%를 차지했고, 프로와 대학 회장에서는 8년부터 10년의 교환 사이클이 반복되고 있습니다. 콘택트 스포츠, 하키, 테니스, 야구장에서는 볼의 구름과 충격의 감쇠를 최적화하는 섬유 배합이 추구되어 수지 코스트가 상승해도 마진을 확보할 수 있는 프리미엄층이 강화되고 있습니다.

현재는 열반사성 안료나 보증 검증을 위해 유지보수 데이터를 기록하는 스티치 라벨 등이 업그레이드되고 있습니다. 한편, 지방자치단체가 가뭄 대책에 중점을 두고 있기 때문에 2030년까지의 CAGR은 15.3%로 예상되어, 모든 스포츠의 하위 부문을 웃돌고 있습니다. 상업시설에서는 솔기의 번거로움을 없애기 위해 와이드 롤 제품을 채용하고, 운동장에서는 ASTM F1292의 폴 높이 기준을 충족하는 언더레이 패드를 지정하고 있습니다.

지역별 분석

북미의 점유율 38.2%는 기준선 수요를 고정하는 교체 사이클의 규칙성과 규제 압력을 강조합니다. 캘리포니아에서는 작동하지 않는 잔디에 대한 식수 금지 명령이 있지만 콜로라도에서는 잔디 심기 모라토리엄이 일정의 유연성이 제한된 즉각적인 준수 프로젝트를 만들고 있습니다. 멕시코의 시영 공원에서는 수도 요금의 상승을 억제하고, 기온의 상승에도 불구하고 플레이 시간을 연장하기 위해, 합성 잔디가 선호되고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)이 14.4%로 아시아태평양이 가장 급성장하며 중국과 인도의 경기장 건설 외에도 공급망을 단축하는 호주 제조 규모가 뒷받침되고 있습니다. 이 지역의 화물 수송의 우위성이 동남아시아 전역으로의 수출을 지지하는 한편, 일본의 밀집 시가지는 열완화 섬유의 테스트 베드가 됩니다. 한국에서는 정부 보조금이 학교용 피치의 초기 비용을 상쇄해 초등 교육 시설에의 보급을 가속시키고 있습니다.

유럽에서는 환경 규제가 복잡해지고 있습니다. 유럽에서는 미립자 인필이 금지되어 있기 때문에 클럽은 폴리머 결합 엘라스토머나 미네랄 옵션으로의 이행을 강요하고, 시스템 가격은 상승하지만, 수명도 연장됩니다. Wembley Stadium의 폐기물 제로 피치 재활용 평가판은 프랑스 리그 1의 클럽이 2026년 리노베이션을 위해 평가하는 순환 템플릿을 소개합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 절수 의무

- 멀티 스포츠 경기장에 설치 확대

- 주택 및 상업용 조원 수요의 급증

- 도시의 열섬 기후 회복 프로젝트

- 자율형 잔디 부설 로봇의 채용

- 잔디의 순환형 리사이클 및 EPR 프로그램

- 시장 성장 억제요인

- 마이크로 플라스틱이나 나노 플라스틱에 의한 오염에 대한 우려

- 높은 초기 도입 비용

- 유럽연합(EU)에 의한 크럼 고무 인필 금지

- 기업에 의한 히트 스트레스 소송의 위험

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자/소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측(금액, 달러)

- 용도별

- 스포츠

- 콘택트 스포츠

- 필드 하키

- 테니스

- 기타 스포츠

- 레저

- 경관

- 스포츠

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Tarkett(FieldTurf)

- TenCate Grass(Leonard Green & Partners, LP)

- Shaw Sports Turf

- CCGrass

- Sports Group(Polytan)

- Act Global(Beaulieu International Group)

- SprinTurf(Integrated Turf Solutions LLC)

- ForeverLawn

- SIS Pitches

- Victoria PLC

- Global Syn-Turf

- Lano Sports(Lano Carpets NV)

- Watershed Geo

제7장 시장 기회와 전망

JHS 25.10.28The artificial turf market is valued at USD 6.5 billion in 2025 and is forecast to reach USD 11.9 billion by 2030, registering a 12.7% CAGR.

Heightened drought risk and mandatory water-conservation laws are shifting demand beyond sports venues into residential, commercial, and civic infrastructure. Competitive intensity remains moderate; global leaders such as Tarkett (FieldTurf) and TenCate Grass defend their share through large-scale extrusion capacity and early-stage recycling programs, while Shaw Sports Turf, CCGrass, and a growing cadre of regional specialists leverage proximity and price agility to win municipal and school contracts. Innovation now centers on low-heat fiber chemistries, PFAS-free formulations, and closed-loop recycling partnerships that address tightening EU microplastics rules and North American extended-producer-responsibility proposals. Buyers increasingly evaluate suppliers on end-of-life solutions and verified cooling performance, giving technology owners a pricing premium even as overall market fragmentation persists.

Global Artificial Turf Market Trends and Insights

Stringent Water-Conservation Mandates

California's AB 1572 and Colorado's SB 24-005 remove potable-water irrigation from nonfunctional lawns and ban new nonfunctional turf, converting discretionary upgrades into compliance obligations. Accelerated timelines strain installer capacity and pull forward replacement cycles, effectively anchoring the artificial turf market to public-policy calendars rather than team-season budgets. Municipalities in Arizona, Nevada, and parts of Australia have begun drafting parallel ordinances to safeguard dwindling aquifers.

Expanding Installation in Multi-Sport Stadia

Elite venues increasingly demand fields that can host football, soccer, and concerts within compressed scheduling windows. Mercedes-Benz Stadium's 2025 FieldTurf CORE installation and SoFi Stadium's hybrid turf pilot for the 2026 World Cup illustrate the visibility that large contracts create for next-generation systems. These specification uplifts migrate to collegiate and secondary facilities within two to three bid cycles, multiplying the revenue influence of each flagship project.

Micro- and Nano-Plastic Pollution Scrutiny

The European Chemicals Agency estimates sports pitches contribute 16,000 tons of microplastics annually, accelerating momentum for a continent-wide crumb-rubber phase-out Manufacturers must redesign infill containment and explore polymer-bound or plant-based alternatives, raising system costs by 8%-12%. Scientific studies have now confirmed nano-plastic fiber shedding under mechanical wear, strengthening arguments for tighter specification limits and extended producer responsibility schemes.

Other drivers and restraints analyzed in the detailed report include:

- Surging Residential and Commercial Landscaping Demand

- Urban Heat-Island Climate-Resilience Projects

- High Upfront Installation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sports accounted for a 42.7% slice of the artificial turf market in 2024, anchoring recurring eight- to ten-year replacement cycles across professional and collegiate venues. Contact Sports, hockey, tennis and baseball fields pursue fiber blends that optimize ball roll and shock attenuation, reinforcing a premium tier that shields margins even when resin costs climb.

Upgrades now include heat-reflective pigments and stitched labels that log maintenance data for warranty validation. Meanwhile, the landscape cohort is advancing at a 15.3% CAGR to 2030, outpacing every sports sub-segment as municipalities pivot toward drought resilience. Commercial complexes adopt wide-roll products to cut seam labor, while playgrounds specify underlay pads that meet ASTM F1292 fall-height criteria.

The Artificial Turf Market is Segmented by Usage (Sports, Leisure, and Landscape) and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 38.2% stake underscores replacement-cycle regularity and regulatory pressure that lock in baseline demand. California's potable-water ban for nonfunctional lawns and Colorado's turf-planting moratorium create immediate compliance projects with limited scheduling flexibility. Mexico's municipal parks favor synthetics to curb rising water bills and extend play hours despite temperature spikes.

Asia-Pacific delivers the fastest growth at 14.4% CAGR through 2030, propelled by stadium construction in China and India, plus an Australian manufacturing scale that shortens supply chains. The region's freight advantage supports exports across Southeast Asia, while Japan's dense urban zones provide test beds for heat-mitigating fibers. Government grants in South Korea offset upfront costs for school pitches, accelerating penetration in primary education facilities.

Europe wrestles with environmental regulation complexity. The European ban on particulate infill forces clubs to transition to polymer-bound elastomers or mineral options, lifting system prices, but also extending service life. Wembley Stadium's zero-landfill pitch-recycling trial showcases a circular template that French Ligue 1 clubs are now evaluating for 2026 renovations.

- Tarkett (FieldTurf)

- TenCate Grass (Leonard Green & Partners, L.P.)

- Shaw Sports Turf

- CCGrass

- Sports Group (Polytan)

- Act Global (Beaulieu International Group)

- SprinTurf (Integrated Turf Solutions LLC)

- ForeverLawn

- SIS Pitches

- Victoria PLC

- Global Syn-Turf

- Lano Sports (Lano Carpets NV)

- Watershed Geo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent water-conservation mandates

- 4.2.2 Expanding installation in multi-sport stadia

- 4.2.3 Surging residential and commercial landscaping demand

- 4.2.4 Urban-heat-island climate resilience projects

- 4.2.5 Adoption of autonomous turf-laying robots

- 4.2.6 Circular turf recycling/EPR programs

- 4.3 Market Restraints

- 4.3.1 Micro and nano-plastic pollution scrutiny

- 4.3.2 High upfront installation cost

- 4.3.3 European Union ban on crumb-rubber infill

- 4.3.4 Player heat-stress litigation risk

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat from Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Usage

- 5.1.1 Sports

- 5.1.1.1 Contact Sports

- 5.1.1.2 Field Hockey

- 5.1.1.3 Tennis

- 5.1.1.4 Other Sports

- 5.1.2 Leisure

- 5.1.3 Landscape

- 5.1.1 Sports

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of Noth America

- 5.2.2 South America

- 5.2.2.1 Brazil

- 5.2.2.2 Argentina

- 5.2.2.3 Rest of South America

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 Russia

- 5.2.3.7 Rest of Europe

- 5.2.4 Asia-Pacific

- 5.2.4.1 China

- 5.2.4.2 Japan

- 5.2.4.3 India

- 5.2.4.4 Australia

- 5.2.4.5 Rest of Asia-Pacific

- 5.2.5 Middle East

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Rest of Middle East

- 5.2.6 Africa

- 5.2.6.1 South Africa

- 5.2.6.2 Rest of Africa

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tarkett (FieldTurf)

- 6.4.2 TenCate Grass (Leonard Green & Partners, L.P.)

- 6.4.3 Shaw Sports Turf

- 6.4.4 CCGrass

- 6.4.5 Sports Group (Polytan)

- 6.4.6 Act Global (Beaulieu International Group)

- 6.4.7 SprinTurf (Integrated Turf Solutions LLC)

- 6.4.8 ForeverLawn

- 6.4.9 SIS Pitches

- 6.4.10 Victoria PLC

- 6.4.11 Global Syn-Turf

- 6.4.12 Lano Sports (Lano Carpets NV)

- 6.4.13 Watershed Geo