|

시장보고서

상품코드

1836524

유전자 발현 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Gene Expression Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

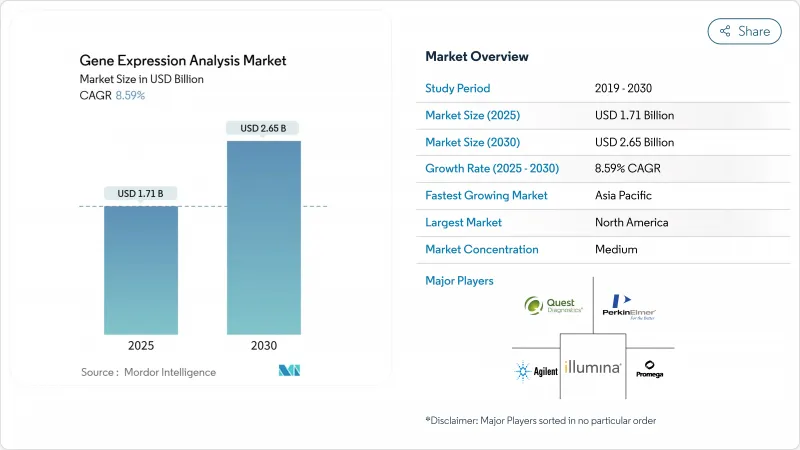

세계의 유전자 발현 분석 시장 규모는 2025년 17억 1,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 8.59%로 확대되어, 2030년에는 26억 5,000만 달러에 달할 것으로 예측됩니다.

이 확장은 시퀀싱 워크플로우에 대한 인공지능의 꾸준한 통합, 멀티오믹스 프로파일링의 임상 이용 확대, 보험 상환 및 규제 체제의 지원을 반영합니다. 연구실이 온전한 조직 내의 유전자 활성을 매핑하는 공간 생물학 도구를 채택하고 정부가 연구의 발견을 일상적인 환자 관리에 연결시키는 유전체 기반에 자금을 투입함에 따라 수요는 가속화되고 있습니다. 플랫폼 공급업체는 보다 빠르고 정밀한 장비를 지원하며, 서비스 제공업체는 클라우드 기반 바이오인포매틱스의 규모를 확대하고 기술 부족을 완화합니다. 시약 공급업체와 장비 제조업체의 통합으로 가격 경쟁이 치열해지고 있지만, 합성 뉴클레오티드 공급망의 취약성과 데이터 주권에 관한 규칙은 여전히 성장에 대한 지속적인 위험이 되고 있습니다.

세계의 유전자 발현 분석 시장 동향과 통찰

NGS 및 qPCR 플랫폼의 급속한 기술 발전

차세대 시퀀서는 현재 텔로미어 사이의 분석에 도달하고 짧은 리드 시스템은 놓친 구조 돌연변이와 후성 유전 마크를 밝히고 있습니다. Oxford Nanopore의 긴 리드 장치는 증폭 단계 없이 직접 RNA 데이터를 제공하고 AI로 강화된 기본 호출을 통해 오류율과 계산의 필요성을 줄입니다. 정량 PCR과의 통합은 확인 워크플로우를 단축하고 총 처리량을 향상시킵니다. QIAGEN의 AI가 탑재된 Ingenuity Pathway Analysis는 원시 리드 데이터를 임상가가 몇 시간 내에 해석할 수 있는 생물학적 패스웨이로 변환합니다. 이러한 진보를 조합하면 소요 시간이 단축되고 루틴 진단에의 채용이 넓어집니다.

유전체학에 대한 정부 자금 증가

국가 프로그램은 유전체학를 경쟁 자산으로 취급합니다. 미국 국립위생연구소는 유전체 데이터를 학습형 의료 시스템에 통합하기 위해 2024년 2,700만 달러를 할당했습니다. 인도는 2025년에 10,000명의 유전체 시퀀싱을 종료하고 집단별 참조를 작성합니다. 중국의 인간 유전체 프로젝트 II는 세계 인구의 1% 시퀀싱을 목표로 하고 있으며, 호주의 Genomics Health Futures Mission은 10년간 5억 10만 달러의 예산을 기록하고 있습니다. 이러한 펀드는 탐색 과학에서 임상 개발로 초점을 옮겨 시퀀싱 능력에 대한 장기적인 수요를 유지합니다.

첨단 시퀀서의 높은 자본 비용

최상급 공간 생물학 플랫폼은 종종 1대당 100만 달러를 초과하며 추가적인 이미징 모듈과 고성능 컴퓨팅이 필요합니다. 라틴아메리카, 아프리카, 아시아의 일부 소규모 실험실에서는 구매가 지연되거나 서비스 제공업체에 의존함으로써 자금력 있는 허브에 대수가 집중됩니다. 유전체당 200달러라는 Illumina의 목표는 여전히 멀고 비용 장벽을 강화하고 있습니다. 임대 계약은 지불을 분산하지만 총 지출을 증가시키고 데이터 파이프라인에 대한 사용자의 통제를 감소시킵니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 정밀의료의 채용 확대

- 공간 오믹스와 단일 세포 프로파일링의 통합

- 숙련된 생물 정보학자 부족

부문 분석

유전자 발현 분석의 기술별 시장 규모는 정량 PCR이 34.28%의 수익을 유지하는 한편, 공간 전사체학는 15.23%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 공간 도구는 조직의 맥락을 유지하고 벌크 분석이 덮는 세포 간 상호 작용을 밝힙니다. 차세대 시퀀서는 여전히 진단에 필수적이지만, 현재는 구조 돌연변이를 해명하는 긴 리드 화학을 통합하고 있습니다. 디지털 PCR은 절대적인 정량을 필요로 하는 사용자를 획득했으며, 마이크로어레이는 타겟팅된 패널에 대응할 수 있게 되었습니다.

공간적 기법은 탐색 파이프라인을 재구성합니다. Oxford Nanopore의 Mk1D MinION은 전염병 발생 시 베드사이드 시퀀싱을 제공하며, ElysION 로봇은 라이브러리 준비를 자동화합니다. 비교 벤치마크에서 10x Genomics의 Chromium Fixed RNA Profiling 키트는 감도로 타사를 능가하며, Becton Dickinson의 Rhapsody 키트는 저렴한 옵션을 제공합니다. 인공지능은 런타임 오류 수정을 줄이고 사용 편의성을 향상시킵니다. 이러한 동향이 결합되어 공간 생물학의 주목도가 높아지고 유전자 발현 분석 시장의 고성장이 유지되고 있습니다.

서비스는 13.23%의 연평균 복합 성장률(CAGR)을 기록했으며 유전자 발현 분석 업계에서 가장 빠릅니다. 이는 실험실이 내부 용량을 넘는 멀티오믹스 분석을 아웃소싱하기 때문입니다. 시약 및 소모품은 여전히 2024년 매출의 48.65%를 차지했으며 일상적인 워크플로우에서 중요한 역할을 하고 있음을 뒷받침하고 있습니다. 클라우드 호스팅의 바이오인포매틱스는 데이터 과학자를 고용하지 않고 신속한 턴어라운드를 요구하는 병원과 제약 스폰서를 끌어들입니다. 위탁 연구 기관은이 수요를 캡처하기 위해 단일 세포 분석을 포함하는 메뉴를 확장합니다.

기업은 보다 이익률이 높은 소프트웨어 및 서비스로 축발을 옮깁니다. QIAGEN은 Digital Insights 포트폴리오를 확대해 5개의 발매를 계획하고, BD는 Biosero와 제휴해 플로우 사이토메트리와 로보틱스를 제휴합니다. 플랫폼의 수명이 5년을 넘었기 때문에 장비 성장이 느려지지만 공간 이미지 애드온 업그레이드는 여전히 필요합니다. 로보틱스는 오염 위험을 줄이고 배치 품질을 일정하게 유지하므로 검사량을 확대하는 진단 실험실에 호소합니다.

지역별 분석

북미는 2024년 매출의 43.56%를 차지하며 바이오마커 검사 보험 적용을 의무화한 혜택을 받고 있습니다. 미국 국립위생연구소(National Institutes of Health)가 유전체 대응 의료 시스템에 투자하면 데이터가 임상 워크플로로 이어집니다. 2024년에 FDA가 8개의 세포 및 유전자 치료를 승인함으로써 규제 당국의 수용이 확인되고 검사 이용이 촉진됩니다. 캐나다는 정밀의료 프로그램을 확장하고 멕시코는 감염 시퀀싱에 자금을 돌려 보냅니다.

아시아태평양은 CAGR 11.64%로 가장 빠른 궤도를 보였으며 유전자 발현 분석 시장 점유율은 급속히 상승하고 있습니다. 인도는 10,000개의 유전체 프로젝트를 완성하여 문화적으로 연관된 참조 세트를 만들었습니다. 중국의 인간 유전체 프로젝트 II의 제안은 세계 인구의 1% 시퀀싱을 목표로 하는 야심을 강조하는 것이며, 일본의 오믹스 브라우저는 동아시아의 유전체에 맞는 멀티오믹스 툴을 제공하는 것입니다. 호주 유전체학 헬스 퓨처스 미션(Genomics Health Futures Mission)은 조정에 어려움이 있음에도 불구하고 88개 프로젝트에 자금을 제공합니다. 한국은 AI와 롱 리드 시퀀싱을 조합한 스타트업 기업을 지원하고 있습니다.

유럽에서는 Horizon 연구 공모와 국가 헬스케어 예산에 의해 꾸준한 확대를 유지합니다. 영국의 Royal Marsden 병원에서는 로봇에 의한 유전체 검사로 처리량이 두배로 되어 에러가 감소합니다. 독일과 프랑스가 NGS 종양 패널의 상환을 합리화합니다. 중동 및 아프리카에서는 사우디아라비아가 QIAGEN과 각서를 나누는 등 관민의 유전체 센터를 모색합니다. 남미는 급성장하지만 브라질과 아르헨티나가 국제 공동 연구에 참여하고 실험실이 시퀀싱 시약을 저렴하게 얻을 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- NGS 및 qPCR 플랫폼의 급속한 기술 진보

- 유전체학에 대한 정부 자금 증가

- 정밀 의학 보급

- 공간 오믹스와 싱글 셀 프로파일링의 통합

- AI 주도의 바이오인포매틱스 및 파이프라인

- 세포 및 유전자 치료 제조 QC 수요

- 시장 성장 억제요인

- 첨단 시퀀서의 높은 자본 비용

- 숙련된 생물 정보학자의 부족

- 유전체 데이터에 관한 데이터 주권 규제

- 시약 공급 체인의 취약성(합성 뉴클레오티드)

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 기술별

- 중합효소 연쇄반응(PCR)

- 정량적 PCR(qPCR)

- 디지털 PCR(dPCR)

- 차세대 시퀀서(NGS)

- 마이크로어레이

- 공간 전사체학

- 기타

- 제품 유형별

- 장치

- 시약 및 소모품

- 서비스

- 용도별

- 종양학

- 유전자 질환 조사

- 감염증 진단

- 농업 및 식물 유전체

- 기타 용도

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 진단 실험실

- 학술 및 연구센터

- 개발 업무 수탁 기관(CRO)

- 병원 및 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Illumina Inc.

- Thermo Fisher Scientific Inc.

- QIAGEN NV

- Agilent Technologies

- Bio-Rad Laboratories Inc.

- F. Hoffmann-La Roche Ltd

- PerkinElmer Inc.

- Novogene Co., Ltd.

- Luminex Corporation

- Quest Diagnostics Incorporated

- Promega Corporation

- Oxford Nanopore Technologies

- Pacific Biosciences of California, Inc.

- Takara Bio Inc.

- BGI Genomics Co., Ltd.

- 10x Genomics

- NanoString Technologies Inc.

- Fluidigm Corporation

- GenScript Biotech Corporation

- Merck KGaA

제7장 시장 기회와 전망

JHS 25.10.28The Gene Expression Analysis Market size is estimated at USD 1.71 billion in 2025, and is expected to reach USD 2.65 billion by 2030, at a CAGR of 8.59% during the forecast period (2025-2030).

This expansion reflects the steady integration of artificial intelligence into sequencing workflows, the widening clinical use of multi-omics profiling, and supportive reimbursement and regulatory frameworks. Demand accelerates as laboratories adopt spatial biology tools that map gene activity within intact tissue, and as governments channel funding toward genomic infrastructure that links research discoveries to routine patient care. Platform suppliers respond with faster, more accurate instruments, while service providers scale cloud-based bioinformatics that lessen the skills shortage. Consolidation among reagent vendors and instrument makers intensifies price competition, yet supply chain fragility for synthetic nucleotides and data-sovereignty rules remain persistent risks to growth.

Global Gene Expression Analysis Market Trends and Insights

Rapid Technological Advancement in NGS & qPCR Platforms

Next-generation sequencing now reaches telomere-to-telomere assemblies that uncover structural variants and epigenetic marks missed by short-read systems. Oxford Nanopore's long-read instruments deliver direct RNA data without amplification steps, while AI-enhanced base-calling lowers error rates and computing needs. Integration with quantitative PCR shortens confirmatory workflows and boosts total throughput. QIAGEN's AI-powered Ingenuity Pathway Analysis converts raw reads into biological pathways that clinicians can interpret within hours. Collectively, these advances cut turnaround times and widen adoption in routine diagnostics.

Increased Government Funding for Genomics

National programs treat genomics as a competitiveness asset. The US National Institutes of Health assigned USD 27 million in 2024 to weave genomic data into learning health systems. India finished sequencing 10,000 genomes in 2025 to create population-specific references. China's Human Genome Project II proposal seeks to sequence 1% of the global population, while Australia's Genomics Health Futures Mission earmarks AUD 500.1 million over ten years. Such funding shifts the focus from discovery science to clinical deployment and sustains long-term demand for sequencing capacity.

High Capital Costs of Advanced Sequencers

Top-tier spatial biology platforms often exceed USD 1 million per unit and require extra imaging modules and high-performance computing. Smaller laboratories in Latin America, Africa, and parts of Asia delay purchases or rely on service providers, which concentrates volume among well-funded hubs. Illumina's target of USD 200 per genome remains distant, reinforcing cost barriers. Leasing agreements spread payments but increase total outlay and reduce user control over data pipelines.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Precision Medicine

- Integration of Spatial-Omics & Single-Cell Profiling

- Shortage of Skilled Bioinformaticians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The gene expression analysis market size for technology segments with quantitative PCR retaining 34.28% revenue while spatial transcriptomics registers an unmatched 15.23% CAGR. Spatial tools preserve tissue context and reveal cell-cell interactions that bulk assays mask. Next-generation sequencing remains essential in diagnostics but now integrates long-read chemistry that resolves structural variants. Digital PCR gains users who need absolute quantification, and microarrays decline yet stay relevant for targeted panels.

Spatial methods reshape discovery pipelines. Oxford Nanopore's Mk1D MinION provides bedside sequencing for infectious disease outbreaks, and its ElysION robot automates library prep. Comparative benchmarks show 10x Genomics' Chromium Fixed RNA Profiling kit outperforming peers on sensitivity, while Becton Dickinson's Rhapsody kit offers budget options. Artificial intelligence reduces run-time error correction, broadening usability. Together these trends elevate spatial biology's profile and sustain high growth inside the gene expression analysis market.

Services posted a 13.23% CAGR, the fastest within the gene expression analysis industry, as labs outsource multi-omics analytics that exceed internal capacity. Reagents and consumables still delivered 48.65% of 2024 revenue, confirming their anchoring role in daily workflows. Cloud-hosted bioinformatics attracts hospitals and pharmaceutical sponsors seeking quick turnaround without hiring data scientists. Contract research organizations expand menu offerings, including single-cell analytics, to tap this demand.

Firms pivot toward higher-margin software and services. QIAGEN expanded its Digital Insights portfolio with five planned launches while BD partnered with Biosero to link flow cytometry and robotics. Instrument growth decelerates since platform life spans now exceed five years, yet upgrades remain necessary for spatial imaging add-ons. Robotic handling lowers contamination risk and keeps batch quality consistent, which appeals to diagnostic labs scaling test volumes.

The Gene Expression Analysis Market Report Segments the Industry Into by Technology (Polymerase Chain Reaction, Quantitative PCR, and More), Product Type (Instruments, and More), Application (Oncology, and More), End-User (Pharmaceutical and Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 43.56% of 2024 revenue and benefits from insurance mandates that compel coverage of biomarker tests. The National Institutes of Health investment in genomics-enabled health systems steers data into clinical workflows. FDA approvals of eight cell and gene therapies in 2024 confirm regulatory acceptance and stimulate test utilization. Canada expands precision medicine programs, while Mexico channels funds toward infectious disease sequencing; yet growth moderates as the market approaches maturity.

Asia-Pacific exhibits the fastest trajectory at 11.64% CAGR, and its share of the gene expression analysis market is rising quickly. India completed the 10,000-genome project that yields a culturally relevant reference set. China's Human Genome Project II proposal underlines ambitions to sequence 1% of the global population, and Japan's Omics Browser tailors multi-omics tools to East Asian genomes. Australia's Genomics Health Futures Mission funds 88 projects despite coordination challenges. South Korea backs start-ups that combine AI and long-read sequencing.

Europe maintains steady expansion through Horizon research calls and national healthcare budgets. Robotic genomic testing at the UK's Royal Marsden hospital doubles throughput and lowers errors. Germany and France streamline reimbursement for NGS tumor panels. The Middle East and Africa explore public-private genomics centers, with Saudi Arabia signing memoranda with QIAGEN. South America records slower gains; however, Brazil and Argentina join international collaborations that give laboratories affordable access to sequencing reagents.

- Illumina

- Thermo Fisher Scientific

- QIAGEN

- Agilent Technologies

- Bio-Rad Laboratories

- Roche

- PerkinElmer

- Novogene Co., Ltd.

- Luminex

- Quest Diagnostics

- Promega

- Oxford Nanopore Technologies

- Pacific Bioscience

- Takara Bio

- BGI Genomics Co., Ltd.

- 10x Genomics

- NanoString Technologies Inc.

- Fluidigm

- Genscript

- Merck

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Technological Advancement in NGS & qPCR Platforms

- 4.2.2 Increased Government Funding for Genomics

- 4.2.3 Growing Adoption of Precision Medicine

- 4.2.4 Integration of Spatial-Omics & Single-Cell Profiling

- 4.2.5 AI-Driven Bioinformatics Pipelines

- 4.2.6 Cell & Gene-Therapy Manufacturing QC Demand

- 4.3 Market Restraints

- 4.3.1 High Capital Costs of Advanced Sequencers

- 4.3.2 Shortage of Skilled Bioinformaticians

- 4.3.3 Data-Sovereignty Regulations on Genomic Data

- 4.3.4 Reagent Supply-Chain Fragility (Synthetic Nucleotides)

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Polymerase Chain Reaction (PCR)

- 5.1.2 Quantitative PCR (qPCR)

- 5.1.3 Digital PCR (dPCR)

- 5.1.4 Next-Generation Sequencing (NGS)

- 5.1.5 Microarrays

- 5.1.6 Spatial Transcriptomics

- 5.1.7 Others

- 5.2 By Product Type

- 5.2.1 Instruments

- 5.2.2 Reagents & Consumables

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Genetic Disease Research

- 5.3.3 Infectious Disease Diagnostics

- 5.3.4 Agriculture & Plant Genomics

- 5.3.5 Other Applications

- 5.4 By End-user

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Diagnostic Laboratories

- 5.4.3 Academic & Research Centers

- 5.4.4 Contract Research Organizations (CROs)

- 5.4.5 Hospitals & Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Illumina Inc.

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 QIAGEN N.V.

- 6.3.4 Agilent Technologies

- 6.3.5 Bio-Rad Laboratories Inc.

- 6.3.6 F. Hoffmann-La Roche Ltd

- 6.3.7 PerkinElmer Inc.

- 6.3.8 Novogene Co., Ltd.

- 6.3.9 Luminex Corporation

- 6.3.10 Quest Diagnostics Incorporated

- 6.3.11 Promega Corporation

- 6.3.12 Oxford Nanopore Technologies

- 6.3.13 Pacific Biosciences of California, Inc.

- 6.3.14 Takara Bio Inc.

- 6.3.15 BGI Genomics Co., Ltd.

- 6.3.16 10x Genomics

- 6.3.17 NanoString Technologies Inc.

- 6.3.18 Fluidigm Corporation

- 6.3.19 GenScript Biotech Corporation

- 6.3.20 Merck KGaA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment