|

시장보고서

상품코드

1836527

핵의학 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Nuclear Medicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

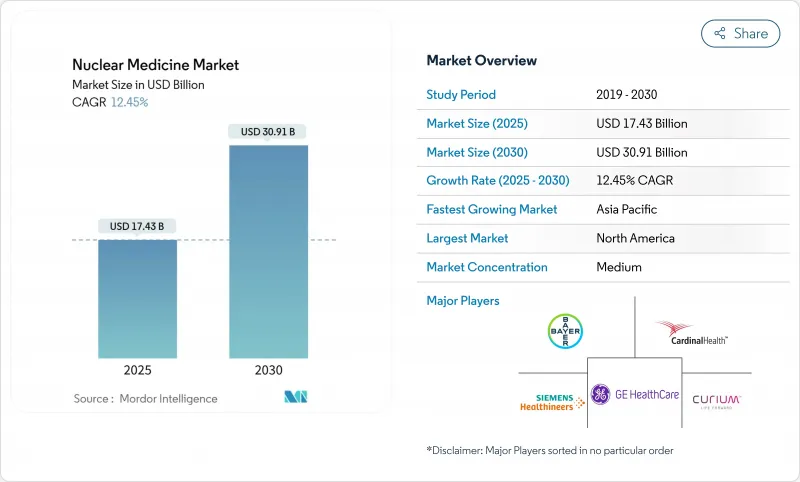

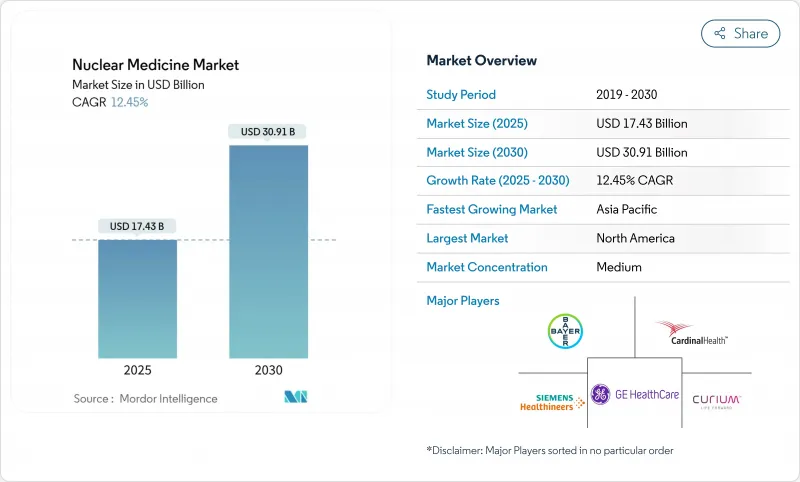

세계의 핵의학 시장 규모는 2025년 174억 3,000만 달러로, 2030년까지 309억 1,000만 달러에 이르고, CAGR 12.15%로 확대될 것으로 예측됩니다.

정밀 종양학 프로토콜, 차세대 방사성 의약품의 신속한 규제 당국 승인, 조기 단계에서 질병을 포착하는 이미지 혁신이 주요 성장 촉진 요인입니다. 국내에서의 아이소토프 생산에 유리한 정부의 대처, 고비용 트레이서에 대한 상환의 강화, AI를 활용한 워크플로우의 가속이 수요를 더욱 강화하고 있습니다. 치료용 방사성동위원소는 루테튬-177이 전립선암 이외에도 사용되게 되어 기세를 늘리고 있지만 진단용 방사성동위원소는 테크네튬-99m이 SPECT에 사용되고 있기 때문에 여전히 매출의 4분의 3을 차지하고 있습니다. 북미는 여전히 리더십을 유지하고 있지만 아시아태평양은 인프라 투자와 규제의 조화로 인해 과거의 격차를 메우고 있으며 두 자리 성장의 속도를 자극하고 있습니다. 공급망의 강인성은 경쟁 전략을 형성하고 핵의학 시장 전체의 수직 통합과 생산 능력 확대를 촉진하고 있습니다.

세계 핵의학 시장 동향과 통찰

표적 질환 부담 증가

심혈관 질환, 종양 질환 및 신경 질환의 유병률이 증가함에 따라, 임상의는 기존의 영상 진단에서 얻지 못한 분자 수준의 정확성을 제공하는 치료법으로 향하고 있습니다. 2024년에는 심장병학만으로 40.82%를 차지했지만 방사성 리간드 치료가 전이성 적응증으로 증거를 획득함에 따라 종양학이 가장 빠르게 확대됩니다. 루테튬 Lu177 도타테이트의 소아용 클리어런스는 신경 내분비 종양의 대상자를 확대하고 핵 의학이 희귀질환의 치료에 도달하는 것으로 나타났습니다. 초고분해능 PET 시스템은 이제 2mm 이하의 병변을 시각화하고 조기 신경학적 진단을 향상시키고 복잡한 질환 관리에서 핵의학 시장의 역할을 강화하고 있습니다(2).

표적 방사선 치료 채택 확대

방사선 리간드 요법은 영상 진단과 치료 투여를 통합하고 암 치료 경로를 재구성합니다. 액티늄 225와 같은 알파선 방출 핵종이 더 높은 살 종양 효과를 보이고 상업적 생산의 확대를 촉진하기 때문에 세계 테라노스틱스 분야는 2032년까지 5배로 확대될 것으로 예측됩니다. 177Lu-PSMA-617의 실제 데이터는 73.5%의 생존율과 임상적으로 의미 있는 PSA 반응을 나타내며 조기 단계에서의 전개와 적응 확대를 촉진하고 있습니다. 이러한 결과는 암 전문의와 건강 관리 지불자의 신뢰를 강화하고 핵 의학 시장을 뒷받침합니다.

복잡한 규제 당국의 승인

방사성 의약품은 의약품 규제, 방사선 규제 및 경우에 따라 장비 규제를 준수해야 하므로 일정을 연장하고 비용을 증가시킵니다. 유럽에서는 승인되지 않은 제형에 대한 9가지 다른 프레임워크가 운영되고 있으며, 액세스가 중단되고 기술 혁신이 지연됩니다. 반대로 FDA는 위험이 낮은 진단제의 보고 부담을 줄이고, 매칭이 시장의 민첩성을 향상시키는 방법을 부각하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 이미징 모달리티의 기술적 진보

- 개별화 및정밀 의약품으로의 전환

- 짧은 반감기의 아이소토프 공급망 위험

부문 분석

진단제는 테크네튬-99m의 편재성과 확립된 SPECT 인프라에 지원되어 2024년 매출의 75.15%를 차지했습니다. 그러나 치료제는 연간 19.78%를 보일 것으로 예측되며 질병 수식 치료로 전환을 보이고 있습니다. 전립선암, 신경내분비암, 그리고 잠재적으로 신장암이 방사성 리간드를 이용한 요법을 채용하기 때문에 치료제의 핵의학 시장 규모는 2025년부터 2030년 사이에 3배 이상이 될 것으로 예측됩니다. Full Pilidas F-18의 FDA 승인은 동시에 PET를 스트레스 검사 프로토콜로 확장하여 진단 범위를 확장합니다.

루테튬-177과 같은 베타선 방출 핵종이 오늘날 치료의 주류이지만, 알파선 방출 핵종도 능력 향상과 함께 임상으로 도입되고 있습니다. Eckert & Ziegler에 의한 악티늄-225의 전개와 큐륨사에 의한 루테튬-177 라인의 확대는 공급의 병목 현상의 완화를 약속하는 것입니다. 진단 약물은 전신 PET와 AI 보고서 작성이 일상 진료에 침투함에 따라 현대화되어 핵 의학 시장에서 핵심 역할을 유지합니다.

테크네튬-99m은 2024년에 42.68%의 점유율을 유지해 수십년에 걸친 임상 증거와 6시간 반감기를 중심으로 구축된 세계적인 물류의 혜택을 받고 있습니다. 그럼에도 불구하고 루테튬-177은 15.37%의 연평균 복합 성장률(CAGR)로 전진하고 있습니다. 이것은 치료의 기세와 이테르븀-176 양자 농축과 같은 새로운 공급 솔루션을 반영합니다. 루테튬-177 치료의 핵의학 시장 규모는 종양학 적응증이 증가함에 따라 확대될 것으로 보입니다.

불소-18은 사이클로트론의 확장성과 출하를 용이하게 하는 거의 2시간의 반감기를 활용하여 여전히 주력 PET 아이소토프입니다. 테르븀-161과 납-212와 같은 새로운 아이소토프는 더 높은 선 에너지 전달과 독특한 붕괴 방식을 제공하여 핵의학 시장을 더욱 다양화시킬 수 있습니다.

지역별 분석

북미는 2024년 세계 매출의 45.99%를 창출해 명확한 상환, 첨단 인프라, 국내 제조 이니셔티브에 지지를 받았습니다. CMS의 2025년 지불 분리 정책은 이용상의 중요한 장벽을 없애고, 인디애나의 신흥 아이소토프 허브에는 Cardinal Health, Eli Lilly, Novartis의 새로운 시설이 건설되어 공급의 안전성이 강화됩니다. 2025년 2월에 풀피리다스 F-18이 처음 임상 투여된 것은 핵의학 시장 전체에서 심장 PET의 채용을 확대하는 이정표가 됩니다.

아시아태평양은 가장 급성장하는 지역으로 CAGR 12.77%로 확대되고 있습니다. 이는 중국이 국내 아이소토프 프로그램을 강화하고 일본이 GE HealthCare에 의한 Nihon Medi-Physics의 완전 인수를 통해 업계의 능력을 심화시키고 있기 때문입니다. 인도에는 300개가 넘는 우수 연구센터가 있으며, 호주는 첨단 치료로 선도하고 있습니다. 규제의 조화와 인프라 투자는 역사적인 접근 격차를 꾸준히 줄이고 아시아태평양을 핵의학 시장에서 매우 중요한 성장 엔진으로 자리매김하고 있습니다.

유럽은 Orano Med의 납-212 플랜트와 Curium의 새로운 루테튬-177 사이트와 같은 프로젝트에 힘입어 강력한 R&D 거점을 유지하고 있습니다. 2007년 이후 분자 방사선 치료 세션 수는 250% 증가하고 있으며 정책 복잡성에도 불구하고 임상 기세가 있음을 알 수 있습니다. 이러한 진보는 핵의학 시장에서 아시아태평양에 비하면 성장 속도는 완만하지만 유럽의 관련성을 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 표적 질환(심혈관 질환, 암, 신경 질환)의 부담 증가

- 표적 방사선 치료의 채용 확대

- 이미징 모달리티의 기술적 진보

- 개별화 및 정밀 의약품으로의 전환

- 핵의학에 대한 정부 및 민간 기업의 주목의 고조

- 테라노스틱스와 보조적 진료 보수의 채용

- 시장 성장 억제요인

- 복잡한 규제 당국에 의한 승인

- 반감기가 짧은 아이소토프 공급망의 위험

- 핵 의학 절차 및 장비의 높은 비용

- 숙련된 방사약사의 부족

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 제품 유형별

- 진단

- SPECT

- PET

- 치료

- 알파 이미터

- 베타 이미터

- 브라키테라피용 아이소토프

- 진단

- 방사성 동위원소별

- 테크네튬-99m

- 불소-18

- 요오드-131

- 루테튬-177

- 기타

- 용도별

- 종양학

- 순환기

- 신경학

- 내분비학

- 정형외과 및 통증 관리

- 기타 용도

- 최종 사용자별

- 병원

- 화상 진단센터

- 방사선 전문 약국

- 연구기관

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- GE HealthCare

- Cardinal Health Inc.

- Curium Pharma

- Bayer AG

- Siemens Healthineers

- Koninklijke Philips NV

- Novartis AG(AAA)

- Lantheus Holdings Inc.

- Bracco Imaging SpA

- Telix Pharmaceuticals Ltd.

- Life Molecular Imaging

- NorthStar Medical Radioisotopes

- Eckert & Ziegler Radiopharma

- Jubilant Radiopharma

- Blue Earth Diagnostics

- Isotopia Molecular Imaging

- SOFIE Biosciences

- Actinium Pharmaceuticals

- IBA Molecular

제7장 시장 기회와 전망

JHS 25.10.28The nuclear medicine market is valued at USD 17.43 billion in 2025 and is forecast to climb to USD 30.91 billion by 2030, expanding at a 12.15% CAGR.

Precision-oncology protocols, rapid regulatory approvals for next-generation radiopharmaceuticals, and imaging innovations that capture disease at earlier stages are the principal growth catalysts. Government initiatives that favor domestic isotope production, stronger reimbursement for high-cost tracers, and AI-enabled workflow acceleration further reinforce demand. Therapeutic radioligands are gaining momentum as lutetium-177 moves beyond prostate cancer, while diagnostics still command three-quarters of revenue thanks to technetium-99m's entrenched use in SPECT. North America retains leadership, yet Asia-Pacific is setting the growth pace on a double-digit trajectory as infrastructure investments and harmonized regulations close historical gaps. Supply-chain resilience now shapes competitive strategy, driving vertical integration and capacity expansions across the nuclear medicine market.

Global Nuclear Medicine Market Trends and Insights

Rising Burden of Targeted Diseases

Escalating prevalence of cardiovascular, oncologic, and neurological disorders is pushing clinicians toward modalities that offer molecular precision unavailable in conventional imaging. Cardiology alone represents 40.82% of procedures in 2024, yet oncology shows the fastest expansion as radioligand therapy gains evidence across metastatic indications. Pediatric clearance of lutetium Lu 177 dotatate widened the eligible population for neuroendocrine tumors, underscoring nuclear medicine's reach into rare-disease care. Ultra-high resolution PET systems now visualize sub-2 mm lesions, improving early neurological diagnoses and reinforcing the nuclear medicine market's role in complex-disease management.[2]

Growing Adoption of Targeted Radiotherapy

Radioligand therapies integrate diagnostic imaging and therapeutic dosing, reshaping cancer care pathways. The global theranostics field is projected to multiply fivefold by 2032 as alpha emitters such as actinium-225 demonstrate higher tumor-killing potency, prompting commercial production ramp-ups. Real-world data for 177Lu-PSMA-617 show 73.5% survival and clinically meaningful PSA responses, encouraging earlier-stage deployment and broadening indications. These outcomes reinforce confidence among oncologists and healthcare payers, propelling the nuclear medicine market.

Complex Multi-Agency Regulatory Approval

Radiopharmaceuticals must comply with drug, radiation, and sometimes device regulations, stretching timelines and raising costs. Europe operates nine distinct frameworks for unlicensed preparations, fragmenting access and slowing innovation. Conversely, the FDA has trimmed reporting burdens for low-risk diagnostics, spotlighting how harmonization can improve market agility.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancement in Imaging Modalities

- Shift Toward Personalized and Precision Medicines

- Short Half-Life Isotope Supply-Chain Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostics generated 75.15% of revenue in 2024, supported by technetium-99m's ubiquity and well-established SPECT infrastructure. Yet therapeutics are forecast to grow at 19.78% annually, illustrating a pivot toward disease-modifying treatments. The nuclear medicine market size for therapeutics is expected to more than triple between 2025 and 2030 as prostate, neuroendocrine, and potentially renal cancers adopt radioligand regimens. FDA clearance of flurpiridaz F-18 simultaneously extends PET into stress-testing protocols, broadening diagnostic reach.

Beta emitters such as lutetium-177 dominate therapy today, but alpha emitters are entering clinical practice as capacity builds. Eckert & Ziegler's actinium-225 rollout and Curium's expanded lutetium-177 line promise to ease supply bottlenecks. Diagnostics are modernizing as total-body PET and AI report-generation penetrate routine practice, preserving their central role within the nuclear medicine market.

Technetium-99m retained 42.68% share in 2024, benefiting from decades of clinical evidence and global logistics built around its six-hour half-life. Nevertheless, lutetium-177 is advancing at a 15.37% CAGR, reflecting therapeutic momentum and emerging supply solutions such as ytterbium-176 quantum enrichment. The nuclear medicine market size for lutetium-177 therapies is set to expand as oncology indications multiply.

Fluorine-18 remains the workhorse PET isotope, leveraging cyclotron scalability and a near two-hour half-life that eases shipping. Novel isotopes like terbium-161 and lead-212 are progressing through trials, offering higher linear energy transfer or unique decay schemes that could further diversify the nuclear medicine market.

The Nuclear Medicine Market Report is Segmented by Product Type (Diagnostics[SPECT and PET], Therapeutics[alpha Emitters and More]), Radioisotope (Technetium-99m, Fluorine-18 and More), Application (Cardiology, Oncology, and More), End User (Hospital, Diagnostic Imaging Centers and More) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and More). He Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 45.99% of global revenue in 2024, supported by clear reimbursement, advanced infrastructure, and domestic manufacturing initiatives. CMS's payment separation policy in 2025 removes a key utilization barrier, while Indiana's emerging isotope hub houses new facilities from Cardinal Health, Eli Lilly, and Novartis, reinforcing supply security. First clinical doses of flurpiridaz F-18 administered in February 2025 mark a milestone that should broaden cardiac PET adoption across the nuclear medicine market.

Asia-Pacific is the fastest-growing region, expanding at 12.77% CAGR as China ramps domestic isotope programs and Japan deepens industry capacity through GE HealthCare's full acquisition of Nihon Medi-Physics. India's 300 plus centers of excellence and Australia's lead in advanced therapies further propel regional demand. Harmonized regulations and infrastructure investments are steadily reducing historic access gaps and positioning Asia-Pacific as a pivotal growth engine for the nuclear medicine market.

Europe retains a strong R&D footprint, buoyed by projects like Orano Med's lead-212 plant and Curium's new lutetium-177 site. Although national regulatory heterogeneity slows market entry, EU-funded consortia such as Thera4Care aim to streamline theranostic adoption.A 250% rise in molecular radiotherapy sessions since 2007 highlights clinical momentum despite policy complexity. These advances sustain Europe's relevance, albeit at a more measured growth pace compared with Asia-Pacific within the nuclear medicine market.

- GE Healthcare

- Cardinal Health

- Curium Pharma

- Bayer

- Siemens Healthineers

- Koninklijke Philips

- Novartis AG (AAA)

- Lantheus

- Bracco Imaging S.p.A.

- Telix Pharmaceuticals Ltd.

- Life Molecular Imaging

- NorthStar Medical Radioisotopes

- Eckert & Ziegler Radiopharma

- Jubilant Radiopharma

- Blue Earth Diagnostics

- Isotopia Molecular Imaging

- SOFIE Biosciences

- Actinium Pharmaceuticals

- IBA Molecular

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Targeted Diseases (Cardiovascular, Cancer and Neurological Disorders)

- 4.2.2 Growing Adoption of Targeted Radiotherapy

- 4.2.3 Technological Advancement in Imaging Modalities

- 4.2.4 Shift Towards Personalized and Precision Medicines

- 4.2.5 Increasing Focus of Government and Private Players in Nuclear Medicine

- 4.2.6 Adoption of Theranostics and Supportive reimbursement

- 4.3 Market Restraints

- 4.3.1 Complex Multi-Agency Regulatory Approval

- 4.3.2 Short Half-Life Isotope Supply Chain Risk

- 4.3.3 High Cost of Nuclear Medicine Procedures and Equipment

- 4.3.4 Scarcity Of Skilled Radio pharmacists

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Type

- 5.1.1 Diagnostics

- 5.1.1.1 SPECT

- 5.1.1.2 PET

- 5.1.2 Therapeutics

- 5.1.2.1 Alpha Emitters

- 5.1.2.2 Beta Emitters

- 5.1.2.3 Brachytherapy Isotopes

- 5.1.1 Diagnostics

- 5.2 By Radioisotope

- 5.2.1 Technetium-99m

- 5.2.2 Fluorine-18

- 5.2.3 Iodine-131

- 5.2.4 Lutetium-177

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Cardiology

- 5.3.3 Neurology

- 5.3.4 Endocrinology

- 5.3.5 Orthopedics & Pain Management

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Specialized Radiopharmacies

- 5.4.4 Research Institutes

- 5.4.5 Ambulatory Surgical Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 GE HealthCare

- 6.3.2 Cardinal Health Inc.

- 6.3.3 Curium Pharma

- 6.3.4 Bayer AG

- 6.3.5 Siemens Healthineers

- 6.3.6 Koninklijke Philips N.V.

- 6.3.7 Novartis AG (AAA)

- 6.3.8 Lantheus Holdings Inc.

- 6.3.9 Bracco Imaging S.p.A.

- 6.3.10 Telix Pharmaceuticals Ltd.

- 6.3.11 Life Molecular Imaging

- 6.3.12 NorthStar Medical Radioisotopes

- 6.3.13 Eckert & Ziegler Radiopharma

- 6.3.14 Jubilant Radiopharma

- 6.3.15 Blue Earth Diagnostics

- 6.3.16 Isotopia Molecular Imaging

- 6.3.17 SOFIE Biosciences

- 6.3.18 Actinium Pharmaceuticals

- 6.3.19 IBA Molecular

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment