|

시장보고서

상품코드

1836568

자동차 연료 공급 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Fuel Delivery System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

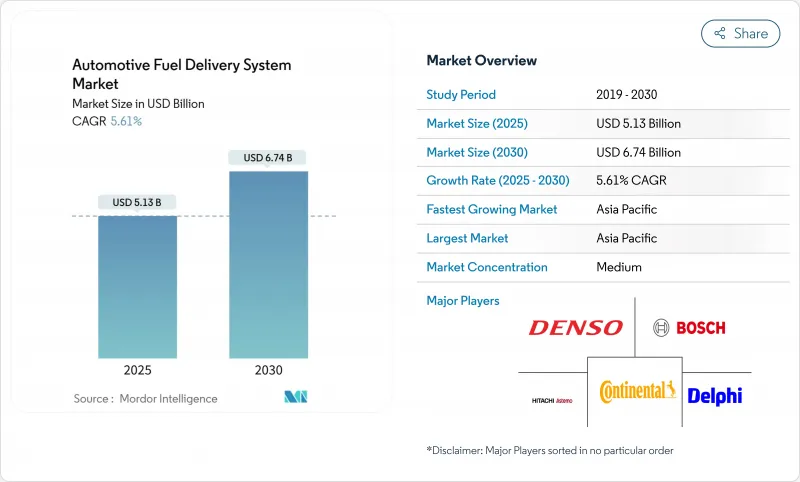

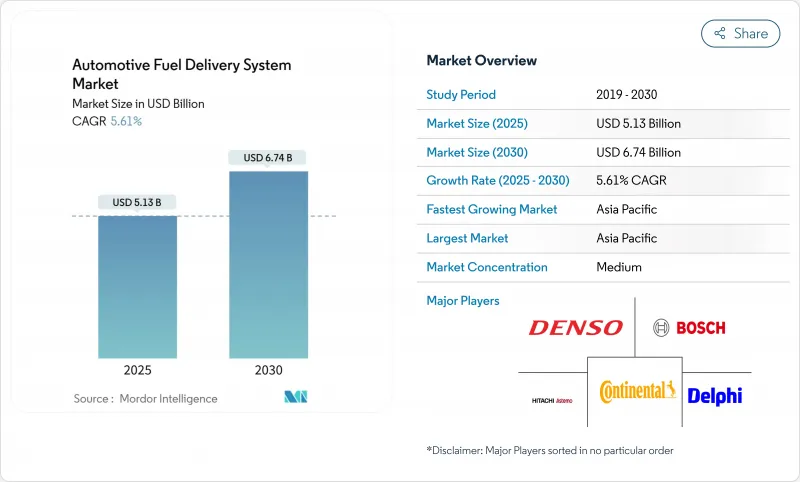

세계의 자동차 연료 공급 시스템 시장 규모는 2025년 51억 3,000만 달러로, 2030년까지 67억 4,000만 달러에 이르고, CAGR 5.61%를 보일 것으로 예측됩니다.

이 성장 궤도는 전기화가 진행되는 시대에 관련성을 유지하면서 보다 엄격한 배출 규제에 대응하는 이 분야의 능력을 반영하고 있습니다. 2025년 7월부터 적용되는 Euro 7 규제와 2027년 발효된 EPA 3단계 기준은 자동차 제조업체를 고정밀 분사 모듈과 내식성 라인으로 향하게 하여 최신 내연 기관(ICE) 아키텍처의 설비 투자를 지속하고 있습니다. 공급업체는 ICE의 가치 흐름을 유지하면서 플러그인과 연료전지 수요 변화에 대비하는 '기술 중립' 포트폴리오를 채택하여 자동차 연료 공급 시스템 시장의 하락 위험을 억제하고 있습니다.

세계 자동차 연료 공급 시스템 시장 동향과 통찰

엄격한 배기 가스 규제가 첨단 연료 공급 모듈을 견인

Euro 7은 2026년 11월부터 모든 소형 엔진의 미립자 물질과 NOx 기준치를 강화하고 EPA 3단계는 2027년 대형 트럭의 NOx를 35mg/hp-hr로 줄입니다. 따라서 자동차 제조업체는 고압 펌프와 가솔린 미립자 필터를 세계 플랫폼에서 표준화합니다. 내구성 요구 사항은 160,000km까지 증가하고 공급업체는 수명이 긴 인젝터와 내식성 레일 개발을 추진합니다.

세계 자동차 생산량 증가와 파크 회춘

2025년에는 소형차 생산량이 회복되고 유럽에서는 차량의 평균 사용연수가 12년을 넘어 교환주기가 단축되어 자동차 연료 공급 시스템 시장의 부품 수요가 강화됩니다. 자동차 제조업체는 인도, 인도네시아 및 멕시코 공장을 현지화하고 Tier-1 공급업체에 지역 소싱 풀을 생성합니다. 플릿 운영자는 연비 벤치마크를 충족하기 위해 하드웨어를 업데이트하고 EV의 보급에도 불구하고 ICE의 관련성을 길게 합니다.

전기자동차의 급성장에 의해 내연 기관차의 점유율이 저하

중국과 캘리포니아는 2035년까지 완전한 제로 방출을 의무화하는 방향으로 가속하고 있습니다. EV의 기세는 지난 10년간 ICE와 관련된 이익 풀을 예상 50% 절감합니다. 연료 펌프와 인젝터는 배터리 플랫폼에 탑재되지 않고 장기적으로는 역풍이 되지만, 지역차에 따라 자동차 연료 공급 시스템 시장은 대형차, 농촌, 신흥국의 각 부문와 관련성을 유지하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 승용차에의 가솔린 직분사 엔진 수요의 확대

- 소형 상용차 판매 증가

- 연료 시스템 부품의 원재료 가격 변동성

부문 분석

연료 펌프는 2024년에 자동차 연료 공급 시스템 시장의 37.81% 매출을 창출해, 모든 엔진 사이즈에 있어서 불가결한 존재로 계속되어, 자동차 연료 공급 시스템 시장을 지지하고 있습니다. 그 편재성은 전기화가 진행되어도 안정된 양을 공급합니다. 인젝터는 2,200psi GDI 요건을 바탕으로 CAGR 7.14%로 2030년까지 급성장하여 '스마트'한 첨단 설계와 에탄올 혼합 연료용 스테인레스 스틸 레일을 뒷받침합니다.

컴포넌트 업그레이드는 현재 온보드 진단, 원격 압력 감지 및 예기치 않은 다운타임을 줄이는 무선 펌웨어에 중점을 둡니다. 바이오연료 증가는 내식성 라인과 필터에 대한 수요를 높이고 증기 회수 밸브와 탱크 장착 센서는 전자 제품의 가치를 높입니다. 이러한 변화가 결합되어 자동차 연료 공급 시스템의 부품 시장 규모는 향후 EV 떨어지는 위협에도 불구하고 상승 곡선을 그립니다.

2024년 자동차 연료 공급 시스템 시장 수익의 64.33%는 승용차가 차지했습니다. 해치백과 세단은 비용 효율적인 리턴리스 펌프를 필요로 하지만 SUV는 토크 부하가 증가하기 때문에 고압 레일을 통합합니다. 소형 상용차의 CAGR 예측은 6.23%로 효율성보다 견고성을 선호하며 스틸 블레이드 호스와 교환 가능한 필터를 유지합니다.

1일 주행거리가 길어져 차량의 텔레매틱스가 개장 사업을 개척하는 한편, 중형 및 대형 트럭은 대수는 적지만, 배터리의 밀도가 장거리 수송의 대체를 가능하게 할 때까지, 대수를 안정시키는 고유량 디젤 분사 레일을 유지하고 있습니다. 따라서 자동차 연료 공급 시스템 시장은 듀티 사이클의 다양성을 유지하고 있습니다.

지역별 분석

아시아태평양은 자동차 연료 공급 시스템 시장의 2024년 매출액의 38.55%를 차지했고, 2030년까지의 CAGR은 6.92%로 다른 지역을 능가할 전망입니다. 중국의 OEM은 관세를 회피하고 물류 체인을 단축하기 위해 태국과 인도네시아에서 연료 시스템 서브 시스템을 구축하고 동남아시아 전역의 자동차 연료 공급 시스템 시장을 강화하고 있습니다. 일본의 반도체 합작사업도 고압펌프용 마이크로컨트롤러의 흐름을 확보하여 지역 공급 리스크를 완화하고 있습니다.

북미는 2027년까지 NOx 0.035g/b-hp-hr을 의무화하는 EPA 규제로 인해 여전히 기술이 풍부합니다. 미국 농무부의 2,600만 달러의 E15 인프라 프로그램 등의 투자는 바이오연료의 보급을 확대하고, 자동차 연료 공급 시스템 시장을 확대하는 에탄올 대응 레일이나 씰의 틈새 수요를 창출하고 있습니다. 멕시코의 매력적인 노동력 가격과 USMCA 무역의 혜택은 라모스 앨리스페와 아과스 칼리엔테스에서 생산 능력 증대를 Tier 1에 촉구합니다.

유럽은 Euro 7과 탄소 중립성 가속화라는 두 가지 압박에 직면하고 있습니다. OEM은 2026년에 앞서 파티큘레이트 필터와 증기 봉쇄 하드웨어를 개수하고 있어 차량당 부품대는 상승하지만 공급자의 수주는 유지되고 있습니다. 동유럽 공장은 라인 어셈블리 비용을 낮추고 서유럽 공장이 전기 모듈로 중심을 옮겨도 경쟁력을 확보합니다. 스페인에서 독일에 이르는 수소 통로의 시험 운영은 자동차 연료 공급 시스템 시장에 연료전지 용도에 조기 발판을 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 배기 가스 규제가 첨단 연료 공급 모듈의 채용을 촉진

- 세계의 자동차 생산 대수 증가와 파크의 회춘

- 승용차에서 가솔린 직분사 엔진 수요 증가

- 신흥 시장에서 소형 상용차 판매 증가

- 전동 연료 펌프에 스마트 진단 기능의 통합

- 내부식성 라인을 필요로 하는 합성 연료/바이오연료 혼합 연료의 급증

- 시장 성장 억제요인

- 전기자동차의 급성장에 의한 내연 기관차의 점유율 저하

- 연료 시스템 부품의 원재료 가격 변동

- 증발 방출 규제 강화로 시스템 비용 상승

- 반도체 부족에 의한 전자 펌프 컨트롤러의 혼란

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액, 달러)

- 컴포넌트별

- 연료 펌프

- 연료 인젝터

- 연료 레일

- 연료 압력 조절기

- 연료 필터

- 연료 라인 호스

- 기타

- 차종별

- 승용차

- 해치백

- 세단

- 스포츠카 및 쿠페

- SUV 및 크로스오버

- 상용차

- 소형 상용차(LCV)

- 중대형 상용차(MCV 및 HCV)

- 승용차

- 연료 유형별

- 가솔린

- 디젤

- 플렉스 연료(E10-E85)

- CNG 및 LPG

- 바이오연료 및 합성연료

- 수소

- 공급방법별

- 포트 연료 분사

- 가솔린 직분사

- 리턴리스 연료 시스템

- 커먼 레일식 디젤 분사

- 유통 채널별

- OEM(공장 설치)

- 애프터마켓(교환)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 아시아태평양의 기타 국가

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- Delphi Technologies(BorgWarner)

- Magna International Inc.

- TI Fluid Systems plc(TI Automotive)

- Toyoda Gosei Co., Ltd.

- Ucal Fuel Systems Ltd.

- Marelli Holdings Co., Ltd.

- Hitachi Astemo Ltd.

- Stanadyne LLC

- Carter Fuel Systems LLC

- Aisin Corporation

- Valeo SA

- MS Motorservice International GmbH(Pierburg)

- Walbro LLC

- Johnson Electric Holdings Ltd.

- Woodward, Inc.

제7장 시장 기회와 전망

- 화이트 스페이스와 미충족 요구 평가

The automotive fuel delivery system market size stood at USD 5.13 billion in 2025 and is forecast to reach USD 6.74 billion by 2030, advancing at a 5.61% CAGR.

The growth trajectory reflects the sector's ability to meet tougher emission limits while staying relevant in an era of rising electrification. Euro 7 rules that apply from July 2025 and the EPA Phase 3 standards, effective 2027, are pushing automakers toward high-precision injection modules and corrosion-resistant lines, sustaining capital expenditure on modern internal-combustion (ICE) architectures. Suppliers adopt "technology-neutral" portfolios that keep ICE value streams alive yet prepare for plug-in and fuel-cell demand shifts, limiting downside risk for the automotive fuel delivery system market.

Global Automotive Fuel Delivery System Market Trends and Insights

Stringent Emission Norms Driving Advanced Fuel-Delivery Modules

Euro 7 tightens particulate and NOx thresholds for all light-duty engines from November 2026, while EPA Phase 3 slashes NOx to 35 mg/hp-hr for heavy trucks in 2027 . Automakers are therefore standardizing high-pressure pumps and gasoline particulate filters across global platforms. Durability requirements rise to 160,000 km, pushing suppliers to develop long-life injectors and corrosion-proof rails, factors that underpin the automotive fuel delivery system market through 2030.

Rising Global Vehicle Production and Parc Rejuvenation

Light-vehicle output rebounded in 2025, and replacement cycles shortened as average fleet age passed 12 years in Europe, reinforcing component demand for the automotive fuel delivery system market. Vehicle-makers localize plants in India, Indonesia, and Mexico, creating regional sourcing pull for tier-1 suppliers. Fleet operators refresh hardware to meet fuel-economy benchmarks, prolonging ICE relevance despite EV penetration.

Rapid Growth of Electric Vehicles Reducing ICE Share

China and California are accelerating toward full zero-emission mandates by 2035. EV momentum is cutting ICE-linked profit pools by an anticipated 50% this decade. Fuel pumps and injectors are absent from battery platforms, creating long-run headwinds, yet regional differences keep the automotive fuel delivery system market relevant in heavy-duty, rural, and developing-country segments.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Gasoline Direct-Injection Engines in Passenger Cars

- Increasing Sales of Light Commercial Vehicles

- Volatility in Raw-Material Prices for Fuel-System Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel pumps generated 37.81% revenue of the automotive fuel delivery system market in 2024 and remain indispensable across all engine sizes, anchoring the automotive fuel delivery system market. Their ubiquity provides steady volumes even as electrification advances. Accelerating fastest, injectors will rise at 7.14% CAGR to 2030 on the back of 2,200 psi GDI requirements, pushing "smart" tip designs and stainless-steel rails for ethanol blends.

Component upgrades now emphasize on-board diagnostics, remote pressure sensing, and over-the-air firmware that cuts unplanned downtime. Biofuel growth lifts demand for corrosion-resistant lines and filters, while vapor-recovery valves and tank-mounted sensors add incremental electronics value. Together, these shifts keep the automotive fuel delivery system market size for components on an upward curve despite future EV displacement threats.

Passenger cars delivered 64.33% of the automotive fuel delivery system market revenue in 2024. Hatchbacks and sedans require cost-efficient returnless pumps, whereas SUVs integrate higher-pressure rails because of increased torque loads. Light commercial vehicles, forecast at 6.23% CAGR, prefer robustness over efficiency, sustaining steel-braid hoses and replaceable filters, a pattern that enlarges the automotive fuel delivery system market share commanded by commercial platforms.

Longer daily mileage and fleet telematics open retrofitting business, while medium and heavy trucks, though smaller in volume, retain high-flow diesel injection rails that stabilize volumes until battery densities permit long-haul substitution. As such, the automotive fuel delivery system market remains diversified across duty cycles.

The Automotive Fuel Delivery System Market Report is Segmented by Component (Fuel Pump, Fuel Injector, and More), Vehicle Type (Passenger Cars, and Commercial Vehicles), Fuel Type (Gasoline, Diesel, and More), Delivery Method (Port Fuel Injection, Gasoline Direct Injection, and More), Distribution Channel (OEM (Factory-Fitted) and Aftermarket (Replacement)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 38.55% of the automotive fuel delivery system market's 2024 turnover and will outpace all other regions with a 6.92% CAGR to 2030, owing to China's outsized production, India's highway expansion, and ASEAN's localized assembly clusters. Chinese OEMs are building fuel-system subsystems in Thailand and Indonesia to bypass tariffs and shorten logistics chains, strengthening the automotive fuel delivery system market across Southeast Asia. Semiconductor joint ventures in Japan also secure microcontroller flow for high-pressure pumps, buffering regional supply risk.

North America remains technology-rich, driven by EPA regulations that mandate 0.035 g/b-hp-hr NOx by 2027. Investments such as the USDA's USD 26 million E15 infrastructure program expand biofuel uptake, creating niche demand for ethanol-ready rails and seals that enlarge the automotive fuel delivery system market. Mexico's attractively priced labor and USMCA trade benefits encourage tier-1s to add capacity in Ramos Arizpe and Aguascalientes.

Europe faces the twin pressures of Euro 7 and accelerated carbon-neutrality pledges. OEMs are retrofitting particulate filters and vapor-containment hardware ahead of 2026, raising per-vehicle bill-of-materials but sustaining supplier order books. Eastern European plants offer lower costs for line assemblies, ensuring competitiveness even as Western European factories pivot to electric modules. Hydrogen corridor pilots from Spain to Germany are also giving the automotive fuel delivery system market an early foothold in fuel-cell applications.

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- Delphi Technologies (BorgWarner)

- Magna International Inc.

- TI Fluid Systems plc (TI Automotive)

- Toyoda Gosei Co., Ltd.

- Ucal Fuel Systems Ltd.

- Marelli Holdings Co., Ltd.

- Hitachi Astemo Ltd.

- Stanadyne LLC

- Carter Fuel Systems LLC

- Aisin Corporation

- Valeo SA

- MS Motorservice International GmbH (Pierburg)

- Walbro LLC

- Johnson Electric Holdings Ltd.

- Woodward, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent emission norms driving adoption of advanced fuel-delivery modules

- 4.2.2 Rising global vehicle production and parc rejuvenation

- 4.2.3 Growing demand for gasoline direct-injection engines in passenger cars

- 4.2.4 Increasing sales of light commercial vehicles in emerging markets

- 4.2.5 Integration of smart diagnostics within electric fuel pumps

- 4.2.6 Surge in synthetic/bio-fuel blends requiring corrosion-resistant lines

- 4.3 Market Restraints

- 4.3.1 Rapid growth of electric vehicles reducing ICE share

- 4.3.2 Volatility in raw-material prices for fuel-system components

- 4.3.3 Tightening evaporative-emission norms raising system cost

- 4.3.4 Semiconductor shortages disrupting electronic pump controllers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Fuel Pump

- 5.1.2 Fuel Injector

- 5.1.3 Fuel Rail

- 5.1.4 Fuel Pressure Regulator

- 5.1.5 Fuel Filter

- 5.1.6 Fuel Line and Hoses

- 5.1.7 Others

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.1.1 Hatchback

- 5.2.1.2 Sedan

- 5.2.1.3 Sports Car and Coupe

- 5.2.1.4 SUV and Crossover

- 5.2.2 Commercial Vehicles

- 5.2.2.1 Light Commercial Vehicles (LCV)

- 5.2.2.2 Medium and Heavy Commercial Vehicles (MCV and HCV)

- 5.2.1 Passenger Cars

- 5.3 By Fuel Type

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.3.3 Flex Fuel (E10-E85)

- 5.3.4 CNG and LPG

- 5.3.5 Biofuel and Synthetic Fuel

- 5.3.6 Hydrogen

- 5.4 By Delivery Method

- 5.4.1 Port Fuel Injection

- 5.4.2 Gasoline Direct Injection

- 5.4.3 Returnless Fuel Systems

- 5.4.4 Common-Rail Diesel Injection

- 5.5 By Distribution Channel

- 5.5.1 OEM (Factory-fitted)

- 5.5.2 Aftermarket (Replacement)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Nigeria

- 5.6.5.6 Egypt

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 DENSO Corporation

- 6.4.4 Delphi Technologies (BorgWarner)

- 6.4.5 Magna International Inc.

- 6.4.6 TI Fluid Systems plc (TI Automotive)

- 6.4.7 Toyoda Gosei Co., Ltd.

- 6.4.8 Ucal Fuel Systems Ltd.

- 6.4.9 Marelli Holdings Co., Ltd.

- 6.4.10 Hitachi Astemo Ltd.

- 6.4.11 Stanadyne LLC

- 6.4.12 Carter Fuel Systems LLC

- 6.4.13 Aisin Corporation

- 6.4.14 Valeo SA

- 6.4.15 MS Motorservice International GmbH (Pierburg)

- 6.4.16 Walbro LLC

- 6.4.17 Johnson Electric Holdings Ltd.

- 6.4.18 Woodward, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment