|

시장보고서

상품코드

1836575

항비만제 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anti-obesity Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

항비만제 시장의 2025년 시장 규모는 259억 3,000만 달러, 2030년에는 1,009억 7,000만 달러로 성장하여 CAGR 31.24%로 확대될 것으로 예측됩니다.

성장의 축이 되는 것은 GLP-1 수용체 작용제가 초래하는 극적인 효능의 향상, 만성 질환으로서의 비만에 대한 인식 증가, 고소득 국가에서의 보상 확대에 중점을 둡니다. 파이프라인의 급속한 진전에 의해 개발 기간이 단축되는 한편, 주사제에 필적하는 유효성이 기대되는 경구제나 다중 작용제 제형에 대한 투자가 진행되고 있습니다. 제조업체 각 사는 왕성한 수요를 전망해 생산 능력을 확대하고 있지만, 단기적인 공급 부족은 지속되고 있습니다. 대기업은 라이프사이클의 연장으로 점유율을 지키고, 중소의 바이오테크놀러지 기업은 신규 메커니즘으로 화이트 스페이스의 기회를 모색함에 따라 경쟁이 치열해지고 있습니다.

세계 항비만제 시장 동향과 통찰

비만과 관련 합병증의 높은 부담

1990년 이후 비만의 유병률은 두 배로 증가했으며, 2024년에는 5세 미만의 어린이 3,500만 명이 과체중이었습니다. World Obesity Atlas는 2035년까지 7억 5,000만 명 이상의 어린이들이 과체중이나 비만과 공존할 것으로 예상하고 있습니다. 고혈압은 비만이 있는 노인의 89.4%에 영향을 미치며 연간 지출은 1,310억 달러에 이릅니다. 충족되지 않은 필요의 규모는 약물 채택을 가속화하고 있으며, 특히 심혈관 위험 감소 데이터가 약리학적 개입을 뒷받침하고 있습니다.

혁신적 의약품의 연구개발 이니셔티브 증가

2025년에는 116개 이상의 화합물이 임상 개발 중이며 2023년 대비 30% 증가했습니다. REDEFINE 1 시험 novonordisk.com에서 22.7%의 체중 감소를 기록한 CagriSema와 52주째 최대 20%의 체중 감소를 달성한 MariTide 등의 이중 및 삼중 작용 프로그램에서 비롯됩니다. 초점은 2상 시험에서 최대 14.7%의 체중 감소를 기록한 올포글리프론과 같은 경구 GLP-1 제형으로 옮겨졌습니다. 벤처 기업의 자금 조달과 전략적 라이선싱 계약은 차세대 메커니즘에 대한 신뢰를 뒷받침합니다.

높은 치료비로 인해 접근 장벽이 생깁니다.

미국에서는 주요 GLP-1 작용제의 1개월당 치료비는 1,000달러에 가깝습니다. 주 메디케이드 시스템 중 적어도 하나의 비만 치료제는 21%에 불과하며 제한이 없는 접근은 15% 이하입니다. 경제 모델링에 따르면 널리 보급되는 경우 연간 시스템 비용은 1,000억 달러를 초과할 수 있습니다. 또한 저소득국가에서는 경제적 격차가 크고 비만의 유병률이 상승하고 있음에도 불구하고 비만치료제의 보급이 방해되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 환자의 의식이 증가하고 비 수술적 선택으로 이동

- 공공 및 민간 혜택 프로그램 확대

- 규제상의 장애물과 안전에 대한 우려가 확대를 막기 위해

부문 분석

말초 작용제는 2024년 매출의 60.10%를 차지하며, 확립된 안전성과 중추신경계에 대한 노출의 낮음에 지지되고 있습니다. 그러나 장관 호르몬 인크레틴은 CAGR 33.15%에서 가장 빠르게 성장하고 있으며 항 비만 약물 시장의 다른 유형을 능가합니다. GLP-1 아날로그는 평균 15-22.5%의 체중 감소를 가져오고, 이에 대해 옛 치료제는 한 자리대입니다. 이중 작용제와 트리플 작용제의 전략은 상보적인 경로를 활용하여 포만감과 에너지 소비를 증가시키고 효능을 비만 수술 영역으로 밀어 올립니다.

효능의 격차가 확대됨에 따라 높은 가격 설정에도 불구하고 의사는 인크레틴을 강하게 선호합니다. 제조업체는 소화기계의 부작용을 줄이고 치료 기간을 연장하기 위해 디지털 코칭을 번들로 제공합니다. GIP/GLP-1/글루카곤 트리아고니스트 등의 신규 진입이 진행됨에 따라 장 호르몬 기반으로 하는 항비만제 시장 규모는 2030년까지 700억 달러 이상에 달할 것으로 예측됩니다. 경쟁의 심각성은 반응의 지속성, 심혈관계에 대한 유익성의 주장, 전달의 혁신성 등을 차별화할 수 있는지 여부에 달려 있습니다.

처방약은 2024년에 84.20%의 점유율을 차지했고, CAGR은 32.56%를 나타내고, 앞으로도 주도권을 유지할 것입니다. 임상의는 복용량 증가를 관리하고 심장 대사계 마커를 모니터링하고 보조 생활 습관 프로그램을 조정하며 의학적 모니터링을 강화합니다. SURMOUNT-1에서 틸제파티드 15mg은 참가자의 3분의 1로 체중을 25% 감소시켜 의사 주도형 치료의 임상적 근거를 강조했습니다.

시판되고 있는 제제는 오를리스타트 제네릭과 식이섬유를 주성분으로 하는 보충제에 한정되어 있어 유효성과 내약성의 점에서 불충분합니다. 다제 병용 요법이 승인됨에 따라 라벨 표시의 복잡성과 위험 관리 프로그램은 처방약 우위를 더욱 견고하게 만들 것입니다. 그러나 개인화된 영양 앱과 번들된 OTC 보조 식품에 대한 소비자의 틈새는 작지 않으며, 항비만제 업계에 약간의 다각화가 이루어지고 있습니다.

지역별 분석

북미는 2024년 매출액의 65.90%를 차지했으며, 40.3%의 성인 비만증에 지지되고 있습니다. FDA에 의한 세마글루티드의 심혈관 위험에 대한 적응은 지불자의 수용을 확대하고, 정책 지침 초안은 상환의 추가 확대를 시사합니다. 이 지역의 견고한 전문가 네트워크는 새로운 약물의 도입을 가속화하고 장기적인 상환 결정에 필수적인 실제 임상 증거 창출을 지원합니다.

아시아태평양은 CAGR 33.65%로 가장 빠르게 성장하는 지역입니다. 가처분 소득 증가, 도시 지역의 식생활, 좌식 라이프 스타일이 비만 발생에 박차를 가하고 있습니다. 2024년 경제 연구에 따르면 비만 관련 의료비는 인도에서 233억 달러, 태국에서 102억 달러로 추정되며, 체중이 10% 감소하면 각각 30억 달러, 22억 달러를 절약할 수 있습니다. 각국 정부는 약물 치료를 비감염성 질환 전략에 통합하여 승인과 현지 생산을 가속화하고 있습니다.

유럽에서는 이질적인 상환에도 불구하고 큰 판매량을 유지하고 있습니다. EMA는 2022년 Wegovy를, 같은 해 Mounjaro를 승인했지만 국가 수준의 접근은 다양합니다. 중부 및 동유럽 시장은 일반적으로 2형 당뇨병으로의 상환을 제한하고 있으며, 성장 가능성을 제한하고 있습니다. 장기적인 심혈관 데이터와 의료 경제 모델에 따라 지불자의 자세가 변화하고 항비만제 시장에 새로운 업사이드가 생길 수 있습니다.

중동과 아프리카, 남미는 여전히 초기 단계이지만 유망합니다. 도시화와 패스트푸드의 보급이 두 자릿수 비만 증가를 이끌고 있습니다. 전문의의 수가 제한되어 있고, 지불자의 예산이 한정되어 있는 것, 공급 체인의 제약이 있는 것이, 단기적인 보급의 방해가 되고 있습니다. 라틴아메리카에서는 고소득 걸프 국가와 민간 보험 분야에 전략적으로 집중함으로써 공공 부문의 광범위한 참여에 앞서 조기 보급을 기대할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 좌식 라이프 스타일 증가에 의한 비만과 거기에 관련되는 합병증의 고부담

- 혁신적 의약품의 연구개발 이니셔티브 증가

- 환자 의식의 높아짐과 외과 수술 이외의 치료법으로의 전환

- 공적기관 및 민간단체에 의한 복리후생 프로그램의 이니셔티브의 고조

- 차세대 경구 GLP-1 수용체 작용제의 상업화의 가속

- 의료용 항비만제의 고용주 부담의 디지털 체중 관리 플랫폼 및 원격 의료 서비스에의 통합

- 시장 성장 억제요인

- 높은 치료비와 한정된 상환액

- 안전성과 부작용에 따른 규제상의 과제

- 대체요법의 가용성과 장기적인 비용효과에 대한 우려

- 복잡한 펩티드 원약의 제조 능력의 병목

- 가치/공급망 분석

- 규제와 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 작용기전별

- 말초성 작용제

- 중추작용약

- 장 호르몬 억제제

- 약물 유형별

- 처방약

- 일반 의약품

- 투여 경로별

- 경구

- 주사제

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 체중 감량 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Novo Nordisk A/S

- Eli Lilly and Company

- F. Hoffmann-La Roche AG

- Pfizer Inc.

- GSK plc

- Currax Pharmaceuticals LLC

- Boehringer Ingelheim Intl. GmbH

- Amgen Inc.

- AstraZeneca plc

- Merck & Co., Inc.

- Bayer AG

- Takeda Pharmaceutical Co. Ltd

- Rhythm Pharmaceuticals, Inc.

- Vivus LLC

- Zydus Lifesciences Ltd.

- Gelesis Holdings Inc.

- Teva Pharmaceuticals Company Limited

- Hanmi Pharm.Co.,Ltd.

- Verdiva

- HK inno.N Corp.

제7장 시장 기회와 전망

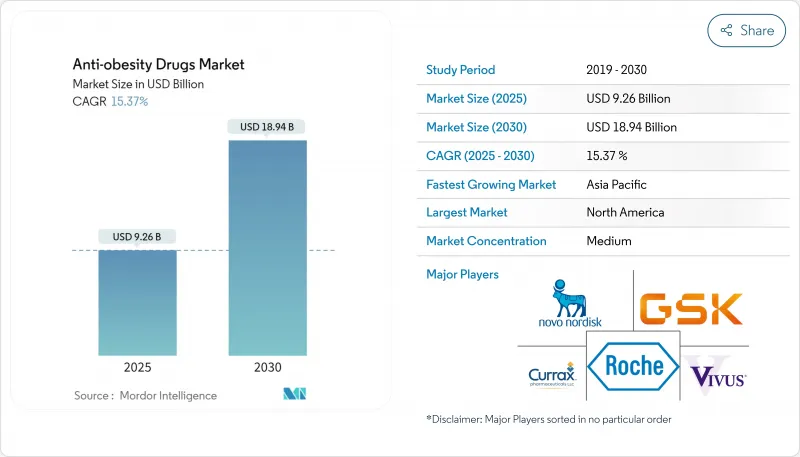

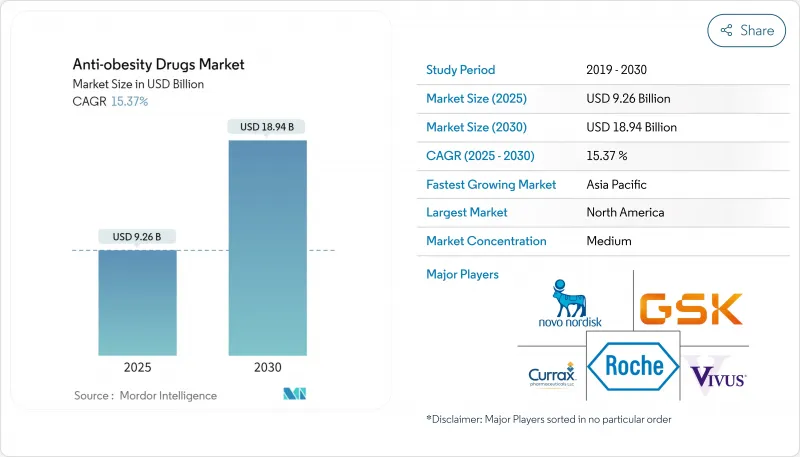

SHW 25.10.28The anti-obesity drugs market is valued at USD 25.93 billion in 2025 and is forecast to grow to USD 100.97 billion by 2030, advancing at a 31.24% CAGR.

Growth pivots on the dramatic efficacy gains delivered by GLP-1 receptor agonists, increasing recognition of obesity as a chronic disease, and expanding reimbursement in high-income countries. Rapid pipeline progress is shortening development timelines, while investment is flowing into oral and multi-agonist formulations that promise comparable efficacy to injectables. Manufacturers are scaling capacity in anticipation of strong demand, yet near-term supply tightness persists. Competition is sharpening as large firms defend share with lifecycle extensions and smaller biotechs seek white-space opportunities in novel mechanisms.

Global Anti-obesity Drugs Market Trends and Insights

High burden of obesity and related comorbidities

Escalating prevalence has doubled since 1990, and 35 million children under 5 were overweight in 2024. The World Obesity Atlas projects more than 750 million children will live with overweight or obesity by 2035. Comorbid conditions amplify the clinical and financial imperative: hypertension affects up to 89.4% of older adults with obesity, adding USD 131 billion to annual spending. The scale of unmet need is accelerating drug adoption, particularly where cardiovascular risk reduction data now support pharmacologic intervention.

Increasing R&D initiatives for innovative drugs

More than 116 compounds were in clinical development in 2025, a 30% increase versus 2023. Momentum stems from dual- and triple-agonist programs such as CagriSema, which recorded 22.7% weight loss in the REDEFINE 1 trial novonordisk.com, and MariTide, which achieved up to 20% weight loss at week 52. The focus is shifting toward oral GLP-1 agents like orforglipron, registering up to 14.7% weight loss in Phase II data. Venture funding and strategic licensing deals underscore confidence in next-generation mechanisms.

High treatment cost creates access barriers

Monthly therapy costs of leading GLP-1 agonists near USD 1,000 in the United States. Only 21% of state Medicaid plans cover at least one obesity medication, and unrestricted access is below 15%. Economic modeling shows annual system costs could surpass USD 100 billion if widespread uptake occurs. Affordability gaps are wider in low-income countries, dampening uptake despite rising obesity prevalence.

Other drivers and restraints analyzed in the detailed report include:

- Increased patient awareness and shift toward non-surgical options

- Growing public and private benefit programs

- Regulatory hurdles and safety concerns impede expansion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peripherally acting drugs contributed 60.10% of 2024 revenue, underpinned by established safety and lower CNS exposure. Yet gut-hormone incretins are growing fastest at a 33.15% CAGR, outpacing every other class in the anti-obesity drugs market. GLP-1 analogs deliver 15-22.5% average weight reductions compared with single-digit results from older therapies. Dual- and triple-agonist strategies leverage complementary pathways to amplify satiety and energy expenditure, pushing efficacy toward bariatric-surgery territory.

The widening efficacy gap drives strong physician preference for incretins despite premium pricing. Manufacturers are bundling digital coaching to mitigate gastrointestinal side effects and extend time on therapy. As new entrants such as GIP/GLP-1/glucagon tri-agonists progress, the anti-obesity drugs market size for gut-hormone-based products is expected to exceed USD 70 billion by 2030. Competitive intensity will hinge on differentiating durability of response, cardiovascular benefit claims, and delivery innovations.

Prescription products held 84.20% share in 2024 and will sustain leadership with a projected 32.56% CAGR. Clinicians manage dose titration, monitor cardiometabolic markers, and coordinate adjunct lifestyle programs, reinforcing medical oversight. In SURMOUNT-1, tirzepatide 15 mg delivered 25% body-weight reduction for one-third of participants, underscoring the clinical rationale for physician-directed therapy.

Over-the-counter formulations remain limited to orlistat generics and fiber-based supplements that underperform on efficacy and tolerability. As multi-agonists gain approval, labeling complexity and risk-management programs will further entrench prescription dominance. However, a small consumer niche persists for OTC aids bundled with personalized nutrition apps, creating modest diversification in the anti-obesity drugs industry.

The Anti-Obesity Drugs Market Report is Segmented by Mechanism of Action (Peripherally Acting Drugs, Centrally Acting Drugs, and Gut Hormone Incretins), Drug Type (Prescription Drugs and OTC Drugs), Route of Administration (Oral and Injectable), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography (North America, Europe, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 65.90% of 2024 revenue, supported by 40.3% adult obesity prevalence. The FDA's cardiovascular-risk indication for semaglutide broadens payor acceptance, and draft policy guidance signals further reimbursement expansion. The region's robust specialist network accelerates uptake of novel agents and supports real-world evidence generation critical for long-term reimbursement decisions.

Asia-Pacific is the fastest-growing region at a 33.65% CAGR. Rising disposable income, urban diets, and sedentary lifestyles fuel obesity incidence. A 2024 economic study estimated obesity-related medical outlays at USD 23.3 billion in India and USD 10.2 billion in Thailand, with potential savings of USD 3.0 billion and USD 2.2 billion respectively from a 10% weight reduction. Governments are integrating pharmacotherapy into non-communicable disease strategies, accelerating approvals and localized manufacturing.

Europe maintains significant volume despite heterogeneous reimbursement. The EMA cleared Wegovy in 2022 and Mounjaro the same year, yet country-level access varies. Central and Eastern European markets generally restrict reimbursement to type 2 diabetes, limiting growth potential. Long-term cardiovascular data and health-economic models could shift payer stances, creating incremental upside for the anti-obesity drugs market.

Middle East and Africa and South America remain nascent but promising. Urbanization and fast-food proliferation are driving double-digit obesity growth. Limited specialist density, restricted payor budgets, and supply chain constraints cap near-term penetration. Strategic focus on high-income Gulf states and private insurance segments in Latin America may unlock earlier adoption ahead of broader public-sector engagement.

- Novo Nordisk

- Eli Lilly and Company

- Roche

- Pfizer

- GlaxoSmithKline

- Currax Pharmaceuticals

- Boehringer Ingelheim Intl. GmbH

- Amgen

- AstraZeneca

- Merck

- Bayer

- Takeda Pharmaceuticals

- Rhythm Pharmaceuticals, Inc.

- Vivus LLC

- Zydus Lifesciences Ltd.

- Gelesis Holdings Inc.

- Teva Pharmaceuticals Company Limited

- Hanmi Pharm.Co.,Ltd.

- Verdiva

- HK inno.N Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Burden of Obesity and Realted Comorbidities Due to Growing Sedentary Lifestyle

- 4.2.2 Increasing Research and Development Initiatives for Innovative Drugs

- 4.2.3 Increased Patient Awarness and Shift Towards Non Surgical Treatment Options

- 4.2.4 Growing Inititaives Taken By Public and Private Organizations for Benefit Programs

- 4.2.5 Accelerated commercialization of next-generation oral GLP-1 receptor agonists

- 4.2.6 Integration of prescription anti-obesity drugs into employer-sponsored digital weight-management platforms and telehealth services

- 4.3 Market Restraints

- 4.3.1 High Treatment Cost and Limited Reimbursement

- 4.3.2 Regulatory Cahllenges Coupled with Safety and Side Effects

- 4.3.3 Availability of Alternative Therapies and Long-Term Cost Effectiveness Concerns

- 4.3.4 Manufacturing-capacity bottlenecks for complex peptide APIs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory andTechnological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value -USD)

- 5.1 By Mechanism of Action

- 5.1.1 Peripherally Acting Drugs

- 5.1.2 Centrally Acting Drugs

- 5.1.3 Gut-Hormone Incretins

- 5.2 By Drug Type

- 5.2.1 Prescription Drugs

- 5.2.2 OTC Drugs

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Injectable

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Weight-Loss Clinics

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Novo Nordisk A/S

- 6.4.2 Eli Lilly and Company

- 6.4.3 F. Hoffmann-La Roche AG

- 6.4.4 Pfizer Inc.

- 6.4.5 GSK plc

- 6.4.6 Currax Pharmaceuticals LLC

- 6.4.7 Boehringer Ingelheim Intl. GmbH

- 6.4.8 Amgen Inc.

- 6.4.9 AstraZeneca plc

- 6.4.10 Merck & Co., Inc.

- 6.4.11 Bayer AG

- 6.4.12 Takeda Pharmaceutical Co. Ltd

- 6.4.13 Rhythm Pharmaceuticals, Inc.

- 6.4.14 Vivus LLC

- 6.4.15 Zydus Lifesciences Ltd.

- 6.4.16 Gelesis Holdings Inc.

- 6.4.17 Teva Pharmaceuticals Company Limited

- 6.4.18 Hanmi Pharm.Co.,Ltd.

- 6.4.19 Verdiva

- 6.4.20 HK inno.N Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment