|

시장보고서

상품코드

1836595

독일의 약물전달 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Germany Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

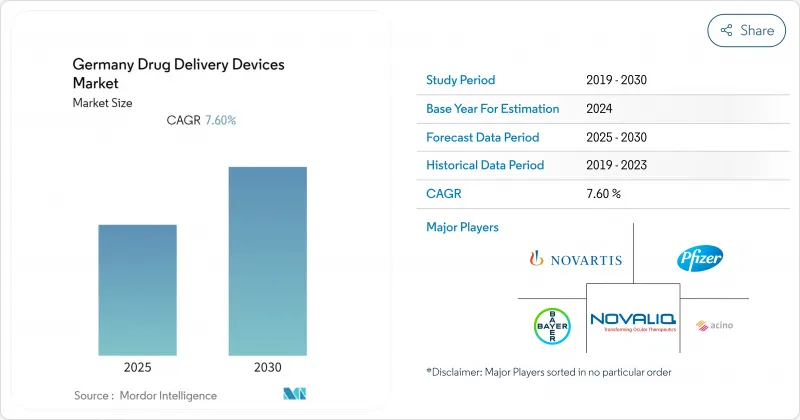

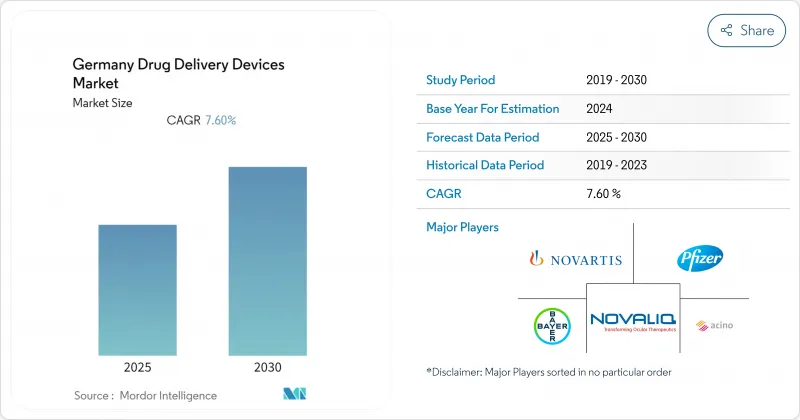

독일의 약물전달 기기 시장은 2025년에 104억 5,000만 달러, 2030년에는 159억 달러에 이를 것으로 예측되며, CAGR은 8.75%를 나타낼 전망입니다.

지속적인 성장은 광범위한 법정 건강보험 보장 범위, 고부가가치 주사기 및 오토인젝터 분야의 탄탄한 제조 기반, 그리고 정밀 투여 기술을 필요로 하는 생물의약품 파이프라인의 확대에서 비롯된 것입니다. 높은 당뇨병 이환율, 암 부담 증가, 충실한 병원망에 의해 독일에서는 주사기에 대한 수요가 계속 증가하고 있는 한편, 재택치료에의 급속한 전환과 지속가능성의 목표에 의해 접속 가능하고 재이용 가능한 포맷에의 공간이 열리고 있습니다. 2025년에 도입된 EU 전역에서의 공동 임상 평가, 국내에서의 고속 트랙 패스웨이, 실시간 디지털 어드히어런스 툴은 출시까지의 기간을 단축하고 차세대 기기의 보급을 뒷받침합니다.

독일 약물전달 기기 시장 동향과 통찰

만성 질환과 감염증의 높은 유병률과 발병률

독일에서는 당뇨병(8.4%), 심혈관 질환(6.8%), 만성 호흡기 질환(11.4%)의 유병률이 EU 평균을 웃돌고 있습니다. 이러한 만성 질환은 충격과 결과를 개선하는 고급 주사기, 인슐린 펜, 스마트팜프 및 서방형 임플란트의 안정적인 수요를 이끌고 있습니다. 당뇨병만으로도 2040년까지 1,090만-1,420만명의 독일인이 이환될 것으로 예측되고 있으며, 자동 인슐린 전달 생태계의 지속적인 업그레이드를 추진하고 있습니다. 독일암 연구센터에서 개발 중인 마이크로 나노 로봇은 전신 독성을 억제하면서 종양 부위에의 흡수를 높이는 것을 목적으로 하고 있습니다. 질병 동향과 연구의 획기적인 결합이 독일 약물전달 기기 시장은 혁신 주도의 궤도를 유지하고 있습니다.

재택건강의 동향과 고령화의 진전

65세 이상의 노인은 2023년 인구의 21%에서 2050년에는 30% 가까이 증가할 것으로 예상됩니다. 동시에 장기 간호가 필요한 사람은 2050년까지 1,400만 명으로 증가할 수 있습니다. 이러한 변화는 전문가가 아니더라도 가정 내에서 안전하게 사용할 수 있는 장비의 필요성을 높이고 있습니다. Gerresheimer사의 Gx SensAir(R)와 같은 체내 주사기는 단일 클론 항체의 주 1회 피하 투여를 임상 방문 없이 가능하게 하고, 이동과 관련된 배출을 감소시키고, 간병인의 부담을 경감시킵니다. 소비자가 원격 의료 플랫폼에 익숙해지면 어드히어런스 대시보드를 통합한 커넥티드 흡입기, 펜, 패치의 보급이 더욱 가속화되어 독일의 약물전달 기기 시장의 기세가 강해집니다.

엄격한 규제 요건 및 제품 리콜

독일에서는 의료기기법 시행법과 함께 EU 의료기기 규제(MDR)가 시행되고 있습니다. 그 결과, 비용 상승과 리콜 책임이 중소기업에 가장 큰 부담이 되며, 때로는 발매가 일시 정지되어 독일의 약물전달 기기 시장의 성장 곡선이 깎일 수도 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 바이오시밀러 및 생물제제 제품의 혁신과 개발에 대한 투자 증가

- 신속한 승인과 상환을 지원하는 정부의 이니셔티브

부문 분석

주사용 기기는 2024년에 전체 매출의 43.45%를 차지해 독일의 약물전달 기기 시장 규모에서 그 역할을 확고히 하고 있습니다. 지속적인 수요는 신약 승인에서 우위를 차지하는 생물학적 제제 치료와 임상 의사 사이에서 비경구적 정확도가 계속 선호되고 있기 때문입니다. SCHOTT Pharma의 고분자 주사기와 유리 주사기의 생산 능력 급증은 업계의 자신감을 뒷받침합니다.

이식 가능한 펌프, 마이크로칩, 생체 흡수성 저장소는 CAGR 10.24%로 가장 빠르게 성장하고 있습니다. 환자 친화적인 흡입기는 만성 호흡기 질환의 국민적 부담이 큰 가운데 점유율을 유지하고, 경피 흡수형 패치는 호르몬과 통증 관리를 위해 단계적으로 채택되고 있습니다. 독일의 약물전달 기기 시장에서 범주에 관계없이 내장형 연결 기능은 복용 기록과 피드백 루프를 강화하여 복약 준수와 데이터 주도 관리 경로를 개선하고 있습니다.

주사제 전달은 백신과 고분자 의약품의 정맥내, 피하, 근육내 투여 경로에 대한 임상의의 신뢰를 반영하여 2024년 매출의 49.67%를 유지했습니다. 이 비율은 독일의 약물전달 시장 점유율을 지원하며, 기동력을 낮추고 2-5mL의 용량을 지원하는 차세대 자동 주사기에 의해 강화되고 있습니다.

경피 흡수형은 마이크로니들 어레이와 무선 음향 패치가 페이로드 크기의 상한을 끌어 올려 CAGR 10.03%로 가장 급속히 확대했습니다. 구강 점막 필름은 신속한 통증 완화를 위한 견인역이 되어 흡입, 점안, 비강은 표적 국소 요법의 선택을 넓히는 동시에 독일 약물전달 기기 시장에서 실무자들이 사용할 수 있는 임상 도구 키트를 풍부하게 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 및 감염증의 높은 유병률과 발생률

- 재택 헬스 케어의 동향과 고령화의 진전

- 바이오시밀러 및 생물제제의 기술 혁신과 개발 투자 증가

- 신속한 승인과 상환을 지원하는 정부의 이니셔티브

- 기술의 진보와 디지털화

- 제조 수탁 거점의 확대

- 시장 성장 억제요인

- 엄격한 규제 요건과 제품 리콜

- G-BA의 가격 규제에 의한 혁신적 시스템에 대한 보험료의 상한 설정

- 종래 시스템 시장 포화와 환자의 컴플라이언스 및 수용성의 문제

- 마이크로플루이딕스공학 및 콤비네이션 제품공학 전문 인력의 한정된 이용가능성

- 가치/공급망 분석

- 규제와 기술적 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 기기 유형별

- 주사용 약물 전달 기기

- 흡입 전달 기기

- 주입 펌프

- 경피 패치

- 이식형 약물전달 시스템

- 안구 삽입 및 전달 임플란트

- 비강 및 구강 약물 전달 기기

- 투여 경로별

- 주사

- 흡입

- 경피

- 구강 점막(뺨측 및 설하)

- 안구

- 비강

- 용도별

- 당뇨병

- 종양

- 순환기

- 호흡기

- 중추 신경계 질환

- 감염증

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 재택치료

- 진료소 및 전문센터

- 기타

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Becton, Dickinson and Company

- Gerresheimer AG

- Ypsomed Holding AG

- Bayer AG

- Boehringer Ingelheim International GmbH

- Pfizer Inc.

- Solventum

- Phillips-Medisize LLC

- Novartis AG

- Owen Mumford Ltd

- Novo Nordisk A/S

- Medtronic plc

- West Pharmaceutical Services Inc.

- SCHOTT AG

- Haselmeier GmbH

- Sanofi SA

- Terumo Corporation

- Teva Pharmaceutical Industries Ltd.

- Vetter Pharma-Fertigung GmbH & Co. KG

- Nemera La Verpilliere SAS

제7장 시장 기회와 전망

SHW 25.10.28The Germany drug delivery devices market is valued at USD 10.45 billion in 2025 and is forecast to reach USD 15.90 billion by 2030, registering an 8.75% CAGR.

Continuous gains stem from the country's broad statutory insurance coverage, strong manufacturing base in high-value syringes and autoinjectors, and an expanding pipeline of biologics that require precise administration technologies. High diabetes prevalence, a rising cancer burden, and Germany's well-resourced hospital network keep demand for injectable systems elevated, while rapid shifts toward home-based care and sustainability goals are opening space for connected, reusable formats. EU-wide joint clinical assessments introduced in 2025, domestic fast-track pathways, and real-time digital adherence tools together shorten launch timelines and support uptake of next-generation devices, even as reference-price rules temper premium options.

Germany Drug Delivery Devices Market Trends and Insights

High Prevalence and Incidence of Chronic and Infectious Diseases

Germany reports higher-than-EU-average prevalence for diabetes (8.4%), cardiovascular diseases (6.8%), and chronic respiratory diseases (11.4%). This chronic-disease load drives steady demand for advanced injectors, insulin pens, smart pumps, and sustained-release implants that improve adherence and outcomes. Diabetes alone is projected to affect 10.9-14.2 million Germans by 2040, pushing continuous upgrades in automated insulin delivery ecosystems. Oncology demand follows a similar path: micro-/nano-robots under development at the German Cancer Research Center aim to raise tumour-site uptake while cutting systemic toxicity. Together, disease trends and research breakthroughs keep the Germany drug delivery devices market on an innovation-driven trajectory.

Growing Trend of Home Healthcare and Aging Population

People aged >= 65 will rise from 21% of the population in 2023 to nearly 30% by 2050. Concurrently, those requiring long-term care could climb to 14 million by 2050. These shifts amplify the need for devices that non-professionals can use safely in domestic settings. On-body injectors such as Gerresheimer's Gx SensAir(R) allow weekly subcutaneous dosing of monoclonal antibodies without clinical visits, cutting travel-related emissions and easing caregiver burdens. Consumer familiarity with telehealth platforms further accelerates uptake of connected inhalers, pens, and patches that integrate adherence dashboards, reinforcing market momentum in Germany drug delivery devices market.

Stringent Regulatory Requirements and Product Recalls

Germany enforces EU Medical Device Regulation (MDR) alongside its Medical Device Law Implementation Act. Combination products must satisfy dual drug-device evidence packages, and higher-risk classes require third-party conformity assessments.Resulting cost spikes and recall liabilities weigh heaviest on SMEs, occasionally pausing launches and trimming the Germany drug delivery devices market growth curve.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Investment in Biosimilar and Biologics Product Innovation and Development

- Government Initiatives Supporting Fast Track Approval and Reimbursement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injectable devices represented 43.45% of all revenues in 2024, cementing their role in the Germany drug delivery devices market size. Sustained demand arises from biologic therapies that dominate new drug approvals and from continuing preference among clinicians for parenteral accuracy. SCHOTT Pharma's capacity surge in polymer and glass syringes underscores industry confidence.

Implantable pumps, micro-chips, and bioresorbable depots post the quickest gains at an 10.24% CAGR. Patient-friendly inhalers preserve share amid a high national burden of chronic respiratory illness, while transdermal patches earn incremental adoption for hormone and pain management. Across categories, embedded connectivity features enhance dose logging and feedback loops, lifting adherence and data-driven care pathways within the Germany drug delivery devices market.

Injectable delivery retained a 49.67% revenue stake in 2024, reflecting clinician trust in intravenous, subcutaneous, and intramuscular routes for vaccines and large-molecule drugs. This proportion anchors the Germany drug delivery devices market share and is bolstered by next-gen autoinjectors that lower activation force and support 2-5 mL volumes.

Transdermal formats scale fastest at a 10.03% CAGR on the back of microneedle arrays and wirelessly powered acoustic patches that raise payload size limits. Oral mucosal films gain traction for rapid pain relief, while inhaled, ocular, and nasal modalities extend options for targeted local therapy, together enriching clinical toolkits available to practitioners in the Germany drug delivery devices market.

Germany Drug Delivery Devices Market Report is Segmented by Device Type (Injectable Delivery Devices, Transdermal Patches, Infusion Pumps, and More), Route of Administration (Injectable, Inhalational, Transdermal, and More), Application (Diabetes, Oncology, Cardiovascular, and More), and End Users (Hospitals, Ambulatory Surgical Centres, Homecare Settings, and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beckton Dickinson

- Gerresheimer

- Ypsomed

- Bayer

- Boehringer Ingelheim

- Pfizer

- Solventum

- Phillips-Medisize LLC

- Novartis

- Owen Mumford

- Novo Nordisk

- Medtronic

- West Pharmaceutical Services

- SCHOTT

- Haselmeier GmbH

- Sanofi

- Terumo

- Teva Pharmaceutical Industries

- Vetter Pharma-Fertigung GmbH & Co. KG

- Nemera La Verpilliere SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence and Incidence of Chronic and Infectious Diseases

- 4.2.2 Growing Trend of Home Healthcare and Aging Population

- 4.2.3 Increasing Investment in Biosimiliar and Biologics Product Innovation and Development

- 4.2.4 Government Initiatives Supporting Fast Track Approval and Reimbursemnet

- 4.2.5 Technological Advancement and Digitalization

- 4.2.6 Expansion of Contract-Manufacturing Hubs

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Requirements and Product Recalls

- 4.3.2 G-BA Price Regulation Capping Premiums for Innovative Systems

- 4.3.3 Market Saturation in Conventional systems Coupled with Patient Compliance and Acceptance Issues

- 4.3.4 Limited Availability of Specialized Microfluidics & Combination-Product Engineering Talent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Injectable Delivery Devices

- 5.1.2 Inhalation Delivery Devices

- 5.1.3 Infusion Pumps

- 5.1.4 Transdermal Patches

- 5.1.5 Implantable Drug Delivery Systems

- 5.1.6 Ocular Inserts & Delivery Implants

- 5.1.7 Nasal & Buccal Delivery Devices

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Inhalation

- 5.2.3 Transdermal

- 5.2.4 Oral Mucosal (Buccal and Sublingual)

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.3 By Application

- 5.3.1 Diabetes

- 5.3.2 Oncology

- 5.3.3 Cardiovascular

- 5.3.4 Respiratory

- 5.3.5 Central Nervous System Disorders

- 5.3.6 Infectious Diseases

- 5.3.7 Others

- 5.4 By End-user

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Homecare Settings

- 5.4.4 Clinics and Speciality Centres

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Becton, Dickinson and Company

- 6.4.2 Gerresheimer AG

- 6.4.3 Ypsomed Holding AG

- 6.4.4 Bayer AG

- 6.4.5 Boehringer Ingelheim International GmbH

- 6.4.6 Pfizer Inc.

- 6.4.7 Solventum

- 6.4.8 Phillips-Medisize LLC

- 6.4.9 Novartis AG

- 6.4.10 Owen Mumford Ltd

- 6.4.11 Novo Nordisk A/S

- 6.4.12 Medtronic plc

- 6.4.13 West Pharmaceutical Services Inc.

- 6.4.14 SCHOTT AG

- 6.4.15 Haselmeier GmbH

- 6.4.16 Sanofi S.A.

- 6.4.17 Terumo Corporation

- 6.4.18 Teva Pharmaceutical Industries Ltd.

- 6.4.19 Vetter Pharma-Fertigung GmbH & Co. KG

- 6.4.20 Nemera La Verpilliere SAS

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment