|

시장보고서

상품코드

1836597

에피제네틱스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Epigenetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

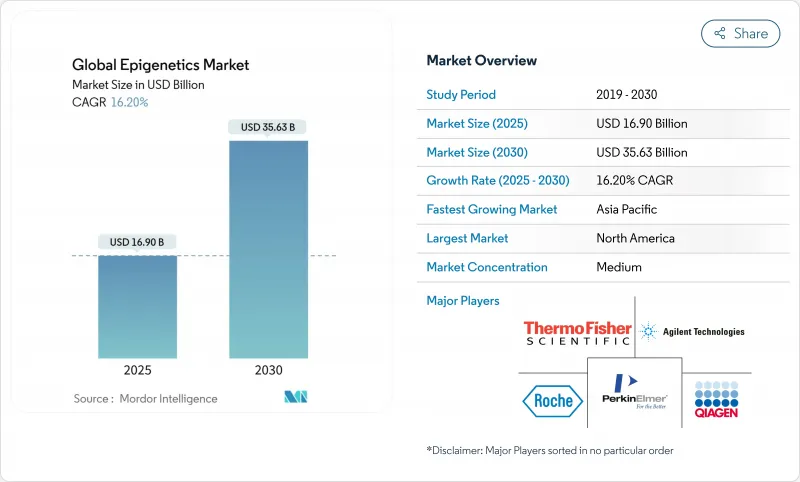

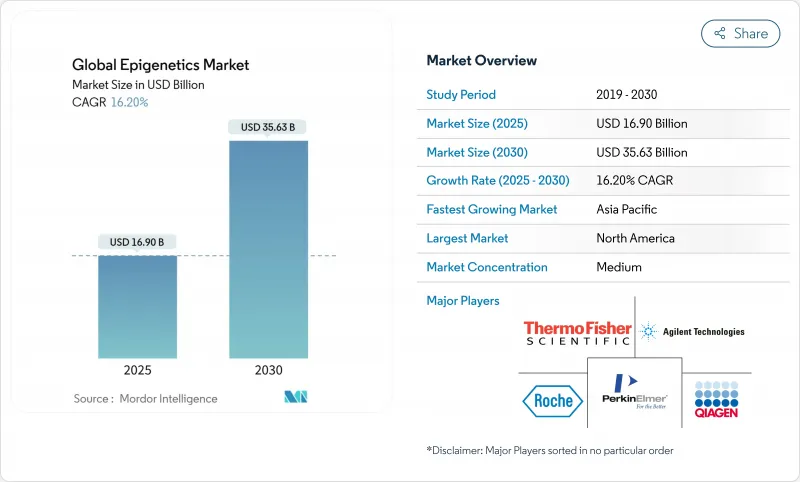

에피제네틱스 시장은 2025년에 169억 달러, 같은 기간에 16.20%의 연평균 복합 성장률(CAGR)로 성장하여 2030년에는 356억 3,000만 달러에 이를 것으로 예측됩니다.

DNA 메틸화 시그니처를 마이닝하는 인공지능 알고리즘의 진보, 복잡한 에피유전체 패턴을 매핑하는 롱 리드 시퀀싱의 획기적인 진보, 혈액 기반의 동반진단약의 규제 당국에 의한 인가의 신속화 등이 수요를 늘리기 위해 융합되고 있습니다. 에피제네틱스를 대사 및 면역파이프라인에 통합하는 제약기업과의 제휴는 가까운 미래의 상업적인 견인력을 강화합니다. 에피제네틱스 시장은 또한 싱글셀 멀티오믹스 플랫폼에 대한 지적 재산 신청의 강화로부터 혜택을 누리지만, 벤처 캐피탈의 유입은 실험실 자동화 및 클라우드 바이오인포매틱스 생태계를 가속화합니다. 북미는 계속 우세하지만 아시아태평양은 정부가 정밀의료 인프라에 보조금을 내고 현지 신규 기업이 페이퍼 유즈 시퀀싱 모델을 채택하고 있기 때문에 가장 급성장을 보여줍니다.

세계 에피제네틱스 시장 동향과 통찰

암 이환율 증가 및 정밀의료 채택

인구의 고령화에 따른 세계적인 암 이환율 증가는 환자를 계층화하고 최소 잔존 병변을 추적하는 에피제네틱스 바이오마커 수요를 촉진하고 있습니다. 일루미나의 확장된 TruSight Oncology 포트폴리오에서는 메틸화 정보를 기반으로 한 변형 콜을 보고하고 치료법 선택을 정밀화합니다. Galleri와 같은 메틸화 시그니처를 읽는 다중 암 조기 발견 혈액 검사는 연구에서 임상으로 이동하여 보다 조기 개입을 가능하게합니다. 혈액 악성 종양에서는 에피유전체-유전체 통합 프로파일링에 의해 내성 관련 아형이 확인되어 에피제네틱스유전제의 적응이 확산되고 있습니다. 메틸화 패널은 차세대 동반진단의 기초 요소로 자리매김하고 있습니다.

비 종양 영역에서 에피제네틱스 응용 확대

긴 사슬 비 코딩 RNA가 알츠하이머 병에서 신경 염증을 조절한다는 것을 보여주는 획기적인 연구는 에피제네틱스 편집의 치료 창구를 열었습니다. 노보놀 디스크와 오메가 세라퓨틱스는 비만 치료를 위해 열 발생을 조절하는 에피유전체 컨트롤러를 공동 개발하고 있습니다. 심장 대사 시스템 파이프라인은 현재 표준 지질 검사를 능가하는 유전적 에피제네틱스 위험 알고리즘을 통합하고 있습니다. DNA를 절단하지 않고 돌연변이 대립유전자를 억제하는 에피제네틱스적 재기록 도구는 헌팅턴병에 대한 초기 단계의 임상시험에 포함되어 있습니다. 이러한 분야 횡단적인 기세는 에피제네틱스 시장의 수익원을 종양학의 핵심을 넘어 다양화시킵니다.

NGS와 1분자 계측 장치의 고비용

전체 유전체 시퀀싱가 미화 100달러의 역치로 향하는 추세에도 불구하고, 종합적인 에피유전체 워크플로우는 더 높은 커버리지, 특수 라이브러리 키트 및 견고한 긴 리드 플랫폼을 필요로 하며, 샘플당 비용이 높아집니다. 예를 들어 Oxford Nanopore의 PromethIon은 고급 유체역학적 유지보수와 하이엔드 GPU를 필요로 합니다. 단일 셀 메틸롬 파이프라인은 태그화 단계, 자체 시약 및 확장된 컴퓨팅 클러스터를 추가합니다. 브라질, 남아프리카, 인도네시아에서는 감가상각비와 정기적인 서비스 계약이 임상 실험실에 부담을 주어 암 이환율이 높은 지역에서의 채택을 늦추고 있습니다. 번들리스와 재렌탈의 계획이 대두되고 있지만, 저렴한 갭을 완전히 채우기에는 이르지 않습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 멀티오믹스 연구 개발 자금의 급증과 공동 연구 컨소시엄

- 동반진단약에의 규제 지원

- 숙련된 바이오인포마티션 부족

부문 분석

시약 및 키트는 2024년 에피제네틱스 시장 점유율의 41.4%를 차지하며, 바이설파이트 전환 화학물질과 염색질 면역침전 시약의 지속적인 대량 구매에 의해 추진되었습니다. 이 장비는 5mC, 5hmC, 6mA를 직접 감지하는 긴 리드 시퀀서에 대한 수요가 증가함에 따라 2위를 차지했습니다. 한편, 바이오인포매틱스의 하위 부문은 원시 신호 데이터를 실용적인 바이오마커의 지견으로 변환하는 AI 탑재의 클라우드 파이프라인에 지지되어 2030년까지 연평균 복합 성장률(CAGR) 20.1%를 보일 것으로 예측되고 있습니다. 고급 분석 공급업체는 현재 종량제 메틸롬 파이프라인을 제공하고 중견 병원 진입 장벽을 낮추고 있습니다. 에피제네틱스 연령, 면역 상태 및 치료 반응에 대한 머신러닝 모델에 대한 새로운 특허는 에피제네틱스 시장 내 데이터 무게 중심 변화를 반영하고 프리미엄 라이선스 비용을 계속 요구하고 있습니다.

에피제네틱스 산업은 시퀀싱의 정확성이 두드러지면서 하드웨어에서 소프트웨어로의 차별화 중심으로 전환하고 있습니다. 멀티오믹스 대시보드는 메틸화, 염색질 접근성, 긴 리드 전사 제품 수를 단일 사용자 인터페이스에 통합합니다. Informatics Suite의 구독 수입은 시약 판매 증가를 능가합니다. 그 결과 장비 공급업체는 시퀀서 구매에 분석 크레딧을 번들하기 시작했습니다. 이러한 흐름을 통해 바이오인포매틱스 플랫폼은 예측 기간 후반에 매출 기여에서 소모품을 추월할 것으로 보입니다.

지역별 분석

북미는 2024년에 에피제네틱스 시장 점유율의 43.4%를 유지했으며, 이는 FDA에 의한 메틸화 정보 진단의 인가와 멀티오믹스 집단 연구를 조성하는 NIH의 자금 제공 덕분입니다. 벤처 투자자는 Tune Therapeutics의 1억 7,500만 달러의 자금 조달로 대표되는 플랫폼 신흥 기업에 전례 없는 자본을 투입하여 B형 간염 에피유전체 침묵 요법의 신속한 임상 도입 트럭을 확보했습니다. 보스턴, 샌프란시스코 및 더럼의 학술 클러스터는 이 지역의 우위를 유지하는 학제간 인력 풀을 육성하고 있습니다.

아시아태평양은 인구동태의 고령화에 의해 암 이환율이 상승하고 각국 정부가 정밀 종양학 검사의 상환을 맡기 때문에 2030년까지 연평균 복합 성장률(CAGR) 17.0%를 보일 것으로 예측됩니다. 중국이 산업 규모의 나노포어 시설에 의해 지역의 시퀀싱 능력을 지지하고 있는 한편, 일본의 전체 유전체 프로그램이 2차적인 에피유전체 해석 수요를 자극하고 있습니다. 싱가포르와 인도의 신흥기업은 현지 스크리닝 규범에 맞추어 문화적으로 조정된 전립선암 메틸화 패널을 발표하고 있습니다. 이러한 노력으로 에피제네틱스 시장은 지금까지 충분한 서비스를 받지 못한 사람들에 대한 침투를 확대하고 있습니다.

유럽은 균형 잡힌 확대를 보여줍니다. GDPR(EU 개인정보보호규정)에 준거한 데이터 페더레이션은 국경을 넘어서는 공동 분석을 늦추고 있지만, European Health Data Space 규정은 동의 조항을 조화시켜 에피유전체 엔드포인트를 통합하는 컨소시엄 시험을 해방하고 있습니다. 영국이 옥스포드 나노포어사와 2억 5,000만 파운드를 투입해, 바이오뱅크의 에피유전체 5만건을 프로파일링하는 양국간 프로젝트는 공공-민간 투자 강도를 잘 보여줍니다. 독일과 프랑스는 LSD1과 EZH2 억제제의 제약 연구를 유지하고 회원국 간의 상환 불균일성에도 불구하고 지역 에피제네틱스 시장의 참여를 증폭시키고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암 이환율 증가와 정밀의료의 채택

- 비암 영역에서의 에피제네틱스 응용 확대

- 멀티오믹스 R&D 자금 조달과 공동 연구 컨소시엄의 급증

- 동반진단약에 대한 규제 지원

- AI를 활용한 에피제네틱스 바이오마커 탐색 가속기

- 단일 셀 및 긴 리드 에피유전체학 플랫폼에 대한 벤처 투자

- 시장 성장 억제요인

- NGS 및 단일 분자 측정 장치의 고비용

- 숙련된 바이오인포마티션의 부족

- 집단 규모의 에피유전체 데이터 세트에 대한 데이터 프라이버시의 장애물

- 에피제네틱스 진단을 위한 제한된 상환 경로

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액)

- 제품별

- 기기

- 시약 및 키트

- 바이오인포매틱스 툴 & 서비스

- 소모품 및 액세서리

- 용도별

- 종양학

- 신경학 및 중추 신경계 질환

- 대사성 질환

- 자가면역 질환

- 심혈관 질환

- 감염증

- 기타

- 기술별

- DNA 메틸화 분석

- 히스톤 수식(아세틸화, 메틸화, 인산화)

- 비 코딩 RNA 분석

- 크로마틴 접근성과 형태

- 기타 기술

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abcam PLC

- Active Motif

- Hologic Inc(Diagenode)

- F. Hoffmann-La Roche Ltd

- Illumina Inc.

- Merck KGaA(Sigma-Aldrich)

- QIAGEN NV

- Thermo Fisher Scientific

- Zymo Research Corp.

- PerkinElmer Inc.

- Bio-Rad Laboratories

- New England Biolabs

- Agilent Technologies

- Pacific Biosciences

- Oxford Nanopore Technologies

- NanoString Technologies

- EpiCypher Inc.

- Guardant Health

- Base Genomics

- Bioneen Inc.

- Element Biosciences

제7장 시장 기회와 전망

SHW 25.10.28The Epigenetics market is valued at USD 16.90 billion in 2025 and is projected to reach USD 35.63 billion by 2030, advancing at a 16.20% CAGR in the same period.

Advancing artificial-intelligence algorithms that mine DNA-methylation signatures, long-read sequencing breakthroughs that map complex epigenomic patterns, and faster regulatory clearance for blood-based companion diagnostics are converging to lift demand. Pharmaceutical alliances that embed epigenetic controllers into metabolic and immunological pipelines reinforce near-term commercial traction. The Epigenetics market also benefits from stronger intellectual-property filings around single-cell multi-omics platforms, while venture capital inflows accelerate laboratory automation and cloud bioinformatics ecosystems. North America continues to dominate, yet Asia Pacific shows the steepest uptake as governments subsidize precision-medicine infrastructure and local start-ups adopt pay-per-use sequencing models.

Global Epigenetics Market Trends and Insights

Growing Cancer Incidence & Precision-Medicine Adoption

Escalating global cancer prevalence amid aging populations fuels demand for epigenetic biomarkers that stratify patients and track minimal residual disease. Illumina's expanded TruSight Oncology portfolio now reports methylation-informed variant calls that refine therapy selection. Multi-cancer early detection blood tests that read methylation signatures, such as Galleri, move from research to clinics, enabling earlier intervention. In hematological malignancies, integrated epigenomic-genomic profiling is identifying resistance-associated subtypes, thereby broadening indications for epigenetic drugs. The cumulative momentum positions methylation panels as foundational elements in next-generation companion diagnostics.

Expansion of Epigenetic Applications in Non-Oncology Application

Breakthrough studies show long non-coding RNAs regulate neuroinflammation in Alzheimer's disease, opening therapeutic windows for epigenetic editing. Novo Nordisk and Omega Therapeutics are co-creating epigenomic controllers that modulate thermogenesis for obesity treatment. Cardiometabolic pipelines now incorporate integrated genetic-epigenetic risk algorithms that outperform standard lipid tests. Epigenetic re-writing tools that suppress mutant alleles without DNA cuts are entering early-phase trials for Huntington's disease. Such cross-disciplinary momentum diversifies revenue streams for the Epigenetics market beyond its oncology core.

High Cost of NGS & Single-Molecule Instruments

Even as whole-genome sequencing trends toward the USD 100 threshold, comprehensive epigenomic workflows still need higher coverage, specialized library kits, and robust long-read platforms that keep per-sample costs elevated. Oxford Nanopore's PromethIon, for instance, requires sophisticated fluidics upkeep and high-end GPUs. Single-cell methylome pipelines add separate tagmentation steps, proprietary reagents, and expanded compute clusters. Depreciation charges and recurring service contracts strain clinical labs in Brazil, South Africa, and Indonesia, slowing adoption in those high-burden cancer territories. Bundled leasing and reagent-rental schemes are emerging but have yet to close the affordability gap fully.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Multi-Omics R&D Funding & Collaborative Consortia

- Regulatory Support for Companion Diagnostics

- Shortage of Skilled Bioinformaticians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits accounted for 41.4% of the epigenetics market share in 2024, propelled by continued bulk purchasing of bisulfite-conversion chemistries and chromatin-immunoprecipitation reagents. Instruments ranked second owing to rising demand for long-read sequencers that detect 5mC, 5hmC, and 6mA directly. The bioinformatics sub-segment, however, is projected to record a 20.1% CAGR through 2030, underpinned by AI-powered cloud pipelines that translate raw signal data into actionable biomarker insights. Advanced analytics vendors now offer pay-as-you-go methylome pipelines, lowering entry barriers for mid-tier hospitals. New patents around machine-learning models for epigenetic age, immune status, and treatment response continue to command premium licensing fees, reflecting the data gravity shift inside the Epigenetics market.

The Epigenetics industry is witnessing a pivot from hardware to software differentiation as sequencing accuracy plateaus. Multi-omics dashboards integrate methylation, chromatin accessibility, and long-read transcript counts in a single user interface. Subscription revenues from informatics suites are outpacing reagent sales growth. Consequently, instrument suppliers have begun bundling analytics credits with sequencer purchases, a tactic that influences total cost-of-ownership decision calculus among clinical labs. Given these currents, bioinformatics platforms are positioned to overtake consumables in revenue contribution by the late forecast horizon.

The Epigenetics Market is Segmented by Product (Instruments, Reagents & Kits, and More), Application (Oncology, Neurology & CNS Disorders, Metabolic Diseases, Autoimmune Diseases, and More), Technology (DNA Methylation Analysis, Histone Modification-Acetylation, Methylation, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 43.4% of the Epigenetics market share in 2024, thanks to FDA clearances for methylation-informed diagnostics and NIH funding that subsidizes multi-omics population studies. Venture investors pumped unprecedented capital into platform start-ups, exemplified by Tune Therapeutics' USD 175 million raise, securing rapid clinical translation tracks for hepatitis B epigenome-silencing therapies. Academic clusters in Boston, San Francisco, and Durham incubate cross-disciplinary talent pools that sustain regional dominance.

Asia Pacific is forecast to grow at 17.0% CAGR through 2030 as aging demographics elevate cancer incidence and governments underwrite precision-oncology test reimbursements. China anchors regional sequencing capacity with industrial-scale nanopore facilities, while Japan's national whole-genome program stimulates secondary epigenome analysis demand. Start-ups in Singapore and India are launching culturally tailored prostate-cancer methylation panels that align with local screening norms. Such initiatives expand the Epigenetics market penetration into previously underserved populations.

Europe exhibits balanced expansion. GDPR-compliant data federations delay cross-border joint analyses, yet the European Health Data Space regulation is harmonizing consent clauses, thereby unlocking consortium trials that integrate epigenomic endpoints. The United Kingdom's GBP 250 million bilateral project with Oxford Nanopore to profile 50,000 biobank epigenomes exemplifies public-private investment intensity. Germany and France sustain pharmaceutical research into LSD1 and EZH2 inhibitors, amplifying regional Epigenetics market engagement despite reimbursement heterogeneity across member states.

- Abcam

- Active Motif

- Hologic Inc (Diagenode)

- Roche

- Illumina

- Merck

- QIAGEN

- Thermo Fisher Scientific

- Zymo Research Corp.

- PerkinElmer

- Bio-Rad Laboratories

- New England Biolabs

- Agilent Technologies

- Pacific Biosciences

- Oxford Nanopore Technologies

- NanoString Technologies

- EpiCypher Inc.

- Guardant Health

- Base Genomics

- Bioneen Inc.

- Element Biosciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cancer Incidence & Precision-Medicine Adoption

- 4.2.2 Expansion Of Epigenetic Applications In Non-Oncology Application

- 4.2.3 Surge In Multi-Omics R&D Funding & Collaborative Consortia

- 4.2.4 Regulatory Support For Companion Diagnostics

- 4.2.5 AI-Enabled Epigenetic Biomarker Discovery Accelerators

- 4.2.6 Venture Investments In Single-Cell & Long-Read Epigenomics Platforms

- 4.3 Market Restraints

- 4.3.1 High Cost Of NGS & Single-Molecule Instruments

- 4.3.2 Shortage Of Skilled Bioinformaticians

- 4.3.3 Data-Privacy Hurdles For Population-Scale Epigenomic Datasets

- 4.3.4 Limited Reimbursement Pathways For Epigenetic Diagnostics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.2 Reagents & Kits

- 5.1.3 Bioinformatics Tools & Services

- 5.1.4 Consumables & Accessories

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Neurology & CNS Disorders

- 5.2.3 Metabolic Diseases

- 5.2.4 Autoimmune Diseases

- 5.2.5 Cardiovascular Diseases

- 5.2.6 Infectious Diseases

- 5.2.7 Others

- 5.3 By Technology

- 5.3.1 DNA Methylation Analysis

- 5.3.2 Histone Modification (Acetylation, Methylation, Phosphorylation)

- 5.3.3 Non-coding RNA Analysis

- 5.3.4 Chromatin Accessibility & Conformation

- 5.3.5 Other Technologies

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abcam PLC

- 6.3.2 Active Motif

- 6.3.3 Hologic Inc (Diagenode)

- 6.3.4 F. Hoffmann-La Roche Ltd

- 6.3.5 Illumina Inc.

- 6.3.6 Merck KGaA (Sigma-Aldrich)

- 6.3.7 QIAGEN N.V.

- 6.3.8 Thermo Fisher Scientific

- 6.3.9 Zymo Research Corp.

- 6.3.10 PerkinElmer Inc.

- 6.3.11 Bio-Rad Laboratories

- 6.3.12 New England Biolabs

- 6.3.13 Agilent Technologies

- 6.3.14 Pacific Biosciences

- 6.3.15 Oxford Nanopore Technologies

- 6.3.16 NanoString Technologies

- 6.3.17 EpiCypher Inc.

- 6.3.18 Guardant Health

- 6.3.19 Base Genomics

- 6.3.20 Bioneen Inc.

- 6.3.21 Element Biosciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment