|

시장보고서

상품코드

1836617

자궁내막암 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Endometrial Cancer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

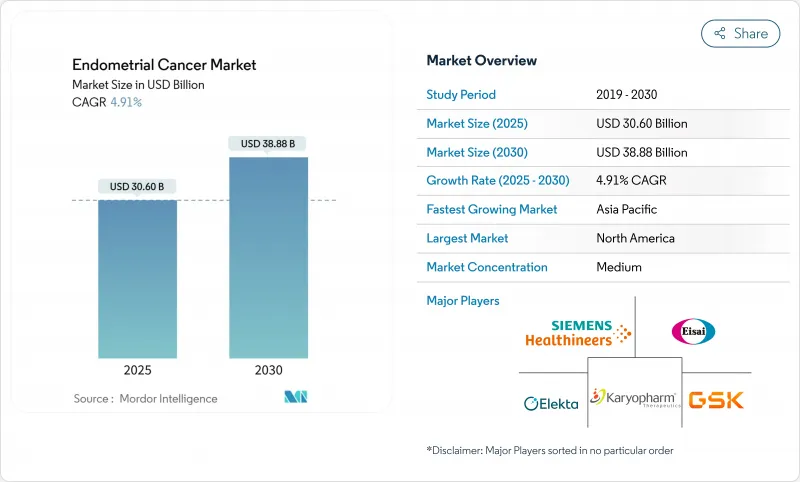

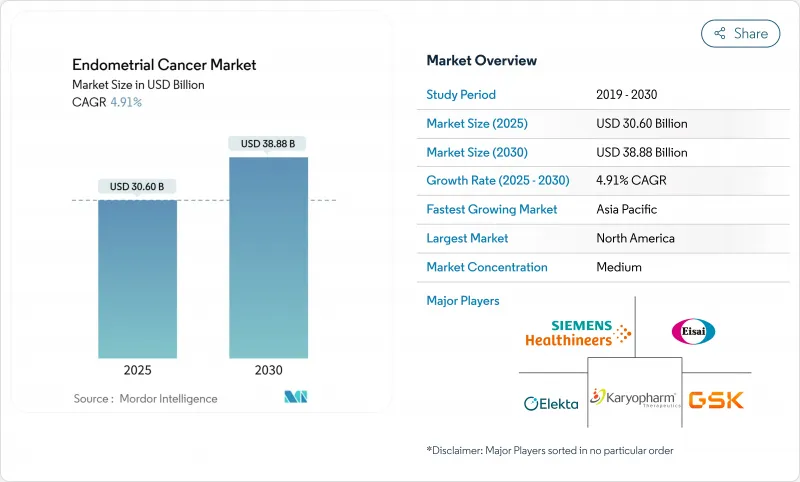

세계의 자궁내막암 시장 규모는 2025년에 306억 달러, CAGR 4.91%로 성장하여, 2030년에는 388억 8,000만 달러에 달할 것으로 예측되고 있습니다.

성장을 뒷받침하는 것은 전체 생존기간을 현저하게 개선하는 면역요법과 화학요법의 병용요법의 급속한 보급, 겨냥한 처방의 지침이 되는 분자검사의 보급, 고소득국가에서의 지원적인 상환정책입니다. 인공지능 이미지 분석 및 단백질체학 바이오마커 패널을 포함한 진단 기술 혁신은 조기 발견의 폭을 넓혀 낮은 침습 수술은 환자에게 스크리닝을 용이하게 합니다. 반면 국내 방사성 동위원소 생산에 대한 공급망 투자는 영상 진단과 브랙세라피에 대한 병목 현상을 완화시켜 치료 능력이 이환율 상승을 따라잡을 수 있도록 합니다. 경쟁의 세력도는 3가지 체크포인트 억제제가 지배적이며, 이들의 병용 시험 프로그램에 의해 종양학 네트워크 전체의 브랜드 충성도를 강화하는 신규 라벨의 확대가 높은 비율로 유지되고 있습니다.

세계 자궁내막암 시장 동향과 통찰

비만과 여성의 노화와 관련된 유병률 상승

세계 비만 증가와 여성의 평균 수명 연장은 치료 대상 인구를 확대하고 종양과 서비스에 부담을 주고 치료제와 진단제에 대한 지속적인 수요를 창출하고 있습니다. 당뇨병과 고혈압과 같은 대사성 합병증은 수술 위험을 증가시키고 수술기 관리를 복잡하게 하기 때문에 전신 치료 옵션의 조기 채택을 촉진합니다. 자궁내막의 두께가 14mm를 넘으면 동시에 발생하는 악성 종양의 위험이 4배가 되므로 병기 분류를 위해 부인과 종양과를 소개하는 빈도가 높아집니다. 헬스케어 시스템은 집학적 클리닉의 규모를 확대하고, 특히 교외나 지방에서 증가하는 사례수를 관리하기 위해 원격 종양학을 활용함으로써 대응하고 있습니다. 보험사는 비만과 관련된 위험을 인식하게 되어 새로 진단된 사례를 치료 파이프라인에 보내는 예방 스크리닝 혜택을 승인하고 있습니다. 고BMI 코호트가 60-65세의 연령층에 들어가면서 자궁내막암 시장은 장기적인 확대가 예상됩니다.

면역요법과 화학요법의 병용요법의 급속한 보급

2024년 1월부터 2025년 3월까지 3가지 체크포인트 억제제 병용 요법이 승인되었으며, 각각 백금 제형 2제 병용 화학요법보다 생존 기간이 연장되었습니다. 도스탈리맙과 카르보플라틴 파클리탁셀의 병용 요법은 화학요법 단독의 28.2개월에 대해 전체 생존 기간 중앙값을 44.6개월로 연장했습니다. 펨브롤리주맙의 요법은 불일치 수리 결핍 종양에서 무증상 생존 기간을 70% 향상시키고, 듀발바맙은 DUO-E 시험에서 병세 진행 위험을 58% 감소시켰습니다. 이러한 데이터는 임상적 기대치를 재설정하며, 국가 가이드라인은 현재 진행성 질환에 대한 최전선 치료로서 병용 요법을 권장하고 있습니다. 이 전환은 바이오마커에 기반한 자격이 상환을 결정하고 결과를 최적화하기 때문에 분자 생물학적 검사의 확대를 강요합니다. 캐나다와 유럽연합(EU)에서의 신속한 승인은 세계 하모나이제이션을 보여주며, 다자간 임상시험 결과를 상업 수익으로 신속하게 전환할 수 있게 합니다.

신약의 높은 치료비

체크포인트 억제제 병용요법은 불일치 수복능을 가진 종양에 대해 질조정 생존년당 15만 달러를 넘는 증분비용효과비를 가져오고, 비싼 정가로 판매되고 있습니다. 약물경제학적 연구에 따르면, 도스탈 리맙과 화학요법의 병용은 중국에서 지불 의사의 임계값을 충족시키기 위해 15%의 가격 인하가 필요합니다. 재발 사례 관리는 비재발 사례에 비해 환자 1인당 연간 8만 4,562달러의 초과 비용을 추가합니다. 저소득지역에서는 최대 7년의 상환지연이 생존기간의 갭을 악화시켜 임상적 돌파구에도 불구하고 자궁내막암 시장을 제약하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 표적 치료에 대한 유리한 상환

- 최소 침습 진단 절차의 성장

- 복약 충동을 제한하는 약물 관련 독성

부문 분석

자궁내막암은 가장 큰 환자 집단과 체크포인트 억제제의 병용에 관한 광범위한 근거에 힘입어 2024년 매출 점유율 73.55%로 자궁내막암 시장을 견인했습니다. 자궁육종은 소수 예이지만 정밀 수술 기술과 적응 외의 표적 약물이 치료 성적을 개선함에 따라 CAGR은 8.25%를 나타내고 있습니다. 암 육종 가이드라인은 미스매치 수리 상태에 따른 생존율의 차이를 반영하여 도스터 리맙 기반 요법을 권장합니다. 진행선암은 펩브로리주맙과 카르보플라틴 파클리탁셀의 병용요법에 특히 잘 반응하고, 70%의 무증악 생존기간의 연장을 나타내며 의사의 취향을 굳히고 있습니다. 분자 서브타이핑은 예기치 않게 공격적인 거동을 나타내는 p53-유사 NSMP 종양을 드러냈습니다. 이러한 병변은 이중 체크포인트 블로케이드를 탐구하는 차세대 시험에 빠르게 등록되고 있습니다.

인공지능을 이용한 병리 조직학적 플랫폼은 이전에 잘못 분류된 고위험 클론에 신고하여 조기 전신 요법을 가능하게 합니다. 암육종의 사례 시리즈에서 연구된 렘바티닙 펨브롤리주맙은 관리 가능한 고혈압과 피로를 동반하면서 60% 이상의 병세 조절률을 달성하였으며 백금 제형 요법이 무효인 경우에 구제적 선택을 제공했습니다. 바이오마커 검사가 일상적으로 이루어지게 되면서, 치료법의 선택은 조직학적인 것에서 변이에 근거한 알고리즘으로 이행해, 자궁내막암 시장의 세분화이 깊어져, 동반진단약 수요가 높아지고 있습니다.

지역별 분석

2024년 자궁내막암 시장 규모는 폭넓은 면역요법보험 적용, 높은 검진 보급률, 전문종양센터의 집중을 배경으로 북미가 37.72%의 점유율로 선두를 차지했습니다. 분자진단제의 보급은 거의 보편적이며, 캐나다 보건부가 2025년에 펨브롤리주맙과 도스터리맙을 몇 주 이내에 승인한 것은 규제 당국의 신속한 대응을 뒷받침하고 있습니다. 아웃컴즈 기반 계약과 같은 가격 협상 메커니즘은 예산에 미치는 영향을 관리하면서 공공 부담으로 적시에 상장을 보장합니다.

유럽은 여전히 기술 혁신에 친화적이지만 비용을 인식하는 환경입니다. CHMP에 의한 도스탈 리맙의 전진행례에 대한 적응확대에 대한 긍정적 견해는 유럽 전역에서의 상환을 위한 포석이 되었지만, 각국 정부는 비용대비비를 조사하고 때로는 적응 전에 위험분담계약을 의무화할 수도 있습니다. 동유럽 국가에서는 도입이 지연되고 있지만 EU의 통합기금이 분자병리검사시설에 보조금을 내게 되어 접근격차가 축소되고 있습니다.

2030년까지 가장 빠른 연평균 복합 성장률(CAGR)로 아시아태평양이 9.22%인데, 이는 인구동태의 압력과 정부의 이니셔티브을 모두 반영하고 있습니다. 일본과 한국은 면역요법을 국가 가이드라인에 통합하고 중국은 해남 리얼 월드 에비던스 시험을 통해 국내 제조를 활용하여 가격을 낮추고 승인을 가속화하고 있습니다. 보다 광범위한 질병 부담에 관한 조사에서는 특히 60-64세 여성에서 2050년까지 이환율이 지속적으로 증가할 것으로 예측되고 있으며, 수요의 지속이 강조되고 있습니다.

남미에서는 확대되는 민간 보험과 의료 관광의 흐름이 도입 패턴에 영향을 미치고 있습니다. 안데스나 중미 국가의 환자들은 현지에서 이용할 수 없는 체크포인트 억제제를 찾아 브라질을 방문하는 경우가 많습니다. 사하라 사막 이남의 아프리카에서는 가장 큰 케어 갭에 직면하고 있습니다. 조사 대상이 되는 의료 제공업체의 92%가 부인과 종양을 위해 국외에의 의료 도항을 보고하고 있어, 미충족 요구를 강조하고 있습니다. 병리실의 업그레이드를 후원하는 국제 원조 프로그램은 진단 격차를 줄이기 시작하여 향후 10년간 시장 성장으로 이어질 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비만과 여성 고령화와 관련된 유병률 상승

- 면역요법과 화학요법의 병용요법의 급속한 보급

- 표적치료에 대한 유리한 상환제도

- 낮은 침습 진단 절차의 성장

- 근접치료의 외래 전환이 치료 접근성을 확대

- 시장 성장 억제요인

- 신규 약제의 높은 치료비

- 치료 순응도를 제한하는 약제 관련 독성

- 영상/치료를 위한 방사성 동위원소 공급 제약 조건

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액, 달러)

- 암 유형별

- 자궁내막암

- 선암암

- 암육종

- 편평상피암

- 기타 유형

- 자궁육종

- 자궁내막암

- 치료 유형별

- 면역요법

- 방사선요법

- 화학요법

- 기타 치료

- 진단 방법별

- 생검

- 골반 초음파 검사

- 자궁경 검사

- CT 스캔

- 기타 방법

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Merck KGaA

- Eisai Co Ltd

- Novartis AG

- Elekta AB

- Siemens Healthineers(Varian)

- GSK plc

- Karyopharm Therapeutics

- Takeda Pharmaceutical

- Bristol Myers Squibb

- F. Hoffmann-La Roche

- Context Therapeutics

- AstraZeneca PLC

- Pfizer Inc

- Hologic Inc

- Myriad Genetics

- GE HealthCare

- Medtronic plc

- Astellas Pharma

- Clovis Oncology

- Seagen Inc

제7장 시장 기회와 전망

SHW 25.10.28The global endometrial cancer market size reached USD 30.60 billion in 2025 and is forecast to climb to USD 38.88 billion by 2030, advancing at a 4.91% CAGR.

Growth is propelled by the rapid uptake of immunotherapy-chemotherapy combinations that markedly improve overall survival, wider molecular testing that guides targeted prescribing, and supportive reimbursement policies in high-income countries. Diagnostic innovation-including artificial-intelligence image analysis and proteomic biomarker panels-broadens early detection while minimally invasive procedures make screening more acceptable to patients. Meanwhile, supply chain investments in domestic radioisotope production ease bottlenecks for imaging and brachytherapy, ensuring treatment capacity keeps pace with rising incidence. Competitive dynamics are dominated by three checkpoint inhibitors, and their combination trial programs sustain a high rate of new label expansions that reinforce brand loyalty across oncology networks.

Global Endometrial Cancer Market Trends and Insights

Rising Prevalence Linked to Obesity & Ageing Women

Global increases in obesity and longer female life expectancy enlarge the treated population, straining oncology services and creating sustained demand for therapies and diagnostics. Metabolic comorbidities such as diabetes and hypertension raise surgical risk and complicate perioperative management, encouraging earlier adoption of systemic therapy options. Endometrial thickness readings above 14 mm quadruple concurrent malignancy risk, prompting more frequent gynecologic oncology referrals for staging. Healthcare systems respond by scaling multidisciplinary clinics and leveraging tele-oncology to manage rising caseloads, especially in suburban and rural settings. Insurers increasingly recognize obesity-linked risk, approving preventive screening benefits that feed newly diagnosed cases into the treatment pipeline. As high-BMI cohorts enter the 60-65 year age band, the endometrial cancer market is set for long-run expansion.

Rapid Adoption of Immunotherapy-Chemotherapy Combinations

Three checkpoint inhibitor combinations won regulatory clearance between January 2024 and March 2025, each showing superior survival to platinum doublet chemotherapy. Dostarlimab plus carboplatin-paclitaxel extended median overall survival to 44.6 months versus 28.2 months for chemotherapy alone. Pembrolizumab regimens improved progression-free survival by 70% in mismatch-repair-deficient tumors, while durvalumab cut disease-progression risk by 58% in the DUO-E trial. Such data reset clinical expectations, and national guidelines now recommend combination therapy as frontline care for advanced disease. The shift forces expansion of molecular testing, because biomarker-guided eligibility determines reimbursement and optimizes outcomes. Rapid approvals in Canada and the European Union illustrate global harmonization, enabling multinational trial readouts to convert swiftly into commercial revenue.

High Treatment Costs of Novel Agents

Checkpoint inhibitor combinations command premium list prices, leading to incremental cost-effectiveness ratios above USD 150,000 per quality-adjusted life year for mismatch-repair-proficient tumors. Pharmacoeconomic studies show dostarlimab plus chemotherapy requires a 15% price trim to meet willingness-to-pay thresholds in China. Recurrent-disease management adds USD 84,562 in excess annual costs per patient compared with non-recurrent cases. In lower-income regions, reimbursement delays of up to seven years exacerbate survival gaps, constraining the endometrial cancer market despite clinical breakthroughs.

Other drivers and restraints analyzed in the detailed report include:

- Favourable Reimbursement for Targeted Therapies

- Growth in Minimally-Invasive Diagnostic Procedures

- Drug-Related Toxicities Limiting Adherence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endometrial carcinoma anchored the endometrial cancer market with a 73.55% revenue share in 2024, supported by the largest patient pool and extensive evidence for checkpoint inhibitor combinations. Uterine sarcomas, though accounting for a minority of cases, are on an 8.25% CAGR trajectory as precision-surgery techniques and off-label targeted agents improve outcomes. Carcinosarcoma guidelines now recommend dostarlimab-based regimens, reflecting solid survival benefits across mismatch-repair status. Advanced adenocarcinoma responds especially well to pembrolizumab plus carboplatin-paclitaxel, which demonstrated a 70% progression-free survival gain, consolidating physician preference. Molecular sub-typing reveals p53-like NSMP tumors with unexpectedly aggressive behavior; these lesions are enrolling rapidly in next-generation trials exploring double-checkpoint blockade.

AI-enabled histopathology platforms flag high-risk clones previously misclassified, allowing earlier systemic therapy. Lenvatinib-pembrolizumab, studied in carcinosarcoma case series, achieved disease-control rates above 60% with manageable hypertension and fatigue, offering a salvage option when platinum regimens fail. With biomarker testing now routine, therapeutic choice shifts from histology to mutation-based algorithms, deepening segmentation and pushing demand for companion diagnostics within the endometrial cancer market.

The Endometrial Cancer Market Report is Segmented by Type of Cancer (Endometrial Carcinoma [Adenocarcinoma, Carcinosarcoma, and More], and Uterine Sarcomas), Type of Therapy (Immunotherapy, Radiation Therapy, and More), Diagnosis Method (Biopsy, Pelvic Ultrasound, Hysteroscopy, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the endometrial cancer market size with 37.72% share in 2024 on the strength of broad immunotherapy insurance coverage, high screening penetration, and concentration of specialized oncology centers. Uptake of molecular diagnostics is near-universal, and Health Canada's 2025 approvals of pembrolizumab and dostarlimab within weeks of each other confirm swift regulatory throughput. Price negotiation mechanisms such as Outcomes-Based Agreements ensure timely public-payer listing while managing budget impact.

Europe remains an innovation-friendly but cost-aware environment. The CHMP's positive opinion for dostarlimab expansion to all advanced cases sets the stage for continent-wide reimbursement, yet national bodies scrutinize cost-effectiveness ratios, sometimes mandating risk-sharing deals before inclusion. Eastern European markets show slower uptake, but EU cohesion funds now subsidize molecular pathology labs, closing access gaps.

Asia-Pacific exhibits the fastest 9.22% CAGR through 2030, reflecting both demographic pressure and government action. Japan and South Korea integrate immunotherapy into national guidelines, while China leverages domestic manufacturing to lower prices and accelerate approvals via the Hainan Real-World Evidence pilot. A broader disease burden study predicts continuous incidence growth until 2050, especially in women aged 60-64, underscoring sustained demand.

In South America, expanding private insurance and medical-tourism flows influence adoption patterns. Patients from Andean and Central American countries often travel to Brazil for checkpoint inhibitors unavailable locally. Sub-Saharan Africa faces the largest care gaps; 92% of providers surveyed report outbound medical travel for gynecologic oncology, spotlighting unmet need. International aid programs that sponsor pathology-lab upgrades are beginning to narrow the diagnostic divide, which will translate into measurable market growth over the next decade.

- Merck

- Eisai

- Novartis

- Elekta

- Siemens Healthineers (Varian)

- GlaxoSmithKline

- Karyopharm Therapeutics

- Takeda Pharmaceuticals

- Bristol-Myers Squibb

- Roche

- Context Therapeutics

- AstraZeneca

- Pfizer

- Hologic

- Myriad Genetics

- GE Healthcare

- Medtronic

- Astellas Pharma

- Clovis Oncology

- Seagen Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Linked To Obesity & Ageing Women

- 4.2.2 Rapid Adoption Of Immunotherapy-Chemotherapy Combinations

- 4.2.3 Favourable Reimbursement For Targeted Therapies

- 4.2.4 Growth In Minimally-Invasive Diagnostic Procedures

- 4.2.5 Outpatient Shift For Brachytherapy Expanding Access

- 4.3 Market Restraints

- 4.3.1 High Treatment Costs Of Novel Agents

- 4.3.2 Drug-Related Toxicities Limiting Adherence

- 4.3.3 Radio-Isotope Supply Constraints For Imaging/Therapy

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Cancer

- 5.1.1 Endometrial Carcinoma

- 5.1.1.1 Adenocarcinoma

- 5.1.1.2 Carcinosarcoma

- 5.1.1.3 Squamous Cell Carcinoma

- 5.1.1.4 Other Types

- 5.1.2 Uterine Sarcomas

- 5.1.1 Endometrial Carcinoma

- 5.2 By Type of Therapy

- 5.2.1 Immunotherapy

- 5.2.2 Radiation Therapy

- 5.2.3 Chemotherapy

- 5.2.4 Other Therapies

- 5.3 By Diagnosis Method

- 5.3.1 Biopsy

- 5.3.2 Pelvic Ultrasound

- 5.3.3 Hysteroscopy

- 5.3.4 CT Scan

- 5.3.5 Other Methods

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Merck KGaA

- 6.3.2 Eisai Co Ltd

- 6.3.3 Novartis AG

- 6.3.4 Elekta AB

- 6.3.5 Siemens Healthineers (Varian)

- 6.3.6 GSK plc

- 6.3.7 Karyopharm Therapeutics

- 6.3.8 Takeda Pharmaceutical

- 6.3.9 Bristol Myers Squibb

- 6.3.10 F. Hoffmann-La Roche

- 6.3.11 Context Therapeutics

- 6.3.12 AstraZeneca PLC

- 6.3.13 Pfizer Inc

- 6.3.14 Hologic Inc

- 6.3.15 Myriad Genetics

- 6.3.16 GE HealthCare

- 6.3.17 Medtronic plc

- 6.3.18 Astellas Pharma

- 6.3.19 Clovis Oncology

- 6.3.20 Seagen Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment