|

시장보고서

상품코드

1836623

세균성 바이오 농약 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bacterial Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

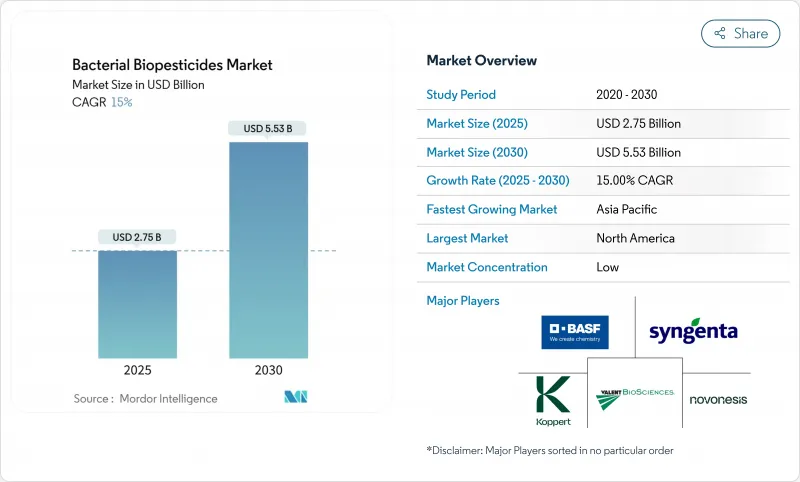

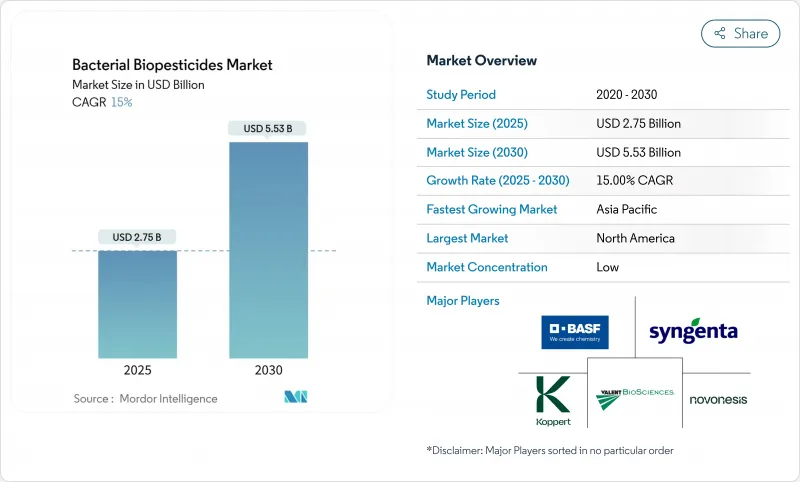

세균성 바이오 농약 시장 규모는 2025년에 27억 5,000만 달러, 예측기간 중(2025-2030년) CAGR은 15%를 나타내고, 2030년에는 55억 3,000만 달러에 달할 것으로 예측됩니다.

시장 성장의 원동력은 신속한 규제 승인, 잔류 농약이 없는 농산물에 대한 소비자 수요 증가, 유기농업의 확대, 제제의 안정성과 현장 유효성을 높이는 기술의 진보입니다. FiBL에 따르면 세계의 유기농업 면적은 2023년 9,890만 헥타르에 달하고, 2.6% 증가를 보입니다. 바실러스 투링기엔시스(Bacillus thuringiensis, Bt)가 74%의 매출 점유율로 시장을 독점하고 있지만, 고초균(Bacillus subtilis)는 해충 방제와 식물 성장 촉진 기능을 겸비한 것으로 급성장을 보이고 있습니다. 정밀 종자 처리에의 응용, 환경 제어형 농업용의 액체 제제, 대기업 농약 회사의 포트폴리오 통합 등이 시장 확대를 지지하고 있습니다. 세균성 바이오 농약의 채택률은 콜드체인에서의 보관 요건이나 화학적 대체품에 비해 완만한 효능에 의해 영향을 받고 있으며, 기업은 경쟁이 격화되는 시장에서 이러한 과제를 해결하기 위해 노력하고 있습니다.

세계 세균성 바이오 농약 시장 동향과 통찰

규제 및 정책 지원

유럽에서의 바이오 농약의 승인 과정은 9년에서 약 3년으로 단축되어 100개 이상의 보류물질을 다루고 있습니다. 유럽위원회는 4분기까지 바이오농약 승인 과정을 최적화하기 위해 2025년에 새로운 EU 규정을 시행할 의향입니다. 2026년 생명공학법은 현재 규제 격차를 메우는 데 중점을 둡니다. 브라질은 불활성화된 버크홀더리아 세포 유래 생물 살충제 제품을 승인하고 유사한 진전을 보여줍니다. 미국 환경보호청(EPA)은 FIFRA(연방 살충·살균·살서제법)에 근거한 신청 잔량의 삭감을 추진하고 있습니다. 이러한 규제 변경으로 등록 기회가 확대되고 컴플라이언스 비용이 절감되고 소규모 기업도 박테리아 생물 농약 시장에 진입 할 수 있습니다.

전통적인 농약의 해에 대한 의식 증가

합성농약에 의한 생물다양성의 손실과 토양의 열화를 입증하는 조사는 고급 소매 채널에서의 구매 결정에 영향을 미치고 있습니다. 2025년 매사추세츠 공과대학의 조사 결과 세계 농지 토양의 31%가 농약 오염으로 인한 높은 위험에 직면하고 있음이 밝혀졌습니다. 북미와 유럽의 소매업체는 엄격한 잔류 제한을 실시하고 잔류 제로 생물학적 제품을 선호합니다. 생산자가 이러한 요건에 적응함에 따라, 박테리아제는 유기농 재배 전용 솔루션에서 병충해 종합 관리 프로그램의 필수 구성 요소로 진화해 왔습니다. 이 전환은 특히 수확 전 간격이 짧은 작물에 대한 박테리아 생물 농약 시장의 성장을 가속합니다.

생물학적 제형의 저장 수명을 제한하는 콜드체인 물류

살아있는 포자 제형은 일반적으로 25℃를 초과하면 생존 능력을 잃기 때문에 냉장 수송과 보관이 필요하며 최종 비용이 상승합니다. 이 문제는 소규모 유통망이 온도 관리 저장 시설이 없는 적도 바로 아래 시장에서 특히 두드러집니다. 새로운 캡슐화 기술은 실온에서의 세포 생존율을 향상시키고 유통상의 제약을 감소시키고 있지만, 스케일 업 및 규제 당국의 허가를 위한 프로세스에는 복수의 재배 기간이 필요합니다. 이러한 물류의 제약은 시장 침투를 제한하고 보존 기간이 길고 보관 요건이 최소한의 화학농약에 대한 세균성 바이오 농약의 경쟁력을 저하시키고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 잔류농약이 없는 농산물에 대한 수요가 Bt 솔루션을 견인

- 관리 환경 농업의 확대가 액체 제제를 뒷받침

- 체감상 느린 살충 효과가 농장에서의 채택을 감소

부문 분석

Bt는 2024년 수익의 74%를 차지하며 세균성 바이오 농약 시장에서 지배적 지위를 유지하고 있습니다. 이 시장 리더십은 나비목 유충에 대한 표적 독성, 광범위한 유기 인증 및 세계 규제 당국의 승인에 기인합니다. Bt 제품 시장 규모는 고자외선 조건 하에서 현장 지속성을 향상시키는 새로운 캡슐화 기술로 확대될 것으로 예측됩니다. 2024년 설문조사에서 나비목, 딱정벌레목, 반달팽이목, 쌍달팽이목, 선충 해충에 대한 Bt 독소의 효능이 확인되었습니다.

고초균은 병해 억제와 식물 성장 촉진이라는 이중의 이점을 가지므로 특히 고가치 원예에서 17%의 연평균 복합 성장률(CAGR)이 예측되어 강력한 성장 가능성을 나타내고 있습니다. 푸소모나스 플루오레센스(Pseudomonas fluorescens)는 토양을 매개로 하는 병원균의 방제에 그 역할을 확립하고 있으며, 세라티아(Serratia)와 스트렙토마이세스(Streptomyces)의 종은 키티나아제 활성과 항생제 대사 생산 능력에 의해 특수한 용도로 인기를 끌고 있습니다.

지역별 분석

북미는 2024년 세계 매출의 38%를 차지해 압도적인 지위를 유지했습니다. 미국은 대규모 옥수수와 대두 재배에서 박테리아 솔루션의 광범위한 통합을 통해 시장을 견인하고 있습니다. 캐나다의 온실 클러스터는 수경 시비 시스템에 적합한 액체 식균제를 이용하여 지역 수요를 강화하고 있습니다. 2023년에는 캐나다의 920개의 상업 온실 야채 사업이 80만 2,163톤의 야채를 생산해 2022년부터 7% 증가했습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 18%로 예상되며 가장 강력한 성장 궤도를 나타냅니다. 중국의 5개년에 걸친 녹색 해충 방제 계획과 인도의 바이오 투입 보조금 제도는 국내 생산과 도입을 촉진합니다. 일본과 싱가포르의 수직 농법은 환경 제어형 농업용으로 개발된 액체 제제 시장을 확립하고 있습니다.

유럽에서는 생물 농약에 대한 엄격한 규제가 유지되고 있지만, 최근의 변경에 의해 그 도입이 가속하고 있습니다. 유럽 위원회의 2025년 고속 트럭 규제는 북미 기준에 맞추기 위해 서류 심사 시간을 단축하고, 보다 많은 제품 등록을 가능하게 하고, 제조업체에게 EU 제품 라벨의 확대를 촉구했습니다. 북유럽의 학교급식용 공공조달 정책과 독일의 Farm-to-Fork 농약 삭감 목표를 통해 바이오 농약에 대한 수요가 높아졌고, 특히 Bt와 고초균 잎면 살포 제품이 혜택을 받았습니다. 동유럽의 곡물 생산자는 수출 시장의 엄격한 잔류 요건에 대응하여 바실러스 기반 종자 처리 시험을 시작하여 기존의 고가치 원예 용도 이외에도 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 규제 및 정책 지원

- 관행농약의 해에 대한 의식의 고조

- 잔류농약이 없는 농산물에 대한 수요가 Bt 솔루션을 견인

- 환경 제어형 농업의 확대가 액체 박테리아 제제 수요 증가

- 종합적 해충 관리(IPM) 전략 채택 증가

- 제제 및 전달 시스템의 기술적 진보

- 시장 성장 억제요인

- 생물 농약의 보존 기간을 제한하는 콜드체인 물류

- 생산과 제제화의 과제

- 체감상 느린 살충 효과가 농장에서의 채택을 감소

- 기존 살충제에 비해 높은 비용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 제품 유형별

- 바실러스 투링기엔시스(Bacillus thuringiensis)

- 고초균

- Pseudomonas fluorescens

- 기타 유형

- 살포 방법별

- 잎면 살포

- 종자 처리

- 토양처리

- 수확 후처리

- 작물 유형별

- 과일 및 야채

- 곡물 및 곡류

- 지방종자 및 콩류

- 잔디 및 관상용 작물

- 농장작물

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 기타 유럽

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 북미

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Certis Biologicals

- Valent BioSciences

- Bayer CropScience AG

- Syngenta AG

- Corteva Agriscience

- BASF SE

- UPL Limited

- FMC Corporation

- Nufarm Limited

- Koppert Biological Systems

- Novonesis

제7장 시장 기회와 앞으로의 동향

SHW 25.10.28The Bacterial Biopesticides Market size is estimated at USD 2.75 billion in 2025, and is anticipated to reach USD 5.53 billion by 2030, at a CAGR of 15% during the forecast period (2025-2030).

The market growth is driven by expedited regulatory approvals, increasing consumer demand for residue-free produce, expansion of organic farming, and technological advancements that enhance formulation stability and field efficacy. According to FiBL, the global organic farming area reached 98.9 million hectares in 2023, representing a 2.6% increase. Bacillus thuringiensis (Bt) dominates the market with a 74% revenue share, while Bacillus subtilis shows rapid growth due to its combined pest control and plant growth promotion capabilities. Precision seed treatment applications, liquid formulations for controlled-environment agriculture, and the consolidation of portfolios among major agrochemical companies support the market expansion. Adoption rate of the bacterial biopesticides is affected by cold-chain storage requirements and slower efficacy compared to chemical alternatives, as companies work to address these challenges in an increasingly competitive market.

Global Bacterial Biopesticides Market Trends and Insights

Regulatory and Policy Support

The European approval process for biopesticides has reduced from nine years to approximately three years, addressing a backlog of over 100 pending substances. The European Commission intends to implement new EU regulations in 2025 to optimize biopesticide approval processes by Q4. The 2026 Biotech Act will focus on filling current regulatory gaps. Brazil has demonstrated similar progress by approving bio-insecticidal products derived from inactivated Burkholderia cells. The United States Environmental Protection Agency (EPA) is reducing application backlogs under FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act). These regulatory changes expand registration opportunities, reduce compliance costs, and enable smaller companies to enter the bacterial biopesticides market.

Rising Awareness of the Harms of Conventional Pesticides

Research demonstrating biodiversity loss and soil degradation from synthetic pesticides influences purchasing decisions in premium retail channels. A 2025 Massachusetts Institute of Technology study revealed that 31% of global agricultural soils faced high risks from pesticide contamination. North American and European retailers implement strict residue limits, favoring zero-residue biological products. As growers adapt to these requirements, bacterial agents have evolved from organic-only solutions to essential components of integrated pest management programs. This transition drives growth in the bacterial biopesticides market, especially for crops with short pre-harvest intervals.

Cold-Chain Logistics Limiting Shelf-Life of Biologicals

Live spore formulations typically lose viability at temperatures above 25°C, necessitating refrigerated transport and storage, which increases the final cost. This challenge is particularly significant in equatorial markets where small-scale distribution networks lack temperature-controlled storage facilities. While new encapsulation technologies are improving cell viability at room temperature and reducing distribution constraints, the processes for scale-up and regulatory approval require multiple growing seasons. These logistical limitations restrict market penetration, reducing the competitiveness of bacterial biopesticides against chemical pesticides that offer extended shelf life and minimal storage requirements.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Residue-Free Produce Driving Bt Solutions

- Expansion of Controlled-Environment Agriculture Boosting Liquid Formulations

- Perceived Slower Knock-Down Reducing Adoption in Farms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bt accounted for 74% of 2024 revenue, maintaining its dominant position in the bacterial biopesticides market. This market leadership stems from its targeted toxicity against lepidopteran larvae, extensive organic certifications, and regulatory acceptance worldwide. The market size for Bt products is projected to expand due to new encapsulation technologies that improve field persistence in high-UV conditions. A 2024 study confirmed Bt toxins' effectiveness against lepidopteran, coleopteran, hemipteran, dipteran, and nematode pests.

Bacillus subtilis shows strong growth potential with a projected 17% CAGR, driven by its dual benefits of disease suppression and plant growth promotion, particularly in high-value horticulture. Pseudomonas fluorescens has established its role in controlling soil-borne pathogens, while Serratia and Streptomyces species are gaining traction in specialized applications through their chitinase activity and antibiotic metabolite production capabilities.

The Bacterial Biopesticides Market Report is Segmented by Product Type (Bacillus Thuringiensis, Bacillus Subtilis, Pseudomonas Fluorescens, and Other Types), Mode of Application (Seed Treatment, Foliar Spray, and More ), Crop Type (Grains and Cereals, Oilseeds and Pulses, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained its dominant position with a 38% share of the 2024 global revenue. The United States drives market volumes through widespread integration of bacterial solutions in large-scale corn and soybean operations. Canadian greenhouse clusters strengthen regional demand by utilizing liquid inoculants compatible with hydroponic fertigation systems. In 2023, Canada's 920 commercial greenhouse vegetable operations produced 802,163 metric tons of vegetables, a 7% increase from 2022.

Asia-Pacific demonstrates the strongest growth trajectory with an anticipated 18% CAGR through 2030. China's five-year green pest-control plan and India's bio-input subsidy programs encourage domestic production and adoption. Japan and Singapore's vertical farming operations provide established markets for liquid formulations specifically developed for controlled environment agriculture.

Europe maintains strict regulations for biopesticides, though recent changes have accelerated their adoption. The European Commission's 2025 fast-track regulation reduced dossier review times to align with North American standards, enabling more product registrations and encouraging manufacturers to expand their EU product labels. The demand for biopesticides has increased through Scandinavian public procurement policies for school meals and Germany's Farm-to-Fork pesticide reduction targets, particularly benefiting Bt and B. subtilis foliar products. Eastern European grain producers have initiated Bacillus-based seed treatment trials in response to export markets' stricter residue requirements, expanding beyond traditional high-value horticultural applications.

- Certis Biologicals

- Valent BioSciences

- Bayer CropScience AG

- Syngenta AG

- Corteva Agriscience

- BASF SE

- UPL Limited

- FMC Corporation

- Nufarm Limited

- Koppert Biological Systems

- Novonesis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory and Policy Support

- 4.2.2 Rising Awareness of the Harms of Conventional Pesticides

- 4.2.3 Demand for residue-free produce driving Bt solutions

- 4.2.4 Expansion of controlled-environment agriculture boosting demand for liquid bacterial formulations

- 4.2.5 Increasing adoption of integrated pest management (IPM) strategies

- 4.2.6 Technological advancements in formulation and delivery systems

- 4.3 Market Restraints

- 4.3.1 Cold-chain logistics limiting shelf-life of Biological biopesticides

- 4.3.2 Production and Formulation Challenges

- 4.3.3 Perceived slower knock-down reducing adoption in farms

- 4.3.4 Higher costs compared to conventional pesticides

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Bargaining Power of Buyers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Bacillus thuringiensis

- 5.1.2 Bacillus subtilis

- 5.1.3 Pseudomonas fluorescens

- 5.1.4 Other Types

- 5.2 By Mode of Application

- 5.2.1 Foliar Spray

- 5.2.2 Seed Treatment

- 5.2.3 Soil Treatment

- 5.2.4 Post-Harvest Treatment

- 5.3 By Crop Type

- 5.3.1 Fruits and Vegetables

- 5.3.2 Cereals and Grains

- 5.3.3 Oilseeds and Pulses

- 5.3.4 Turf and Ornamentals

- 5.3.5 Plantation Crops

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Rest of Europe

- 5.4.4 Africa

- 5.4.4.1 South Africa

- 5.4.4.2 Egypt

- 5.4.4.3 Rest of Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Rest of Asia-Pacific

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Certis Biologicals

- 6.3.2 Valent BioSciences

- 6.3.3 Bayer CropScience AG

- 6.3.4 Syngenta AG

- 6.3.5 Corteva Agriscience

- 6.3.6 BASF SE

- 6.3.7 UPL Limited

- 6.3.8 FMC Corporation

- 6.3.9 Nufarm Limited

- 6.3.10 Koppert Biological Systems

- 6.3.11 Novonesis