|

시장보고서

상품코드

1836625

바이오 임플란트 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bio-Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

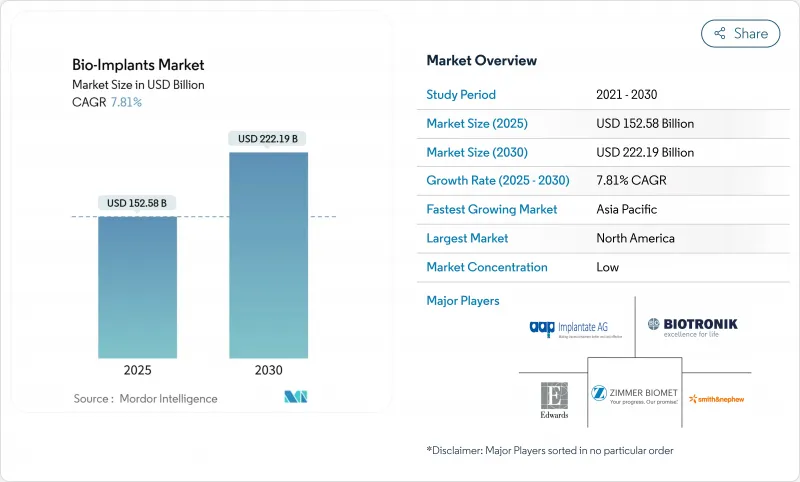

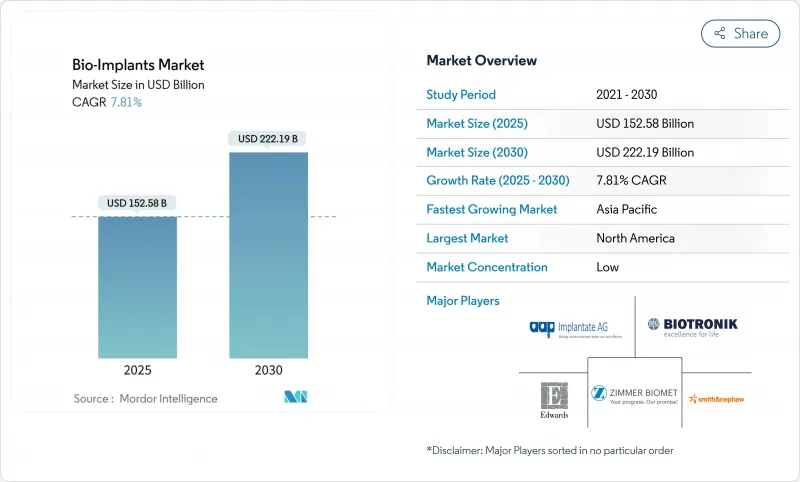

바이오 임플란트 세계 시장은 2025년에 1,525억 8,000만 달러, 2030년에는 2,221억 9,000만 달러에 이르고, CAGR은 7.81%를 나타낼 전망입니다.

급속한 확산의 배경은 인구 고령화, 만성 질환의 급증, 케어 팀에 실시간 임상 데이터를 전송하는 센서 지원 장비의 일상적인 사용을 포함합니다. 또한 생체 흡수성 재료는 제거 수술의 후속 조치를 필요로 하지 않습니다. 의료 제공업체가 의료기기의 가격뿐만 아니라 총 에피소드 비용을 중시하는 신흥국에서는 가치 기반의 상환을 목표로 하는 의료 시스템의 움직임이 채택을 가속화하고 있습니다. 선도적인 공급업체가 틈새 혁신자를 인수하고 근골격과 심장혈관의 완전한 포트폴리오를 갖추면서 경쟁의 치열성이 커지고 있습니다.

세계 바이오 임플란트 시장 동향과 통찰

만성 질환과 생활 습관병의 부담 증가

당뇨병, 심혈관 질환, 근골격계 질환이 수요 패턴을 재구성하고 있습니다. 제넨텍의 Susvimo는 2025년 미국 식품의약국(FDA)으로부터 연 2회의 보충으로 끝나는 최초의 지속적 안구 약물 전달 임플란트로서 승인을 받아 다기능 디바이스가 얼마나 적은 개입으로 만성적인 병태에 대처할 수 있게 되었는지를 강조하고 있습니다. 고소득국가의 헬스케어 시스템은 재입원을 줄이는 오래 지속되는 임플란트를 지지하고 적극적인 관리로 전환하고 있습니다.

낮은 침습 수술에 대한 선호도 증가

외래수술센터(ASC)에서는 2024년에 4,400만 건의 수술을 실시하고, 지불자가 외래 인공 관절 치환술에 보험 적용함에 따라, 향후에도 확대가 전망됩니다. 임플란트 제조업체는 수술 시간 단축과 당일 퇴원 프로토콜에 최적화된 디바이스를 개발함으로써 이에 대응하고 기존 병원 극장의 틀을 넘어 대응 가능한 바이오 임플란트 시장을 확대하고 있습니다.

고급 임플란트의 고액 초기 비용

프리미엄 센서 기반 장비는 여전히 비싸기 때문에 자본 예산에 제한이 있는 지역에서는 지불자가 망설입니다. 의료 시스템이 혁신을 멈추지 않고 경제성 현실에 기능을 적응할 수 있도록 공급업체는 점진적인 포트폴리오를 개발하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 고령화에 의한 관절 치환술의 급증

- 3D 프린팅에 의한 환자 전용 임플란트의 급증

- 불리한/단편적인 상환 경로

부문 분석

정형외과 장치는 2024년 바이오 임플란트 시장 점유율의 28.12%를 차지했으며, 단일 및 최대 수익 블록이 되었습니다. 그러나 심혈관 임플란트는 경 카테터 밸브와 이식형 혈행동태센서를 원동력으로 하여 CAGR 8.54%로 가장 높은 모멘텀을 제공합니다. 이 분야는 말기 부전을 목표로 한 BiVACOR의 완전한 인공 심장을 포함한 FDA의 획기적인 장치 지정으로부터 혜택을 누리고 있습니다. 미래에는 원격 텔레메트리와 통합된 스마트 페이스메이커가 바이오 임플란트 시장에서 심장혈관 발자국을 더욱 확대할 것으로 보입니다.

정형외과 기술 혁신은 로봇의 지침과 베어링 수명을 연장하는 트라이 볼 로지의 개선으로 견고성을 유지합니다. 신경 자극 장치는 환자의 피드백에 따라 재조정하는 적응 알고리즘을 활용하며, 인공 내이는 완전히 이식 가능한 폼 팩터로 향하고 있습니다. 이 범주는 2030년까지 9억 4,010만 달러에 이를 것으로 예측됩니다. Susvimo와 같은 안과용 플랫폼은 예상되는 치료 빈도를 재형성하여 모든 임플란트 라인에서 안정적인 수요를 강화합니다.

티타늄의 비교할 수 없는 강도 대 중량비로 인해 금속과 합금은 2024년 매출의 44.34%를 차지했지만, 폴리에테르-에테르-케톤(PEEK)과 폴리유산(PLA)의 변종이 응력 차폐를 완화하기 때문에 복합재료가 8.43%로 가장 빠르게 성장할 것으로 예상됩니다. 항균성은 이온을 첨가한 세라믹은 감염 위험을 줄이고 생체활성 유리 매트릭스는 염증 캐스케이드 없이 뼈 형성을 촉진합니다. 단단한 코어에서 컴플라이언트 아웃터 존으로 이동하는 그라데이션 빌드는 천연 조직을 모방하여 연조직 수리의 적응을 넓힙니다.

지역 분석

북미는 2025년에 FDA의 인가를 받은 메드트로닉의 브레인센스 플랫폼과 같은 폐루프 신경 자극기의 보급을 촉진하기 위해 2024년 세계 매출의 48.67%를 차지했습니다. 캐나다와 멕시코에서 국경을 넘은 환자 유입이 절차의 성장을 더욱 지원하는 한편, 다양한 지불자 구성이 가격 실현을 안정시킵니다.

아시아태평양은 CAGR 8.45%에서 가장 빠르게 성장하는 바이오 임플란트 시장입니다. 중국은 국내 제조를 지원하고 인도는 규제 코드를 국제 표준에 맞추고 일본의 초고령화 사회는 관절과 심장 장치를 선호합니다. 한국의 디지털 의료 인프라는 원격 모니터링의 보급을 가속화하고 호주 연구 허브는 지역 출시 위험을 줄이는 매우 중요한 임상시험을 실시합니다.

유럽에서는 의료기기 규제(MDR) 인증의 병목을 고민하고 있으며, 불과 43개의 노티파이드 바디가 50만대의 기기를 관리하고 있을 뿐, 시장 진입이 늦어지고 있습니다. 2027년까지의 전환기간 연장은 제한적인 유예를 제공하지만, 여전히 기업은 새로운 조달 기준에 포함된 엄격한 환경 요건을 충족해야 합니다. 지속가능성을 중시하는 병원은 입찰의 일부로 라이프사이클 분석 및 재활용 가능한 포장재를 요구하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성질환과 생활습관병의 부담증

- 저침습 수술에의 기호의 고조

- 고령화에 의한 인공관절 치환술의 급증

- 3D 프린팅에 의한 환자 전용 임플란트의 급증

- 생체 흡수성 및 스마트 센서 대응 임플란트의 상업화

- 밸류 베이스 케어 번들이 EM에서의 임플란트의 보급을 촉진

- 시장 성장 억제요인

- 고급 임플란트의 높은 초기 비용

- 불리한/단편적인 상환 경로

- 특수 생체 재료공급 체인 취약성

- 승인을 지연시키는 ESG 및 라이프사이클 영향 조사

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 바이오 임플란트 유형별

- 심혈관 임플란트

- 정형외과 임플란트

- 척추 임플란트

- 치과 임플란트

- 안과 임플란트

- 신경 및 인공 내이 임플란트

- 기타 임플란트

- 재료별

- 금속과 합금

- 폴리머

- 세라믹 & 생체 활성 유리

- 복합 및 하이브리드 바이오 소재

- 기타 재료

- 유래별

- 자가이식

- 동종이식편

- 이종이식편

- 합성/인공

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Johnson & Johnson(DePuy Synthes)

- Medtronic PLC

- Abbott Laboratories

- Zimmer Biomet

- Stryker Corporation

- Boston Scientific Corporation

- Edwards Lifesciences

- BIOTRONIK

- Smith & Nephew

- Straumann Holding AG

- Dentsply Sirona

- Cochlear Limited

- Bausch & Lomb

- aap Implantate AG

- Endo International PLC

- MiMedx Group

- LifeNet Health

- Arthrex Inc.

- Globus Medical

- NuVasive

- Exactech

- Commed Corporation

제7장 시장 기회와 전망

SHW 25.10.28The global bio-implants market stood at USD 152.58 billion in 2025 and is forecast to reach USD 222.19 billion by 2030, advancing at a 7.81% CAGR.

Rapid uptake is driven by population aging, surging chronic-disease prevalence, and the routine use of sensor-enabled devices that transmit real-time clinical data to care teams. Demand is reinforced by 3-D-printed patient-specific constructs that shorten theatre time and enhance post-operative outcomes, while bioresorbable materials eliminate follow-up extraction surgeries. Health-system moves toward value-based reimbursement are accelerating adoption in emerging economies where providers focus on total-episode cost rather than device price alone. Competitive intensity is rising as major suppliers acquire niche innovators to assemble complete musculoskeletal and cardiovascular portfolios.

Global Bio-Implants Market Trends and Insights

Rising Burden of Chronic & Lifestyle Diseases

Diabetes, cardiovascular disease, and musculoskeletal disorders are reshaping demand patterns. Genentech's Susvimo received United States Food and Drug Administration (FDA) approval in 2025 as the first continuous ocular drug-delivery implant needing only twice-yearly refills, underscoring how multifunctional devices now address chronic pathologies with fewer interventions. Healthcare systems in high-income countries are pivoting toward proactive management, favoring long-lasting implants that reduce rehospitalization.

Growing Preference for Minimally-Invasive Surgeries

Ambulatory surgery centers performed 44 million procedures in 2024 and will keep expanding as payers reimburse outpatient joint replacements. Implant manufacturers respond by creating devices optimized for shorter operative windows and same-day discharge protocols, increasing the addressable bio-implants market well beyond traditional hospital theatres.

High Upfront Cost of Advanced Implants

Premium sensor-based devices remain expensive, making payers hesitate in regions where capital budgets are constrained. Suppliers are developing tiered portfolios so health systems can match functionality to economic reality without halting innovation.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population Accelerating Joint-Replacement Volumes

- Surge in 3-D-Printed, Patient-Specific Implants

- Unfavorable / Fragmented Reimbursement Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Orthopedic devices represented the single-largest revenue block in 2024, contributing 28.12% of the bio-implants market share. Cardiovascular implants, however, deliver the highest momentum with an 8.54% CAGR, powered by transcatheter valves and implantable hemodynamic sensors. The segment benefits from FDA breakthrough-device designations such as BiVACOR's total artificial heart that target end-stage failure. Over the forecast horizon, smart pacemakers integrated with remote telemetry will further enlarge the cardiovascular footprint within the bio-implants market.

Orthopedic innovation stays robust through robotic guidance and improved tribology that extends bearing life. Neuro-stimulators leverage adaptive algorithms to recalibrate in response to patient feedback, while cochlear implants inch toward fully implantable form factors; the category is projected to reach USD 940.1 million by 2030. Ophthalmic platforms like Susvimo re-shape treatment frequency expectations, reinforcing steady demand across all implant lines.

Metals and alloys accounted for 44.34% of 2024 revenue thanks to titanium's unmatched strength-to-weight ratio, but composites will grow the fastest at 8.43% as polyether-ether-ketone (PEEK) and polylactic acid (PLA) variants mitigate stress shielding. Ceramics doped with antimicrobial silver ions diminish infection risk, and bio-active glass matrices encourage osteogenesis without inflammatory cascade. Gradient builds that shift from rigid cores to compliant outer zones imitate natural tissue and broaden indications for soft-tissue repair.

Global Bio Implants Market is Segmented by Type of Bio-Implants (Cardiovascular Implants, Orthopedic Implants, Spinal Implants, and More), Material (Metals & Alloys, Polymers, and More), Origin (Autograft, Allograft, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 48.67% of global revenue in 2024 as reimbursement parity and advanced R&D ecosystems speed adoption of closed-loop neuro-stimulators like Medtronic's BrainSense platform, cleared by the FDA in 2025. Cross-border patient flows from Canada and Mexico further support procedure growth while diversified payer mixes stabilize price realization.

Asia-Pacific is the fastest-moving bio-implants market at an 8.45% CAGR. China supports domestic manufacturing, India aligns its regulatory code with international standards, and Japan's super-aged society prioritizes joint and cardiac devices. Digital health infrastructure in South Korea accelerates remote monitoring uptake, and Australian research hubs host pivotal trials that de-risk regional launches.

Europe wrestles with Medical Device Regulation (MDR) certification bottlenecks-only 43 notified bodies oversee half-a-million devices-slowing market entry. Transition extensions to 2027 grant limited reprieve, yet firms must still meet stringent environmental requirements incorporated into new procurement criteria. Sustainability-minded hospitals increasingly request lifecycle analyses and recyclable packaging as part of tender bids.

- Johnson & Johnson

- Medtronic

- Abbott Laboratories

- Zimmer Biomet

- Stryker

- Boston Scientific

- Edward Lifesciences

- BIOTRONIK

- Smiths Group

- Straumann Group

- Dentsply Sirona

- Cochlear

- Bausch Health

- AAP Implantate

- Endo International

- MiMedx Group

- LifeNet Health

- Arthrex

- Globus Medical

- NuVasive

- Exactech

- Conmed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic & Lifestyle Diseases

- 4.2.2 Growing Preference for Minimally-invasive Surgeries

- 4.2.3 Aging Population Accelerating Joint-replacement Volumes

- 4.2.4 Surge in 3-D-printed, Patient-specific Implants

- 4.2.5 Commercialization of Bioresorbable & Smart Sensor-enabled Implants

- 4.2.6 Value-based-care Bundles Boosting Implant Uptake in EMs

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Advanced Implants

- 4.3.2 Unfavorable/Fragmented Reimbursement Pathways

- 4.3.3 Supply-chain Vulnerability for Specialty Biomaterials

- 4.3.4 ESG & Lifecycle-impact Scrutiny Delaying Approvals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Type of Bio-Implants

- 5.1.1 Cardiovascular Implants

- 5.1.2 Orthopedic Implants

- 5.1.3 Spinal Implants

- 5.1.4 Dental Implants

- 5.1.5 Ophthalmic Implants

- 5.1.6 Neurological & Cochlear Implants

- 5.1.7 Other Implants

- 5.2 By Material

- 5.2.1 Metals & Alloys

- 5.2.2 Polymers

- 5.2.3 Ceramics & Bio-active Glass

- 5.2.4 Composite & Hybrid Biomaterials

- 5.2.5 Other Materials

- 5.3 By Origin

- 5.3.1 Autograft

- 5.3.2 Allograft

- 5.3.3 Xenograft

- 5.3.4 Synthetic / Prosthetic

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Clinics

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Johnson & Johnson (DePuy Synthes)

- 6.4.2 Medtronic PLC

- 6.4.3 Abbott Laboratories

- 6.4.4 Zimmer Biomet

- 6.4.5 Stryker Corporation

- 6.4.6 Boston Scientific Corporation

- 6.4.7 Edwards Lifesciences

- 6.4.8 BIOTRONIK

- 6.4.9 Smith & Nephew

- 6.4.10 Straumann Holding AG

- 6.4.11 Dentsply Sirona

- 6.4.12 Cochlear Limited

- 6.4.13 Bausch & Lomb

- 6.4.14 aap Implantate AG

- 6.4.15 Endo International PLC

- 6.4.16 MiMedx Group

- 6.4.17 LifeNet Health

- 6.4.18 Arthrex Inc.

- 6.4.19 Globus Medical

- 6.4.20 NuVasive

- 6.4.21 Exactech

- 6.4.22 Conmed Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment