|

시장보고서

상품코드

1836632

자동차 클러치 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Clutch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

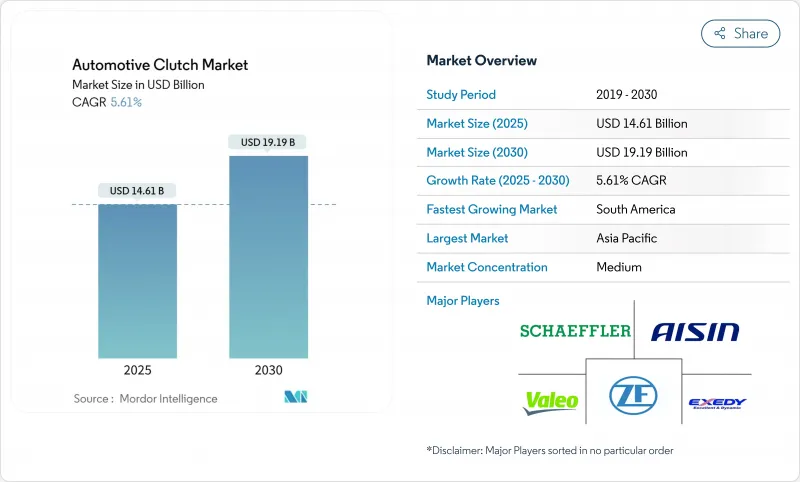

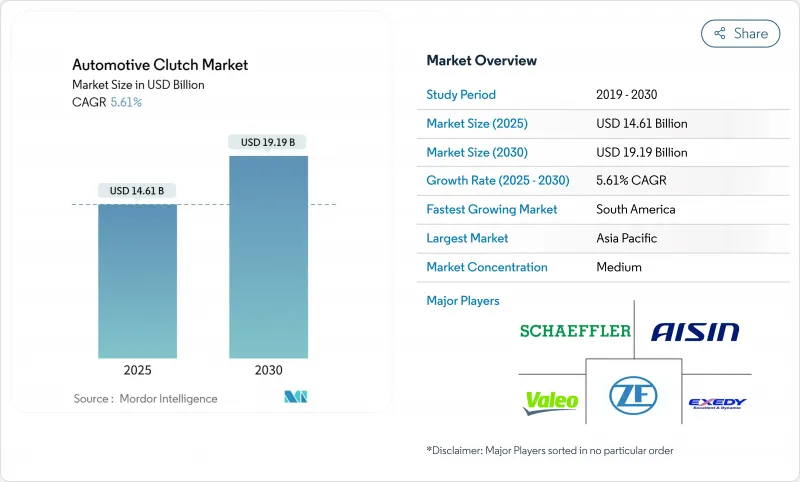

자동차 클러치 시장의 2025년 시장 규모는 146억 1,000만 달러, 2030년에는 191억 9,000만 달러에 이르고, CAGR 5.61%로 확대될 것으로 예측되고 있습니다.

DCT 기술의 채택, 세계 CO2 규제 강화, 아시아태평양을 중심으로 한 경차 생산의 견고한 성장이 이 전망을 뒷받침하고 있습니다. 신형 차량은 마일드 하이브리드 시스템과 전자 제어 액추에이션의 조합이 늘어나 시프트 속도와 효율이 향상되어 OEM 수준 수요가 대부분을 차지하고 있습니다. 한편, 자동차 보유 대수가 12년 이상 경과해, 배터리 전기자동차(BEV)에 의해 종래의 마찰 클러치의 설치 대수가 감소해도 교환 수요가 유지되고 있기 때문에 애프터마켓의 대수는 계속 견고합니다. 경쟁의 역학은 변화하고 있습니다. 주요 공급업체는 하이브리드 아키텍처를 지원하기 위해 기계적 노하우와 소프트웨어 및 전자 제품을 결합하여 공유를 보호하려고 합니다. 가장 두드러진 예로는 Sheffler와 Vitesco Technologies의 합병이 있습니다.

세계 자동차 클러치 시장 동향 및 통찰

듀얼 클러치 및 자동 변속기로의 빠른 OEM 시프트

DCT의 효율은 토크 컨버터형 자동 변속기보다 최대 28% 뛰어나므로 자동차 제조업체는 성능을 저하시키지 않고 차량의 CO2 목표를 달성할 수 있어 프리미엄 부문에서 대중 시장 부문으로의 광범위한 전환을 촉진하고 있습니다. 컴포넌트의 공통화가 진행됨에 따라 단가가 낮아지고, 6단과 8단의 DCT가 B부문나 C부문의 자동차에 채택되고 있습니다. Magna의 48V DCT와 같은 하이브리드 자동차는 연소와 전기 추진을 긴밀한 패키징으로 통합하여 더욱 부드러운 엔진 오프 코스를 가능하게합니다. 상용차 OEM은 장거리 노선의 연료 소비를 줄이기 위해 하이브리드 자동 매뉴얼을 채택하여 더 높은 열용량을 가진 헤비 듀티 클러치에 대한 수요를 강화하고 있습니다.

신흥경제국에서 소형차 생산 증가

자동차 제조업체가 드라이브 트레인을 현지화하고 지역 공급망을 활용함으로써 중국과 인도의 조립 대수 확대가 핵심 수요를 유지합니다. 인도에서는 정부 우대 조치로 많은 수의 수동 클러치를 지정하는 새로운 공장이 장려되었지만 트림 수준 상승으로 자동화 옵션이 통합되어 프리미엄 마찰재의 기회가 증가하고 있습니다. 중국에서는 2024년 난기류 이후 생산이 안정되고 현지 브랜드는 경쟁력을 유지하기 위해 DCT를 채택하여 단위 가치 증가를 견인하고 있습니다. 아시아 이외에서는 브라질과 멕시코가 신뢰할 수 있는 부품 교체 사이클을 촉진하는 기반이 되었습니다. 도시화가 진행됨에 따라 Tier-2 및 Tier-3 도시에서 라이드 헤일링의 함대가 증가하고 정지 및 고의 의무로 마모가 가속화되고 애프터마켓의 수가 증가합니다.

BEV의 보급이 가속되고 기존의 클러치가 폐지됨

중국은 10년 후까지 신차 판매에 차지하는 EV의 비율을 45%로 하는 것을 목표로 하고 있으며, 유럽의 OEM은 적극적인 전동화 로드맵을 전개해 기존의 마찰 클러치를 고정비의 e-drive 커플링으로 직접 대체하고 있습니다. 그럼에도 불구하고 하이브리드 아키텍처에서는 고속도로 순항 중에 엔진을 분리하기 위해 디스커넥트 클러치가 여전히 사용되고 있습니다. 클러치 기반 하이브리드 기어 세트에 대한 General Motors의 특허 활동은 전동화된 드라이브 라인에서도 정교한 맞물림 시스템의 필요성이 계속되고 있음을 보여줍니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 엄격한 CO2 목표가 연비 효율이 높은 클러치에 대한 수요를 촉진

- 마일드 하이브리드 아키텍처에 48V e-클러치 시스템의 채택

- 엔트리 레벨 자동차에서 CVT 파워트레인의 인기 상승

부문 분석

2024년 자동차 클러치 시장의 65.10%는 여전히 수동 유닛에서 차지하고 있지만, 2025-2030년의 CAGR 9.19%로 듀얼 클러치 변속기가 가장 급성장하는 부문으로 부상했습니다. 이 성장은 비용 격차가 줄어들고 규제 압력이 효율적으로 보상되는 컴팩트 자동차에서의 주류 채택으로 인한 것입니다. 듀얼 클러치 시스템의 자동차 클러치 시장 규모는 엔진 회전수를 보다 엄격하게 제어하면서 성능을 유지하는 8단 설계와 연동하여 상승할 것으로 예측됩니다.

2페달 아키텍처에서 공급업체는 공회전 시 드래그 토크를 제한하는 저관성 허브와 높은 전도성 라이너가 있는 마찰 팩을 재설계합니다. Zet-Ef의 8단 습식 DCT는 28%의 손실 감소를 실현하고 마일드 하이브리드 P2 구성을 지원하는 기술 변화를 보여줍니다. 대형 트럭의 자동 수동 변속기(AMT)는 고열 유기 라이닝과 결합 된 단일 또는 트윈 카운터 샤프트를 채택하고 함대 운영자에게 풀 하이브리드 비용없이 연료를 절약 할 수있는 옵션을 제공합니다. 이러한 동향을 맞추면 클러치 기술의 폭넓은 다양성이 유지되고 자동차 클러치 시장 전체의 기세가 10년간 유지됩니다.

승용차는 2024년에 수요의 74.57%를 공급하지만, 하이브리드 드라이브트레인이 지역 운송과 도시 배송에서 급증함에 따라 중형 및 대형 트럭이 연평균 7.88%로 가장 빠르게 증가하고 있습니다. 헤비 듀티 플랫폼과 관련된 자동차 클러치 시장 규모는 1대당 단가가 높다는 장점이 있습니다. 이는 그라디언트에서의 발진시 토크 피크를 처리하기 위해 다판 팩과 더 큰 열 질량이 필요하기 때문입니다.

DT12 및 i-Shift와 같은 자동 매뉴얼을 위해 설계된 이튼 헤비 듀티 클러치는 이 기회를 강조하고 정지 시작 의무 하에서 열을 방출하는 고속 공기 흐름 설계를 포함합니다. 수소 연료 트럭의 조종사는 단단 기어 박스와 펌프와 압축기를 분리하는 분리 클러치를 결합하여 다른 틈새를 제공합니다. 승용차의 하이브리드 파워트레인은 엔진 및 변속기 사이에 P2 또는 P3 모듈을 삽입하여 전기 항행을 가능하게 함으로써 클러치의 관련성을 확장합니다. 그 결과, 자동차 클러치 시장은 BEV가 확대되어도 차량 클래스 전체에서 균형 잡힌 노출을 유지하고 있습니다.

지역 분석

아시아태평양은 2024년에 자동차 클러치 시장에서 49.65%의 점유율을 유지해 중국의 생산규모와 인도 정책에 힘입어 제조업 증가에 지지되고 있습니다. 2030년까지의 지역별 CAGR 5.41%로 안정된 내연기관 수요에 더해 하이브리드의 전개가 가속하고 있는 것을 반영하고 있습니다. 전자 액추에이션의 리더인 일본과 한국은 통합 전자 클러치 모듈을 지정하여 평균 단가 상승을 견인합니다. ASEAN의 어셈블러는 세계 OEM이 공급망을 다양화하고 클러치의 현지 조달을 대규모로 확보함으로써 새로운 투자를 유치합니다.

남미는 CAGR 6.77%에서 가장 급성장하고 있는 지역입니다. 브라질을 포함한 남미 국가에서는 자동차 인구가 증가하고 있으며 견고한 교환 대수를 유지하고 있습니다. 새로운 지역 무역 인센티브가 새로운 운송 능력 확보를 촉구하고 도시 지역의 화물 전기 시험에 하이브리드 AMT가 도입되어 차량 1대당 운송량이 증가합니다. 아르헨티나의 노후화된 차량은 독립형 애프터마켓에 크게 의존하고 있으며 공급업체는 OEM 채널 이외에도 폭넓게 진입하고 있습니다.

북미와 유럽의 CAGR은 각각 3.21%와 2.81%로 완만하지만, 두 지역 모두 가장 엄격한 배출가스 규제와 입자상물질 규제를 부과하고 있습니다. 미국의 CAFE 지침은 연간 2%의 효율 향상을 규정하고 있으며, OEM은 마일드 하이브리드 모듈과 고효율 클러치의 조합을 장려하고 있습니다. 유럽의 유로 7 규제는 브레이크와 클러치의 마모 분말을 제한하는 것으로, 구리를 사용하지 않는 라이닝과 경량 플레이트의 채택을 가속시키고 있습니다. 러시아와 중동 및 아프리카는 현지 조립과 도시 지역의 소유율 상승과 관련된 증가 성장에 기여합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 듀얼 클러치 및 자동 변속기로의 급속한 OEM 시프트

- 신흥국의 소형 자동차 생산 증가

- 엄격한 CO2 목표가 저연비 클러치 수요를 촉진

- 마일드 하이브리드 아키텍처용 48V e-클러치 시스템의 채택

- 차량 전체의 MPG 기준을 충족하기 위한 경량 복합 마찰재

- Tier2/3 도시에 있어서의 배기가스 규제 대응 택시의 후부 수요 증가

- 시장 성장 억제요인

- 기존 클러치를 배제하는 BEV의 보급 확대

- 엔트리 카에서 CVT 파워트레인의 인기 상승

- 듀얼 매스 플라이휠의 신뢰성 문제에 의한 보증 비용의 상승

- 공급 체인을 혼란시키는 마찰재 구리 프리의 의무화

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측(금액, 억미 달러)

- 변속기 유형별

- 매뉴얼

- 자동 변속기(토크 컨버터)

- 자동 수동 변속기(AMT)

- 듀얼 클러치 변속기(DCT)

- 기타(e클러치, CVT 클러치팩 등)

- 차종별

- 승용차

- 소형 상용차

- 중대형 상용차

- 오프 하이웨이(농업용, 건설용)

- 클러치 컴포넌트별

- 클러치 디스크 & 허브

- 압력판과 커버

- 릴리즈 베어링/슬레이브 실린더

- 플라이휠(싱글 및 듀얼 매스)

- 액추에이션 시스템(유압식, 전기 유압식, 전자식)

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Schaeffler AG

- Valeo SA

- ZF Friedrichshafen AG

- EXEDY Corporation

- Aisin Corporation

- Eaton Corporation plc

- BorgWarner Inc.

- Magneti Marelli SpA

- Continental AG

- LuK

- WABCO(ZF CV Systems)

- Setco Automotive Ltd.

- FCC Co., Ltd.

- Zhejiang Tieliu Clutch Co., Ltd.

- Nissin Kogyo Co., Ltd.

- Haldex AB

- Twin Disc Inc.

- Transtar Industries Inc.

- Helix Auto Transmission

- Sachs

제7장 시장 기회와 전망

SHW 25.10.28The automotive clutch market is valued at USD 14.61 billion in 2025 and is forecast to reach USD 19.19 billion by 2030, expanding at a 5.61% CAGR.

DCT technology adoption, tightening global CO2 rules, and steady light-vehicle production growth, particularly in Asia-Pacific, underpin this outlook. OEM-level demand dominates because new models increasingly pair mild-hybrid systems with electronic actuation that improves shift speed and efficiency. Meanwhile, aftermarket volumes remain resilient as vehicle fleets age well past 12 years, sustaining replacement demand even as battery-electric vehicles (BEVs) reduce installations of conventional friction clutches. Competitive dynamics are changing: leading suppliers are bundling mechanical know-how with software and electronics to protect their share while positioning for hybrid architectures, most visibly in Schaeffler's merger with Vitesco Technologies, which folds power electronics into a historic clutch portfolio.

Global Automotive Clutch Market Trends and Insights

Rapid OEM Shift Toward Dual-Clutch & Automated Transmissions

DCT efficiency advantages of up to 28% over torque-converter automatics allow carmakers to hit fleet CO2 targets without detracting from performance, prompting broad migration from premium to mass-market segments. Unit costs fall as component commonality rises, making six- and eight-speed DCTs viable for B- and C-segment cars. Hybrid variants such as Magna's 48 V DCT merge combustion and electric propulsion within tight packaging, enabling smoother engine-off coasting. Commercial-vehicle OEMs adopt hybrid automated manuals to cut fuel burn on long-haul routes, reinforcing demand for heavy-duty clutches with higher thermal capacity.

Rising Light-Vehicle Production in Emerging Economies

Expanding assembly volumes in China and India sustain core demand as automakers localize drivetrains and leverage regional supply chains. Government incentives in India encourage new plants that specify high-volume manual clutches, yet rising trim levels integrate automated options, adding premium friction-material opportunities. In China, output stabilized after 2024 turbulence, and local brands now adopt DCTs to stay competitive, driving incremental unit value. Outside Asia, Brazil and Mexico collectively field a base that fuels a dependable parts replacement cycle. Urbanization accelerates ride-hailing fleets in Tier-2 and Tier-3 cities, where stop-and-go duty accelerates wear and lifts aftermarket volumes.

Escalating BEV Penetration Eliminating Conventional Clutches

China targets a 45% EV share of new-vehicle sales by decade-end, and European OEMs deploy aggressive electric roadmaps, directly substituting the traditional friction clutch with fixed-ratio e-drive couplings. Nonetheless, hybrid architectures still use disconnect clutches to de-link engines at highway cruise. Patent activity from General Motors on clutch-based hybrid gearsets demonstrates the ongoing need for sophisticated engagement systems even in electrified drivelines.

Other drivers and restraints analyzed in the detailed report include:

- Stringent CO2 Targets Driving Demand for Fuel-Efficient Clutches

- Adoption of 48-V e-Clutch Systems for Mild-Hybrid Architectures

- Rising Popularity of CVT Powertrains in Entry-Level Cars

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual units still represented 65.10% of the automotive clutch market in 2024, yet the dual-clutch transmissions emerged as the fastest-growing segment at 9.19% CAGR from 2025-2030. That growth rides on mainstream adoption in compact cars, where cost gaps have narrowed and regulatory pressure rewards efficiency. The automotive clutch market size for dual-clutch systems is forecast to rise in tandem with eight-speed designs that maintain performance while controlling engine speed more tightly.

Across two-pedal architectures, suppliers are re-engineering friction packs with low-inertia hubs and high-conductivity liners that limit drag torque at idle. ZF's 8-speed wet DCT illustrates the technology shift, offering 28% loss reduction and supporting mild-hybrid P2 configurations. Automated manual transmissions (AMTs) in heavy trucks deploy single or twin countershafts coupled with high-heat organic linings, giving fleet operators a fuel-saving alternative without the cost of full hybrids. Together, these trends sustain broad diversity in clutch technology and preserve overall automotive clutch market momentum through the decade.

Passenger cars delivered 74.57% of demand in 2024, but medium and heavy trucks are the fastest-rising slice, expanding at 7.88% CAGR as hybrid drivetrains proliferate in regional haul and urban delivery. The automotive clutch market size attached to heavy-duty platforms benefits from higher unit value per vehicle, since multi-plate packs and greater thermal mass are needed to handle torque peaks during launch on grades.

Eaton's heavy-duty clutches, engineered for automated manuals such as DT12 and I-Shift, underscore this opportunity and include high-velocity airflow designs that dissipate heat under stop-start duty. Hydrogen-fuel truck pilots pair single-stage gearboxes with disconnect clutches that isolate pumps and compressors, offering another niche. In passenger cars, hybrid powertrains extend clutch relevance by inserting P2 or P3 modules between the engine and transmission to enable electric sailing. Consequently, the automotive clutch market maintains a balanced exposure across vehicle classes even as BEVs expand.

The Automotive Clutch Market Report is Segmented by Transmission Type (Manual, Automatic, AMT, DCT, and More), Vehicle Type (Passenger Cars, LCV, and More), Clutch Component (Clutch Disc and Hub, Pressure Plate and Cover, Release Bearing/Slave Cylinder, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific maintained a 49.65% share of the automotive clutch market in 2024, underpinned by China's production scale and India's policy-fueled manufacturing uptick. Regional CAGR of 5.41% through 2030 reflects stable internal combustion demand plus accelerating hybrid rollouts. Japan and South Korea, leaders in electronic actuation, drive higher average unit value by specifying integrated e-clutch modules. ASEAN assemblers attract new investment as global OEMs diversify supply chains, ensuring localized clutch sourcing at scale.

South America is the fastest-growing geography at 6.77% CAGR, fueled by a larger vehicle population in Brazil and other South American countries that sustains robust replacement volumes. New regional trade incentives spark fresh capacity commitments, while urban freight electrification trials integrate hybrid AMTs that lift content per vehicle. Argentina's aging fleet leans heavily on the independent aftermarket, widening supplier exposure beyond OEM channels.

North America and Europe show modest 3.21% and 2.81% CAGRs, respectively, yet both regions impose the toughest emissions and particulate rules. CAFE mandates in the United States stipulate 2% annual efficiency gains, encouraging OEMs to pair mild-hybrid modules with high-efficiency clutches. European Euro 7 standards limit brake and clutch wear particles, accelerating the adoption of copper-free linings and lightweight plates. Russia and the Middle East and Africa contribute incremental growth tied to localized assembly and rising urban ownership.

- Schaeffler AG

- Valeo SA

- ZF Friedrichshafen AG

- EXEDY Corporation

- Aisin Corporation

- Eaton Corporation plc

- BorgWarner Inc.

- Magneti Marelli SpA

- Continental AG

- LuK

- WABCO (ZF CV Systems)

- Setco Automotive Ltd.

- FCC Co., Ltd.

- Zhejiang Tieliu Clutch Co., Ltd.

- Nissin Kogyo Co., Ltd.

- Haldex AB

- Twin Disc Inc.

- Transtar Industries Inc.

- Helix Auto Transmission

- Sachs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid OEM shift toward dual-clutch and automated transmissions

- 4.2.2 Rising light-vehicle production in emerging economies

- 4.2.3 Stringent CO2 targets driving demand for fuel-efficient clutches

- 4.2.4 Adoption of 48-V e-clutch systems for mild-hybrid architectures

- 4.2.5 Lightweight composite friction materials to meet fleet-wide MPG norms

- 4.2.6 Growing retrofit demand in Tier-2/3 cities for emission-compliant taxis

- 4.3 Market Restraints

- 4.3.1 Escalating BEV penetration eliminating conventional clutches

- 4.3.2 Rising popularity of CVT powertrains in entry-level cars

- 4.3.3 Dual-mass-flywheel reliability issues causing warranty cost spikes

- 4.3.4 Upcoming copper-free friction-material mandates disrupting supply chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Transmission Type

- 5.1.1 Manual

- 5.1.2 Automatic (Torque-Converter)

- 5.1.3 Automated Manual Transmission (AMT)

- 5.1.4 Dual-Clutch Transmission (DCT)

- 5.1.5 Others (e-Clutch, CVT Clutch Packs, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Off-Highway (Agricultural and Construction)

- 5.3 By Clutch Component

- 5.3.1 Clutch Disc and Hub

- 5.3.2 Pressure Plate and Cover

- 5.3.3 Release Bearing/Slave Cylinder

- 5.3.4 Flywheel (Single and Dual-Mass)

- 5.3.5 Actuation Systems (Hydraulic, Electro-Hydraulic, Electronic)

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Schaeffler AG

- 6.4.2 Valeo SA

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 EXEDY Corporation

- 6.4.5 Aisin Corporation

- 6.4.6 Eaton Corporation plc

- 6.4.7 BorgWarner Inc.

- 6.4.8 Magneti Marelli SpA

- 6.4.9 Continental AG

- 6.4.10 LuK

- 6.4.11 WABCO (ZF CV Systems)

- 6.4.12 Setco Automotive Ltd.

- 6.4.13 FCC Co., Ltd.

- 6.4.14 Zhejiang Tieliu Clutch Co., Ltd.

- 6.4.15 Nissin Kogyo Co., Ltd.

- 6.4.16 Haldex AB

- 6.4.17 Twin Disc Inc.

- 6.4.18 Transtar Industries Inc.

- 6.4.19 Helix Auto Transmission

- 6.4.20 Sachs

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment