|

시장보고서

상품코드

1836637

자동차용 공압 액추에이터 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Pneumatic Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

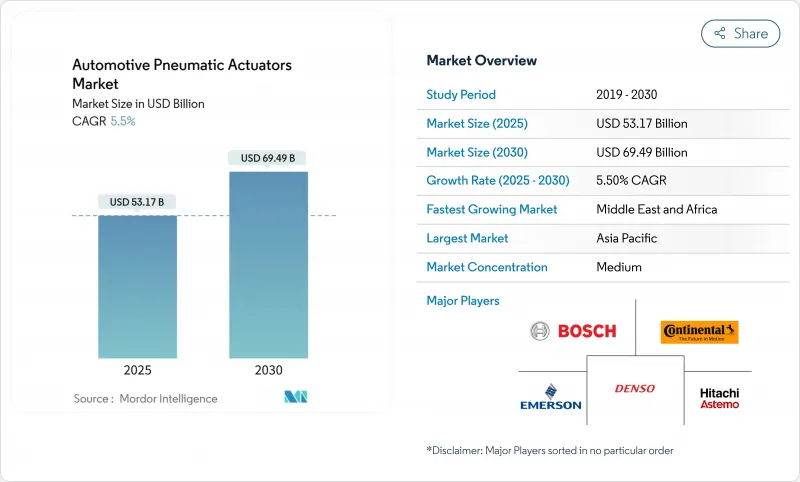

자동차용 공압 액추에이터 시장 규모는 2025년에 531억 7,000만 달러, 예측 기간(2025-2030년)의 CAGR은 5.50%를 나타내고, 2030년에는 694억 9,000만 달러에 달할 것으로 예측됩니다.

에너지 효율적인 전동 액추에이터와의 경쟁에도 불구하고 자동차 제조업체는 안전, 파워트레인 및 섀시의 기능을 공압 장비에 의존하고 있습니다. 배기가스 규제의 엄격화와 ADAS의 채택 확대가 수요를 견인하고, 아시아태평양은 강력한 공급망에 의해 선도하고 있습니다. 동시에 중동 및 아프리카, 남미에서는 현지 조립 프로그램의 확대로 급성장을 하고 있습니다.

세계 자동차용 공압 액추에이터 시장 동향 및 통찰

배기가스 규제 강화가 정밀한 공연비 제어를 촉진

2024년에 시행되는 미국 환경보호청(EPA)의 대형차 규제 3단계에서는 NOx 기준치가 강화되므로 디젤 제조업체는 고해상도 공압 밸브에 의존하는 EGR 및 투약 전략을 개량할 필요가 있습니다. 유럽에서는 비슷한 Euro 7 초안이 수요 피크를 유발합니다. 실험실에서의 테스트를 대신하여 현장에서의 검증 테스트를 실시하게 되어, 액추에이터는 실제의 진동이나 온도 변화하에서도 정밀도를 유지해야 합니다. 디지털 피드백 루프를 닫는 전공식 패키지가 있는 공급업체는 입찰에서 명확한 이점을 누릴 수 있습니다. 규제 일정은 낙찰 결정을 가속화하고 예측 기간 동안 수익 가시성을 보장합니다.

세계 자동차 생산 증가

경량 및 중장비 물량이 증가함에 따라 조립된 모든 유닛이 여러 개의 액추에이터 포인트를 운반하기 때문에 모든 공압 애플리케이션에서 기본 수요가 증가합니다. 일본 자동차 공업회는 2025년을 위한 OEM 일정에 연비 효율과 컴플라이언스를 보장하기 위해 브레이크, 스로틀 및 EGR 회로에 공압 솔루션을 통합하는 것을 확인했습니다. 하나의 액추에이터 패밀리가 형제 차종에 걸쳐 설치될 수 있게 되어, 공급자에게 있어서의 스케일 메리트가 높아졌기 때문에 플랫폼의 공유화는 더욱 대수를 확대합니다. 구미 제조업체는 최종 조립의 거점을 동남아시아에 옮기려고 하고 있어, 액추에이터 제조업체에 모듈 라인의 병설을 촉구하고 있습니다. 따라서, 라이벌이 되는 전동 액추에이터가 그 비용 제안을 보다 선명하게 하고 있음에도 불구하고, 생산의 회복에 의해 자동차용 공압 액추에이터 시장의 당면의 성장은 확실하게 되고 있습니다.

에너지 효율적인 전동 액추에이터로의 전환

전자 기계 시스템은 배터리 전력을 최대 80%의 효율로 운동으로 변환합니다. 와트를 절약할 때마다 항속 거리가 늘어나는 전기자동차에서는 이 차이가 더욱 두드러집니다. 라인 빌더는 또한 용접 로봇과 자재관리 암을 전동 실린더로 이동시켜 경로 정밀도를 높입니다. 그러나 대형 트럭의 드럼 브레이크와 같이 압축 공기가 이미 차량 플랫폼과 통합되어있는 큰 하중 노드에서는 여전히 공압이 지배적입니다. 따라서 공급업체는 압력 기반 힘을 유지하면서 저에너지 위치 제어를 통합한 혼합 기술 액추에이터를 향해 연구 개발을 진행하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 정확한 액추에이션을 요구하는 ADAS의 보급

- 연비 향상을 위한 경량화의 동향

- 공압의 복잡성과 높은 유지 보수 비용

부문 분석

브레이크 챔버와 주차 브레이크 캘리퍼스 유닛은 2024년 자동차용 공압 액추에이터 시장에서 31.50%의 점유율을 차지합니다. 그 존재는 모든 승용차와 상용차의 변형에서 의무화되어 있으며 기본 물량이 확보됩니다. 전기 기계식 주차 브레이크는 고급 세단에 침투하고 있지만, 대형 트럭의 드럼 브레이크는 여전히 낮은 단가와 높은 클램핑력을 발휘하는 공기 챔버에 의존하고 있습니다. 터보차저의 웨이스트 게이트 액추에이터는 가장 빠르게 성장하며 CAGR로 6.70%로 성장을 지속하고, 있습니다. 스로틀 밸브, HVAC 블렌드 도어, EGR 버터플라이는 한 자릿수 중반의 성장을 유지하며 각각 규제 또는 편안함의 필요성을 지원합니다.

공압식 연료 분사 레일 레귤레이터는 브라질에서 인기 있는 플렉스 연료 레이아웃으로 살아남으며, 도어록 플런저는 비용에 중점을 둔 해치백에서 흔히 남아 있습니다. 공급업체는 액추에이터 본체에 스마트 압력 센서를 내장하고 건강 데이터를 차량 제어 네트워크에 공급하는 실험을 수행하고 있습니다. 직접적인 전기 모터 구동이 경쟁력의 차이를 줄이는 동안에도, 이러한 강화는 공압 구동 장치의 관련성을 길게 만듭니다. 전반적으로 자동차용 공압 액추에이터 시장이 2자리억 달러의 매출을 유지하는 이유는 용도 조합에 있습니다.

승용차는 2024년 매출의 56.70%를 차지하며, 이는 세계 공장에서 생산량이 많음을 반영합니다. 그러나 대형 상용차는 CAGR 5.90%로 자동차용 공압 액추에이터 시장 규모 확대를 견인할 것으로 예측되고 있습니다. 플리트 오퍼레이터는 극심한 듀티 사이클 하에서 에어 브레이크 및 에어 서스펜션 회로의 내구성을 높이 평가하고, 한편으로는 보다 엄격한 CO2 규제로 기술의 전반적인 교환보다 컴프레서의 최적 관리가 요구되고 있습니다. 소형 상업용 밴은 전자상거래의 소포 수요를 추적하고 도시 물류 성장을 배경으로 견고한 CAGR을 달성합니다. 건설 기계와 광산기계는 주로 고온 배기 플랩 제어 장치와 견고한 스티어링 스태빌라이저를 요구합니다.

이륜차는 여전히 일부 아시아 경제권에 집중하는 마이크로 부문이지만 스쿠터의 OEM은 자동 클러치 작동용 저압 에어 서보를 시험하고 있습니다. 교외용 승용차는 NVH의 장점을 추구해 컴팩트한 전기 구동에 끌려가지만, 고부하 차량은 힘의 밀도와 입증된 보수성을 요구하여 공압을 유지합니다. 이 차이는 Tier-1 공급업체의 향후 플랫폼 전략을 형성하고 자격 증명 프로토콜을 다시 작성하지 않고 마이크로에서 헤비 듀티 정격까지 확장하는 모듈 식 제품군을 생산하는 것을 강력하게 합니다.

지역 분석

아시아태평양은 중국의 멀티브랜드 승용차 생산과 일본의 고정밀 밸브의 능력에 힘입어 2024년 세계 매출의 45.50%를 차지했습니다. 이 지역은 베트남, 태국, 인도공급 거점이 가치 곡선을 상승시키고 역내 조달이 세계 제조업체들에게 매력적이기 때문에 CAGR은 7.10%를 나타낼 것으로 예측되고 있습니다. 한국의 전공 R&D센터는 이 나라의 선진적인 반도체 에코시스템을 활용하여 압력 MEMS 센서를 액추에이터 PCB에 통합하여 경쟁력을 높이고 있습니다. 전기자동차의 보급에도 불구하고 비용 효율적으로 최적화된 서브 컴팩트 부문은 여전히 공압 구동 HVAC 및 터보 웨이스트 게이트 유닛을 탑재하고 있으며 공급업체에게 대수를 확보하고 있습니다.

중동 및 아프리카는 CAGR 7.80%로 가장 급성장하고 있는 클러스터입니다. 사우디아라비아의 '비전 2030' 산업 정책이 CKD 조립 라인을 유치해, 건설 붐에 대응하는 상용 트럭용의 액추에이터 컨텐츠의 현지화를 각 사가 요구하고 있습니다. 아랍에미리트(UAE)는 프리존 물류를 활용하여 예비 부품 키트를 아프리카 시장 깊숙이 재수출합니다. 튀르키예 유럽에 대한 세관조합 접근은 부품 수출을 뒷받침하며 공압 장비 공급업체는 이즈미르와 부르사 시설을 확장할 수밖에 없습니다. 이러한 역학은 조달의 방향성이 대륙 횡단 수송에서 시장 근방에서의 생산으로 전환되어 리드 타임의 단축과 화물 배출량의 삭감을 실현합니다.

남미에서는 이 지역 특유의 플렉스 연료 엔진 아키텍처가 에탄올의 혼합에 의해 연소 스토키가 매일 변화하기 때문에 EGR과 연료 레일 액추에이터 수요를 자극하고 있습니다. 다국적 공급업체는 씰 스택을 수입하는 것보다 미나스 제라이스 주에 엘라스토머 경화 프레스를 설치하도록 현지 조달 규제를 추진하고 있습니다. 아르헨티나의 대형 트럭 조립 공장은 통화 안정화 조치 후에 회복되어 대용량 브레이크 챔버 용으로 증가합니다. 환율 변동과 정치적 위험은 전망을 약화시키지만, 설치 기반 관성으로 인해 자동차용 공압 액추에이터 시장은 반구에서 견고합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 배기 가스 규제의 강화가 정밀한 공연비 제어를 촉진

- 세계 자동차 생산 증가

- 정확한 작동을 요구하는 ADAS의 보급

- 연비 향상을 위한 경량화 동향

- 수소 ICE의 밸브 타이밍 채택

- OTA 대응 액추에이터 소프트웨어의 수익화

- 시장 성장 억제요인

- 에너지 효율이 높은 전동 액추에이터로의 시프트

- 공압 액추에이터의 복잡성과 높은 유지 보수 비용

- 씰용 고급 엘라스토머의 부족

- 공압기기의 연구개발을 억제하는 Tier-1의 탈탄소화

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측 : 금액(달러)·수량(유닛)

- 용도 유형별

- 스로틀 액추에이터

- 연료 분사 액추에이터

- 브레이크 액추에이터

- 배기 가스 재순환 액추에이터

- 터보차저 웨이스트 게이트 액추에이터

- HVAC 액추에이터

- 도어록 액추에이터

- 기타

- 차종별

- 승용차

- 소형 상용차

- 중대형 상용차

- 오프 하이웨이 자동차

- 이륜차

- 액추에이터 기구별

- 싱글 다이어프램 공압

- 진공 부스트 공압

- 전공(EP)

- 서보 공압

- 랙&피니언

- 로터리 베인

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Emerson(ASCO Valve)

- Hitachi Astemo Ltd

- CTS Corporation

- Schrader Duncan Ltd

- Rotex Automation

- Nucon Industries Pvt Ltd

- Magneti Marelli SpA

- Mitsubishi Electric Corp

- Del-Tron Precision Inc

- Procon Engineering

- Valeo SA

- Aisin Corporation

- Mahle GmbH

- BorgWarner Inc

제7장 시장 기회와 전망

SHW 25.10.28The Automotive Pneumatic Actuators Market size is estimated at USD 53.17 billion in 2025, and is expected to reach USD 69.49 billion by 2030, at a CAGR of 5.50% during the forecast period (2025-2030).

Despite competition from energy-efficient electric actuators, vehicle makers continue to rely on pneumatic devices for safety, powertrain, and chassis functions. Stricter emission regulations and the growing adoption of ADAS drive demand, with Asia-Pacific leading due to strong supply chains. At the same time, the Middle East and Africa, as well as South America, see rapid growth from expanding local assembly programs.

Global Automotive Pneumatic Actuators Market Trends and Insights

Stricter emission norms driving precise air-fuel control

The US EPA's Phase 3 heavy-duty standards enacted in 2024 tighten NOx thresholds, compelling diesel makers to refine EGR and dosing strategies that rely on high-resolution pneumatic valves. Similar Euro 7 drafts trigger demand peaks in Europe. Field-valid testing replaces laboratory cycles, forcing actuators to sustain precision under real-world vibration and temperature excursions. Suppliers with electro-pneumatic packages that close the digital feedback loop enjoy distinct bidding advantages. The regulatory timetable accelerates award decisions, locking in revenue visibility for the forecast period.

Increasing global vehicle production

Rising light-duty and heavy-duty volumes lift baseline demand across all pneumatic applications because every unit assembled carries multiple actuator points. The Japan Automobile Manufacturers Association confirmed that OEM schedules for 2025 still embed pneumatic solutions in brake, throttle, and EGR circuits to assure fuel efficiency and compliance. Platform sharing further magnifies volumes because a single actuator family can now be fitted across sibling models, raising economies of scale for suppliers. Western manufacturers are repositioning final-assembly footprints toward Southeast Asia, which encourages actuator makers to co-locate module lines. The production rebound therefore secures near-term growth in the automotive pneumatic actuators market even as electric rivals sharpen their cost proposition.

Shift toward energy-efficient electric actuators

Electromechanical systems convert battery power into motion with up to 80% efficiency, dwarfing the 20% ceiling of air-driven counterparts. The delta becomes more pronounced in electric cars, where every watt saved extends range. Line-builders are also migrating their welding robots and material-handling arms to electric cylinders for tighter path accuracy. Yet pneumatics still dominates the highest-force nodes, such as heavy truck drum brakes, where compressed air is already integral to the vehicle platform. Consequently suppliers are channeling R&D toward mixed-technology actuators that preserve pressure-based force while embedding low-energy position control.

Other drivers and restraints analyzed in the detailed report include:

- ADAS proliferation demanding accurate actuation

- Lightweighting trend for fuel economy

- Complexity & high maintenance cost of pneumatics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake chambers and parking brake caliper units commanded 31.50% share of the automotive pneumatic actuators market in 2024. Their presence is mandated across every passenger and commercial vehicle variant, cementing baseline volume. Electromechanical parking brakes are penetrating luxury sedans, but heavy truck drum brakes still rely on air chambers that deliver high clamping force at low unit cost. Turbocharger wastegate actuators follow as the fastest riser, posting a 6.70% CAGR because downsized gasoline engines depend on accurate boost management to meet power and emission targets. Throttle valves, HVAC blend doors, and EGR butterflies retain mid-single-digit growth, each backed by regulatory or comfort imperatives.

Pneumatic fuel-injection rail regulators survive in certain flex-fuel layouts popular in Brazil, while door-lock plungers remain common in cost-sensitive hatchbacks. Across the board, suppliers experiment with smart pressure sensors embedded in actuator bodies to supply health data back to the vehicle control network. The enhancements prolong relevance of pneumatically powered devices even as direct electric motor drives tighten competitive gaps. Overall, the application mix underscores why the automotive pneumatic actuators market maintains double-digit billion-dollar revenues: it spans mandatory safety, emissions, and comfort functions that every vehicle must carry.

Passenger cars generated 56.70% of 2024 revenue, reflecting sheer production volume across global plants. Yet heavy commercial vehicles are projected to pace the automotive pneumatic actuators market size expansion with a 5.90% CAGR. Fleet operators prize the durability of air-brake and air-suspension circuits under intense duty cycles, while stricter CO2 quotas push for optimized compressor management rather than wholesale technology swaps. Light commercial vans track e-commerce parcel demand and achieve a robust CAGR on the back of city-logistics growth. Construction and mining equipment are, chiefly for high-temperature exhaust-flap controllers and robust steering stabilizers.

Two-wheelers remain a micro-segment concentrated in select Asian economies, yet scooter OEMs are trialing low-pressure air servos for automatic clutch actuation. The diversity highlights a bifurcation: suburban passenger cars gravitate toward compact electric drives for NVH advantages, whereas high-payload vehicles sustain pneumatics for force density and proven maintainability. That divergence shapes future platform strategies of tier-1 suppliers, compelling them to produce modular families that scale from micro to heavy-duty ratings without rewriting qualification protocols.

The Automotive Pneumatic Actuator Market is Segmented by Application Type (Throttle Actuators, Fuel Injection Actuators, Brake Actuators, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Actuator Mechanism (Single-Diaphragm Pneumatic and More), Sales Channel (OEM and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific generated 45.50% of global revenue in 2024, underpinned by China's multi-brand passenger car output and Japan's high-precision valve competence. The region is forecast to post a 7.10% CAGR as supply bases in Vietnam, Thailand, and India climb the value curve, making in-region sourcing attractive for global nameplates. Electro-pneumatic R&D centers in South Korea exploit the country's advanced semiconductor ecosystem to integrate pressure MEMS sensors onto actuator PCBs, heightening competitive edge. Notwithstanding electric-vehicle penetration, cost-optimized sub-compact segments still install pneumatically driven HVAC and turbo wastegate units, securing volume for suppliers.

Middle East & Africa stands out as the fastest-growing cluster at a robust CAGR of 7.80%. Saudi Vision 2030 industrial policy lures CKD assembly lines, each demanding localized actuator content for commercial trucks that service construction booms. The UAE leverages free-zone logistics to re-export spare parts kits deeper into African markets. Turkey's customs-union access to Europe boosts its component exports, compelling pneumatic suppliers to expand Izmir and Bursa facilities. These dynamics re-orient procurement away from trans-continental shipping toward near-market production, shortening lead times and cutting freight emissions.

In South America, flex-fuel engine architectures unique to the region stimulate EGR and fuel-rail actuator demand because ethanol blends alter combustion stoichiometry daily. Local content rules push multinational suppliers to site elastomer curing presses in Minas Gerais rather than import seal stacks. Argentine heavy-truck assembly rebounds after currency stabilization measures, adding lift for high-capacity brake chambers. Currency volatility and political risk temper the outlook, yet installed base inertia keeps the automotive pneumatic actuators market resilient in the hemisphere.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Emerson (ASCO Valve)

- Hitachi Astemo Ltd

- CTS Corporation

- Schrader Duncan Ltd

- Rotex Automation

- Nucon Industries Pvt Ltd

- Magneti Marelli SpA

- Mitsubishi Electric Corp

- Del-Tron Precision Inc

- Procon Engineering

- Valeo SA

- Aisin Corporation

- Mahle GmbH

- BorgWarner Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter emission norms driving precise air-fuel control

- 4.2.2 Increasing global vehicle production

- 4.2.3 ADAS proliferation demanding accurate actuation

- 4.2.4 Lightweighting trend for fuel economy

- 4.2.5 Hydrogen ICE valve-timing adoption

- 4.2.6 OTA-enabled actuator software monetisation

- 4.3 Market Restraints

- 4.3.1 Shift toward energy-efficient electric actuators

- 4.3.2 Complexity & high maintenance cost of pneumatics

- 4.3.3 Shortage of high-grade elastomers for seals

- 4.3.4 Tier-1 decarbonisation curbing pneumatic R&D

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Application Type

- 5.1.1 Throttle Actuators

- 5.1.2 Fuel Injection Actuators

- 5.1.3 Brake Actuators

- 5.1.4 Exhaust Gas Recirculation Actuators

- 5.1.5 Turbocharger Wastegate Actuators

- 5.1.6 HVAC Actuators

- 5.1.7 Door Lock Actuators

- 5.1.8 Others

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Off-Highway Vehicles

- 5.2.5 Two-Wheelers

- 5.3 By Actuator Mechanism

- 5.3.1 Single-Diaphragm Pneumatic

- 5.3.2 Vacuum-Boost Pneumatic

- 5.3.3 Electro-pneumatic (EP)

- 5.3.4 Servo-pneumatic

- 5.3.5 Rack-and-Pinion

- 5.3.6 Rotary-Vane

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 Emerson (ASCO Valve)

- 6.4.5 Hitachi Astemo Ltd

- 6.4.6 CTS Corporation

- 6.4.7 Schrader Duncan Ltd

- 6.4.8 Rotex Automation

- 6.4.9 Nucon Industries Pvt Ltd

- 6.4.10 Magneti Marelli SpA

- 6.4.11 Mitsubishi Electric Corp

- 6.4.12 Del-Tron Precision Inc

- 6.4.13 Procon Engineering

- 6.4.14 Valeo SA

- 6.4.15 Aisin Corporation

- 6.4.16 Mahle GmbH

- 6.4.17 BorgWarner Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment