|

시장보고서

상품코드

1836643

인도네시아의 섬유 제조 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Indonesia Textile Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

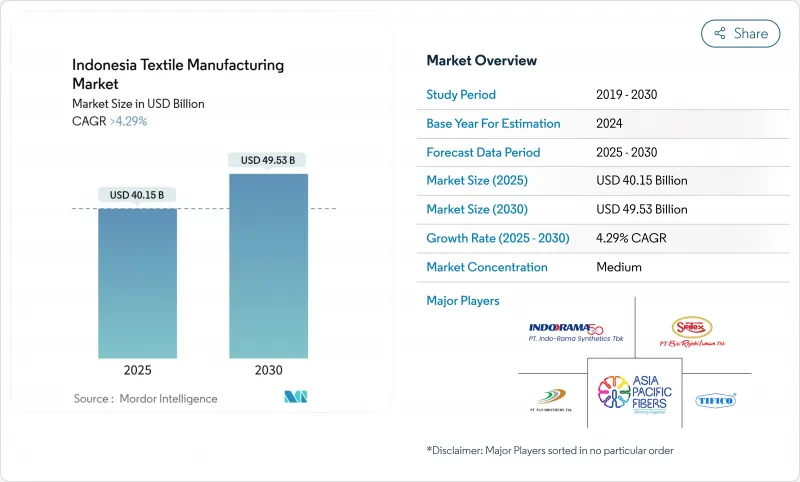

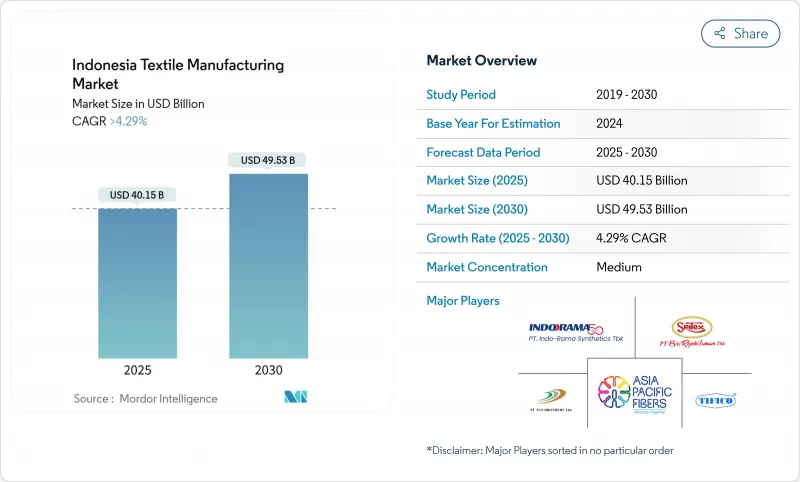

인도네시아의 섬유 제조 시장은 2025년 401억 5,000만 달러, 2030년에는 495억 3,000만 달러에 이르고, CAGR 4.29%로 성장할 것으로 예측됩니다.

인도네시아 만들기 4.0 로드맵을 통한 견고한 정책적 뒷받침, 숙련 노동자의 풍부한 수영장, 해외로부터의 수주의 부활에 의해 인도네시아는 아시아공급 체인의 다양화를 목표로 하는 브랜드에 있어서 중요한 조달 거점으로서 자리매김되고 있습니다. 자바 섬의 성숙한 산업 에코시스템은 공장 자동화의 진전과 석유화학의 통합과 함께 임금 압력이 높아지는 가운데 비용 경쟁력을 유지하고 있습니다. 적당한 마모와 기술 섬유에 대한 수요가 증가함에 따라 생산 품질을 지속적으로 높이고 재활용 섬유로의 전환은 세계적인 지속가능성 기준과의 무결성을 높이고 있습니다. 물류 병목과 수입 주도 가격 경쟁에도 불구하고 적극적인 세제 우대 조치, 친환경 산업 인증, 지역 개발 프로그램은 중기 성장 전망을 지원합니다.

인도네시아의 섬유 제조 시장 동향과 통찰

미국 및 EU 브랜드에서 자바 섬 클러스터로의 액티브웨어 주문의 니어 쇼어링 증가

레거시 아시아 허브의 인건비 상승과 보다 신속한 보충의 필요성으로 구미 라벨이 자바 섬의 대규모 공장에 진출하고 있습니다. 연간 생산 능력 1억 1,700만 장의 팬 브라더스는 퍼포먼스 니트웨어의 추가 계약을 획득하여 인도네시아로의 전환을 강조하고 있습니다. 자바 섬의 산업 단지 내에서 원사, 직물 및 봉제 공장이 가까이 있기 때문에 리드 타임이 단축되고 처리 비용이 절감됩니다. 그럼에도 불구하고, 미국의 잠재적인 관세 인상에 대한 불확실성은 생산자에게 여전히 감시대상입니다.

무슬림 패션 수출의 붐이 부가가치 의류 생산을 견인

인도네시아는 문화적 친화성과 디자인의 재능을 활용하여 2023년에 3,610억 달러로 추정되는 확대하는 세계 모드 패션 분야에 공급하고 있습니다. 뉴욕 패션 위크의 쇼케이스는 국제적인 지명도를 높여 현지 브랜드가 더 높은 가격대에서 거래될 수 있도록 했습니다. 부가가치가 높은 라인은 고객과의 관계를 더욱 견고하게 만들고 고급 장식 기술이 필요하기 때문에 공장은 특수 기계 및 숙련된 장인에 대한 투자를 촉구합니다.

불법 저가 수입이 중소기업 직물 마진을 침식

불법 수입품이 현지 가격을 낮추고 공장 폐쇄와 해고를 일으켰기 때문에 정부는 수입 허가를 엄격히 하고 검사를 강화하고 있습니다. 200%의 세이프가드 관세가 있어도 단속이 약하기 때문에 위조품이나 표준 이하의 직물이 항구를 빠져나가 지역 밀착형의 직물 클러스터는 제경비를 회수하지 못하고 있습니다. 새로운 Permenperin 5/2024 규칙은 문서 요구 사항을 명확히하고 세관 데이터베이스를 동기화하여 허점을 막는 것을 목표로 합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 섬유 자동화를 가속화하는 정부의 "인도네시아 4.0 만들기" 인센티브

- Z세대 소비자들 사이에서 이커머스 주도의 국내 의류 수요 급증

- 만성 항구와 철도 병목이 섬 간 물류 비용을 팽창시킵니다.

부문 분석

2024년 인도네시아 텍스타일 제조 시장에서 직물은 37.3%의 점유율을 유지하고 서자바 클러스터에서 셔틀 직기와 레피아 직기의 생산 능력이 정착하고 있습니다. 생산은 주로 셔츠와 데님에 대응하고 수출량은 여전히 안정적입니다. 한편, 니트는 퍼포먼스 어패럴과 애슬레저 라인이 급증하기 때문에 2030년까지의 CAGR은 5.08%를 나타낼 전망입니다. 생산자는 작은 로트 생산과 기능적인 실의 혼방이 가능한 원 뜨개질 기계를 도입하여 온라인 소매업체가 선호하는 쇼트런 모델에 맞춥니다.

니트의 성장은 동남아시아의 신속한 보충을 요구하는 스포츠웨어 라벨의 주문 증가도 반영합니다. 자바섬에 본사를 둔 제조업체는 염색공장과 인쇄공장을 병설하여 완전히 포장된 의류를 제공하고, 원단 전용 공급업체보다 높은 가치를 획득하고 있습니다. 중기적으로는 피팅가 없는 구조와 같은 첨단 니트 기술은 생산성을 향상시키고, 생산 후 낭비를 줄이고, 컴포트 의류에서 인도네시아의 경쟁력을 강화할 것으로 예측됩니다.

2024년 인도네시아 텍스타일 제조업 시장 점유율의 59.5%는 의류품으로, 이 나라의 봉제에 관한 깊은 전문 지식과 풍부한 노동력을 이야기하고 있습니다. 생산자는 컷 메이크 트림에서 풀 패키지 서비스로 전환하여 브랜드 고객에게 디자인 입력, 머천다이징 및 컴플라이언스 문서화를 제공합니다. 가장 급성장하고 있는 것은 테크니컬 & 인더스트리얼 텍스타일로 CAGR 5.04%이며, 인프라 투자와 자동차 OEM의 현지화를 반영하고 있습니다.

의류가 계속 주도권을 잡고 있는 것은 전통적인 모티브와 현대적인 실루엣을 융합시켜 수출 시장을 노리는 인도네시아 모드웨어의 틈새 시장에도 기인하고 있습니다. 업스트림 직물과 염색 공정을 관리하는 통합 기업은 마진을 개선하고 브랜드 감사와의 품질 무결성을 보장합니다. 반면 패브릭 전용 생산자는 더 많은 생산량을 보호복, 여과, 자동차 부품으로 돌려 패션 사이클에 대한 의존도를 줄이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 「Making Indonesia 4.0」장려책에 의한 섬유 자동화의 가속

- 미국·EU 브랜드에서 자바섬 클러스터로의 액티브웨어의 니어쇼어링 증가

- 이슬람계 패션의 수출 붐이 부가가치가 높은 의류품 생산을 촉진

- 전자상거래 주도에 의한 Z세대 소비자의 국내 의류 수요 급증

- 면화 의존도가 높은 가운데, 인공 섬유의 수입 대체가 진행

- 중부 자바의 친환경 염료 하우스 업그레이드에 대한 투자자 감세

- 시장 성장 억제요인

- 불법 저가 수입에 의한 중소기업의 직물 마진의 악화

- 만성 항구와 철도 병목에 의한 섬 간 물류 비용 상승

- 불안정한 PLN의 전력요금 체계가 에너지 집약형의 방적업을 압박

- 서자바의 노동 인구 박박, 임금 인플레이션

- 밸류체인/공급망 분석

- 규제 및 정부 주도의 전망

- 기술적 전망- Industry 4.0과 디지털 전환의 준비

- 산업의 매력 - Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 최근 세계적 혼란이 인도네시아 섬유 제조업에 미친 영향

- 지속가능성과 서큘러·이코노미의 동향

제5장 시장 규모 및 성장 예측

- 프로세스 유형별

- 방적

- 직물

- 뜨개질

- 마무리 가공

- 기타 공정(부직포)

- 텍스타일 유형별

- 섬유

- 실

- 패브릭

- 옷

- 기타 섬유

- 소재별

- 천연섬유(면, 실크 등)

- 합성 섬유(폴리에스테르, 나일론 등)

- 기타(재생 및 리사이클 섬유, 특수 섬유)

- 용도별

- 의류

- 홈 섬유

- 공업용 섬유

- 기타 용도

- 지역별(인도네시아)

- 자바 섬

- 수마트라

- 기타(칼리만탄, 술라웨시, 발리 등)

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일 {}(영어)

- PT Asia Pacific Fibres Tbk

- Indo-Rama Synthetics Tbk

- PT Sri Rejeki Isman Tbk(Sritex)

- PT Tifico Fiber Indonesia Tbk

- PT Pan Brothers Tbk

- PT Ever Shine Tex Tbk

- PT Trisula Textile Industries Tbk

- PT Century Textile Industry Tbk(토레이)

- PT Polychem Indonesia Tbk

- PT Argo Pantes Tbk

- Duniatex Group

- PT Kahatex

- PT Apac Inti Corpora

- PT Eratex Djaja Tbk

- PT Ateja Tritunggal

- PT Sinar Para Taruna

- PT Kewalram Indonesia

- PT Pura Group(Textile Div.)

- PT Multi Garmenjaya

- PT Delami Garment Industries

제7장 시장 기회와 전망

SHW 25.10.28The Indonesia Textile Manufacturing Market is valued at USD 40.15 billion in 2025 and is projected to reach USD 49.53 billion by 2030, expanding at a 4.29% CAGR.

Robust policy backing through the Making Indonesia 4.0 roadmap, a large pool of skilled labor, and resurging foreign orders position the country as a vital sourcing hub for brands looking to diversify Asian supply chains. Java's mature industrial ecosystem, together with rising factory automation and petrochemical integration, sustains cost competitiveness even as wage pressures inch up. Expanding demand for modest wear and technical textiles continues to lift output quality, while the shift toward recycled fibers signals growing alignment with global sustainability standards. Despite logistics bottlenecks and import-led price competition, proactive tax incentives, green-industry certifications, and regional development programs underpin medium-term growth prospects.

Indonesia Textile Manufacturing Market Trends and Insights

Rising Near-Shoring of Activewear Orders from US & EU Brands to Java Clusters

Labor cost escalation in legacy Asian hubs and the need for faster replenishment bring Western labels to Java's large-scale plants. Pan Brothers, with annual capacity of 117 million pieces, has secured incremental contracts for performance knitwear, underscoring the pivot toward Indonesia. Close proximity among yarn, fabric, and garment units inside the island's industrial estates compresses lead times and lowers handling expenses. Nevertheless, uncertainty over potential US tariff hikes remains a watchpoint for producers.

Boom in Muslim Fashion Exports Driving Value-Added Garment Production

Indonesia leverages cultural affinity and design talent to supply the expanding global modest-fashion segment, estimated at USD 361 billion in 2023. Showcases at New York Fashion Week have raised international visibility, allowing local brands to command higher price points. Value-added lines create stickier customer relationships and require advanced embellishment techniques, prompting mills to invest in specialty machinery and skilled artisans.

Illegal Low-Priced Imports Eroding SME Weaving Margins

Unlawful inflows undercut local price points and have triggered factory closures and layoffs, pushing the government to tighten import permits and step up inspections. Even with 200% safeguard tariffs, weak enforcement lets counterfeit and sub-standard fabrics slip through ports, leaving community-based weaving clusters unable to recover overheads. The new Permenperin 5/2024 regulation aims to close loopholes by clarifying documentation requirements and synchronizing customs databases.

Other drivers and restraints analyzed in the detailed report include:

- Government "Making Indonesia 4.0" Incentives Accelerating Textile Automation

- Surge in E-Commerce-Led Domestic Apparel Demand Among Gen-Z Consumers

- Chronic Port & Rail Bottlenecks Inflating Inter-Island Logistics Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Weaving retained a 37.3% share of the Indonesia textile manufacturing market in 2024, anchored by entrenched shuttle and rapier loom capacity across West Java clusters. Output caters mainly to shirtings and denim, segments that still support steady export volumes. Knitting, however, posts a 5.08% CAGR through 2030 as performance apparel and athleisure lines surge. Producers deploy circular knitting machines capable of smaller lot sizes and functional yarn blends, aligning with the short-run model favored by online retailers.

Knitting's growth also reflects rising orders from sportswear labels seeking quick replenishment out of Southeast Asia. Java-based makers leverage co-located dye-houses and print shops to deliver fully packaged garments, capturing greater value than fabric-only suppliers. In the medium term, advanced knitting techniques such as seamless construction are expected to lift productivity and reduce post-production waste, reinforcing Indonesia's competitiveness in comfort apparel.

Garments represented 59.5% of the Indonesia textile manufacturing market share in 2024, testifying to the country's deep sewing expertise and abundant workforce. Producers have moved beyond cut-make-trim to full-package services, offering design input, merchandising, and compliance documentation to brand customers. The fastest expansion occurs in technical and industrial textiles at 5.04% CAGR, reflecting infrastructure spending and automotive OEM localization.

Continued garment leadership also stems from Indonesia's modest-wear niche, where brands merge traditional motifs with modern silhouettes for export markets. Integrated players that control upstream fabric and dyeing steps capture improved margins and ensure quality alignment with brand audits. Meanwhile, fabric-only producers channel more output into protective wear, filtration, and automotive components, reducing reliance on fashion cycles.

The Indonesia Textile Manufacturing Market Report is Segmented by Process Type (Weaving, Knitting, Spinning, and More), by Textile Type (Fabric, Yarn, Fiber, and More), by Material Type (Natural Fibers (Cotton, Silk Etc. ), and More), by Application (Apparel, Home Textiles, and More), and by Region (Java, Sumatra and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- PT Asia Pacific Fibres Tbk

- Indo-Rama Synthetics Tbk

- PT Sri Rejeki Isman Tbk (Sritex)

- PT Tifico Fiber Indonesia Tbk

- PT Pan Brothers Tbk

- PT Ever Shine Tex Tbk

- PT Trisula Textile Industries Tbk

- PT Century Textile Industry Tbk (Toray)

- PT Polychem Indonesia Tbk

- PT Argo Pantes Tbk

- Duniatex Group

- PT Kahatex

- PT Apac Inti Corpora

- PT Eratex Djaja Tbk

- PT Ateja Tritunggal

- PT Sinar Para Taruna

- PT Kewalram Indonesia

- PT Pura Group (Textile Div.)

- PT Multi Garmenjaya

- PT Delami Garment Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government "Making Indonesia 4.0" incentives accelerating textile automation

- 4.2.2 Rising near-shoring of activewear orders from US & EU brands to Java clusters

- 4.2.3 Boom in Muslim fashion exports driving value-added garment production

- 4.2.4 Surge in e-commerce-led domestic apparel demand among Gen-Z consumers

- 4.2.5 Import-substitution push for man-made fibers amid high cotton dependency

- 4.2.6 Investor tax breaks for green dye-house upgrades in Central Java

- 4.3 Market Restraints

- 4.3.1 Illegal low-priced imports eroding SME weaving margins

- 4.3.2 Chronic port & rail bottlenecks inflating inter-island logistics cost

- 4.3.3 Volatile PLN electricity tariffs squeezing energy-intensive spinning

- 4.3.4 Tight labour pool in West Java driving wage inflation vs. Vietnam

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Government-Initiative Outlook

- 4.6 Technological Outlook - Industry 4.0 & Digital Transformation Readiness

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Recent Global Disruptions on the Indonesia Textile Manufacturing Industry

- 4.9 Sustainability & Circular Economy Trends

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Process Type

- 5.1.1 Spinning

- 5.1.2 Weaving

- 5.1.3 Knitting

- 5.1.4 Finishing

- 5.1.5 Other Processes (non-woven)

- 5.2 By Textile Type

- 5.2.1 Fiber

- 5.2.2 Yarn

- 5.2.3 Fabric

- 5.2.4 Garments

- 5.2.5 Other Textiles

- 5.3 By Material Type

- 5.3.1 Natural Fibers (Cotton, Silk etc.)

- 5.3.2 Synthetic Fibers (Polyester, Nylon etc.)

- 5.3.3 Others (Regenerated & Recycled Fibers, Speciality Fibers)

- 5.4 By Application

- 5.4.1 Apparel

- 5.4.2 Home Textiles

- 5.4.3 Technical/Industrial Textiles

- 5.4.4 Other Applications

- 5.5 By Region (Indonesia)

- 5.5.1 Java

- 5.5.2 Sumatra

- 5.5.3 Others (Kalimantan, Sulawesi, Bali, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 PT Asia Pacific Fibres Tbk

- 6.4.2 Indo-Rama Synthetics Tbk

- 6.4.3 PT Sri Rejeki Isman Tbk (Sritex)

- 6.4.4 PT Tifico Fiber Indonesia Tbk

- 6.4.5 PT Pan Brothers Tbk

- 6.4.6 PT Ever Shine Tex Tbk

- 6.4.7 PT Trisula Textile Industries Tbk

- 6.4.8 PT Century Textile Industry Tbk (Toray)

- 6.4.9 PT Polychem Indonesia Tbk

- 6.4.10 PT Argo Pantes Tbk

- 6.4.11 Duniatex Group

- 6.4.12 PT Kahatex

- 6.4.13 PT Apac Inti Corpora

- 6.4.14 PT Eratex Djaja Tbk

- 6.4.15 PT Ateja Tritunggal

- 6.4.16 PT Sinar Para Taruna

- 6.4.17 PT Kewalram Indonesia

- 6.4.18 PT Pura Group (Textile Div.)

- 6.4.19 PT Multi Garmenjaya

- 6.4.20 PT Delami Garment Industries

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment