|

시장보고서

상품코드

1836654

디지털 X선 기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Digital X-ray Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

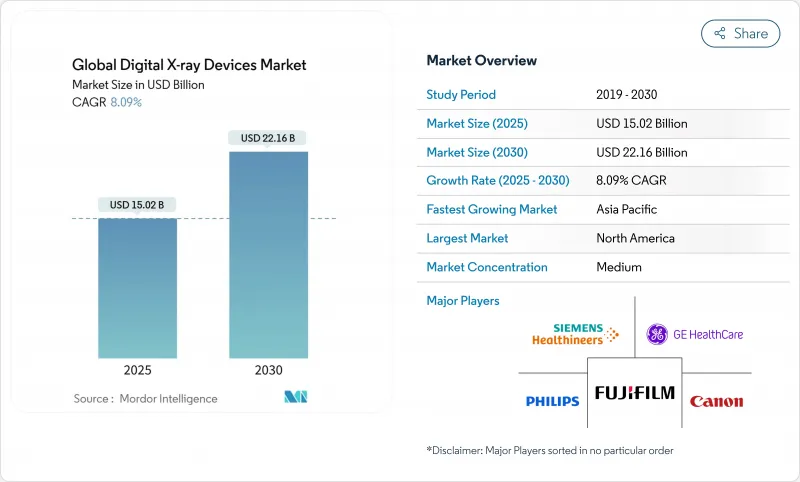

디지털 X선 기기 시장 규모는 2025년 150억 2,000만 달러로 추정되고, 2030년 221억 6,000만 달러에 이를 것으로 예상되며, 이 기간 CAGR은 8.09%로 성장할 전망입니다.

필름 및 컴퓨팅 라디오그래피(CR) 시스템에서 일관된 대체, 선량 관리 강화, AI 통합 확대가 이 성장 궤도를 지원합니다. CR에 대한 메디케어 벌칙 강화, 만성질환의 영상처리 수요 증가, 병원 워크플로우 최적화 등으로 다이렉트 라디오그래피(DR) 업그레이드가 가속화되고 있으며, 휴대용 플랫폼은 병원 부지 밖으로의 접근을 확대하고 있습니다. 인공지능 감지기, 광자 계수 기술 및 클라우드 지원 워크 플로 솔루션이 성능 벤치 마크를 밀어 올리고 기존 벤더에게 새로운 경쟁 압력을 제공합니다. 동시에 희토류 신틸레이터의 원재료 제약과 방사선 기사의 인력 부족이 운영 리스크를 가져오고, 프로바이더는 생산성 주도의 혁신을 요구할 수밖에 없습니다.

세계의 디지털 X선 기기 시장 동향 및 인사이트

만성 질환 및 정형외과 질환 증가

세계적인 노화로 인해 근골격계와 흉부 영상 진단이 필요한 환자의 수가 증가하고 있습니다. 골다공증, 골관절염, 심폐질환은 현재 외래 진단의 대부분을 차지하고, 정기적인 X-선 후속을 촉구하며, 기기의 반복 이용을 창출하고 있습니다. 세계보건기구(WHO)는 2030년까지 세계 사망의 4분의 3 가까이를 만성 질환이 차지할 것으로 예측하고, X선 촬영이 최전선 진단 도구로 확고한 지위를 구축하고 있습니다. AI로 강화된 DR 플랫폼은 일상 검사 중에 미묘한 척추 골절을 감지하여 부가가치를 높입니다. 이는 NHS 시설 전체에서 수천 개의 진단되지 않은 사례를 발견한 Nanox AI의 HealthOST 알고리즘에 의해 입증되었습니다. 조기 발견은 다운스트림 비용을 낮추고 예방적 영상 진단의 상환을 지원합니다. 따라서 정형외과 이미징 수요 증가는 디지털 X선 기기 시장에서 병원, 이미징 센터, 외래 클리닉에서 일관된 단위 배치를 지원합니다.

DR 패널에서 검출기 및 AI 신속한 업그레이드

플랫 패널 검출기는 현재 노광 파라미터, 노이즈 억제 및 자동 콜리메이션을 개선하는 온보드 컴퓨팅이 내장되어 있습니다. 광자 계수 아키텍처는 공간 해상도와 대비 대 잡음비를 더욱 향상시켜 임상가에게 낮은 복용량으로 더 많은 진단 정보를 제공합니다. 지멘스 헤르티니어스, GE 헬스케어 및 기타 OEM은 하드웨어와 소프트웨어의 공동 로드맵에 많은 투자를 하고 있으며, 이를 통해 설치된 장비의 경쟁력 있는 라이프사이클을 연장하고 있습니다. GE 헬스케어와 엔비디아의 협업은 이 축발을 보여주며, 이미지의 위치 결정과 품질 체크를 자동화함으로써 검사 시간을 단축하고 검사 기사의 생산성을 향상시키는 것을 목표로 하고 있습니다. 이에 따라 시설은 지속적인 펌웨어 업그레이드가 가능한 검출기를 우선시하고, 설비 투자를 보호하며, 디지털 X선 기기 시장의 혁신 흐름을 강화하고 있습니다.

높은 CAPEX 및 총 소유 비용

첨단 AI 기능을 갖춘 프리미엄 DR실은 50만 달러를 초과할 수 있으며, 소규모 병원에 있어서는 큰 재무적 장벽이 됩니다. 지속적인 유지 보수 계약, 사이버 보안 업그레이드, 정기적인 검출기 교체는 수명주기 지출을 증가시킵니다. 미국에서는 2025년 진료 보상 개정으로 세계 영상 진료 보상이 3.55% 낮아지기 때문에 새로운 장비 투자 회수 기간이 길어집니다. 따라서 시설은 자본 계획을 보다 면밀히 조사하고, 일부 구매를 늦추거나, 후부 키트나 재생품의 검출기를 선택적으로 선택하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 필름 및 CR과 비교한 비용 절감 및 선량 저감

- 중규모 병원의 리노베이션 업그레이드를 위한 조달 인센티브

- 외래 환경에서의 상환 갭

부문 분석

흉부와 폐 검사는 2024년 디지털 X선 기기 시장 규모의 32.47%를 차지했습니다. 응급, 치명적인 치료, 일상적인 외래 검사 빈도가 높아 시스템 사용을 유지하고 지속적인 검출기 업그레이드를 촉진합니다. 폐렴과 결핵의 AI 스크리닝 알고리즘은 진단의 신뢰성을 향상시키고 DR은 호흡기 평가의 첫 번째 선택 양식으로 강화됩니다. 치과용 영상 처리는 CAGR 8.91%에서 가장 빠르게 확대되었습니다. 이는 의자 사이드 워크플로우를 합리화하는 소형의 구강내 센서와 AI를 지원하는 촉감 감지에 지지되고 있습니다. 정형외과 영상 진단은 노인들이 골절 평가와 수술 후 모니터링을 자주 수행해야 하기 때문에 순조롭게 성장하고 있습니다.

흉부 X선 촬영은 이미지 라이브러리가 풍부하고 라벨링이 표준화되어 신속한 알고리즘 개발이 가능합니다. 감염의 유행 시에 배치된 휴대용 흉부 시스템은 2차 오염의 위험을 줄이면서 치료의 연속성을 보장하고 명확한 가치를 입증했습니다. 치과 진료소에서는 3차원 재구성과 클라우드 기반 컨설팅의 혜택을 누리며 내원 1회당 수익이 증가할 수 있습니다. 이러한 요인들이 결합되어 디지털 X선 기기 시장의 용도 믹스가 확대되고 성숙한 대량 생산 분야와 급성장하는 전문 분야의 균형이 맞추어지고 있습니다.

다이렉트 X선 촬영 플랫폼은 2024년 디지털 X선 기기 시장 점유율의 83.91%를 차지했으며, 우수한 화질, 워크플로우 속도, 유리한 상환에 지지된 확대가 계속되고 있습니다. 현재 평가 중인 포톤 카운팅 검출기는 듀얼 에너지 분리와 동등한 분해능으로 저선량화를 기대할 수 있어 검출기 혁신의 다음 도약을 나타냅니다. 컴퓨팅 라디오 그래피는 예산에 제약이 있는 시설에서만 사용되지만, 진료 보상 벌칙이 강화되고 엔트리 레벨 DR 기기의 가격이 하락하기 때문에 전환이 진행되고 있습니다.

디지털 X선 기기 업계는 현재 검출기의 픽셀 크기보다 통합 소프트웨어의 성능을 차별화하고 있습니다. 스마트 촬영 프로토콜, 예지 보전 경고, 자동화된 품질 보증은 임상 신뢰성을 높이는 동시에 서비스 비용을 절감합니다. 그 결과, 조달팀은 하드웨어를 구입하기 전에 소프트웨어 생태계의 종합적인 능력을 평가하게 되었고, 디지털 X선 기기 시장의 기술적 백본으로서의 직접 라디오그래피의 역할은 확고해집니다.

지역별 분석

북미는 성숙한 병원 네트워크와 메디케어의 처벌로 가속화된 업그레이드 사이클을 배경으로 디지털 X선 기기 시장의 2024년 매출의 38.52%를 차지했습니다. 미국 병원이 2025년 설비 예산으로 방사선 안전, 사이버 보안, AI에 대한 대응을 우선했기 때문에 OEM 각사는 검출기의 출하 대수를 늘렸습니다. 캐나다에서도 비슷한 선량 감소 목표가 적용되고 멕시코의 세구로 파퓰러(Seguro Popular) 제도는 지방의 이미지 센터에 자금을 흘리고 있습니다. 이러한 규모에도 불구하고 연간 성장률은 7.43%로 완만해졌습니다.

아시아태평양은 CAGR 8.86%에서 가장 급성장하고 있으며 수십억 달러 규모의 공립 병원 건설 계획과 중간층의 보험 적용 확대에 추진되고 있습니다. 중국의 Healthy China 2030 청사진에서는 현 수준에서의 이미지 처리 능력을 확대할 의무가 있으며, 지역 OEM이 검출기 조립을 현지화하는 인센티브가 되고 있습니다. 인도의 스마트 시티와 아유슈만 바라트 이니셔티브는 농촌 지역의 진단 범위를 확대하고 견고한 휴대용 DR 판매에 박차를 가하고 있습니다. 한편, 일본과 한국 공급자는 심혈관과 종양의 하위 전문성을 위해 하이 엔드 포톤 카운팅 프로토타입을 구입하고 있습니다. 그러나 희토류 신틸레이터 공급망 위험은 수출 규제가 지속되면 최종 가격이 상승하고 아시아태평양의 조달 주기에 변동을 초래할 수 있습니다.

유럽에서는 국민 모두 보험 제도가 노후화한 CR 플릿으로부터 대체하기 위해, 2030년까지 CAGR 7.79%로 견조하게 추이할 전망입니다. 유럽 방사선 방호 지령이 선량 추적 소프트웨어를 시행해, AI 대응 DR의 채용이 진행됩니다. 독일과 프랑스는 지역에 서비스를 제공하기 위해 원격 영상 진단 네트워크에 투자하고 영국은 휴대용 DR을 지원하는 지역 진단 허브를 추진하고 있습니다. 중동 및 아프리카는 걸프 협력 회의 국가에서 멀티 클리닉에 대한 투자와 남아프리카의 보험 보급 확대로 CAGR 8.35%를 나타냅니다. 남미에서는 브라질의 공공-민간 양보 모델이 진단 장비에 자금을 지원함에 따라 남미는 8.12% 성장하여 역사적인 공급 부족과 싸우고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 및 정형외과 질환 증가

- DR 패널의 검출기 및 AI의 급속한 업그레이드

- 필름 및 CR과 비교한 비용 절감과 선량 저감

- 중견 병원에서 복고풍 업그레이드를 위한 조달 인센티브

- 포인트 오브 케어 및 홈 이미징 에코시스템의 성장

- AI를 활용한 원격 영상 진단 네트워크 확대

- 시장 성장 억제요인

- 높은 CAPEX 및 총소유 비용

- 외래환자에서의 상환 격차

- 고급 DR 및 AI 워크플로우를 위한 숙련된 방사선 기사 부족

- 희토류 신틸레이터 공급망 위험

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측 : 금액

- 용도별

- 정형외과

- 흉부 및 호흡기

- 치과

- 심장혈관

- 종양학

- 기타 용도

- 기술별

- 컴퓨티드 라디오그래피(CR)

- 직접 X선 촬영(DR)

- 플랫 패널 검출기

- CCD 및 CMOS 패널

- 휴대성별

- 룸 베이스 고정 시스템

- 휴대용 시스템

- 핸드헬드 유닛

- 모바일 카트

- 최종 사용자별

- 병원

- 화상 진단센터

- 외래수술센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Agfa-Gevaert NV

- Analogic Corporation

- Canon Medical Systems Corporation

- Carestream Health, Inc.

- DRGEM Corporation

- Esaote SpA

- Fujifilm Holdings Corporation

- GE Healthcare

- Hitachi, Ltd.

- Hologic, Inc.

- Konica Minolta, Inc.

- Koninklijke Philips NV

- Lotus Healthcare

- Mindray Medical International Limited

- Planmed Oy

- Samsung Electronics Co., Ltd.

- Shimadzu Corporation

- Siemens Healthineers AG

- Skanray Technologies Limited

- United Imaging Healthcare Co., Ltd.

- Varex Imaging Corporation

- Vieworks Co., Ltd.

제7장 시장 기회 및 전망

AJY 25.10.27The digital X-ray devices market size is currently valued at USD 15.02 billion in 2025 and is forecast to reach USD 22.16 billion by 2030, reflecting an 8.09% CAGR over the period.

Consistent replacement of film and computed radiography (CR) systems, stronger emphasis on dose management, and expanding AI integration sustain this growth trajectory. Intensified Medicare penalties on CR, rising chronic disease imaging demand, and hospital workflow optimization continue to accelerate direct radiography (DR) upgrades, while portable platforms extend access beyond the hospital campus. AI-ready detectors, photon-counting technology, and cloud-enabled workflow solutions push performance benchmarks higher, creating fresh competitive pressure for traditional vendors. Simultaneously, raw-material constraints in rare-earth scintillators and radiographer staffing gaps introduce operational risk, compelling providers to seek productivity-driven innovations.

Global Digital X-ray Devices Market Trends and Insights

Rising Prevalence of Chronic & Orthopedic Disorders

Global population aging enlarges the base of patients requiring musculoskeletal and chest imaging. Osteoporosis, osteoarthritis, and cardiopulmonary diseases now dominate outpatient diagnostics, driving regular radiographic follow-ups that create repeat equipment utilization. The World Health Organization projects that chronic disorders will account for nearly three-quarters of worldwide deaths by 2030, firmly anchoring radiography as a frontline diagnostic tool. AI-enhanced DR platforms add value by detecting subtle vertebral fractures during routine studies, as demonstrated by Nanox AI's HealthOST algorithm, which uncovered thousands of undiagnosed cases across NHS sites. Early detection lowers downstream costs and supports reimbursement for preventative imaging. Growing orthopedic imaging demand, therefore, sustains consistent unit placements across hospitals, imaging centers, and ambulatory clinics within the digital X-ray devices market.

Rapid Detector & AI Upgrades in DR Panels

Flat-panel detectors now incorporate on-board computing that improves exposure parameters, noise suppression, and automated collimation. Photon-counting architectures further enhance spatial resolution and contrast-to-noise ratios, giving clinicians more diagnostic information at lower doses. Siemens Healthineers, GE Healthcare, and other OEMs invest heavily in joint hardware-software roadmaps that extend competitive life cycles for installed fleets. GE Healthcare's collaboration with NVIDIA illustrates this pivot, aiming to automate image positioning and quality checks, thereby shortening exam times and improving technologist productivity. Facilities, therefore, prioritize detectors that can receive continuous firmware upgrades, protecting capital investments and reinforcing the digital X-ray devices market's innovation cadence.

High CAPEX & Total-Cost-of-Ownership

Premium DR rooms with advanced AI features can exceed USD 500,000, representing significant financial barriers for small hospitals. Ongoing maintenance contracts, cybersecurity upgrades, and periodic detector replacements inflate lifecycle spending. In the United States, 2025 Physician Fee Schedule adjustments cut global imaging reimbursement by 3.55%, lengthening return-on-investment horizons for new equipment. Facilities therefore scrutinize capital plans more closely, delaying some purchases and selectively favoring retrofit kits or refurbished detectors.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Savings & Dose-Reduction Versus Film/CR

- Procurement Incentives for Retrofit Upgrades in Mid-Tier Hospitals

- Reimbursement Gaps in Outpatient Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chest and pulmonary studies represented 32.47% of the digital X-ray devices market size in 2024. High examination frequency in emergency, critical-care, and routine outpatient settings sustains system utilization and encourages continuous detector upgrades. AI screening algorithms for pneumonia and tuberculosis enhance diagnostic confidence, reinforcing DR as the modality of choice for first-line respiratory evaluation. Dental imaging registers the fastest expansion at an 8.91% CAGR, helped by compact intraoral sensors and AI-assisted caries detection that streamline chairside workflows. Orthopedic imaging also climbs steadily as elderly populations require frequent fracture assessment and postoperative monitoring.

Beyond volumes, chest radiography leads AI adoption because image libraries are large and labeling is standardized, enabling rapid algorithm development. Portable chest systems deployed during infectious disease outbreaks demonstrated clear value, ensuring continuity of care while reducing cross-contamination risks. Dental practices benefit from three-dimensional reconstruction and cloud-based consults, increasing the revenue potential per visit. Together, these factors broaden the digital X-ray devices market's application mix, balancing mature high-volume segments with faster-growing specialty niches.

Direct radiography platforms captured 83.91% of digital X-ray devices market share in 2024, with continued expansion underpinned by superior image quality, workflow speed, and favorable reimbursement. Photon-counting detectors under evaluation show promise for dual-energy separation and lower dose at equal resolution, marking the next leap in detector innovation. Computed radiography remains only in budget-constrained facilities, yet escalating reimbursement penalties and the falling price of entry-level DR units drive conversion.

The digital X-ray devices industry now differentiates primarily on integrated software performance rather than raw detector pixel size. Smart acquisition protocols, predictive maintenance alerts, and automated quality assurance raise clinical confidence while reducing service costs. Consequently, procurement teams assess total software ecosystem capability before committing to hardware, cementing direct radiography's role as the technology backbone of the digital X-ray devices market.

The Digital X-Ray Devices Market Report is Segmented by Application (Orthopedic, Dental, and More), Technology (Computed Radiography and Direct Radiography [Flat-Panel Detectors and More]), Portability (Fixed Systems and Portable Systems [Hand-Held Units and Mobile Carts]), End-User (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.52% of 2024 revenue within the digital X-ray devices market, anchored by mature hospital networks and accelerated upgrade cycles motivated by Medicare penalties. OEMs raised detector shipments after U.S. hospitals prioritized radiation safety, cybersecurity, and AI readiness in their 2025 capital budgets. Canada applies similar dose-reduction targets, while Mexico's Seguro Popular replacement scheme channels funding toward provincial imaging centers. Despite this scale, annual growth moderates to 7.43% as substitution rather than new installation dominates demand.

Asia-Pacific is the fastest-growing territory at 8.86% CAGR, propelled by multi-billion-dollar public hospital construction programs and expanding middle-class insurance coverage. China's Healthy China 2030 blueprint mandates imaging capacity expansion at county level, incentivizing regional OEMs to localize detector assembly. India's smart-city and Ayushman Bharat initiatives increase rural diagnostic reach, spurring sales of rugged portable DR. Meanwhile, Japanese and South-Korean providers purchase high-end photon-counting prototypes for cardiovascular and oncology subspecialties. Supply-chain risk in rare-earth scintillators, however, could inflate end prices if export restrictions persist, injecting volatility into Asia-Pacific procurement cycles.

Europe posts a steady 7.79% CAGR to 2030 as universal health systems replace aging CR fleets. The European Radiation Protection Directive enforces dose-tracking software, elevating AI-ready DR adoption. Germany and France invest in teleradiology networks to serve rural regions, while the United Kingdom advances community diagnostic hubs that favor portable DR. Middle East & Africa demonstrates 8.35% CAGR owing to multi-clinic investments in Gulf Cooperation Council states and expanding insurance penetration in South Africa. South America grows 8.12% as Brazil's public-private concession model funds diagnostic equipment, combating historical under-supply.

- Agfa-Gevaert

- Analogic

- Canon

- Carestream Health

- DRGEM Corporation

- Esaote S.p.A.

- FUJIFILM

- GE Healthcare

- Hitachi

- Hologic

- Konica Minolta

- Koninklijke Philips

- Lotus Healthcare

- Mindray

- Planmed

- Samsung Group

- Shimadzu

- Siemens Healthineers

- Skanray Technologies Limited

- United Imaging Healthcare Co., Ltd.

- Varex Imaging

- Vieworks Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of chronic & orthopaedic disorders

- 4.2.2 Rapid detector & AI upgrades in DR panels

- 4.2.3 Cost-savings & dose-reduction versus film/CR

- 4.2.4 Procurement incentives for retrofit upgrades in mid-tier hospitals

- 4.2.5 Growth of point-of-care & home imaging ecosystems

- 4.2.6 Expansion of AI-driven teleradiology networks

- 4.3 Market Restraints

- 4.3.1 High CAPEX & total-cost-of-ownership

- 4.3.2 Reimbursement gaps in outpatient settings

- 4.3.3 Skilled radiographer shortage for advanced DR & AI workflows

- 4.3.4 Supply-chain risk in rare-earth scintillators

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Orthopaedic

- 5.1.2 Chest / Pulmonary

- 5.1.3 Dental

- 5.1.4 Cardiovascular

- 5.1.5 Oncology

- 5.1.6 Other Applications

- 5.2 By Technology

- 5.2.1 Computed Radiography (CR)

- 5.2.2 Direct Radiography (DR)

- 5.2.2.1 Flat-Panel Detectors

- 5.2.2.2 CCD/CMOS Panels

- 5.3 By Portability

- 5.3.1 Fixed Room-Based Systems

- 5.3.2 Portable Systems

- 5.3.2.1 Hand-held Units

- 5.3.2.2 Mobile Carts

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centres

- 5.4.3 Ambulatory Surgical Centers (ASCs)

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Agfa-Gevaert N.V.

- 6.4.2 Analogic Corporation

- 6.4.3 Canon Medical Systems Corporation

- 6.4.4 Carestream Health, Inc.

- 6.4.5 DRGEM Corporation

- 6.4.6 Esaote S.p.A.

- 6.4.7 Fujifilm Holdings Corporation

- 6.4.8 GE Healthcare

- 6.4.9 Hitachi, Ltd.

- 6.4.10 Hologic, Inc.

- 6.4.11 Konica Minolta, Inc.

- 6.4.12 Koninklijke Philips N.V.

- 6.4.13 Lotus Healthcare

- 6.4.14 Mindray Medical International Limited

- 6.4.15 Planmed Oy

- 6.4.16 Samsung Electronics Co., Ltd.

- 6.4.17 Shimadzu Corporation

- 6.4.18 Siemens Healthineers AG

- 6.4.19 Skanray Technologies Limited

- 6.4.20 United Imaging Healthcare Co., Ltd.

- 6.4.21 Varex Imaging Corporation

- 6.4.22 Vieworks Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment