|

시장보고서

상품코드

1836656

무수말레인산 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Maleic Anhydride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

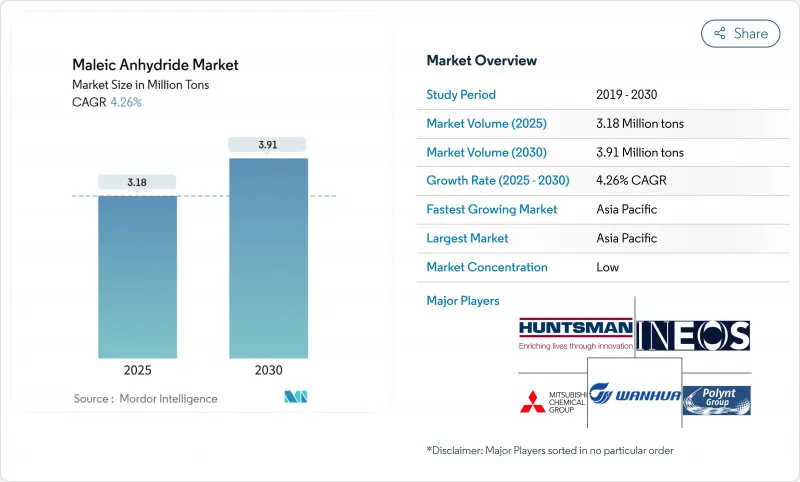

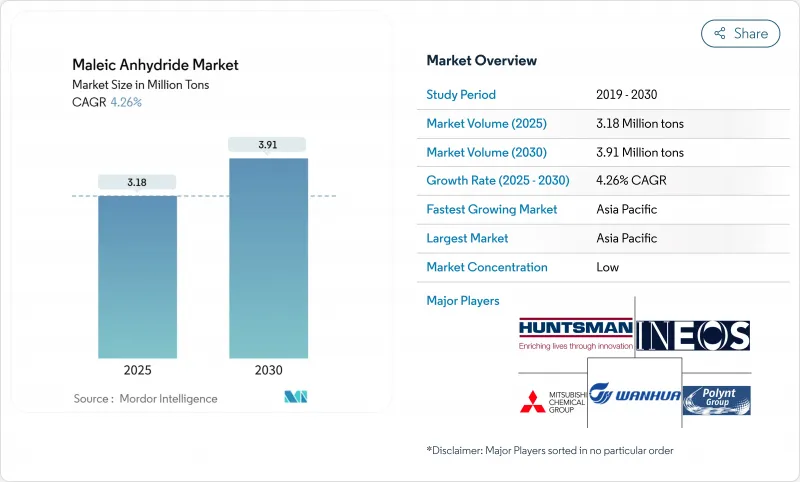

무수말레인산 시장 규모는 2025년 318만 톤으로 추정되고, 2030년에는 391만 톤으로 증가할 것으로 예측되며, CAGR 4.26%로 성장이 전망됩니다.

인프라 계획 확대, 불포화 폴리에스테르 수지의 지속적인 수요, 벤젠에서 n-부탄 원료로의 급속한 대안은 무수말레인산 시장을 지원하는 주요 성장 벡터입니다. 소비의 대부분을 차지하는 것은 건설용이며, 재생 PET UPR의 채용과 유럽의 엄격한 그린 빌딩 규칙이 이것을 뒷받침하고 있습니다. 북미의 자동차 제조업체는 경량 SMC 패널의 용도 범위를 넓혀 수지 수요에 기세를 두고 있습니다. 공급면에서는 아시아태평양의 생산 능력이 여전히 우위를 유지하고 있지만, 중국 공급 과잉이 세계의 마진을 압박하고, 다른 생산자를 고가치의 틈새 분야로 밀고 있습니다.

세계의 무수말레인산 시장 동향 및 인사이트

유럽 건설 산업에서 재활용 PET UPR 채택 급증

2024년 EU 포장 및 용기 포장 폐기물 규제에 의한 재활용 함유 기준치의 의무화에 의해 건설업자는 리사이클 PET 불포화 폴리에스테르 수지로 방향타를 끊고 있습니다. 이러한 배합은 버진 UPR과 동등한 65-72MPa의 인장 강도를 실현하여 매립 탄소를 최대 25% 삭감합니다. 무수말레인산은 폴리머 매트릭스의 계면 접착성을 향상시키고 복합재료의 내구성을 강화하며 저탄소 건축 재료에 대한 무수말레인산 시장을 뒷받침합니다.

원료 비용을 낮추는 N-부탄 플랜트의 능력 증강

최근 n-부탄의 스윙 용량 프로젝트는 벤젠에 대한 원료 비용의 격차를 넓히고 있습니다. BASF의 삼엽 촉매는 무수말레인산의 수율을 최대 2% 향상시키고 핫스팟 온도를 억제함으로써 에너지 강도를 감소시킵니다. 그 결과 비용면에서 유리하며, 무수말레인산 시장에서 n-부탄 루트의 점유율은 70%에 달했습니다.

OECD의 벤젠 배출 규제 강화로 컴플라이언스 비용 상승

미국의 유해물질 규제법 및 EU의 화학물질 관리 규칙의 개정은 벤젠 기반 유닛의 개조 또는 폐쇄를 강요하고 운전 비용을 증가시키고 n-부탄 산화로의 전환을 촉진합니다. 이 전환은 자본 투자의 필요성을 높이고 오래된 자산이 지배적인 지역에서 성장을 억제합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- EV용 경량 SMC 패널이 북미에서 UPR 소비 가속

- 바이오의 숙신산 루트가 고이익률의 공중합체 창출

- 원유에 연동하는 N-부탄 가격의 난고하

부문 분석

불포화 폴리에스테르 수지는 2024년에 무수말레인산 시장 점유율의 50%를 차지하였고, 이 부문은 2030년까지 연평균 복합 성장률(CAGR) 4.9%에서 상승할 전망입니다. 재활용 PET UPR 등급은 동일한 기계적 성능과 최대 25% 낮은 탄소 실적를 제공하여 에너지 효율적인 건물 채용을 촉진합니다. 동시에 경량 해양 구조물 및 전기자동차 부품의 성장도 수요를 지원합니다. 따라서 UPR 용도의 무수말레인산 시장 규모는 업계 전체의 평균을 넘어서고 있습니다.

1,4-부탄디올, 공중합체, 특수 계면활성제로의 다각화로 제품 믹스의 폭이 넓어지고 있습니다. 무수말레인산의 BDO로의 연속 수소화는 Cu-ZnO 촉매를 이용하여 190℃에서 85%의 수율을 달성하여 공정 효율의 향상을 나타내고 있습니다. 바이오의 숙신산으로부터 얻은 특수 공중합체는 생분해성 플라스틱의 프리미엄 가격을 획득하여 무수말레인산 산업의 마진 확대를 지원합니다.

N-부탄산화 공정은 벤젠에 비해 단가가 낮고 유해한 부산물이 적기 때문에 2024년 무수말레인산 시장에 70% 기여했습니다. 헌츠맨의 고정층 기술과 BASF의 삼엽 촉매의 조합은 압력 손실을 낮추면서 수율을 높이고 비용면에서 리더십을 강화합니다.

벤젠을 기반으로 하는 유닛은 주로 기존의 인프라가 있는 지역에서 운영하고 있습니다. 규모는 작지만 2030년까지 CAGR 4.69%로, 선택적 업그레이드와 특정 시장에서의 경쟁 원료 가격을 반영하고 있습니다. 이러한 원료 이중 세팅 시나리오는 자본 배분 결정을 형성하고 무수말레인산 시장에서 공급 유연성을 지원합니다.

지역 분석

아시아태평양은 2024년 무수말레인산 시장의 69%를 차지하였고, 2030년까지 CAGR 4.61%로 성장할 전망입니다. 중국의 생산 능력은 전 세계의 3분의 2를 넘어 공급을 지지하고 있습니다. 인도와 동남아시아는 인프라 투자 및 자동차 생산량 증가를 통해 수요를 유지하고 일본과 한국은 일본 촉매 등 기업을 통해 프로세스 혁신에 기여하고 있습니다.

북미는 기술적으로 선진적이면서 비용 경쟁력 있는 생산 거점입니다. 헌츠맨은 플로리다와 루이지애나에서 대규모 유닛을 운영하고 있으며, 원료 흐름과 다운스트림 용도를 통합합니다. 경량 EV 패널과 향후 n-부탄 증설이 이 지역의 성장을 강화하고 무수말레인산 시장의 수익 회복력을 강화하고 있습니다. 유럽은 에너지 비용 상승과 엄격한 배출 규제에 직면하고 있지만 지속가능성 채택, 특히 재생 PET UPR을 선도하고 있습니다.

남미의 점유율은 소폭이지만, 특수 비료용 킬레이트에서는 상승하고 있습니다. YPF 키미카는 지역 정밀 농업 우선순위에 따라 바이오 경로를 개발하고 있습니다. 중동 및 아프리카는 석유화학의 다양화에 투자하고 있으며, 미래의 무수말레인산 시장의 세계 확산을 초래할 수 있는 n-부탄 프로젝트를 위해 풍부한 원료를 활용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유럽 건설 업계에서 재활용 PET 기반 UPR 채용 급증

- N-부탄 플랜트의 능력 증강에 의한 원료 비용 저하

- 북미에서 UPR 소비를 가속하는 EV용 경량 SMC 패널

- 고이익률의 공중합체를 생산하는 바이오의 숙신산 루트

- 남미에서의 수용성 비료용 킬레이트 성장

- 시장 성장 억제요인

- OECD에서 벤젠 배출 규제 강화로 컴플라이언스 비용 상승

- 중국의 신규 생산 능력에 의한 세계 공급 과잉

- 원유에 연동하는 N-부탄 가격의 변동

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 가격 동향

제5장 시장 규모 및 성장 예측 : 수량

- 제품 유형별

- 불포화 폴리에스테르 수지

- 1,4-부탄디올

- 윤활유 첨가제

- 무수말레인산 공중합체

- 사과산

- 푸마르산

- 알킬숙신산 무수물

- 계면활성제 및 가소제

- 기타 제품 유형

- 원재료별

- N-부탄

- 벤젠

- 형상별

- 고체(플레이크 및 슬러리)

- 용융

- 최종 사용자 산업별

- 건설

- 자동차

- 일렉트로닉스

- 음식

- 석유제품

- 퍼스널케어

- 의약품

- 농업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AOC

- Arkema

- Ashland

- Bartek Ingredients Inc.

- BASF

- Borealis AG

- Clariant

- Evonik Industries AG

- Huntsman International LLC

- IG Petrochemicals Ltd.(IGPL)

- INEOS AG

- LANXESS

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- NIPPON SHOKUBAI CO., LTD.

- PETRONAS Chemicals Group Berhad

- Polynt SpA

- Sinopec Qilu Petrochemical

- SK Functional Polymer

- Thirumalai Chemicals

- Wanhua

제7장 시장 기회 및 전망

AJY 25.10.27The maleic anhydride market size reached 3.18 million tons in 2025 and is forecast to climb to 3.91 million tons by 2030, translating to a 4.26% CAGR.

Expanding infrastructure programs, sustained demand for unsaturated polyester resins, and the rapid substitution of benzene with n-butane feedstock are the principal growth vectors behind the maleic anhydride market. Construction accounts for the bulk of consumption, reinforced by recycled-PET UPR adoption and stringent green-building rules in Europe. North American automakers are broadening the application scope of lightweight SMC panels, adding momentum to resin demand. On the supply side, Asia Pacific's capacity leadership remains decisive, yet Chinese oversupply is compressing global margins and pushing producers elsewhere toward high-value niches.

Global Maleic Anhydride Market Trends and Insights

Surging Adoption of Recycled-PET UPR in Europe Construction

Mandatory recycled-content thresholds under the 2024 EU Packaging and Packaging Waste Regulation are steering builders toward recycled-PET unsaturated polyester resins. These formulations deliver tensile strength of 65-72 MPa, on par with virgin UPR, and trim embedded carbon by up to 25%. Maleic anhydride enhances interfacial adhesion in the polymer matrix, reinforcing composite durability and supporting the maleic anhydride market's push into low-carbon building materials.

Capacity Additions of N-Butane Plants Lowering Feedstock Cost

Recent n-butane swing-capacity projects are widening the feedstock cost gap versus benzene. BASF's trilobe-shaped catalyst lifts maleic anhydride yield by up to 2% and curbs hot-spot temperatures, translating into lower energy intensity. The resulting cost advantage is reinforcing the n-butane route's 70% share of the maleic anhydride market.

Stricter Benzene Emission Caps in OECD Raising Compliance Cost

Revisions to the U.S. Toxic Substances Control Act and EU chemical-management rules compel retrofits or closures of benzene-based units, inflating operating costs and incentivizing the migration to n-butane oxidation. The shift increases capital-spending needs and tempers growth in regions where older assets dominate.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight SMC Panels for EVs Accelerating UPR Consumption in North America

- Bio-based Succinic Acid Routes Creating High-Margin Copolymers

- N-Butane Price Volatility Linked to Crude

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unsaturated polyester resin held 50% of the maleic anhydride market share in 2024, and the segment is set to rise at a 4.9% CAGR through 2030. Recycled-PET UPR grades, offering identical mechanical performance and up to 25% lower carbon footprints, are catalyzing adoption in energy-efficient buildings. Concurrently, growth in lightweight marine structures and electric-vehicle components sustains demand. The maleic anhydride market size for UPR applications is therefore tracking above the overall industry average.

Diversification into 1,4-butanediol, copolymers, and specialty surfactants is widening the product mix. Continuous hydrogenation of maleic anhydride to BDO, achieving 85% yield over Cu-ZnO catalysts at 190 °C, illustrates process efficiency gains. Specialty copolymers derived from bio-based succinic acid are capturing premium pricing in biodegradable plastics, supporting margin expansion within the maleic anhydride industry.

N-butane oxidation processes contributed 70% to the maleic anhydride market in 2024, driven by lower unit costs and fewer hazardous by-products compared with benzene. Huntsman's fixed-bed technology, coupled with BASF's trilobe catalyst, lifts yield while lowering pressure drop, reinforcing cost leadership.

Benzene-based units operate mainly in regions where legacy infrastructure exists. Although smaller in scale, their 4.69% CAGR to 2030 reflects selective upgrades and competitive feedstock pricing in certain markets. This dual-track raw-material scenario shapes capital-allocation decisions and underpins supply flexibility in the maleic anhydride market.

The Maleic Anhydride Market Report Segments the Industry by Product Type (Unsaturated Polyester Resin, 1, 4-Butanediol, Lubricant Additives, and More), Raw Material (N-Butane and Benzene), Physical Form (Solid (Flake/Prill) and Molten), End-User Industry (Construction, Automobile, Food and Beverage, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia Pacific held 69% of the maleic anhydride market in 2024, and the region is poised for a 4.61% CAGR through 2030. China's capacity exceeds two-thirds of the global total, underpinning supply. India and Southeast Asia sustain demand through infrastructure spending and rising automotive output, while Japan and South Korea contribute process innovations via firms such as Nippon Shokubai.

North America presents a technologically advanced yet cost-competitive production base. Huntsman operates large-scale units in Florida and Louisiana, integrating feedstock streams and downstream applications. Lightweight EV panels and forthcoming n-butane expansions reinforce regional growth, reinforcing the maleic anhydride market's revenue resilience. Europe faces higher energy costs and strict emission curbs, yet leads sustainability adoption, especially recycled-PET UPR.

South America's share is modest but rising in specialty fertilizer chelates. YPF Quimica is developing bio-based pathways to align with regional precision-agriculture priorities. The Middle East and Africa are investing in petrochemical diversification, leveraging feedstock abundance for future n-butane projects that could broaden the maleic anhydride market's global footprint.

- AOC

- Arkema

- Ashland

- Bartek Ingredients Inc.

- BASF

- Borealis AG

- Clariant

- Evonik Industries AG

- Huntsman International LLC

- I G Petrochemicals Ltd. (IGPL)

- INEOS AG

- LANXESS

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- NIPPON SHOKUBAI CO., LTD.

- PETRONAS Chemicals Group Berhad

- Polynt S.p.A.

- Sinopec Qilu Petrochemical

- SK Functional Polymer

- Thirumalai Chemicals

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Recycled-PET-Based UPR in Europe Construction

- 4.2.2 Capacity Additions of N-Butane Plants Lowering Feedstock Cost

- 4.2.3 Lightweight SMC Panels for EVs Accelerating UPR Consumption in North America

- 4.2.4 Bio-based Succinic Acid Routes Creating High-Margin Copolymers

- 4.2.5 Water-Soluble Fertilizer Chelates Growth in South America

- 4.3 Market Restraints

- 4.3.1 Stricter Benzene Emission Caps in OECD Raising Compliance Cost

- 4.3.2 Global Oversupply from New Chinese Capacity

- 4.3.3 N-Butane Price Volatility Linked to Crude

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Price Trend

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Unsaturated Polyester Resin

- 5.1.2 1,4-Butanediol

- 5.1.3 Lubricant Additives

- 5.1.4 Maleic Anhydride Copolymers

- 5.1.5 Malic Acid

- 5.1.6 Fumaric Acid

- 5.1.7 Alkyl Succinic Anhydrides

- 5.1.8 Surfactants and Plasticizers

- 5.1.9 Other Product Types

- 5.2 By Raw Material

- 5.2.1 N-Butane

- 5.2.2 Benzene

- 5.3 By Physical Form

- 5.3.1 Solid (Flake/Prill)

- 5.3.2 Molten

- 5.4 By End-user Industry

- 5.4.1 Construction

- 5.4.2 Automobile

- 5.4.3 Electronics

- 5.4.4 Food and Beverage

- 5.4.5 Oil Products

- 5.4.6 Personal Care

- 5.4.7 Pharmaceuticals

- 5.4.8 Agriculture

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AOC

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Bartek Ingredients Inc.

- 6.4.5 BASF

- 6.4.6 Borealis AG

- 6.4.7 Clariant

- 6.4.8 Evonik Industries AG

- 6.4.9 Huntsman International LLC

- 6.4.10 I G Petrochemicals Ltd. (IGPL)

- 6.4.11 INEOS AG

- 6.4.12 LANXESS

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 NAN YA PLASTICS CORPORATION

- 6.4.15 NIPPON SHOKUBAI CO., LTD.

- 6.4.16 PETRONAS Chemicals Group Berhad

- 6.4.17 Polynt S.p.A.

- 6.4.18 Sinopec Qilu Petrochemical

- 6.4.19 SK Functional Polymer

- 6.4.20 Thirumalai Chemicals

- 6.4.21 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Commercialization of Bio-based Maleic Anhydride