|

시장보고서

상품코드

1836657

바이오포토닉스 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Biophotonics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

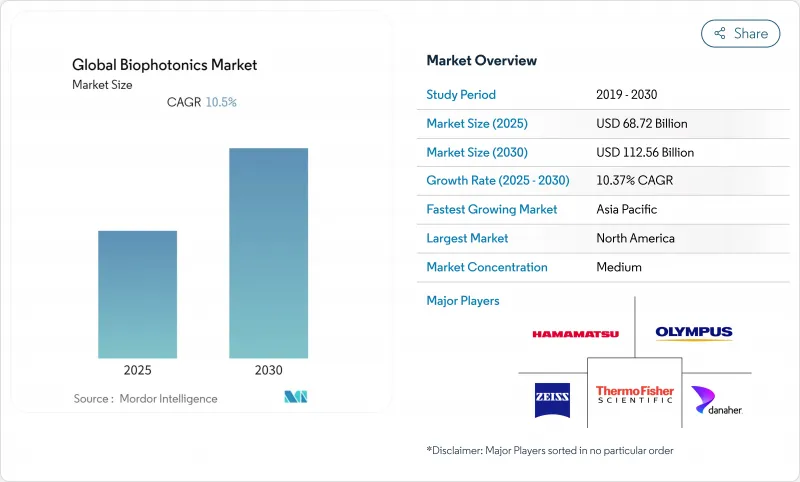

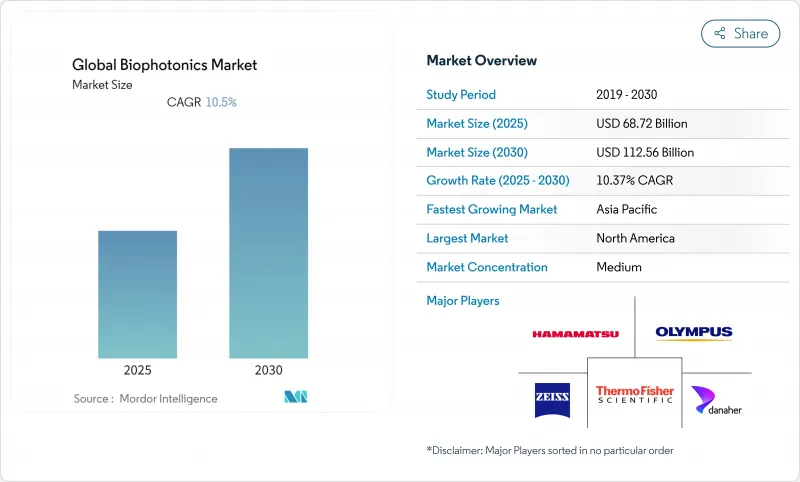

바이오포토닉스 시장 규모는 2025년에 687억 2,000만 달러로 추정되고, 2030년에는 1,125억 6,000만 달러에 이를 전망이며, CAGR 10.37%로 성장할 것으로 예측됩니다.

강력한 성장은 인공지능과 광학 기술의 융합에 기인하고 있으며, AI 대응 분광법은 비침습적 포도당 모니터링으로 98.8%의 정확도를 실현하고 있습니다. 광음향 토모그래피와 결합된 나노 기술은 현재 실시간 뇌졸중 평가를 지원하며 기존의 이미징에서 정밀 치료 지침으로의 전환을 시사하고 있습니다. 아시아태평양은 중국의 바이오제조에 대한 2024년 41억 7,000만 달러의 투자와 일본의 광칩에 대한 3억 700만 달러의 프로그램이 지역 기세를 만들고 가장 빠른 확대를 기록하고 있습니다. 레이저는 정밀 외과 수술의 채용에 의해 주요 제품 포지션을 유지하고, 이미징 시스템은 2030년까지 다른 제품 그룹을 상회할 전망입니다. 병원은 계속 수요를 지지하고 있지만 정부가 R&D 이니셔티브를 선호하기 때문에 학술기관의 움직임은 빠릅니다.

세계의 바이오포토닉스 시장 동향 및 인사이트

진단에서 바이오포토닉스 이용 증가

머신러닝으로 개량된 표면 증강 라만 분광법은 귀지 샘플을 이용한 두경부암 검출로 87%의 밸런스 정밀도를 달성했습니다. 광음향 단층 촬영은 뇌졸중 치료 중 실시간 혈관 모니터링을 제공합니다. 스마트폰 분광기는 440-1,300nm 노천 진단에서 1nm 해상도를 제공합니다. FDA는 근적외선 혈종 검출기를 위한 클래스 II 특수 제어 장치를 만들어 광학적 접근 방식을 검증했습니다. 6G 네트워크와의 통합은 즉각적인 임상 결정을 위한 초저지연 전송을 제공합니다.

증가하는 노인 인구

65세 이상의 고령자는 젊은층에 비해 3-4배의 진단 절차가 필요하며 장기적인 수요가 높아지고 있습니다. 근적외선 분광법은 지속적인 포도당 모니터링을 가능하게 하며 5억 3,700만 명의 당뇨병 환자를 수용합니다. 자가 형광 이미징은 구강암 수술에서 97%의 무종양 마진을 확보합니다. 광 바이오 모듈레이션은 알츠하이머의 관리를 지원합니다. 바이오 포토닉 플랫폼의 채택을 유지하기 위해 노화의 동향은 정밀의료와 일치합니다.

인식 및 숙련자 부족

직원은 광학, 생물학 및 데이터 사이언스 기술을 통합해야 하기 때문에 학제 간 전문 지식의 격차가 채용을 늦추고 있습니다. 광학 진단에 익숙하지 않은 임상의는 새로운 도구의 통합을 주저합니다. 대학은 목표를 잡은 커리큘럼의 제공에 고민하고 있어 즉전력이 되는 인재가 한정되어 있습니다. 규제 네비게이션이 복잡성을 늘리고 있습니다. 센트럴 플로리다 대학의 전용 실험실은 초기 조직적 대응을 반영합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 바이오포토닉스에서 나노 기술 출현

- 광음향 토모그래피(PAT)의 진보

- 바이오포토닉스 시스템의 고비용

부문 분석

2024년의 바이오포토닉스 시장 점유율은 레이저가 36.29%를 차지하였고, 정밀한 광선역학적 치료와 수술에서의 역할을 반영하고 있습니다. 이미징 시스템은 11.56%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되며, 이는 제품 중에서 최고입니다. 광섬유는 소형화의 동향으로부터 혜택을 누리고 웨어러블 바이오 센서에 전력을 공급하는 이점을 누릴 수 있습니다. 하이브리드 양자 감지는 단일 분자 검출을 향상시킵니다. 칼자이스는 포토닉스 사업부를 설립하여 역량을 강화합니다. 제조업체는 비용을 절감하고 부피 증가를 충족하기 위해 자동화된 라인에 투자합니다. 부품 표준화를 통해 장치 인증 속도를 높입니다. 광학 회사와 AI 스타트업 간의 협업 R&D는 플랫폼 융합을 가속화합니다. 환경 모니터링 장치는 핵심 이미징 모듈을 재사용하여 농업 및 수질 안전 전반에 걸쳐 해결 가능한 수요를 확대합니다.

시장 진출 기업은 빔 품질과 펄스 안정성을 개선하고 새로운 광 면역 요법 프로토콜을 지원합니다. 부품 공급업체는 고출력 다이오드 레이저를 위해 갈륨 비소 웨이퍼의 생산 능력을 확대합니다. 이미징 시스템 공급업체는 클라우드 기반 분석을 통합하여 해석 시간을 단축합니다. 이러한 복합적인 효과는 제품의 리더십을 유지하고 보다 광범위한 바이오포토닉스 시장을 지원합니다.

in-vitro 플랫폼은 확립된 실험실 워크플로우로 2024년에는 바이오포토닉스 시장 규모의 61.38%를 유지했습니다. 생체내 시스템은 임상가가 표본을 제거하지 않고 실시간 조직 평가를 제공하는 저침습 수술 지침 시스템을 선호하기 때문에 CAGR 10.89%로 상승할 것으로 예측됩니다. 광음향 단층 촬영은 현재 온전한 두개골을 통해 뇌 혈관을 시각화합니다. 라이트가이드는 단일 삽입 뇌생검으로 100% 진단 성공을 달성했습니다. 규제 당국이 실시간 장비에 관한 합리화된 경로를 개설하여 상업화를 촉진하고 있습니다. 웨어러블 모니터가 IoT 네트워크에 연결하여 지속적인 데이터 피드를 실현합니다. 에너지 효율이 높은 광원이 기기의 가동 시간을 연장합니다. 병원이 생체 내 출력을 전자 의료 기록에 통합하여 종단 케어를 강화합니다. 신흥 기업은 컴팩트한 콘솔로 외래수술센터(ASC)를 대상으로 합니다. 신흥 경피 프로브는 신진 대사 추적을 가능하게 하여 생체광학 시장의 확대 전망을 강화하고 있습니다.

지역별 분석

북미는 2024년에 바이오포토닉스 시장 점유율의 37.62%를 차지하였고, 성숙한 헬스케어 시스템과 보다 신속한 인가를 위해 방사선 최적화 시스템을 클래스 II로 분류하는 FDA의 틀에 의해 지원되고 있습니다. 서모 피셔는 국내 확대에 20억 달러를 할당해 분석기기 공급을 강화했습니다. Medicare의 상환 갭으로 인해 일부 진단 장비 배포가 제한됩니다. 전문 센터가 자궁 경부 광검진의 보험 적용을 획득하여 수요를 유지하고 있습니다. 연구 보조금이 AI와 포토닉스의 융합을 지원하고 지역의 희토류 정책이 레이저 다이오드 투입 확보를 목표로 합니다. 신흥기업이 핸드헬드 이미징을 상품화하고 바이오포토닉스 시장에 두께가 늘어남에 따라 경쟁이 격화됩니다.

유럽은 1,246억 유로의 포토닉스 에코시스템이 견인해, CAGR 10.14%로 견조한 성장을 나타냅니다. 칼자이스는 DORC를 흡수하고 매출의 15%를 연구개발에 투자함으로써 안과 포트폴리오를 강화했습니다. 의료기기 규제는 기준을 조화시키지만 소규모 기업의 컴플라이언스 비용을 상승시킵니다. 호라이즌 유럽의 자금 지원은 정밀 농업을 선호하고 광학 센서의 보급을 촉진합니다. 국경을 넘은 학술 컨소시엄이 기술 검증을 강화하고 지역의 지속가능성 목표에 합치하고 있습니다. 드레스덴의 반도체 연구소는 산업용 현미경 솔루션을 가속화하고 시장 깊이를 넓힙니다.

아시아태평양은 CAGR 11.20%로 전망되는 급성장 지역입니다. 중국은 2024년 41억 7,000만 달러의 바이오매뉴팩처링 주입으로 주도하고 있습니다. 상하이 교통 대학의 파일럿 포토닉 칩라인이 AI와 양자 애플리케이션을 뒷받침하고 있습니다. 일본의 3억 700만 달러의 광칩 프로그램은 반도체의 리더십을 목표로 하고 있습니다. 인도, 인프라 격차에도 불구하고 양자 포토닉스에 투자했습니다. 가격에 민감한 헬스케어 제공업체를 만족시키기 위해 현지 기업은 저가격 레이저 광원을 중시합니다. 정부의 우대조치로 진단용 광학기기의 수입세가 인하되고, 원격 의료에의 대처로 모바일 분광계가 충분한 서비스를 받지 않은 지역에 보급합니다. 동남아 전역의 급속한 클리닉 건설이 수요를 가속화하고 바이오포토닉스 시장의 확대를 지원하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 진단에서 바이오포토닉스의 이용 증가

- 신속한 PoC 검사를 위한 AI 대응 분광법

- 고령 인구 증가

- 바이오포토닉스에서 나노 기술 출현

- 광음향 토모그래피(PAT)의 진보

- 바이오포토닉스 센서의 정밀 농업 수요

- 시장 성장 억제요인

- 인식 및 숙련된 인재의 부족

- 바이오포토닉스 시스템의 고비용

- 엄격한 상환의 틀

- 레이저 다이오드의 희토류 공급 위험

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측 : 금액

- 제품 유형별

- 이미징 시스템

- 레이저

- 광섬유

- 기타

- 기술별

- In-Vitro

- In-Vivo

- 용도별

- 표면 이미징

- 인사이드 이미징

- 시스루 이미징

- 현미경 검사

- 바이오센서

- 분석 센싱

- 분광분자

- 광치료

- 광 코히어런스 토모그래피

- 용도별

- 검사 및 컴포넌트

- 의료 치료

- 의료 진단

- 비의료 용도

- 최종 사용자별

- 병원 및 클리닉

- 학술기관 및 연구기관

- 바이오테크놀러지 및 제약회사

- 식품품질연구소

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Agilent Technologies, Inc.

- Becton, Dickinson and Company

- Bruker Corporation

- Canon Medical Systems Corporation

- Carl Zeiss AG

- Danaher Corporation

- FUJIFILM Corporation

- GE Healthcare

- Glenbrook Technologies, Inc.

- Hamamatsu Photonics KK

- IDEX Corporation

- IPG Photonics Corporation

- LUMICKS

- Olympus Corporation

- Oxford Instruments PLC

- Revvity, Inc.

- Thermo Fisher Scientific Inc.

- Thorlabs, Inc.

- Toshiba Corporation

- Zenalux Biomedical Inc.

제7장 시장 기회 및 전망

AJY 25.10.27The biophotonics market size is USD 68.72 billion in 2025 and is forecast to reach USD 112.56 billion by 2030, advancing at a 10.37% CAGR.

Strong growth stems from the convergence of artificial intelligence with optical technologies, where AI-enabled spectroscopy delivers 98.8% accuracy in non-invasive glucose monitoring. Nanotechnology paired with photoacoustic tomography now supports real-time stroke assessment, signaling a shift beyond conventional imaging toward precision therapeutic guidance. Asia-Pacific records the fastest expansion as China's USD 4.17 billion 2024 investment in biomanufacturing and Japan's USD 307 million program in optical chips build regional momentum. Lasers hold the leading product position due to precision surgical adoption, while imaging systems outpace other product groups through 2030. Hospitals continue to anchor demand, yet academic institutes move quickly as governments prioritize R&D initiatives.

Global Biophotonics Market Trends and Insights

Increasing Use of Biophotonics in Diagnostics

Surface-enhanced Raman spectroscopy improved with machine learning reaches 87% balanced accuracy for head and neck cancer detection using ear wax samples. Photoacoustic tomography supplies real-time vascular monitoring during stroke treatment. Smartphone spectrometers delivering 1 nm resolution across 440-1,300 nm open field diagnostics. The FDA created Class II special controls for near-infrared hematoma detectors, validating optical approaches. Integration with 6G networks offers ultra-low latency transmission for instant clinical decisions.

Growing Geriatric Population

Individuals aged 65 plus require three to four times more diagnostic procedures than younger cohorts, elevating long-term demand. Near-infrared spectroscopy enables continuous glucose monitoring, addressing 537 million diabetes cases. Autofluorescence imaging secures 97% tumor-free margins in oral cancer surgery. Photobiomodulation supports Alzheimer's management. Aging trends align with precision medicine to sustain biophotonic platform adoption.

Lack of Awareness & Skilled Personnel

Interdisciplinary expertise gaps slow adoption because staff must unite optics, biology, and data science skills. Clinicians unfamiliar with optical diagnostics hesitate to integrate new tools. Universities struggle to offer targeted curricula, limiting ready talent. Regulatory navigation adds complexity. Dedicated laboratories at the University of Central Florida reflect early institutional responses.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Nanotechnology in Biophotonics

- Advancements in Photo-acoustic Tomography (PAT)

- High Cost of Biophotonic Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lasers contributed 36.29% to the biophotonics market share in 2024, reflecting their role in precise photodynamic therapy and surgical work. Imaging systems are forecast to register an 11.56% CAGR, the highest among products, as surgeons seek real-time tissue characterization during operations. Fiber optics benefit from miniaturization trends, powering wearable biosensors. Hybrid quantum sensing improves single-molecule detection. Carl Zeiss consolidated capabilities by forming photonics business units. Manufacturers invest in automated lines to curb costs and meet growing volume. Greater component standardization speeds device certification. Collaborative R&D between optics firms and AI start-ups accelerates platform convergences. Environmental monitoring devices reuse core imaging modules, widening the addressable demand across agriculture and water safety.

Market participants refine beam quality and pulse stability to support emerging photoimmunotherapy protocols. Component vendors expand gallium arsenide wafer capacity for higher-power diode lasers. Imaging system suppliers integrate cloud-based analytics to cut interpretation time. The combined effect sustains product leadership while anchoring the broader biophotonics market.

In-vitro platforms maintained 61.38% of the biophotonics market size in 2024, thanks to established lab workflows. In-vivo systems are predicted to rise at a 10.89% CAGR as clinicians favor minimally invasive surgical guidance systems that provide real-time tissue assessment without specimen removal. Photoacoustic tomography now visualizes cerebral vessels through intact skulls. Optical guidance achieves 100% diagnostic success in single-insertion brain biopsies. Regulatory agencies outline streamlined pathways for real-time devices, aiding commercialization. Wearable monitors connect to IoT networks for continuous data feeds. Energy-efficient light sources extend device operating times. Hospitals integrate in vivo outputs into electronic health records, enhancing longitudinal care. Start-ups target ambulatory surgery centers with compact consoles. Emerging transdermal probes enable metabolic tracking, reinforcing expansion prospects for the biophotonics market.

The Biophotonics Market Report is Segmented by Product Type (Imaging Systems and More), Technology (In-Vitro and In-Vivo), Application (Surface Imaging, Inside Imaging, and More), Usage (Tests and Components, Medical Therapeutics, and More), End-User (Hospitals & Clinics and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 37.62% of biophotonics market share in 2024, supported by a mature healthcare system and an FDA framework that now classifies radiological optimization systems under Class II for faster clearance. Thermo Fisher allocated USD 2 billion for domestic expansion, reinforcing analytical instrument supply. Medicare reimbursement gaps limit some diagnostic rollouts. Specialist centers gain coverage for optical cervical screening, sustaining demand. Research grants underpin AI-photonics convergence, while the region's rare-earth policies aim to secure laser diode inputs. Competition intensifies as start-ups commercialize handheld imaging, adding depth to the biophotonics market.

Europe posts a steady 10.14% CAGR, driven by a EUR 124.6 billion photonics ecosystem. Carl Zeiss advances ophthalmic portfolios by absorbing DORC and investing 15% of revenue back into R&D. The Medical Device Regulation harmonizes standards yet raises compliance costs for small firms. Horizon Europe funding prioritizes precision agriculture, lifting uptake of optical sensors. Cross-border academic consortia enhance technology validation, aligning with regional sustainability goals. Semiconductor laboratories in Dresden accelerate industrial microscopy solutions, extending market depth.

Asia-Pacific is the fastest-growing region at 11.20% CAGR. China leads with a USD 4.17 billion biomanufacturing infusion in 2024. Pilot photonic chip lines in Shanghai Jiao Tong University boost AI and quantum applications. Japan's USD 307 million optical chip program seeks semiconductor leadership. India invests in quantum photonics despite infrastructure gaps. Local firms emphasize low-cost laser sources to satisfy price-sensitive healthcare providers. Government incentives lower import taxes on diagnostic optics, while telehealth efforts spread mobile spectrometers to underserved zones. Rapid clinic construction across Southeast Asia accelerates demand, supporting expansion of the biophotonics market.

- Agilent Technologies

- Beckton Dickinson

- Bruker

- Canon

- Carl Zeiss

- Danaher

- FUJIFILM

- GE Healthcare

- Glenbrook Technologies, Inc.

- Hamamatsu Photonics

- IDEX

- IPG Photonics

- LUMICKS

- Olympus

- Oxford Instruments

- Revvity, Inc.

- Thermo Fisher Scientific

- Thorlabs

- Toshiba

- Zenalux Biomedical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing use of biophotonics in diagnostics

- 4.2.2 AI-enabled spectroscopy for rapid PoC testing

- 4.2.3 Growing geriatric population

- 4.2.4 Emergence of nanotechnology in biophotonics

- 4.2.5 Advancements in photo-acoustic tomography (PAT)

- 4.2.6 Precision-agriculture demand for biophotonic sensors

- 4.3 Market Restraints

- 4.3.1 Lack of awareness & skilled personnel

- 4.3.2 High cost of biophotonic systems

- 4.3.3 Stringent reimbursement frameworks

- 4.3.4 Rare-earth supply risk for laser diodes

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Imaging Systems

- 5.1.2 Lasers

- 5.1.3 Fiber Optics

- 5.1.4 Others

- 5.2 By Technology

- 5.2.1 In-Vitro

- 5.2.2 In-Vivo

- 5.3 By Application

- 5.3.1 Surface Imaging

- 5.3.2 Inside Imaging

- 5.3.3 See-through Imaging

- 5.3.4 Microscopy

- 5.3.5 Biosensors

- 5.3.6 Analytics Sensing

- 5.3.7 Spectromolecular

- 5.3.8 Light Therapy

- 5.3.9 Optical Coherence Tomography

- 5.4 By Usage

- 5.4.1 Tests and Components

- 5.4.2 Medical Therapeutics

- 5.4.3 Medical Diagnostics

- 5.4.4 Non-Medical Application

- 5.5 By End-User

- 5.5.1 Hospitals & Clinics

- 5.5.2 Academic & Research Institutes

- 5.5.3 Biotechnology & Pharma Companies

- 5.5.4 Food-Quality Labs

- 5.5.5 Other End-Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Agilent Technologies, Inc.

- 6.4.2 Becton, Dickinson and Company

- 6.4.3 Bruker Corporation

- 6.4.4 Canon Medical Systems Corporation

- 6.4.5 Carl Zeiss AG

- 6.4.6 Danaher Corporation

- 6.4.7 FUJIFILM Corporation

- 6.4.8 GE Healthcare

- 6.4.9 Glenbrook Technologies, Inc.

- 6.4.10 Hamamatsu Photonics KK

- 6.4.11 IDEX Corporation

- 6.4.12 IPG Photonics Corporation

- 6.4.13 LUMICKS

- 6.4.14 Olympus Corporation

- 6.4.15 Oxford Instruments PLC

- 6.4.16 Revvity, Inc.

- 6.4.17 Thermo Fisher Scientific Inc.

- 6.4.18 Thorlabs, Inc.

- 6.4.19 Toshiba Corporation

- 6.4.20 Zenalux Biomedical Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment