|

시장보고서

상품코드

1836659

약물감시 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Pharmacovigilance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

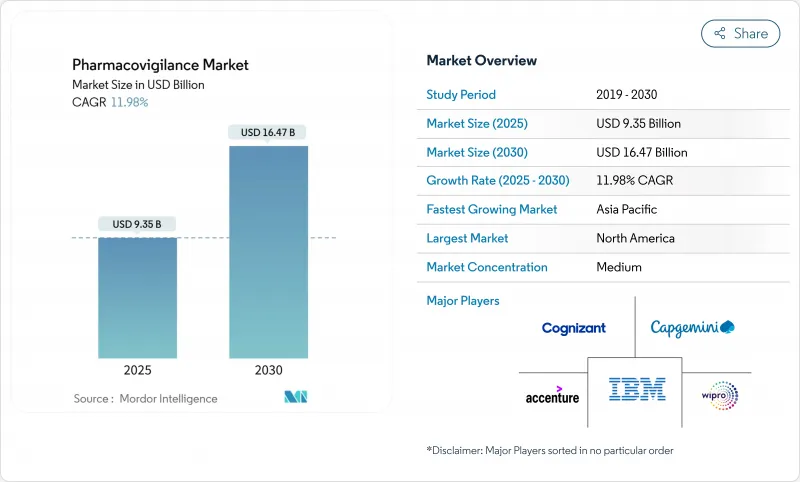

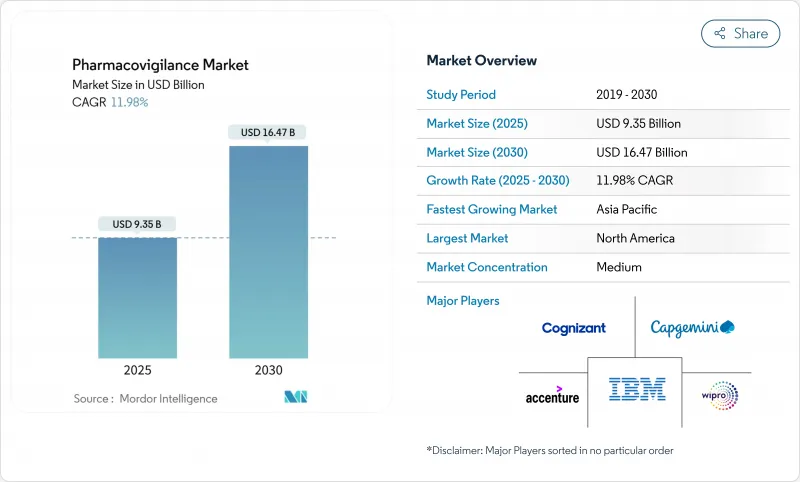

약물감시 시장은 2025년 93억 5,000만 달러로 추정되고, CAGR 11.98%로 성장할 전망이며, 2030년에는 164억 7,000만 달러에 이를 것으로 예측됩니다.

의약품 파이프라인의 확대, 시판 후 조사 규칙의 엄격화, 안전성 감시 워크플로우에 대한 인공지능(AI)의 급속한 도입이 이 기세를 지지하고 있습니다. 제약 회사는 생물 제제, 유전자 치료 및 기타 복잡한 치료법이 상업적으로 사용됨에 따라 적극적인 안전 관리에 자원을 돌리고 있습니다. 클라우드 기반 AI 플랫폼을 갖춘 CRO(의약품 개발 업무 수탁기관)는 비용 효율적인 컴플라이언스를 제공하여 아웃소싱 시프트를 가속화하고 있습니다. 시판 후 조사 의무에 의해 데이터량이 증대하고, 전자 차트(EHR)의 마이닝이 가장 급성장하고 있는 보고 방법이 되고 있습니다. 북미는 성숙한 규제 과학에 의해 주도권을 유지하고 있지만, 아시아태평양(APAC)의 하모나이제이션 이니셔티브가 이 지역의 2자리 성장을 뒷받침하고 있습니다.

세계의 약물감시 시장 동향 및 인사이트

의약품 소비 및 개발 파이프라인 증가

FDA는 2024년에 50개의 새로운 분자 엔티티를 승인했으며, 획기적인 승인이 모든 후원자에게 시판 후 안전 의무를 어떻게 확대하는지 강조하고 있습니다. 유전자 치료제, CAR-T 치료제 및 제제는 제품의 수명주기를 통해 신중한 모니터링이 필요한 독특한 위험 프로파일을 제공합니다. 조건부 승인은 리얼 월드 에비던스(RWE)에 대한 기대를 높여 지속적인 모니터링 인프라에 예산을 돌려줍니다. 이러한 역학을 통해 약물감시 팀은 임상 개발을 넘어 작업량 증가를 유지하는 장기적인 확대 사이클에 통합될 것입니다.

부작용(ADR) 증가

유럽 의약품청(EMA)의 약물감시 위험 평가위원회(PRAC)는 최근 2차 악성 종양의 가능성을 관찰한 후 CAR-T 수령인의 평생 모니터링을 강조했습니다. 노인 집단의 다균성은 약물-약물 상호 작용을 증가시키고 ADR 사례 수를 증가시킵니다. 팬데믹 시대의 백신 배포는 수백만 건의 안전 보고서를 몇 주 이내에 처리할 수 있는 대규모 신호 감지 네트워크의 중요성을 확인했습니다.

사이버 보안 및 데이터 프라이버시 위험

정밀성이 높은 환자 데이터의 클라우드 전개로 안전 시스템은 랜섬웨어와 국가에 의한 침입에 노출됩니다. 최근의 헬스케어 침해로 인해 일부 스폰서들은 EHR 통합을 일시중지해야 했지만, 한편으로는 감사가 안전성 시그널링을 수행하지 않았음을 확인하였습니다. 일반 데이터 보호 규칙(GDPR-EU 개인정보보호규정)과 유사한 법률은 데이터 최소화 및 현지화 전략을 의무화하며 세계 분석의 야심과 상충될 수 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- CRO 및 BPO 벤더에의 PV 서비스의 아웃소싱

- AI에 의한 신호 검출 및 예측 분석

- PV 전문 인력 부족 및 높은 이직률

부문 분석

4단계 시험은 2024년 약물감시 시장 점유율의 32.18%를 차지했으며, 혁신적 치료의 평생 모니터링에 대한 규제 당국 수요를 반영합니다. 전임상 안전성 평가에 수반되는 약물감시 시장 규모는 리스크 기반의 초기단계 분석에 의해 13.13%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 적응 시험 설계는 2단계 및 3단계를 단축하지만, 제품이 광범위한 집단에 투여되면 충실도가 높은 신호 검출의 중요성이 높아집니다. 업데이트된 ICH E6(R3) 가이드라인은 스폰서에게 전체 단계에 걸쳐 품질-비-디자인 지표를 통합하도록 강제하고, 인간에게 처음 투여한 것으로부터 추적 가능한 안전성 데이터의 획득을 보장합니다.

약물감시 시장은 환자에 대한 직접 샘플링과 웨어러블 센서를 이용한 분산형 시험을 통합함으로써 대응하고 있습니다. AI 모델은 최초 환자 투여 전에 표적외 영향을 시뮬레이션하여 기업이 리스크 관리 계획을 선점하게 합니다. 조건부 승인이 증가함에 따라 승인 후 안전성 시험(PASS) 예산은 기존의 3단계 지출을 초과하며 4단계의 장점은 장기 전망에 고정됩니다.

아웃소싱 계약은 2024년 전체 수익의 55.46%를 차지했고, 2030년까지 13.73%로 성장할 것으로 예측되며 약물감시 시장에서 가장 큰 슬라이스를 유지하고 있습니다. 자사 부서는 중요한 의사결정을 유지하지만 CRO 플랫폼이 정형 업무를 처리하는 하이브리드 모델에 대한 의존도가 높아지고 있습니다. 팔렉셀의 패런티어와의 다년간에 걸친 AI 제휴와 같은 전략적 제휴는 기술 강화된 CRO가 어떻게 경쟁력을 키우는지를 보여줍니다.

약물감시 업계에서는 현재 확장 가능한 데이터 레이크, 과학문헌의 자연언어처리(NLP), 흡입 시 로봇에 의한 프로세스 자동화가 중시되고 있습니다. 결과적으로 주요 제약 회사조차도 워크로드를 인도, 아일랜드, 동유럽의 외부 허브로 전환하고 단편 공급업체 목록을 AI 투자 로드맵을 보장하는 기본 서비스 계약에 통합합니다.

지역별 분석

북미는 2024년에 약물감시 시장의 44.18%를 차지했는데, 이는 높은 연구개발 강도, 고급 EHR의 보급, 명확한 규제 상의 기대 때문입니다. FDA가 점진적인 검증 프레임워크를 발표함에 따라 AI 파일럿이 급속히 받아들여지며, 이 지역은 디지털 약물감시의 세계적인 기준으로 자리매김하고 있습니다.

유럽은 EudraVigilance 네트워크를 지원하는 성숙한 법률과 알고리즘의 투명성을 요구하는 한편 혁신을 장려하는 새로운 AI 반영 페이퍼로 추종하고 있습니다. 첨단 치료제에 초점을 맞추면 전문적인 모니터링 요구가 생겨 2030년까지 투자가 지속될 전망입니다. EU 기반 PASS의 약물감시 시장 규모는 희귀의약품의 승인과 함께 성장하고 있습니다.

아시아태평양의 CAGR은 13.64%로 세계에서 가장 빠른 것으로 예측됩니다. 이것은 중국의 규제 개혁과 인도의 임상시험 상황의 확대와 관련이 있습니다. ASEAN 국가는 표시와 전자 신청 기준을 맞추어 여러 국가에서 안전 캠페인을 간소화합니다. 국내 생명공학 제조업에 대한 투자는 현지에 뿌리를 둔 사례 처리 허브에 대한 수요를 자극합니다. 중동, 아프리카 및 남미는 의약품 수입량과 신흥 제조 클러스터에 맞추어 약물감시 인프라의 규모를 확대하여 더욱 성장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의약품 소비량 및 개발 파이프라인 증가

- 부작용(ADRS) 증가

- CRO 및 BPO 벤더에 대한 Pv 서비스 아웃소싱

- AI에 의한 신호 검출 및 예측 분석

- 리얼 월드 에비던스(RWE) 플랫폼의 확대

- 적극적인 시판 후 안전성 조사에 대한 엄격한 규제의 의무화

- 시장 성장 억제요인

- 사이버 보안 및 데이터 프라이버시의 위험

- 세계 규제 조화 및 데이터 표준의 부족

- PV 전문 인력 부족 및 높은 이직률

- 배합제 및 ATMP 요법의 복잡성

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 임상시험 페이즈별

- 전 임상시험

- 페이즈 I

- 페이즈 II

- 페이즈 III

- 페이즈 IV

- 서비스 제공업체별

- 인하우스

- 아웃소싱 계약

- 보고 유형별

- 자발적 보고

- ADR 보고 강화

- 대상 자발 보고

- 코호트 이벤트 모니터링

- EHR 마이닝

- 최종 사용자별

- 병원

- 제약회사

- CRO 및 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Accenture

- ArisGlobal

- BioClinica(NOW Clario)

- Capgemini

- Cognizant

- IBM

- ICON plc

- IQVIA

- ITClinical

- Labcorp

- Linical Accelovance

- Parexel

- UBC(United BioSource)

- TAKE Solutions(Navitas Life Sciences)

- Wipro

- Oracle Health Sciences

- Ennov

- Extedo

- Clarivate(Drug Safety Triager)

- SGS Life Sciences

제7장 시장 기회 및 전망

AJY 25.10.27The pharmacovigilance market is valued at USD 9.35 billion in 2025 and is forecast to reach USD 16.47 billion by 2030, advancing at an 11.98% CAGR.

Expanding drug pipelines, stricter post-marketing surveillance rules and rapid adoption of artificial intelligence (AI) across safety-monitoring workflows sustain this momentum.Pharmaceutical companies are redirecting resources toward proactive safety management as biologics, gene therapies and other complex modalities enter commercial use. Contract research organizations (CROs) equipped with cloud-based AI platforms offer cost-efficient compliance, accelerating the outsourcing shift. Post-marketing surveillance obligations enlarge data volumes, making electronic health record (EHR) mining the fastest-growing reporting method. North America retains leadership owing to mature regulatory science, but harmonization initiatives in Asia-Pacific (APAC) propel that region's double-digit growth.

Global Pharmacovigilance Market Trends and Insights

Increasing Drug Consumption & Development Pipeline

The FDA cleared 50 new molecular entities in 2024, underscoring how breakthrough approvals widen post-marketing safety duties for every sponsor. Gene therapies, CAR-T treatments and combination products pose unique risk profiles that require vigilant monitoring throughout the product life cycle. Conditional approvals further heighten real-world evidence (RWE) expectations, redirecting budgets toward continuous surveillance infrastructures. These dynamics lock pharmacovigilance teams into a long-term expansion cycle that sustains workload growth beyond clinical development.

Growing Incidence Of Adverse Drug Reactions (ADRs)

The European Medicines Agency (EMA) Pharmacovigilance Risk Assessment Committee (PRAC) recently emphasized lifelong monitoring for CAR-T recipients after observing potential secondary malignancies. Polypharmacy in elderly populations multiplies drug-drug interactions, pushing ADR case volumes higher. The pandemic-era vaccine rollout validated the importance of large-scale signal-detection networks capable of processing millions of safety reports within weeks.

Cyber-Security & Data-Privacy Risks

Cloud deployment of sensitive patient data exposes safety systems to ransomware and nation-state intrusions. Recent healthcare breaches forced several sponsors to suspend EHR integrations while audits ensured no safety signal manipulation occurred. General Data Protection Regulation (GDPR) and similar laws mandate data-minimization and localization strategies that sometimes conflict with global analytics ambitions.

Other drivers and restraints analyzed in the detailed report include:

- Outsourcing Of PV Services To CRO/BPO Vendors

- AI-Enabled Signal Detection & Predictive Analytics

- Shortage Of Specialised PV Talent & High Staff Turnover

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Phase IV studies held 32.18% of pharmacovigilance market share in 2024, reflecting regulators' demand for life-long monitoring of innovative therapies. The pharmacovigilance market size attached to pre-clinical safety assessments is projected to expand at a 13.13% CAGR thanks to risk-based early-phase analytics. Adaptive trial designs shorten Phases II and III, but heighten the importance of high-fidelity signal detection once products reach broad populations. Updated ICH E6(R3) guidelines compel sponsors to embed quality-by-design metrics across all phases, ensuring traceable safety data capture from first-in-human dosing.

The pharmacovigilance market responds by integrating decentralized trials with direct-to-patient sampling and wearable sensors. AI models simulate off-target effects before first-patient dosing, giving companies a head start in risk-management planning. As conditional approvals rise, Post-Authorization Safety Studies (PASS) budgets eclipse traditional Phase III spends, locking Phase IV dominance into the long-term outlook.

Contract outsourcing controlled 55.46% of overall revenue in 2024 and is forecast to grow at 13.73% through 2030, sustaining the largest slice of the pharmacovigilance market. In-house units retain critical decision-making but increasingly rely on hybrid models where CRO platforms process routine tasks. Strategic alliances such as Parexel's multi-year AI pact with Palantir exemplify how tech-enhanced CROs cultivate competitive edge.

The pharmacovigilance industry now values scalable data lakes, natural language processing (NLP) for scientific literature and robotic process automation in intake. As a result, even large pharmaceutical companies migrate workloads to external hubs in India, Ireland and Eastern Europe, consolidating fragmented vendor lists into master service agreements that guarantee AI investment roadmaps.

The Pharmacovigilance Market Report is Segmented by Clinical Trial Phase (Preclinical, Phase I, Phase II, and More), Service Provider (In-House, Contract Outsourcing), Type of Reporting (Spontaneous Reporting, Intensified ADR Reporting, and More), End User (Hospitals, Pharmaceutical Companies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 44.18% of the pharmacovigilance market in 2024 due to high R&D intensity, advanced EHR penetration and clear regulatory expectations. AI pilots gain rapid acceptance as the FDA publishes step-wise validation frameworks, positioning the region as the global reference for digital pharmacovigilance.

Europe follows with mature legislation underpinning the EudraVigilance network and new AI reflection papers that encourage innovation while demanding algorithm transparency. Focus on Advanced Therapy Medicinal Products brings specialized monitoring needs, sustaining investment through 2030. The pharmacovigilance market size for EU-based PASS grows alongside orphan-drug approvals.

Asia-Pacific is projected to log a 13.64% CAGR, the fastest worldwide, as China's regulatory reforms and India's expanded clinical-trial landscape converge. ASEAN nations align labeling and electronic submission standards, simplifying multi-country safety campaigns. Investments in domestic biotech manufacturing stimulate demand for localized case-processing hubs. Middle East & Africa and South America add incremental growth where pharmacovigilance infrastructure scales with pharmaceutical import volumes and emerging manufacturing clusters.

- Accenture

- Aris Global

- BioClinica (NOW Clario)

- Capgemini

- Cognizant

- IBM

- ICON

- IQVIA

- ITClinical

- LabCorp

- Linical Accelovance

- Parexel International

- UBC (United BioSource)

- TAKE Solutions (Navitas Life Sciences)

- Wipro

- Oracle Health Sciences

- Ennov

- Extedo

- Clarivate (Drug Safety Triager)

- SGS Life Sciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Drug Consumption & Development Pipeline

- 4.2.2 Growing Incidence Of Adverse Drug Reactions (ADRS)

- 4.2.3 Outsourcing Of Pv Services To CRO/BPO Vendors

- 4.2.4 AI-Enabled Signal Detection & Predictive Analytics

- 4.2.5 Expansion Of Real-World Evidence (RWE) Platforms

- 4.2.6 Stringent Regulatory Mandates For Proactive Post-Marketing Safety Surveillance

- 4.3 Market Restraints

- 4.3.1 Cyber-Security & Data-Privacy Risks

- 4.3.2 Lack Of Global Regulatory Harmonisation & Data Standards

- 4.3.3 Shortage Of Specialised PV Talent & High Staff Turnover

- 4.3.4 Complexity Of Combination & ATMP Therapies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Clinical Trial Phase

- 5.1.1 Pre-clinical

- 5.1.2 Phase I

- 5.1.3 Phase II

- 5.1.4 Phase III

- 5.1.5 Phase IV

- 5.2 By Service Provider

- 5.2.1 In-house

- 5.2.2 Contract Outsourcing

- 5.3 By Type of Reporting

- 5.3.1 Spontaneous Reporting

- 5.3.2 Intensified ADR Reporting

- 5.3.3 Targeted Spontaneous Reporting

- 5.3.4 Cohort Event Monitoring

- 5.3.5 EHR Mining

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Pharmaceutical Companies

- 5.4.3 CROs & Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Accenture

- 6.3.2 ArisGlobal

- 6.3.3 BioClinica (NOW Clario)

- 6.3.4 Capgemini

- 6.3.5 Cognizant

- 6.3.6 IBM

- 6.3.7 ICON plc

- 6.3.8 IQVIA

- 6.3.9 ITClinical

- 6.3.10 Labcorp

- 6.3.11 Linical Accelovance

- 6.3.12 Parexel

- 6.3.13 UBC (United BioSource)

- 6.3.14 TAKE Solutions (Navitas Life Sciences)

- 6.3.15 Wipro

- 6.3.16 Oracle Health Sciences

- 6.3.17 Ennov

- 6.3.18 Extedo

- 6.3.19 Clarivate (Drug Safety Triager)

- 6.3.20 SGS Life Sciences

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment