|

시장보고서

상품코드

1836663

첨단 시각화 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Advanced Visualization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

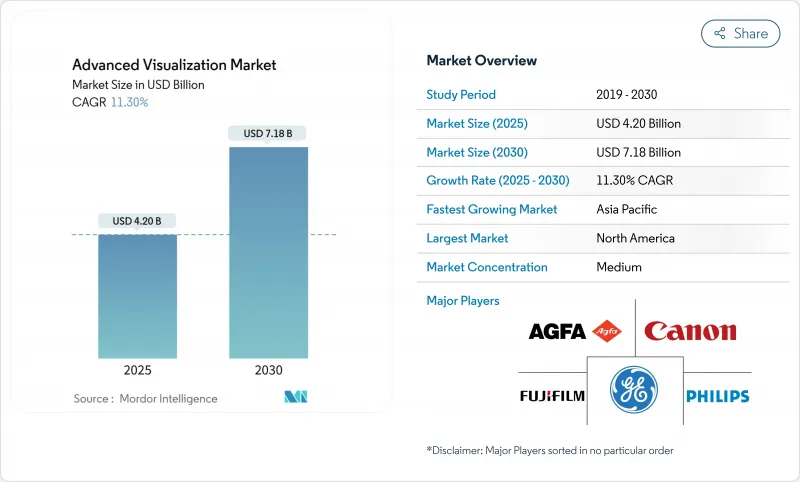

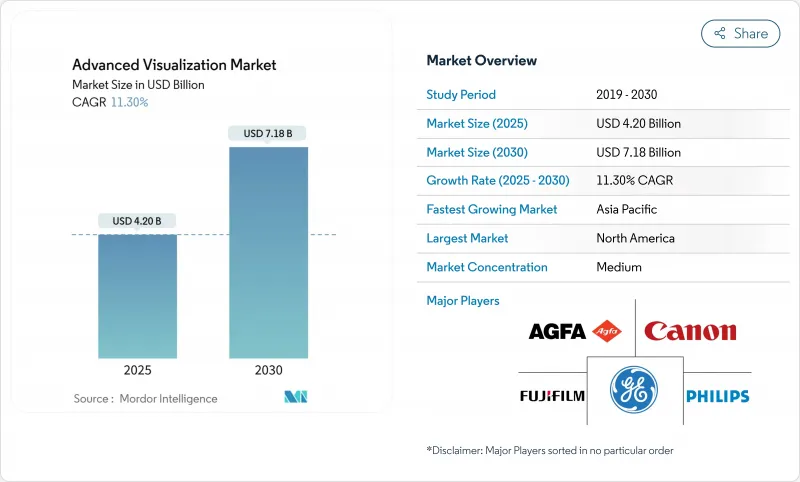

첨단 시각화 시장은 2025년에 42억 달러로 추정되고, CAGR 11.3%로 성장할 전망이며, 2030년에는 71억 8,000만 달러로 상승할 것으로 예측되고 있습니다.

AI를 탑재한 이미지 처리 소프트웨어, 광자 카운팅 CT 스캐너, 클라우드 대응 엔터프라이즈 플랫폼에 대한 왕성한 수요가 병원과 진단센터의 설비 투자를 가속화하고 있습니다. 임상 현장에서는 AI의 자동 세분화에 의해 방사선 판독 시간이 40% 이상 단축되고, 포톤 카운팅 CT는 저선량으로 0.2mm 이하의 해상도를 실현하며, 정량적인 뇌 영상 및 심혈관 영상을 위한 새로운 CPT 코드가 새로운 상환의 흐름을 이끌어내고 있습니다. 대규모 기업용 PACS/VNA의 도입은 다시설 연계를 촉진하고, 보안 클라우드의 도입은 유럽의 엄격한 데이터 주권 규칙에도 불구하고 지지를 모으고 있습니다. 디바이스 제조업체가 GPU 벤더와 함께 실시간 AI를 스캐너에 통합함과 동시에 서비스 계약에 의해 수익이 단발 시스템 판매에서 정기적인 구독 기반 모델로 이동함으로써 경쟁의 격렬함이 증가하고 있습니다.

세계의 첨단 시각화 시장 동향 및 인사이트

AI를 활용한 자동 세분화가 진단 효율 변화

1,000개가 넘는 임상 AI 애플리케이션(방사선과용은 77%)의 연방정부 인가로 워크플로우 자동화가 합법화되고, Canon Medical INSTINX와 같은 플랫폼은 심장 CT 워크플로우 클릭을 40% 삭제하며, Phillips SmartSpeed Precise는 80% 선명한 이미지로 MRI 스캔을 3배 빨리 종료시킵니다. 이러한 생산성 향상은 방사선기사의 결원률 18.1%를 상쇄하는 데 도움이 됩니다. 인터벤셔널 스위트에서는 실시간 세분화이 경동맥 스텐트 유치술을 94%의 재현 정확도로 안내하게 되어 AI의 가치가 진단에서 치료 계획으로 퍼지고 있습니다.

엔터프라이즈 PACS 통합이 비즈니스 통합 촉진

Sectra의 클라우드 엔터프라이즈 이미징 제품군에 대한 40억 크로네 이상의 기록적인 주문은 데이터 사일로를 근절하고 방사선과, 순환기과 및 병리학 워크플로우를 표준화하는 통합 아키텍처에 대한 의료 시스템의 의욕을 뒷받침합니다. PACSonWEB와 같은 클라우드 네이티브 PACS의 도입은 의사가 언제 어디서나 이미지를 볼 수 있기 때문에 12개월 이내에 병원 간 도입을 10% 증가시켰습니다. 구독 가격은 영구 라이선스를 추월하고 자본 지출을 줄이며 업타임 및 사이버 보안 성능 보증을 공급업체 인센티브와 일치시킵니다.

데이터 프라이버시 규정이 클라우드 장벽 구축

암호화 키의 주권을 국경과 연결하는 GDPR(EU 개인정보보호규정) 조항을 통해 클라우드 PACS 공급업체는 정교한 키 관리 인프라를 도입해야 하며, 유럽에서는 도입 비용이 상승하고 판매 사이클이 장기화됩니다. 방사선과를 대상으로 하는 사이버 사건은 2024년 67% 증가해 퍼블릭 클라우드의 리스크 프로파일에 대한 구매자의 모니터링이 강화되고 병원은 환자 식별자를 온프레미스로 유지하면서 AI 추론을 위해 비식별화된 이미지를 클라우드로 푸시하는 하이브리드 아키텍처로 유도되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 보험 상환의 확대가 정량적 화상 진단의 가치를 검증

- 차세대 스펙트럼 이미징을 가능하게 하는 광자 계수 CT

- 헬스케어 IT의 인력 부족이 채용 억제

부문 분석

소프트웨어 솔루션은 세분화, 관류 매핑 및 구조화된 리포팅을 자동화하는 AI 애널리틱스의 채택이 가속화됨에 따라 2024년 전체 수익의 45.67%를 차지했고, 고급 비주얼리제이션 규모의 약 19억 달러에 해당합니다. 구독 기반 업그레이드는 지속적인 알고리즘 업데이트를 제공하고 95% 이상의 연속률을 강화합니다. 광자 계수 CT와 3 테슬라 MR 시스템은 특수 GPU와 검출기 어레이가 필요하기 때문에 하드웨어 판매는 여전히 큽니다. 서비스는 공급업체가 사후 처리, 사이버 보안 및 운영 보증을 관리 서비스 계약에 위탁했기 때문에 13.12%의 성장 전망으로 다른 모든 범주를 초과했습니다.

보다 광범위한 첨단 시각화 산업은 바쁜 응급 부문 전반에 걸쳐 씬 클라이언트 액세스를 가능하게 하는 클라우드 오케스트레이션을 채택하여 설치 주기를 수개월에서 수주로 단축하고 있습니다. 현재 공급업체의 로드맵은 타사 AI 개발자가 워크플로를 중단하지 않고 새로운 알고리즘을 플러그인할 수 있도록 API가 풍부한 플랫폼을 선호하며 이전 하드웨어 구매 수익률을 높이고 있습니다. 종양학 및 순환기학 프로그램이 전용 AI 번들을 전개함에 따라 소프트웨어 청구는 공급업체의 수익을 임상량과 일치시키는 검사 기반 가격으로 전환하고 있습니다.

헬스케어 네트워크는 방사선과, 순환기과, 디지털 병리까지 다루는 단일 작업 목록, 단일 뷰어 구현을 선호하기 때문에 엔터프라이즈 플랫폼은 2024년에 54.12%의 점유율을 획득했습니다. 여러 병원으로 구성된 구매 그룹이 벤더 중립 아이 부카이브와 제로 풋 프린트 뷰어를 규정하고 표준의 조화를 도모하고 있기 때문입니다. 그럼에도 불구하고 독립형 AI 애플리케이션은 대규모 제품군이 천천히 통합되는 척추 골절 검출과 같은 충족되지 않은 마이크로워크플로우를 타겟팅함으로써 12.30%의 연평균 복합 성장률(CAGR)을 기록합니다.

기업용 판매에서는 광자 카운트 CT 라이선스, 종양학 자동 윤곽 그리기, 클라우드 재해 복구가 7년간의 옥스 계약에 번들되는 경우가 많아 스위칭 비용이 증가하고 브랜드 로열티가 정착합니다. 틈새 개발자에게는 주요 플랫폼에 내장된 마켓플레이스 앱 스토어를 통한 판매로 현장 판매에 막대한 비용을 들이지 않고 시장을 개척할 수 있어 중소기업에서도 대응할 수 있는 첨단 시각화 시장을 확대할 수 있습니다.

지역별 분석

북미는 2024년에 43.14%의 매출을 차지하였고, 밀도 높은 모달리티 설치 기반, 가장 빠른 AI 510(k)의 클리어런스, 관상동맥 CTA를 1검사당 357.13달러로 상환하는 CMS의 지불 개혁에 지지되었습니다. GE 헬스케어와 엔비디아의 자율 스캔으로 대표되는 산학 연계는 나중에 세계에 전개되는 알고리즘의 인큐베이션을 계속하고 있습니다. 인력 부족이 계속되고 있기 때문에 방사선 기사 그룹이 수요 증가에 대응하려고 생산성 소프트웨어에 추풍이 불고 있습니다.

아시아태평양은 일본, 호주, 한국이 광자 계수형 CT로 업그레이드하는 한편 인도와 같은 인구가 많은 국가가 제3차 수준의 진단을 Tier-II 도시로 확대하기 위해 저렴한 클라우드 PACS를 도입하기 때문에 CAGR이 13.54%로 가장 급상승할 전망입니다. GE Healthcare에 의한 일본 메지피직스 인수는 시각화 플랫폼을 보완하는 분자 이미징 공급망에 대한 지역적 관심을 강조하고 있습니다. 싱가포르와 한국의 국가 AI 거버넌스 프레임워크는 규제 경로를 간소화하여 현지 신흥 기업이 국제 장비 생태계에 통합하도록 촉구합니다.

유럽은 복잡한 GDPR(EU 개인정보보호규정) 대응 중에서 완만한 이익을 계상하고 있습니다. EU 역내의 암호화 키 거주를 보증할 수 있는 벤더가 경쟁 우위에 놓여있습니다. Philips의 HealthSuite Imaging의 소블린 클라우드 인스턴스에서의 배포는 규제 준수와 혁신이 어떻게 공존할 수 있는지 보여줍니다. 게다가 사이버 보안에 대한 경계감 증가는 레거시 PACS를 제로 트러스트의 벤더 중립 아카이브로 대체하는 것에 박차를 가해 첨단 시각화 시장의 수익을 증가시킵니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI에 의한 자동 세분화으로 읽기 시간을 40% 이상 단축

- 기업용 PACS/VNA 생태계에 AV 통합

- 정량 화상 CPT 코드의 상환 확대

- 벤더 중립적인 클라우드 플랫폼이 다시설 연계 실현(언더 레이더)

- 포톤 카운팅 CT와 스펙트럼 MRI가 4D 시각화 수요 촉진(언더 레이더)

- 인터벤셔널 스위트에서의 스캐너 내 의사 결정 지원(언더 레이더)

- 시장 성장 억제요인

- 미국과 일본 이외에서는 상환 불안정

- EU의 데이터 프라이버시 규제가 클라우드 전개 지연

- 병원에서의 화상 처리 IT 스탭의 부족(언더 레이더)

- GPU 공급망의 불안정성이 벤더의 TCO 상승시킴(언더 레이더)

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 제품 및 서비스별

- 하드웨어

- 소프트웨어

- 서비스

- 솔루션 유형별

- 엔터프라이즈 플랫폼

- 독립형 도구

- 전개 모델별

- 온프레미스

- 클라우드 기반

- 하이브리드

- 화상 모달리티별

- 자기 공명 영상법(MRI)

- 컴퓨터 단층 촬영(CT)

- 초음파

- 핵의학(PET/SPECT)

- 새로운 모달리티(포톤 카운팅 CT, 광음향법)

- 임상 용도별

- 종양학

- 심장혈관

- 신경학

- 정형외과 및 근골격

- 소화기 및 간장

- 최종 사용자별

- 병원

- 화상 진단센터

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Agfa-Gevaert Group

- Canon Inc.(Canon Medical Systems)

- Carestream Health

- Fujifilm Holdings Corporation

- GE HealthCare Technologies Inc.

- Koninklijke Philips NV

- Siemens Healthineers AG

- Sectra AB

- Pro Medicus Ltd(Visage Imaging)

- Terarecon Inc.

- Intelerad Medical Systems

- Vital Images(Canon Group)

- Merative(ex-IBM Watson Health)

- Rad AI

- Blackford Analysis

- Circle Cardiovascular Imaging

- Coreline Soft

- VoxelCloud

제7장 시장 기회 및 전망

AJY 25.10.27The advanced visualization market reached USD 4.20 billion in 2025 and is forecast to climb to USD 7.18 billion by 2030, reflecting an 11.3% CAGR.

Strong demand for AI-powered imaging software, photon-counting CT scanners and cloud-enabled enterprise platforms continues to accelerate capital spending among hospitals and diagnostic centers. In clinical practice, AI auto-segmentation cuts radiology reading time by over 40%, photon-counting CT delivers sub-0.2 mm resolution at lower dose, and new CPT codes for quantitative brain and cardiovascular imaging are unlocking fresh reimbursement streams. Large-scale enterprise PACS/VNA rollouts are fostering multi-site collaboration, while secure-cloud deployments gain traction despite strict data-sovereignty rules in Europe. Competitive intensity is rising as device manufacturers pair with GPU vendors to embed real-time AI into scanners, and service contracts shift revenue away from one-off system sales toward recurring, subscription-based models.

Global Advanced Visualization Market Trends and Insights

AI-Powered Auto-Segmentation Transforms Diagnostic Efficiency

Federal clearance of more than 1,000 clinical AI applications-77% for radiology-has legitimized workflow automation, enabling platforms like Canon Medical INSTINX to remove 40% of cardiac-CT workflow clicks and Philips SmartSpeed Precise to finish MRI scans three-times faster with 80% sharper images. These productivity gains help offset a radiologist vacancy rate of 18.1% that professional bodies project will persist well beyond 2030. In interventional suites, real-time segmentation now guides carotid stenting with 94% recall accuracy, broadening AI value from diagnostics into therapy planning.

Enterprise PACS Integration Drives Operational Consolidation

Record order bookings above SEK 4 billion for Sectra's cloud enterprise imaging suite underscore health-system appetite for unified architectures that eradicate data silos and standardize workflow across radiology, cardiology and pathology departments. Cloud-native PACS rollouts such as PACSonWEB have lifted cross-hospital referrals by 10% within 12 months because physicians can view images anywhere, anytime. Subscription pricing is overtaking perpetual licenses, lowering capital outlays and aligning vendor incentives with uptime and cybersecurity performance guarantees.

Data-Privacy Regulations Create Cloud Barriers

GDPR clauses that tie encryption-key sovereignty to national boundaries force cloud PACS vendors to deploy elaborate key-management infrastructure, elevating deployment cost and lengthening sales cycles in Europe. Cyber incidents targeting radiology grew 67% in 2024, intensifying buyer scrutiny over public-cloud risk profiles and nudging hospitals toward hybrid architectures that keep patient identifiers on-premise while pushing de-identified images into the cloud for AI inference .

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Expansion Validates Quantitative Imaging Value

- Photon-Counting CT Enables Next-Generation Spectral Imaging

- Healthcare IT Staffing Shortages Constrain Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions contributed 45.67% to overall 2024 revenue, equivalent to roughly USD 1.9 billion of advanced visualization market size, due to accelerating adoption of AI analytics that automate segmentation, perfusion mapping and structured reporting. Subscription-based upgrades deliver continuous algorithm refreshes, cementing retention rates above 95%. Hardware revenues remain sizable because photon-counting CT and 3-Tesla MR systems require specialized GPUs and detector arrays, yet the value narrative is shifting toward software-defined imaging where clinical improvements come through code instead of tubes and gantries. Services out-paced every other category with a 13.12% growth outlook as providers outsource post-processing, cybersecurity and uptime guarantees to managed-service contracts.

The broader advanced visualization industry is embracing cloud orchestration that allows thin-client access across busy emergency departments, collapsing installation cycles from months to weeks. Vendor roadmaps now prioritize API-rich platforms so third-party AI developers can plug-in novel algorithms without disrupting workflow, enhancing return on earlier hardware purchases. As oncology and cardiology programs roll out dedicated AI bundles, software billing is moving to exam-based pricing that aligns vendor revenue with clinical volume.

Enterprise platforms captured 54.12% share in 2024 as health networks favor single worklist, single viewer implementations that cover radiology, cardiology and even digital pathology. These integrated hubs are poised to keep expanding because multi-hospital purchasing groups stipulate vendor-neutral archives and zero-footprint viewers to harmonize standards. Standalone AI applications nevertheless post a 12.30% CAGR by targeting unmet micro-workflows-such as spine fracture detection-that large suites integrate only slowly.

An enterprise sale often bundles photon-counting CT licenses, oncology auto-contouring and cloud disaster-recovery into a seven-year opex contract, increasing switching costs and entrenching brand loyalty. For niche developers, distribution through marketplace app-stores embedded in leading platforms offers reach without heavy field-sales overheads, broadening the advanced visualization market addressable by smaller firms.

The Advanced Visualization Market Report Segments the Industry Into by Product and Service (Hardware, and More), by Solution Type (Enterprise Platform, Standalone Tool), by Deployment Model (On-Premise, and More), Imaging Modality ((MRI), (CT), and More), by Clinical Application (Oncology, Cardiovascular, and More), End User (Hospitals, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 43.14% revenue in 2024, underpinned by dense modality install bases, earliest AI 510(k) clearances and CMS payment reforms that now reimburse coronary CTA at USD 357.13 per exam. Academic-industry partnerships-exemplified by GE HealthCare and NVIDIA's work on autonomous scanning-continue to incubate algorithms later deployed worldwide. Ongoing staff shortages create tailwinds for productivity software as radiology groups seek to meet rising demand.

Asia-Pacific registers the steepest 13.54% CAGR as Japan, Australia and South Korea upgrade to photon-counting CT while populous countries such as India deploy affordable cloud PACS to extend tertiary-level diagnostics into tier-II cities. GE HealthCare's acquisition of Nihon Medi-Physics underscores regional interest in molecular imaging supply chains that complement visualization platforms. National AI governance frameworks in Singapore and South Korea streamline regulatory paths, encouraging local startups to integrate into international device ecosystems.

Europe posts moderate gains amid complex GDPR compliance. Vendors able to guarantee encryption-key residency within EU borders gain competitive advantage. Philips' rollout of HealthSuite Imaging on sovereign-cloud instances demonstrates how regulatory adherence and innovation can coexist. Furthermore, heightened cybersecurity vigilance spurs replacement of legacy PACS with zero-trust, vendor-neutral archives-driving incremental advanced visualization market revenues.

- Agfa-Gevaert

- Canon Inc. (Canon Medical Systems)

- Carestream Health

- FUJIFILM

- GE HealthCare Technologies Inc.

- Koninklijke Philips

- Siemens Healthineers

- Sectra

- Pro Medicus Ltd (Visage Imaging)

- Terarecon

- Intelerad Medical Systems

- Vital Images (Canon Group)

- Merative (ex-IBM Watson Health)

- Rad AI

- Blackford Analysis

- Circle Cardiovascular Imaging

- Coreline Soft

- VoxelCloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-powered auto-segmentation cuts reading time by >40%

- 4.2.2 Integration of AV into enterprise PACS/VNA ecosystems

- 4.2.3 Reimbursement expansion for quantitative imaging CPT codes

- 4.2.4 Vendor-neutral cloud platforms enable multi-site collaboration (under-radar)

- 4.2.5 Photon-counting CT & spectral MRI drive 4-D visualisation demand (under-radar)

- 4.2.6 In-scanner decision-support for interventional suites (under-radar)

- 4.3 Market Restraints

- 4.3.1 Patchy reimbursement outside US & Japan

- 4.3.2 Data-privacy rules slowing cloud roll-outs in EU

- 4.3.3 Ongoing shortage of imaging IT staff at hospitals (under-radar)

- 4.3.4 GPU supply-chain volatility raises TCO for vendors (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Product & Service

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Solution Type

- 5.2.1 Enterprise Platform

- 5.2.2 Standalone Tool

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.3.3 Hybrid

- 5.4 By Imaging Modality

- 5.4.1 Magnetic Resonance Imaging (MRI)

- 5.4.2 Computed Tomography (CT)

- 5.4.3 Ultrasound

- 5.4.4 Nuclear Medicine (PET/SPECT)

- 5.4.5 Emerging Modalities (Photon-Counting CT, Photoacoustic)

- 5.5 By Clinical Application

- 5.5.1 Oncology

- 5.5.2 Cardiovascular

- 5.5.3 Neurology

- 5.5.4 Orthopedics & Musculoskeletal

- 5.5.5 Gastro-Hepatology

- 5.6 By End User

- 5.6.1 Hospitals

- 5.6.2 Diagnostic Imaging Centers

- 5.6.3 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agfa-Gevaert Group

- 6.3.2 Canon Inc. (Canon Medical Systems)

- 6.3.3 Carestream Health

- 6.3.4 Fujifilm Holdings Corporation

- 6.3.5 GE HealthCare Technologies Inc.

- 6.3.6 Koninklijke Philips N.V.

- 6.3.7 Siemens Healthineers AG

- 6.3.8 Sectra AB

- 6.3.9 Pro Medicus Ltd (Visage Imaging)

- 6.3.10 Terarecon Inc.

- 6.3.11 Intelerad Medical Systems

- 6.3.12 Vital Images (Canon Group)

- 6.3.13 Merative (ex-IBM Watson Health)

- 6.3.14 Rad AI

- 6.3.15 Blackford Analysis

- 6.3.16 Circle Cardiovascular Imaging

- 6.3.17 Coreline Soft

- 6.3.18 VoxelCloud

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment