|

시장보고서

상품코드

1836670

정형외과용 전동 공구 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Orthopedic Power Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

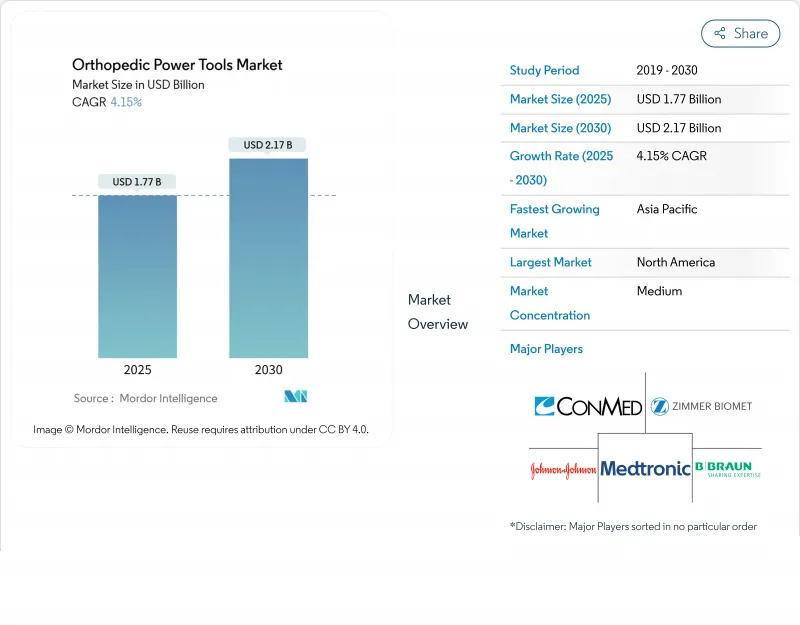

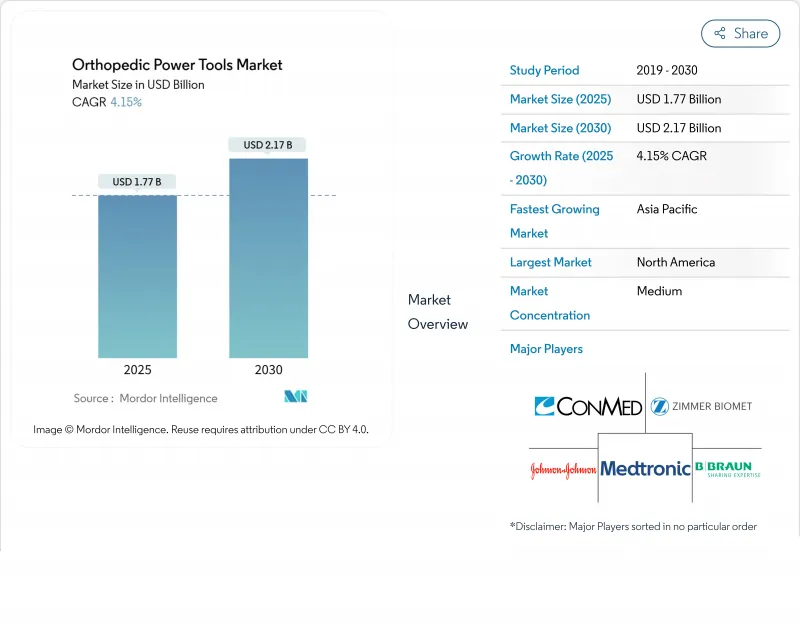

정형외과용 전동 공구 시장 규모는 2025년에 17억 7,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 4.15%로 성장할 전망이며, 2030년에는 21억 7,000만 달러에 달할 것으로 예측됩니다.

성장을 뒷받침하는 것은 수술 효율을 향상시키는 배터리 구동 플랫폼으로의 꾸준한 이동과 함께 근골격계 질환의 부담이 크게 증가하고 있다는 것입니다. 북미는 수술 건수와 디지털 수술실 기술의 급속한 보급을 배경으로 주도권을 유지하고 있지만, 아시아태평양은 고령화 사회에 대응하기 위한 의료 인프라 규모의 확대에 따라 가장 급속히 진보하고 있습니다. 외래수술센터(ASC)에서는 단기간 정형외과 수술에 적합한 컴팩트한 무선 장치가 선호되고 있으며 수요가 더욱 높아지고 있습니다. 경쟁은 핸드피스를 로봇 공학과 네비게이션에 맞추는 지속적인 업그레이드에 집중하고 있지만, 고액의 자본 지출 및 멸균 검증 비용이 예산을 압박하기 때문에 구매를 주저하는 경향이 계속되고 있습니다.

세계의 정형외과용 전동 공구 시장 동향 및 인사이트

세계의 근골격계 질환 부담으로 수술 건수 증가

골관절염과 외상의 유병률이 증가함에 따라 인공 관절 치환술 후보자의 대응 가능한 풀이 확산되고 있습니다. 연간 인공 고관절 치환술과 인공 슬관절 치환술의 건수는 2050년까지 225만 건에 달할 것으로 예측되고 있으며, 외과의사는 이 페이스에 늦지 않도록 증례 수를 배증시켜야 합니다. 정형외과용 전동 공구 시장 수요가 높아지는 것은 모든 인공 관절 치환술에 전동 톱과 전동 드릴이 불가결하기 때문입니다. 이 동향은 특히 미국에서 두드러집니다. 미국에서 절차의 처리 능력은 광범위한 보험 상환의 적용과 회복 강화 경로의 광범위한 채용에 의해 지원됩니다. 서유럽에서도 임상 지침이 선택적 관절 재건술의 연령 기준을 낮추고 있기 때문에 비슷한 기운이 높아지고 있습니다.

외래 및 데이 케이스 정형외과가 컴팩트 도구 수요 견인

ASC로 환자 수를 이동하면 방을 빠르게 회전시킬 수 있는 가볍고 무선 기구에 대한 새로운 요구를 끌어냅니다. 메디케어는 현재 ASC에서 어깨 관절 전치환술에 보험 적용하고 있으며, 같은 날 퇴원의 비즈니스 케이스를 강화하고 있습니다. 비용 벤치마크에 따르면 ASC의 총 에피소드 비용은 병원의 외래 부문에 비해 35% 낮고, 지불자나 외과의사에게 인센티브를 주고 있습니다. 정형외과용 전동 공구 시장은 중앙 송기 라인에 의존하지 않는 배터리 시스템의 판매 증가로 이익을 얻고 있습니다. 공구 제조업체는 설치 및 멸균 사이클을 몇 분 단축하기 위해 AI 대응 사례 관리를 통해 제안을 강화하고 있습니다.

수작업 대체에 비해 높은 자본 비용 및 서비스 비용

프리미엄 전기 세트 및 배터리 세트의 구입 가격은 특히 저소득 지역의 소규모 시설 예산에 엄격합니다. 연간 유지보수 비용은 초기 비용의 15-20%로 라이프사이클을 압박합니다. 따라서 정형외과용 전동 공구 시장은 교체 사이클의 장기화에 직면하고 있으며, 구매자는 투자 회수 시간과 급속한 기능의 진부화를 저울질하고 있습니다. 척추진료소를 대상으로 한 조사에 따르면 77%가 전동 보조 기구나 로봇 보조 기구를 도입할 때의 주요 장벽으로 구입 비용을 꼽고 있습니다. 임대 및 클릭당 사용료와 같은 새로운 자금 조달 모델은 스티커 충격을 완화하려는 시도이지만, 이제 막 시작되었습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 로보틱스+네비게이션의 융합이 동력 공구의 업그레이드 가속

- 세계적인 고령화 인구 증가

- 엄격한 멸균 및 재처리 검증 요건

부문 분석

2024년 정형외과용 전동 공구 시장의 31.7%를 대골용 기구가 차지하였고, 고관절 성형술과 무릎 관절 성형술 수요에 지지되고 있습니다. 그러나 저침습성 감압술과 관절경 기술은 미세하고 균형 잡힌 고 RPM 핸드 피스를 사용하므로 고속 장비는 CAGR 5.8%로 가장 빨리 기록됩니다. 스포츠 부상의 재건이 증가하고 있으며 열괴사를 일으키지 않고 뼈를 제거할 수 있는 발리가 선호되기 때문에 수익 가속이 강화되고 있습니다. 제조업체는 피질골의 무결성을 보호하기 위해 분당 회전 수를 자동으로 조정하는 토크 피드백 센서를 내장하고 있습니다.

섬세한 손과 발을 치료하는 외과의사는 낮은 진동으로 미세 토크를 제공하는 작은 뼈 드릴에 계속 의존하고 있습니다. 정형외과용 전동 공구 시장은 외래 환자 센터가 매일 여러 증례를 예정하고 있기 때문에 안정적인 수량이 되고 있습니다. 또한 인공 고관절 치환술에서는 반드시 골수 형성이 필요하기 때문에 정형외과용 리머도 큰 매출을 올리고 있습니다. 제품 설계는 수내압을 줄이는 칩 배출 플루트를 선호하므로 대퇴골 압입시 지방 색전증의 위험이 감소합니다.

배터리 플랫폼은 2024년 정형외과용 전동 공구 시장 점유율의 40.4%를 차지하였고, 2025-2030년 CAGR 4.8%로 최대의 성장 엔진으로 지속될 것으로 예측되고 있습니다. 호스에서 해제하면 방 레이아웃이 간소화되고 설치 시간이 몇 분 단축됩니다. 현재의 리튬 이온 팩은 일일 사례 목록을 지원하고 새로운 무선 충전 트레이는 무균 상태를 깨지 않고 처리 중에 배터리 잔량을 유지합니다.

전동식 코드가 장착된 유닛은 흔들리지 않는 파워가 중요한 3시간을 초과할 수도 있는 복잡한 재수술에서 여전히 확고한 틈새를 차지하고 있습니다. 한때 주류였던 공압식 모델은 공기 인프라가 감소하고 병원이 소음 감소의 의무화를 목표로 하고 있기 때문에 현재는 축소되고 있습니다. 하이브리드 모듈형 시스템은 중복성을 강조하는 고급 급성기 센터에서 채택되어 라인 전압이 변할 때 전원 간 전환을 가능하게 합니다. 팩의 에너지 밀도의 지속적인 향상은 2030년까지 정형외과용 전동 공구 시장을 이끌어내는 매우 중요한 주제입니다.

정형외과용 전동 공구 시장 보고서는 업계를 유형별(대골용 전동 공구, 기타), 기술별(전동 시스템, 기타), 사용 형태별(재사용 시스템, 일회용 시스템), 최종 사용자별(병원, 기타), 지역별(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미)로 분류하고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 정형외과용 전동 공구 시장 매출의 53.1%를 차지했으며, 임플란트 건수가 많아 디지털 수술실의 조기 전개에 지지를 받았습니다. 미국의 무릎 관절 수술 건수는 79만 건, 고관절 수술 건수는 54만 4,000건으로 안정된 기준선 수요를 뒷받침하고 있습니다. 장비 패스스루 지불 확대 2025년 CMS ASC 최종 규정을 포함한 호의적인 상환은 프리미엄 배터리 드릴로의 섭취를 더욱 향상시킵니다.

유럽은 국민 모두 보험제도와 엄격한 의료기기 안전기준에 지지되어 높은 점유율을 유지하고 있습니다. 정책 입안자는 녹색 조달을 중시하고 라이프사이클 평가에서 일회용 포장보다 85% 저탄소 발자국을 보여주는 재사용 가능한 케이싱 시스템에 구매자를 유도하고 있습니다. 서유럽 정형외과용 전동 공구 시장도 재치환율을 추적하는 관절 등록의 혜택을 받고 있어 병원을 얼라인먼트 에러를 최소화하는 네비게이션과 조합한 정밀기계로 유도하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 6.7%로 가장 급성장하고 있는 지역입니다. 일본의 초고령화 사회가 치료 건수를 밀어 올리는 한편, 중국의 2급 도시에서는 도시 생활과 함께 근골격계 장애가 증가하기 때문에 치료 건수가 증가합니다. 배터리 채용은 대도시 병원에서 기세를 늘리고 있습니다. 대조적으로, 공압식의 보급률은 자본 예산이 여전히 엄격한 2차 시설에서 멈추고 있습니다. 정형외과용 전동 공구 시장은 인도와 동남아시아에서도 기회를 포착하고 있으며, 거기서는 민간 정형외과 체인이 북미의 진료에 뒤따른 ASC 모델에 투자하고 있습니다.

중동 및 아프리카에서는 걸프 국가들이 새로운 의료 도시 내에서 수술실의 현대화를 추진하고 있습니다. 정부로부터의 자금 지원에 의해 대규모 입찰이 행해져, 애프터 서비스가 충실하고 있는 벤더가 유리하게 됩니다. 남미에서는 공공 보험 회사가 외상 치료 예산을 확대하고 있으며 현지 조립 파트너십을 통해 수입 관세를 상쇄하고 배터리 플랫폼 가격 경쟁을 개선할 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 근골격계 질환에 의한 수술 건수 증가

- 외래 및 당일 정형외과 수술이 소형 수술 기구 수요 촉진

- 로봇+네비게이션의 융합이 파워 툴의 업그레이드 가속

- 세계의 고령화 인구 증가

- SSI를 억제하기 위한 멸균된 핸드피스의 일회용 지향

- 전동 자전거 및 도로 교통에 의한 대골 외상 건수 급증

- 시장 성장 억제요인

- 수동 대체품에 비해 높은 자본 비용 및 서비스 비용

- 엄격한 멸균 및 재처리 밸리데이션 요건

- 리튬 이온 배터리 폐기 규제에 의한 라이프사이클 비용 상승

- 인가를 지연시키는 재처리 검증 기준

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 기기 유형별

- 대골용 전동 공구

- 소골용 전동 공구

- 고속 전동 공구

- 정형외과용 리머

- 수술용 드릴

- 외과용 톱

- 액세서리(블레이드, 버즈, 배터리)

- 기술별

- 전동 시스템

- 배터리 구동 시스템

- 공압식 시스템

- 하이브리드 모듈 시스템

- 사용 형태별

- 재사용 가능 시스템

- 일회용 시스템

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 정형외과 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Stryker Corporation

- Johnson & Johnson(DePuy Synthes)

- Zimmer Biomet

- Medtronic

- Commed Corporation

- B. Braun Melsungen AG

- Arthrex Inc.

- Smith & Nephew plc

- De Soutter Medical Ltd.

- MicroAire Surgical Instruments

- Ortho Life Systems Pvt. Ltd.

- Brasseler USA

- NSK Nakanishi Inc.

- Acumed LLC(OsteoMed)

- Adeor Medical AG

- Peter Brehm GmbH

- Medicon eG

- Shanghai Bojin Medical

- IndoSurgicals Private Limited

- Zimmer Surgical(Exactech)

제7장 시장 기회 및 전망

AJY 25.10.27The Orthopedic Power Tools Market size is estimated at USD 1.77 billion in 2025, and is expected to reach USD 2.17 billion by 2030, at a CAGR of 4.15% during the forecast period (2025-2030).

Growth is propelled by a significant and rising musculoskeletal disease burden alongside the steady shift toward battery-powered platforms that improve surgical efficiency. North America keeps its leadership on the back of high procedure volumes and rapid uptake of digital operating-room technologies, while Asia-Pacific is advancing fastest as health-care infrastructure scales to meet an aging population. Demand is further lifted by ambulatory surgical centers (ASCs) that favor compact, cordless devices tailored for short-stay orthopedic interventions. Competitive intensity centers on continuous upgrades that align handpieces with robotics and navigation, yet purchasing hesitancy persists where high capital outlays and sterilization validation costs strain budgets.

Global Orthopedic Power Tools Market Trends and Insights

Global Musculoskeletal Disease Burden Elevating Surgical Volumes

Growing prevalence of osteoarthritis and trauma injuries is widening the addressable pool of joint replacement candidates. Annual hip and knee arthroplasty volumes are projected to reach 2.25 million by 2050, requiring surgeons to double caseload capacity to keep pace. The orthopedic power tools market demand intensifies because powered saws and drills are indispensable for every replacement procedure. The trend is particularly visible in the United States, where procedure throughput is supported by expansive reimbursement coverage and widespread adoption of enhanced-recovery pathways. Similar momentum is building in Western Europe as clinical guidelines lower age thresholds for elective joint reconstruction.

Ambulatory & Day-Case Orthopedics Driving Compact Tool Demand

Shifting volumes toward ASCs unlocks fresh requirements for lightweight, cordless instruments that can turn over rooms quickly. Medicare now reimburses total shoulder arthroplasty in ASCs, reinforcing the business case for same-day discharge. Cost benchmarking shows 35% lower total episode spend in ASCs compared with hospital outpatient departments, incentivizing payers and surgeons alike. The Orthopedic power tools market benefits through heightened sales of battery systems that do not rely on central air lines. Device makers are augmenting propositions with AI-enabled case management to shave minutes off setup and sterilization cycles.

High Capital & Service Costs Versus Manual Alternatives

Premium electric and battery sets carry acquisition prices that can challenge budgets of smaller facilities, especially in lower-income regions. Annual maintenance outlays run 15-20% of initial spend, adding life-cycle pressure. The orthopedic power tools market therefore faces elongated replacement cycles where buyers weigh payback time against rapid feature obsolescence. Surveys of spine practices indicate 77% cite purchase expense as the leading barrier to adopting powered or robotic adjuncts. Emerging financing models such as leasing and per-click usage fees attempt to mitigate sticker shock yet remain nascent.

Other drivers and restraints analyzed in the detailed report include:

- Robotics + Navigation Convergence Accelerating Power-Tool Upgrades

- Rise in Aging Population Across the World

- Stringent Sterilization / Reprocessing Validation Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large-bone instruments accounted for 31.7% of the orthopedic power tools market in 2024, supported by hip and knee arthroplasty demand. High-speed devices, however, register the quickest 5.8% CAGR because minimally invasive decompressions and arthroscopic techniques rely on finely balanced, high-RPM handpieces. Revenue acceleration is reinforced by rising sports injury reconstructions that favor burrs capable of bone removal without thermal necrosis. Manufacturers embed torque-feedback sensors that auto-adjust revolutions per minute to safeguard cortical bone integrity.

Surgeons performing delicate hand and foot repairs continue to rely on small-bone drills that deliver micro-torque at low vibration. The orthopedic power tools market sees stable volumes here as outpatient centers schedule multiple cases daily. Orthopedic reamers also contribute sizable sales because every hip replacement demands medullary preparation. Product design prioritizes chip-evacuation flutes that reduce intramedullary pressure, thereby lowering fat embolism risk during press-fit femoral implantations.

Battery platforms held 40.4% orthopedic power tools market share in 2024 and are projected to remain the largest growth engine with 4.8% CAGR from 2025-2030. Freedom from hoses simplifies room layout and shortens setup time by several minutes, a meaningful efficiency in high-throughput ASCs. Current lithium-ion packs support full-day case lists, and new wireless charging trays keep batteries topped between procedures without breaking sterility.

Electric corded units still occupy a firm niche in complex revision surgeries that can exceed three hours, where unwavering power is critical. Pneumatic models, once dominant, now contract as air infrastructure dwindles and hospitals target noise reduction mandates. Hybrid modular systems appear in high-acuity centers that value redundancy, allowing transition between power sources if line voltage fluctuates. Continuous improvement in pack energy density is a pivotal theme guiding the Orthopedic power tools market through 2030.

The Orthopedic Power Tools Market Report Segments the Industry Into by Type (Large-Bone Power Tools, and More), Technology (Electric-Powered Systems, and More), Usage Modality (Reusable Systems, and Single-Use / Disposable Systems), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 53.1% of the orthopedic power tools market revenue in 2024, anchored by high implant volumes and early rollouts of digital operating rooms. United States procedural counts of 790,000 knees and 544,000 hips underscore a stable baseline demand. Favorable reimbursement, including the 2025 CMS ASC final rule that broadens device pass-through payments, further sustains uptake of premium battery drills.

Europe follows with a strong share supported by universal health coverage and rigorous device safety standards. Policy makers emphasize green procurement, steering buyers toward reusable casing systems whose life-cycle assessments show 85% lower carbon footprints than disposable packaging. The Orthopedic power tools market in Western Europe also benefits from joint registries that track revision rates, nudging hospitals toward precision machines paired with navigation to minimize alignment errors.

Asia-Pacific stands out as the fastest-growing region at 6.7% CAGR through 2030. Japan's super-aged society drives volume, while China's tier-2 cities add capacity as musculoskeletal disorders rise with urban living. Battery adoption gains momentum in metropolitan hospitals; in contrast, pneumatic prevalence stays high in secondary facilities where capital budgets remain tight. The Orthopedic power tools market also captures opportunity in India and Southeast Asia, where private orthopedic chains invest in ASC models patterned on North American practices.

A smaller yet strategic opportunity exists in the Middle East & Africa, where Gulf states modernize surgical suites within new medical cities. Governmental funding drives large bulk tenders that favor vendors offering robust after-sales service. South America sees incremental gains as public insurers stretch budgets for trauma care; local assembly partnerships can offset import tariffs, improving price competitiveness for battery platforms.

- Stryker

- Johnson & Johnson

- Zimmer Biomet

- Medtronic

- Conmed

- B. Braun

- Arthrex

- Smiths Group

- De Soutter Medical Ltd.

- MicroAire

- Ortho Life Systems Pvt. Ltd.

- Brasseler USA

- NSK Nakanishi Inc.

- Acumed LLC (OsteoMed)

- Adeor Medical

- Peter Brehm GmbH

- Medicon eG

- Shanghai Bojin Medical

- IndoSurgicals Private Limited

- Zimmer Surgical (Exactech)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global Musculoskeletal Disease Burden Elevating Surgical Volumes

- 4.2.2 Ambulatory and Day-Case Orthopedics Driving Compact Tool Demand

- 4.2.3 Robotics + Navigation Convergence Accelerating Power-Tool Upgrades

- 4.2.4 Rise in Aging Population Across the World

- 4.2.5 Preference for Single-Use Sterile Handpieces to Curb SSIs

- 4.2.6 E-Bike & Road-Traffic Trauma Surge Boosting Large-Bone Volumes

- 4.3 Market Restraints

- 4.3.1 High Capital & Service Costs Versus Manual Alternatives

- 4.3.2 Stringent Sterilization/Reprocessing Validation Requirements

- 4.3.3 Lithium-Ion Battery Disposal Regulations Raising Lifecycle Costs

- 4.3.4 Reprocessing Validation Standards Slowing Approvals

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Device Type

- 5.1.1 Large-Bone Power Tools

- 5.1.2 Small-Bone Power Tools

- 5.1.3 High-Speed Power Tools

- 5.1.4 Orthopedic Reamers

- 5.1.5 Surgical Drills

- 5.1.6 Surgical Saws

- 5.1.7 Accessories (Blades, Burs, Batteries)

- 5.2 By Technology

- 5.2.1 Electric-Powered Systems

- 5.2.2 Battery-Powered Systems

- 5.2.3 Pneumatic-Powered Systems

- 5.2.4 Hybrid Modular Systems

- 5.3 By Usage Modality

- 5.3.1 Reusable Systems

- 5.3.2 Single-Use / Disposable Systems

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Orthopedic Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Stryker Corporation

- 6.4.2 Johnson & Johnson (DePuy Synthes)

- 6.4.3 Zimmer Biomet

- 6.4.4 Medtronic

- 6.4.5 Conmed Corporation

- 6.4.6 B. Braun Melsungen AG

- 6.4.7 Arthrex Inc.

- 6.4.8 Smith & Nephew plc

- 6.4.9 De Soutter Medical Ltd.

- 6.4.10 MicroAire Surgical Instruments

- 6.4.11 Ortho Life Systems Pvt. Ltd.

- 6.4.12 Brasseler USA

- 6.4.13 NSK Nakanishi Inc.

- 6.4.14 Acumed LLC (OsteoMed)

- 6.4.15 Adeor Medical AG

- 6.4.16 Peter Brehm GmbH

- 6.4.17 Medicon eG

- 6.4.18 Shanghai Bojin Medical

- 6.4.19 IndoSurgicals Private Limited

- 6.4.20 Zimmer Surgical (Exactech)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment