|

시장보고서

상품코드

1836672

어깨 인공관절 치환술 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Shoulder Replacement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

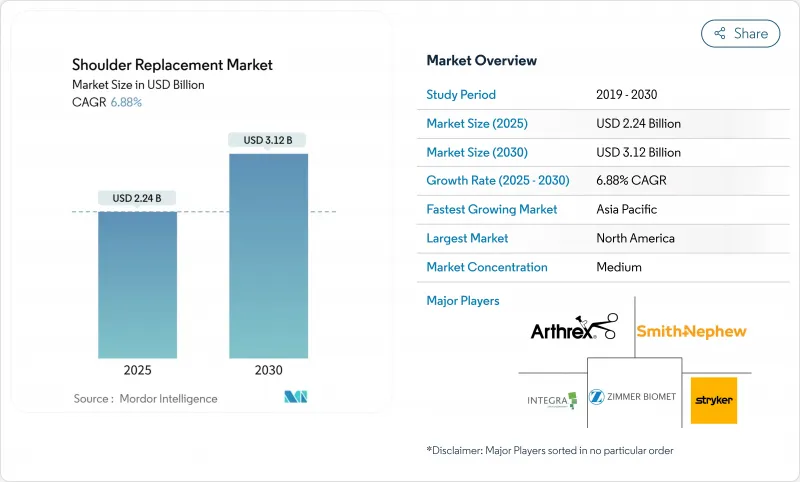

어깨 인공관절 치환술 시장 규모는 2025년에 22억 4,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 6.88%로 성장할 전망이며, 2030년에는 31억 2,000만 달러에 달할 것으로 예측됩니다.

이 확장은 노인층으로의 인구 역학 변화, 관절염 유병률 증가, 임플란트 내구성 및 수술 정확도를 높이는 지속적인 설계 혁신을 반영합니다. 인공지능, 3D 계획 소프트웨어, 로봇 지원 시스템은 현재 외과의사를 실시간으로 유도하고 수술의 편차를 줄이며 회복 시간을 단축하고 있습니다. 또한 외래수술센터(ASC)로의 수술 전환도 성장의 원동력이 되고 있으며, 이로 인해 유리한 상환과 낮은 수술 비용이 지불자의 우선사항과 일치하고 있습니다. 한편, 아시아태평양의 의료 투자는 기술 도입을 가속화하고, 북미의 우위성을 약화시키며, 다국적 기기 제조업체의 경쟁을 재구축하고 있습니다.

세계의 어깨 인공관절 치환술 시장 동향 및 인사이트

관절염의 유병률 증가

관절염은 미국에서만 5,400만 명의 성인이 앓고 있으며, 변형성 상완관절증은 현재 인공관절 치환술의 소개 건수에 차지하는 비율을 증가시키고 있습니다. 힘줄 병변을 가진 환자의 연골 변성이 가속되면 복잡한 역수술로 진행되는 경우가 많아서 대응 가능한 베이스가 넓어지고 있습니다. 고해상도 이미징을 통한 조기 발견은 어린 나이에 수술 적응을 증가시키고 메디케어 적용 확대는 적격 사례에 대한 경제적 장벽을 제거합니다. 생산성 감소, 치료 장기화, 오피오이드 사용과 같은 관리되지 않은 관절통의 경제적 부담은 인공 관절 치환술의 가치 제안을 강화하고 있습니다. 이러한 요인을 종합하면 헬스케어에 대한 액세스가 확립된 지역 전체에서 수기 건수의 꾸준한 성장을 지원하고 있습니다.

인공 관절 디자인의 기술적 진보

스미스 앤 네퓨와 짐머 바이오메트의 스템레스 시스템은 2024년 FDA 승인을 받아 골 스톡을 절약하고 인공 관절 주위 골절 위험을 줄입니다. 또, 파이로카본제의 상완골두는 피질골의 탄성률에 근사하고 있어 코발트 크롬제의 대체품에 비해 관절와의 침식을 경감하고 있습니다. 외과의사는 3D 수술 전 계획과 수술 중 트래커를 결합한 네비게이션 플랫폼을 점점 더 활용할 수 있어 정확한 관절포의 착석을 보장하고 있습니다. 이러한 융합 기술은 임플란트의 긴 수명화를 실현하고 첨단 연구개발에 투자할 준비가 된 공급업체를 차별화합니다.

수술 후 합병증 및 임플란트의 이완

노르웨이의 장기 데이터에서 인공관절 치환술의 합병증 발생률은 14.3%로 불안정성과 감염이 재치환술의 원인이 되었습니다. 관절포의 이완은 2년 이내에 해부학적 사례의 최대 48%에 나타나고 고정 전략에 대한 우려를 야기합니다. 폴리에틸렌 인서트와 결합된 금속 백 구성요소는 재치환술의 위험이 높으며 폴리에틸렌 모노블록 및 하이브리드 디자인으로의 전환을 촉진합니다. 인공관절 치환술 후 5년 사망률은 메디케어 수급자들 사이에서 16.6%에 달하여 합병증이 결과에 큰 영향을 미친다는 것을 상기시킵니다. 지속적인 설계 개선과 엄격한 감염 제어 프로토콜은 여전히 가장 중요합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 확대하는 노년 인구 및 평균 수명

- 외래인공관절 치환술 프로그램 성장

- 높은 수술 비용 및 임플란트 비용

부문 분석

해부학적 인공관절은 2024년 매출의 66.34%를 공급했지만, 리버스 시스템은 CAGR 7.13%로 그 차이를 줄이고 있습니다. 해부학적인 인공 관절은 정상적인 운동학을 모방하고 상완골을 보존하기 때문에 힘줄이 온전한 환자에게 선호됩니다. 스템리스형 임플란트는 루멘 형성의 번거로움을 없애고 미래의 재치환술을 단순화함으로써 수술 시간을 단축할 수 있습니다. 리버스 임플란트는 커프 결손증, 불안정 골절증, 재치환술 사례를 지배하고 있으며 88% 이상의 10년 생존율을 자랑합니다.

디자인의 진화의 중심은 삼각근의 장력을 높이고 움직이는 영역을 확장하는 측방화된 회전 중심과 원위화된 관절포입니다. 인레이 리버스 시스템은 관절포의 노출을 단순화하는 반면, 온레이 플랫폼은 골 결손 사례에 안정성을 증가시킵니다. 모듈형 플랫폼은 해부학적 구성과 리버스 구성 모두에 대응할 수 있게 되어 재고를 추가하지 않고 수술 중 의사 결정을 이동할 수 있습니다. 이러한 진보는 적응증을 확대하고 어깨 인공관절 치환술 시장에서 구성 가능한 솔루션을 제공하는 기업의 경쟁력을 강화하고 있습니다.

어깨 인공관절 치환술은 2024년에 44.39%의 매출을 유지했으며, 수십년에 걸친 치료 성적 데이터와 외과의의 보급에 지지되고 있습니다. 그러나 역치환형 어깨 인공관절 치환술은 복잡한 단열관절증, 골절, 재치환술의 경로를 통해 CAGR 8.20%로 수량 확대를 추진하고 있습니다. 표면 치환형 반관절성형술은 전치환술을 연장할 수 있는 젊은 운동선수의 국소 연골 병변에 여전히 효과적이지만, 반경절 절제술은 역치환 요법이 더 높은 통증 완화와 기능을 보이면서 후퇴하고 있습니다.

역전 치환술로의 흐름은 힘줄 이식을 결합하여 32° 외선을 회복하고 일상 생활 활동을 향상시킬 수 있다는 증거를 반영합니다. 로봇 플랫폼은 해부학적 수술과 리버스 수술 워크플로를 모두 지원하고 계기를 통합하고 학습 곡선을 줄입니다. 외래 환자의 이동은 더 이상 해부학적인 1차 사례에 국한되지 않으며, 신중하게 선택된 역수술이 동등한 안전성 프로파일로 당일 퇴원할 수 있게 되었습니다. 이러한 절차의 다양성은 다양한 임상 적응증에 성장을 분산시킴으로써 어깨 인공관절 치환술 시장에 탄력성을 주입하고 있습니다.

지역별 분석

북미는 2024년 매출액 점유율 39.81%로 우위를 유지했으며, 이는 성숙한 상환 구조와 미국에서만 연간 약 5만 3,000건의 인공관절 치환술에 지지되고 있습니다. CMS가 어깨 인공관절 치환술을 ASC의 대상 목록에 포함시킴으로써 절차의 전환이 촉진되는 반면, 전국적인 관절 등록은 증거 기반 기구 선택을 지원합니다. 캐나다는 극장의 용량을 늘려 대기 수술에 맞서고, 멕시코는 비용 차이를 이용하여 외국인 환자를 유치하고 있습니다.

아시아태평양의 2030년까지 연평균 복합 성장률(CAGR)은 8.47%로 가장 빠른 성장이 전망되며, 병원 인프라 확대, 중간소득층 소득 증가, 저렴한 정형외과 솔루션을 요구하는 정부 정책 등이 그 요인입니다. 중국의 수량 기준 조달은 입원 환자의 비용을 절반으로 줄여 품질을 희생하지 않고 임플란트에 광범위한 접근을 가능하게 합니다. 일본의 초고령화 사회는 엄격한 규제 감독을 실시하면서도 수술 수요를 확대하고 있습니다. 인도의 민간 병원 체인은 의료 관광을 추구하고 하이엔드 임플란트를 수입하는 한편 '메이크인 인디아'의 틀 아래 국내 제조를 추진하고 있습니다. 호주는 임상시험에서 인구비 이상의 성과를 계속 올리고 있으며, 신기술의 조기 채용 기회를 제공합니다.

유럽에서는 관민을 불문하고 꾸준히 도입이 진행되고 있습니다. 독일의 제조 거점은 국내에서 높은 도입률을 뒷받침하고 영국은 브렉짓의 규제 재편에도 불구하고 인공관절 치환술 연구에 고집하고 있습니다. 프랑스와 이탈리아는 재입원을 늘리지 않고 입원 기간을 단축하는 회복 강화 프로토콜을 개선하고 있습니다. 북유럽의 레지스트리는 절차 및 결과의 상관 관계를 밝히는 세밀한 데이터를 제공하고 세계의 진료 패턴을 이끌고 있습니다. 유럽의 의료기기 규제는 승인까지의 기간을 연장하고 있지만, 그 안전성 중시의 자세는 차세대 임플란트에 대한 지역의 신뢰를 높이고 있습니다. 이러한 지역적 패턴을 종합하면 어깨 인공관절 치환술 시장을 고립된 정책 충격으로부터 보호하는 다양한 수익원이 확보됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 관절염의 유병률 증가

- 인공 관절 설계의 기술적 진보

- 노년 인구 및 평균 수명 확대

- 외래인공관절 치환술 프로그램의 성장

- AI를 활용한 환자별 기구의 개발

- 젊은층 수요를 견인하는 스포츠 장애 증가

- 시장 성장 억제요인

- 수술 후 합병증 및 임플란트 이완

- 높은 수술 비용 및 임플란트 비용

- 의료 등급 금속 및 UHMWPE의 불안정한 공급

- 리버스 보철의 승인 사이클의 엄격화

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 제품 유형별

- 해부학적 인공관절

- 스템 첨부 아나토미컬

- 스템리스 아나토미컬

- 리버스형 보철

- 인레이 리버스

- 온레이 리버스

- 스템리스 리버스

- 하이브리드 및 생물학적 인공관절

- 해부학적 인공관절

- 술식별

- 표면 치환 반구개 성형술

- 줄기 반월체 성형술

- 어깨 인공관절 치환술

- 리버스 어깨 인공관절 치환술

- 어깨 관절 부분 치환술

- 고정 방법별

- 시멘트

- 시멘트리스

- 하이브리드

- 최종 사용자별

- 병원

- 정형외과 센터

- 외래수술센터(ASC)

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Arthrex Inc.

- Zimmer Biomet Holdings Inc.

- Integra LifeSciences Holdings Corporation

- Johnson & Johnson(DePuy Synthes)

- Smith & Nephew plc

- Wright Medical Group NV

- Stryker Corporation

- Enovis Corporation(DJO Global)

- Acumed LLC

- Exactech Inc.

- LimaCorporate SpA

- Commed Corporation

- B. Braun Melsungen AG

- Medacta International

- Stryker Corporation

- Apex Biomedical

- Globus Medical Inc.

- FH Orthopedics

- Biotechni SAS

- Ascension Orthopedics

제7장 시장 기회 및 전망

AJY 25.10.27The Shoulder Replacement Market size is estimated at USD 2.24 billion in 2025, and is expected to reach USD 3.12 billion by 2030, at a CAGR of 6.88% during the forecast period (2025-2030).

The expansion reflects demographic shifts toward older age cohorts, rising arthritis prevalence, and continuous design innovation that enhances implant durability and surgical precision. Artificial intelligence, 3D planning software, and robotic-assisted systems now guide surgeons in real time, shrinking operative variability and shortening recovery times. Growth also draws momentum from the migration of procedures to ambulatory surgery centers, where favorable reimbursement and lower operating costs align with payer priorities. Meanwhile, Asia-Pacific healthcare investments accelerate technology adoption, tempering North American dominance and reshaping the competitive calculus for multinational device makers.

Global Shoulder Replacement Market Trends and Insights

Growing Prevalence of Arthritis

Arthritis afflicts 54 million adults in the United States alone, and glenohumeral osteoarthritis now triggers a rising share of anatomic arthroplasty referrals. Accelerated cartilage degeneration in patients with rotator-cuff pathology often progresses to complex reverse procedures, broadening the addressable base. Earlier detection through high-resolution imaging increases surgical candidacy at younger ages, while Medicare coverage expansion removes financial barriers for qualified cases. The economic burden of unmanaged arthritic pain-lost productivity, prolonged therapy, and opioid use-reinforces the value proposition of definitive joint replacement. Collectively, these factors anchor steady procedural volume growth across regions with established healthcare access.

Technological Advances in Prosthesis Design

Stemless systems from Smith + Nephew and Zimmer Biomet, cleared by the FDA in 2024, conserve bone stock and lower periprosthetic fracture risk. Reverse designs now incorporate lateralization and distalization principles that restore deltoid mechanics, and pyrocarbon humeral heads approximate cortical bone modulus, reducing glenoid erosion relative to cobalt-chromium alternatives. Surgeons increasingly rely on navigation platforms that marry 3D preoperative plans with intraoperative trackers to ensure precise glenoid seating. These converging technologies deliver longer implant survival and differentiate suppliers prepared to invest in advanced R&D.

Post-Operative Complications & Implant Loosening

Long-term data from Norway cite 14.3% complication rates for reverse arthroplasty, with instability and infection driving revisions. Glenoid loosening manifests in up to 48% of anatomic cases within two years, raising concerns about fixation strategies. Metal-backed components paired with polyethylene inserts exhibit elevated revision risk, prompting shifts toward monoblock polyethylene or hybrid designs. Five-year mortality after arthroplasty reaches 16.6% among Medicare beneficiaries, a reminder that comorbidities significantly influence outcomes. Continuous design refinement and rigorous infection-control protocols remain paramount.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Geriatric Population & Life Expectancy

- Growth of Outpatient Arthroplasty Programs

- High Procedure & Implant Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anatomical prostheses supplied 66.34% of 2024 revenue, yet reverse systems are closing the gap at a 7.13% CAGR. Surgeons favor anatomical implants for patients with intact rotator cuffs because these devices imitate normal kinematics and preserve humeral bone. Stemless variants shorten operative time by sidestepping canal preparation and simplifying future revision. Reverse implants dominate cuff-deficient cases, unstable fractures, and revisions, boasting 10-year survival above 88%.

Design evolution centers on lateralized centers of rotation and distalized glenospheres, which boost deltoid tension and extend range of motion. Inlay reverse systems simplify glenoid exposure, whereas onlay platforms provide incremental stability in cases with bone loss. Modular platforms now accommodate both anatomical and reverse configurations, permitting intraoperative decision shifts without additional inventory. These advancements broaden indications and reinforce the competitive posture of companies delivering configurable solutions across the shoulder replacement market.

Total shoulder replacement maintained 44.39% revenue in 2024, supported by decades of outcome data and widespread surgeon familiarity. Reverse total shoulder replacement, however, propels volume expansion at 8.20% CAGR through complex tear arthropathy, fractures, and re-revision pathways. Resurfacing hemiarthroplasty remains relevant for focal chondral lesions in young athletes who may postpone total replacement, while stemmed hemiarthroplasty has receded as reverse alternatives demonstrate higher pain relief and function.

The trajectory toward reverse total procedures reflects evidence that combined tendon transfers can regain 32° of external rotation, enhancing daily living activities. Robotic platforms support both anatomical and reverse workflows, unifying instrumentation and reducing learning curves. Outpatient migration is no longer limited to primary anatomical cases; carefully selected reverse procedures are now discharged the same day with equivalent safety profiles. This procedural diversity injects resilience into the shoulder replacement market by dispersing growth across varied clinical indications.

The Shoulder Replacement Market Report is Segmented by Product Type (Anatomical Prosthesis, Reverse Prosthesis, and More), Procedure (Resurfacing Hemiarthroplasty, Stemmed Hemiarthroplasty, and More), Fixation (Cemented, and More), End User (Hospitals, Orthopedic Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains primacy with a 39.81% revenue share in 2024, underpinned by mature reimbursement structures and roughly 53,000 annual arthroplasty procedures in the United States alone. CMS inclusion of total shoulder replacement in the ASC covered list amplifies procedural migration, while national joint registries support evidence-based device selection. Canada confronts elective surgery backlogs by increasing theater capacity, whereas Mexico leverages cost differentials to attract international patients.

Asia-Pacific posts the fastest CAGR at 8.47% to 2030, fueled by hospital infrastructure expansion, rising middle-class income, and government policies that seek affordable orthopedic solutions. China's volume-based procurement has reduced inpatient costs by half, enabling broader access to implants without sacrificing quality. Japan's super-aged society magnifies procedure demand even as it exercises strict regulatory oversight. India's private hospital chains pursue medical tourism, importing high-end implants while promoting indigenous manufacturing under the "Make in India" framework. Australia continues to punch above its population weight in clinical trials, offering early adoption opportunities for new technologies.

Europe records steady uptake across public and private systems. Germany's manufacturing base underwrites high domestic adoption, while the United Kingdom persists in joint replacement research despite Brexit regulatory realignment. France and Italy refine enhanced recovery protocols that trim length of stay without increasing readmissions. Nordic registries provide granular data that illuminate technique-outcome correlations, guiding global practice patterns. Although the European Medical Device Regulation has extended approval timelines, its emphasis on safety may elevate regional confidence in next-generation implants. Collectively, these regional patterns assure diversified revenue streams that insulate the shoulder replacement market from isolated policy shocks.

- Arthrex

- Zimmer Biomet

- Integra LifeSciences

- Johnson & Johnson

- Smiths Group

- Wright Medical Group

- Stryker

- Enovis Corporation (DJO Global)

- Acumed

- Exactech

- LimaCorporate S.p.A

- Conmed

- B. Braun

- Medacta International

- Stryker

- Apex Biomedical

- Globus Medical

- FH Orthopedics

- Biotechni SAS

- Ascension Orthopedics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Arthritis

- 4.2.2 Technological Advances in Prosthesis Design

- 4.2.3 Expanding Geriatric Population & Life Expectancy

- 4.2.4 Growth of Outpatient Arthroplasty Programs

- 4.2.5 AI-Driven Patient-Specific Instrumentation

- 4.2.6 Rising Sports-Injury Cases Driving Young Demand

- 4.3 Market Restraints

- 4.3.1 Post-Operative Complications & Implant Loosening

- 4.3.2 High Procedure & Implant Costs

- 4.3.3 Volatile Supply of Medical-Grade Metals & UHMWPE

- 4.3.4 Stricter Approval Cycles for Reverse Prostheses

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Anatomical Prosthesis

- 5.1.1.1 Stemmed Anatomical

- 5.1.1.2 Stemless Anatomical

- 5.1.2 Reverse Prosthesis

- 5.1.2.1 Inlay Reverse

- 5.1.2.2 Onlay Reverse

- 5.1.2.3 Stemless Reverse

- 5.1.3 Hybrid/Biological Prosthesis

- 5.1.1 Anatomical Prosthesis

- 5.2 By Procedure

- 5.2.1 Resurfacing Hemiarthroplasty

- 5.2.2 Stemmed Hemiarthroplasty

- 5.2.3 Total Shoulder Replacement

- 5.2.4 Reverse Total Shoulder Replacement

- 5.2.5 Partial Shoulder Replacement

- 5.3 By Fixation

- 5.3.1 Cemented

- 5.3.2 Cementless

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Orthopedic Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Arthrex Inc.

- 6.3.2 Zimmer Biomet Holdings Inc.

- 6.3.3 Integra LifeSciences Holdings Corporation

- 6.3.4 Johnson & Johnson (DePuy Synthes)

- 6.3.5 Smith & Nephew plc

- 6.3.6 Wright Medical Group N.V.

- 6.3.7 Stryker Corporation

- 6.3.8 Enovis Corporation (DJO Global)

- 6.3.9 Acumed LLC

- 6.3.10 Exactech Inc.

- 6.3.11 LimaCorporate S.p.A

- 6.3.12 Conmed Corporation

- 6.3.13 B. Braun Melsungen AG

- 6.3.14 Medacta International

- 6.3.15 Stryker Corporation

- 6.3.16 Apex Biomedical

- 6.3.17 Globus Medical Inc.

- 6.3.18 FH Orthopedics

- 6.3.19 Biotechni SAS

- 6.3.20 Ascension Orthopedics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment