|

시장보고서

상품코드

1836694

인도의 고급차 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)India Luxury Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

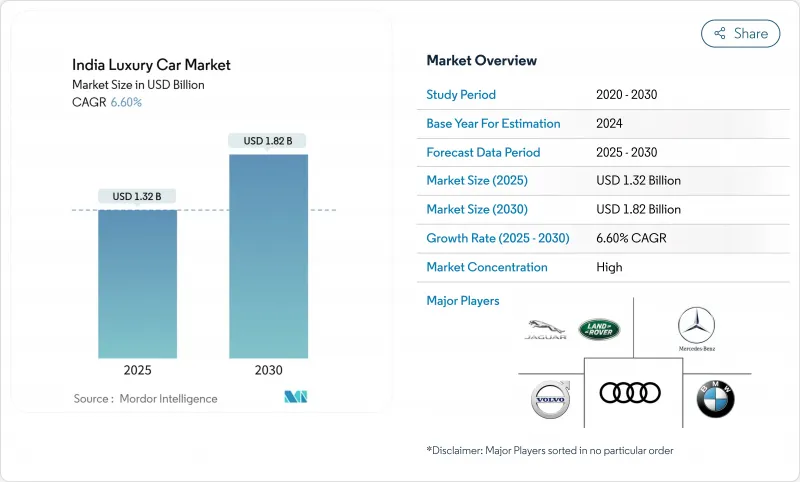

인도의 고급차 시장 규모는 2025년에 13억 2,000만 달러로 추정되고, 2030년에는 18억 2,000만 달러에 이를 전망이며, CAGR 6.60%로 확대될 것으로 예측됩니다.

견조한 성장의 배경은 중상류층 가구의 가처분 소득 증가, 사용 가능한 크레딧 확대, 고급차의 총 소유 비용을 압축하는 차별화된 주 수준의 EV 인센티브를 포함합니다. 독일의 기존 기업을 중심으로 경쟁이 격화되어 제품 선택의 폭이 넓어지고 모델 사이클이 단축되고 있습니다. 수요면에서는 수입관세를 삭감하고 가격을 5-8만 루피로 억제한 현지조립을 뒷받침하며, 티아 II 도시로부터의 열망적인 구매층은 프리미엄 브랜드에 대한 지지를 강화하고 있습니다. 세제의 복잡성과 ADAS 서비스의 기술 부족이 성장 곡선을 약화시키고 있는 것, 고객층이 확대되고 OEM이 디지털 소매 저니를 구매 프로세스에 통합함에 따라 장기적인 궤도는 계속 견조합니다.

인도의 고급차 시장 동향 및 인사이트

중상류층 가구의 프리미엄화

연간 수입 2천만 루피 이상의 부유층 가구는 2025년까지 1천만 명에서 2천 6백만 명으로 증가할 것으로 예측되어 인도의 고급차 시장에 광범위한 기반을 구축했습니다. 젊은 전문가와 1세대 기업가들은 고급차를 스테이터스 심볼로 파악하는 경향이 강해져 구매당 예산 배분을 높이고 있습니다. 메르세데스 벤츠는 2024년에는 납차의 80%가 대출을 받았고 스타 어질리티 체계의 보급률은 63%에 달했다고 합니다. 술라트와 코임바톨 등 Tier-II의 거점에 있는 브랜드의 쇼룸에서는 방문객 수가 2배가 되어 대도시권 이외에의 보급을 시사하고 있습니다. 이러한 인구 동태의 변화로 인해 판매가능한 베이스가 크게 확대되고 거시적인 변동이 있는 가운데도 일관된 성장을 추진하고 있습니다.

엔트리 모델(CKD) 가용성 증가

현지 조립을 통해 OEM은 완전 생산 차량의 수입 관세를 피할 수 있으며, 고급차으로서의 가치를 손상시키지 않으면서 엔트리 모델을 경쟁력있는 위치에 배치할 수 있습니다. BMW는 50% 현지화를 달성했고, 메르세데스 벤츠는 60%에 이르렀으며 INR 20-50,000개의 게이트웨이 부문에서 전략적 가격 설정을 가능하게 합니다. 긴 휠 기반 파생 차종, 후방 좌석의 냉각 기능 강화, 인도 특유의 서스펜션 설정 등은 CKD 사업이 세계 모델을 현지 선호도에 맞추는 방법을 보여줍니다. 그러나 2024년 예산의 새로운 규칙은 중요한 파워트레인 컴포넌트의 국내 조립을 의무화하고 손익분기점을 끌어올려 일부 소량 생산 차종은 가격 인상에 몰렸습니다. 그럼에도 불구하고 OEM은 CKD를 대수 규모 확장, 공급업체 에코시스템 구축, 모델 업데이트 사이클 가속화에 필수적인 것으로 간주하고 있으며 시장 성장에 대한 CKD의 순 플러스 기여를 강화하고 있습니다.

높은 GST 및 Cess 구조(최대 50개)

GST와 Cess를 합산하면 전시회 가격이 50% 상승할 수 있으며, 취득 비용이 늘어나 풍부함이 증가함에도 불구하고 대응 가능한 총 수요가 억제됩니다. 2024년도 예산에서는 4만 달러 이상의 프리미엄 수입품에 대한 관세가 70%로 반감된 반면 40%의 농업 인프라 개발세스가 도입되어 실질적인 과세율은 110%로 돌아왔습니다. 이 변동은 OEM의 가격 전략을 복잡하게 만들고 재고를 쓸어내기 위해 브랜드를 최대 15,000 루피까지 할인하는 방향으로 유도합니다. 이 페널티는 초고급 CBU에서는 더욱 심각하지만, 현지 조립 모델은 비교적 보호되어 틈새 모델이라도 CKD 라인의 지속적인 확대가 추진되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 주정부에 의한 EV 우대조치

- 도시간 회랑에서의 150kW 이상의 공공 DC 충전기의 급속 전개

- 공인 중고차 네트워크 구축 지연

부문 분석

SUV는 인지된 안전성, 도로에서의 압도적인 존재감, 혼합된 고속도로 상황에 적합한 뛰어난 지상고를 배경으로 2024년 인도의 고급차 시장 점유율의 48.10%를 획득했습니다. 캐빈의 부피가 크다는 것도 기업의 사장에서 자주 볼 수 있는 운전자와 함께 이용 사례를 지지하고 있습니다. 메르세데스 벤츠 GLE와 BMW X5가 계속 판매 대수의 축이 되는 한편, 현지 조립의 아우디 Q3는 동경을 품게 하는 층에 대한 리치를 넓혔습니다. OEM 각사는 '오프로드' 체험 이벤트를 통해 수요를 더욱 확대해 처음으로 고급차를 구입하는 소비자에게 제품의 견고성을 재확인시켰습니다.

세단은 운전에 열심인 밀레니얼 세대와 X세대 소비자가 역동적인 핸들링과 세련된 미관에 매료되어 CAGR 예상 9.80%로 부활하고 있습니다. 2024년 BMW M 시리즈 판매량은 250% 급증했고 메르세데스 마이바흐 판매량은 거의 두 배로 증가했습니다. 이것은 고출력 파워트레인과 후방 좌석의 럭셔리에 대한 왕성한 의욕을 보여줍니다. 또한 BMW i7과 메르세데스 EQS와 같은 전동화 리무진은 성능과 지속가능성을 결합하여 부문 인식을 재설정하고 유비쿼터스 SUV에 대해 차별화된 가치 제안을 만들어 냈습니다. 대수 기반에서는 세단이 2024년 27%에서 2030년 32%로 증가하여 모든 주요 OEM 포트폴리오의 다양성을 높일 것으로 예측됩니다.

가솔린 하이브리드와 디젤 파워트레인이 입증된 신뢰성, 신속한 급유, 275개 이상의 공인 정비 공장에 의한 광범위한 서비스 지원을 제공하고 있는 것이 주된 이유입니다. 고급 BEV의 CAGR은 21.35%로 예상되고 있습니다. BMW의 iX, i4, i7 모델은 처음으로 EV를 구입하는 사용자에게 많은 ICE 차량을 능가하는 첨단 운전 지원 기능을 소개합니다.

DC 급속 충전의 가용성이 확대됨에 따라, 부유층 소비자는 항속 거리에 대한 마지막 불안의 장애물을 넘어, 러닝 비용의 저하와 그린 넘버 플레이트 특전이 편리성의 가치를 높이고 있습니다. 하이브리드 자동차는 일시적인 부문을 차지하고 연비 효율에 열성이지만, 자신이 사는 도시의 충전 인프라에 납득하지 않은 고객을 흡수하고 있습니다. 테슬라가 2025년 뭄바이에 쇼룸을 연 것으로 경쟁이 심화되고 무선 업데이트, 역동적인 소프트웨어 기능, 직접 판매 투명성에 대한 고객의 기대가 높아질 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중상류층 세대의 프리미엄화

- 엔트리 모델(CKD) 증가

- 주정부에 의한 EV 우대조치

- 도시 간 회랑에서 150kW 이상의 공공 DC 충전기 급속 전개

- OEM에 의한 구독과 리스 및 스킴

- 중국의 초고급 EV 브랜드가 인도를 다음 진출 지역으로 주목

- 시장 성장 억제요인

- 높은 GST 및 Cess 구조(최대 50)

- CBU에 대한 수입관세 불확실성

- 인증 중고차 네트워크 구축 지연

- ADAS 및 고전압 시스템의 훈련을 받은 기술자의 부족

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(USD)

- 자동차 유형별

- SUV

- 세단

- 해치백

- 구동 유형별

- IC 엔진

- 하이브리드

- 배터리 및 일렉트릭

- 가격대별

- INR 20 L-50 L

- INR 50 L-80 L

- INR 80L 이상

- 판매 채널별

- 직영 쇼룸

- 정규 딜러 및 프랜차이즈

- 온라인(소비자 직접 판매)

- 지역별(인도)

- 북인도

- 서인도

- 남 인도

- 동 및 북동 인도

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Mercedes-Benz AG

- BMW Group

- Audi AG

- Jaguar Land Rover Automotive PLC

- Volvo Car AB

- Lexus

- Porsche AG

- Rolls-Royce Motor Cars India

- Bentley Motors Limited

- Automobili Lamborghini SpA

- Ferrari India

- Maserati SpA

- Aston Martin Lagonda Global Holdings PLC

- Jeep(Stellantis)

제7장 시장 기회 및 전망

AJY 25.10.27The India luxury car market size stands at USD 1.32 billion in 2025 and is forecast to reach USD 1.82 billion by 2030, expanding at a 6.60% CAGR.

Robust growth stems from rising disposable income among upper-middle-class households, expanded credit availability, and differentiated state-level EV incentives that compress the total cost of ownership for premium automobiles. Intensifying competitive activity, particularly among German incumbents, continues to widen product choice and shorten model cycles, while accelerating infrastructure roll-outs ease range anxiety for high-performance battery electric vehicles. On the demand side, aspirational buyers from Tier-II cities increasingly favour premium brands, helped by localized assembly that trims import duties and keeps prices within the INR 50-80 lakh bracket. Although taxation complexity and skill shortages in ADAS servicing temper the growth curve, the long-term trajectory remains firmly positive as customer cohorts expand and OEMs embed digital retail journeys into the purchase process.

India Luxury Car Market Trends and Insights

Premiumization of Upper-middle-class Households

Affluent households earning over INR 20 lakh annually are forecast to increase from 10 million to 26 million by 2025, laying a broad foundation for the Indian luxury car market. Younger professionals and first-generation entrepreneurs increasingly view premium vehicles as status symbols, driving higher budget allocations per purchase. OEM finance programmes reinforce the trend; Mercedes-Benz notes that 80% of deliveries were financed in 2024 and that its Star Agility scheme grew 63% in penetration. Brand showrooms in Tier-II hubs such as Surat and Coimbatore are now seeing double the footfall, signaling diffusion beyond metropolitan areas. This demographic shift materially enlarges the addressable base, propelling consistent growth even amid macro volatility.

Rising Availability of Entry-level Models (CKD)

Localized assembly enables OEMs to bypass steep import duties on completely built units, positioning entry variants competitively without eroding luxury cachet. BMW has achieved 50% localization, while Mercedes-Benz has reached 60%, allowing strategic pricing in the INR 20-50 lakh gateway segment. Tailored long-wheelbase derivatives, enhanced rear-seat cooling, and India-specific suspension setups showcase how CKD operations adapt global models to local preferences. New 2024 Budget rules, however, require domestic assembly of critical powertrain components, raising breakeven thresholds and pushing some low-volume nameplates toward price hikes. Even so, OEMs regard CKD as indispensable for volume scale, supplier ecosystem development, and faster model refresh cycles, reinforcing its net positive contribution to market growth.

High GST & Cess Structure (up to 50%)

Combined GST and cess charges can lift ex-showroom prices by 50%, inflating acquisition costs and constricting total addressable demand despite rising affluence. While the 2024 Budget halved customs duty on premium imports above USD 40,000 to 70%, it introduced a 40% Agriculture Infrastructure and Development Cess, returning the effective levy to 110% . This volatility complicates OEM pricing strategies and nudges brands toward discounting, often up to INR 15 lakh, to clear inventory. The penalty is more acute for ultra-luxury CBUs, whereas locally assembled variants remain relatively sheltered, driving continuous expansion of CKD lines even for niche models.

Other drivers and restraints analyzed in the detailed report include:

- EV Incentives by State Governments

- Rapid Rollout of 150 kW+ Public DC Chargers on Inter-city Corridors

- Slow Build-out of Certified Pre-owned Luxury Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs captured 48.10% of India's luxury car market share in 2024 on the back of perceived safety, commanding road presence, and superior ground clearance suited to mixed highway conditions. Larger cabin volume also supports chauffeur-driven use cases common among corporate principals. Mercedes-Benz GLE and BMW X5 remained volume anchors, while locally assembled Audi Q3 extended reach into aspirational cohorts. OEMs further amplified demand through 'off-road' experiential events that reassured first-time luxury buyers about product robustness.

Sedans are resurging with a forecast 9.80% CAGR as driving-enthusiast millennials and Gen-X consumers gravitate toward dynamic handling and sleek aesthetics. BMW M series deliveries soared 250% in 2024, and Mercedes-Maybach nearly doubled volumes, indicating a robust appetite for high-output powertrains and rear-seat luxury. Electrified limousines such as the BMW i7 and Mercedes EQS also reset segment perception by combining performance with sustainability, creating a differentiated value proposition against omnipresent SUVs. In volume terms, sedans are expected to lift their contribution from 27% in 2024 to 32% by 2030, boosting portfolio diversity for all major OEMs.

Internal combustion platforms still underpin 75.20% of deliveries, largely because petrol hybrids and diesel powertrains offer proven reliability, quick refuelling, and extensive service support across 275+ authorized workshops. However, electrification momentum is unmistakable: luxury BEVs are expected to register a 21.35% CAGR. BMW's iX, i4, and i7 models are introducing first-time EV buyers to advanced driver-assist features that surpass many ICE counterparts.

Widening DC-fast-charge availability pushes affluent consumers over the last range-anxiety hurdle, while lower running costs and green-number-plate privileges add material convenience value. Hybrids occupy a transitory segment, absorbing customers keen on fuel efficiency but unconvinced about charging infrastructure in their city. Tesla's Mumbai showroom opening in 2025 is likely to intensify competition and elevate customer expectations for over-the-air updates, dynamic software features, and direct sales transparency.

The India Luxury Car Market Report is Segmented by Vehicle Type (SUV, Sedan and More), Drive Type (IC Engine, Hybrid and More), Price Range (INR 20 L- 50 L, INR 50 L - 80 L and More), Sales Channel (Company-Owned Showrooms, Authorized Dealerships/Franchise and More) and Region. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mercedes-Benz AG

- BMW Group

- Audi AG

- Jaguar Land Rover Automotive PLC

- Volvo Car AB

- Lexus

- Porsche AG

- Rolls-Royce Motor Cars India

- Bentley Motors Limited

- Automobili Lamborghini S.p.A.

- Ferrari India

- Maserati S.p.A

- Aston Martin Lagonda Global Holdings PLC

- Jeep (Stellantis)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of Upper-middle-class households

- 4.2.2 Rising availability of entry-level models (CKD)

- 4.2.3 EV incentives by state governments

- 4.2.4 Rapid rollout of 150 kW+ public DC chargers on inter-city corridors

- 4.2.5 OEM-financed subscription & leasing schemes

- 4.2.6 Chinese ultra-luxury EV brands eyeing India as next launch pad

- 4.3 Market Restraints

- 4.3.1 High GST & Cess structure (up to 50 %)

- 4.3.2 Import duty uncertainty on CBUs

- 4.3.3 Slow build-out of certified pre-owned luxury networks

- 4.3.4 Scarcity of trained technicians for ADAS & high-voltage systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 SUV

- 5.1.2 Sedan

- 5.1.3 Hatchback

- 5.2 By Drive Type

- 5.2.1 IC Engine

- 5.2.2 Hybrid

- 5.2.3 Battery Electric

- 5.3 By Price Range

- 5.3.1 INR 20 L to 50 L

- 5.3.2 INR 50 L to 80 L

- 5.3.3 Above INR 80 L

- 5.4 By Sales Channel

- 5.4.1 Company-owned Showrooms

- 5.4.2 Authorized Dealerships / Franchise

- 5.4.3 Online (Direct-to-Consumer)

- 5.5 By Region (India)

- 5.5.1 North India

- 5.5.2 West India

- 5.5.3 South India

- 5.5.4 East & North-East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mercedes-Benz AG

- 6.4.2 BMW Group

- 6.4.3 Audi AG

- 6.4.4 Jaguar Land Rover Automotive PLC

- 6.4.5 Volvo Car AB

- 6.4.6 Lexus

- 6.4.7 Porsche AG

- 6.4.8 Rolls-Royce Motor Cars India

- 6.4.9 Bentley Motors Limited

- 6.4.10 Automobili Lamborghini S.p.A.

- 6.4.11 Ferrari India

- 6.4.12 Maserati S.p.A

- 6.4.13 Aston Martin Lagonda Global Holdings PLC

- 6.4.14 Jeep (Stellantis)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment