|

시장보고서

상품코드

1836697

세라믹 매트릭스 복합재(CMC) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ceramic Matrix Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

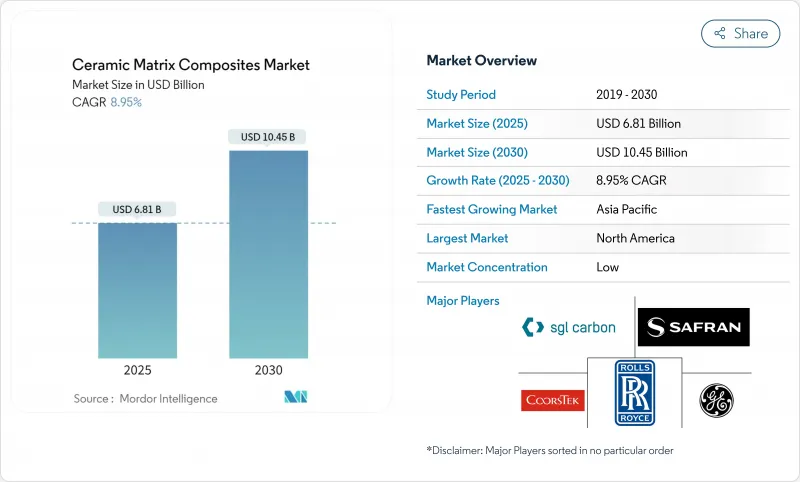

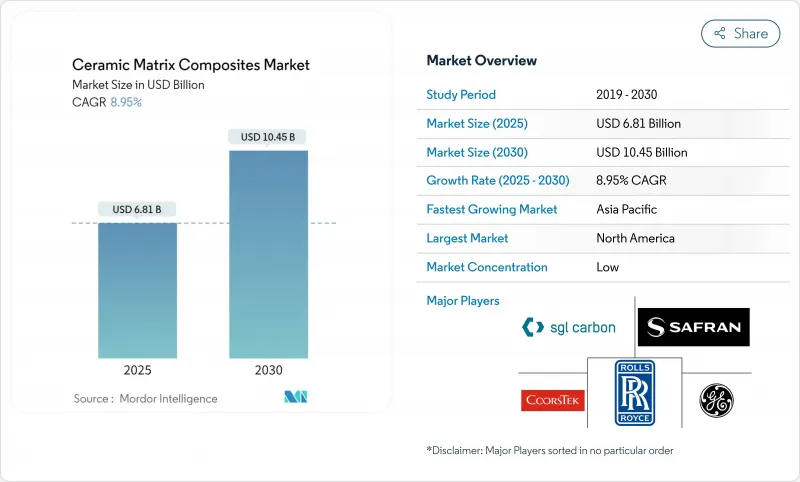

세계의 세라믹 매트릭스 복합재 시장 규모는 2025년 68억 1,000만 달러로 평가되었고, 2030년 104억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 동안 8.95%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

이 시장의 확대는 금속의 인성과 세라믹의 내열성을 겸비한 이 재료의 능력에 달려 있으며, 이 밸런스는 항공우주 엔진, 극초음속 시스템, 산업용 가스 터빈의 성능을 향상시킵니다. 경량 추진에 대한 투자, 연료 연소 기준의 엄격화, 가변 연료 터빈의 채용, 고온 부품의 장수명화의 추구가 현재 수요 전망을 형성하고 있습니다. 섬유의 자동 배치와 반응성 용융 침투의 비용 절감의 발전은 사이클 시간을 단축하고 니켈 초합금과의 비용 격차를 줄였습니다. 화학처리 업체부터 핵융합 에너지 개발업자에 이르기까지 보다 폭넓은 최종 사용자가 CMC를 지정하게 되어 장기적인 성장회복력을 지원하는 기회 구성의 다양화가 반영되고 있습니다.

세계의 세라믹 매트릭스 복합재 시장 동향 및 인사이트

방위 등급 차열 용도 증가

국방기관은 현재 열 능력을 주요 설계 필터로 취급하고 있습니다. 미국의 초음속 탄약 프로그램은 2,000°C 이상에서 구조적으로 안정한 상태를 유지하는 재료가 필요하며,이 임계 값은 대부분의 초합금을 제거합니다. 록히드 마틴의 일련의 테스트는 전자 장비의 견고성과 에어로 쉘 보호에 CMC의 필요성을 돋보이게 합니다. 국방 계약업체가 생존 가능성에 대해 받아들이는 값 비싼 가격은 조기 CMC 인증을 가속화하고 다른 부문에 이익을 제공하는 학습 곡선을 생성합니다. 탄소섬유 강화 실리콘 카바이드 복합재료는 여러 번의 고열 사이클 후에 재사용 가능한 성능을 입증하며, 수명주기 비용 방정식을 전환하는 이점이 있습니다.

경량 차량 플랫폼 수요

전기자동차와 자율주행차 프로그램은 1킬로그램을 절약할 때마다 주행거리와 냉각 효율이 향상되므로 적극적인 질량 삭감 목표를 추구하고 있습니다. 세라믹 매트릭스 복합재는 니켈계 합금보다 무게가 최대 65% 가볍지만 배기 온도에서도 기능 강도를 유지합니다. 일본에서 실시한 세라믹 가스터빈의 실증 시험에서는 부품 중량을 2자리 줄이면서 열효율은 40% 이상에 달했습니다. 자동차 생산량은 몇 시간에 걸친 레이업을 분 단위의 사이클로 변환하는 자동 섬유 배치와 같은 니어 넷 모양 공정을 공급업체로 밀어 올리고 있습니다.

높은 제조 비용 및 수퍼 합금 비교

CMC 부품은 고온 섬유 인발과 긴 침투 단계로 인해 동등한 금속 부품보다 여전히 3-5배 더 비쌉니다. SCANCUT 프로젝트는 획기적인 밀링 패스로 가공 시간을 70% 단축하고 유사한 자동화 돌파를 통해 차이가 줄어들고 있습니다. CMC의 수명이 연장됨에 따라 총소유비용은 개선되지만, 가격에 민감한 전력과 자동차 사용자에게는 초기 취득 가격이 여전히 장애물이 되고 있습니다. GE의 2억 달러를 투자한 앨라배마 공장은 항공우주 분야에서의 비용 평준화를 목표로 하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 성장하는 신재생 가스 터빈의 리노베이션 초음속

- 자동차의 연구개발 가속

- 복잡한 다단계 제조 경로

부문 분석

SiC/SiC 복합재료는 2024년에 55.19%의 세라믹 매트릭스 복합재 시장 점유율을 차지했으며, 2030년까지 11.05%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 2GPa 이상의 강도를 실현하는 미세 피치 섬유의 통합으로 그 구조적 범위가 확대되고 있습니다. SiC/SiC 용도의 세라믹 매트릭스 복합재 시장 규모는 새로운 제트 엔진의 코어가 슈라우드, 연소기 라이너, 노즐의 연장을 적격으로 하는 것으로 급증할 것으로 예측됩니다. 탄소/탄소 시스템은 산화를 제어할 수 있는 로켓 노즐의 틈새를 유지하며, 산화물/산화물 등급은 피크 온도보다 고유한 산화 안정성을 중시하는 산업용 열교환기의 견인 역할을 하고 있습니다.

공정의 진보는 열 사이클 동안 섬유의 손상을 완화시키는 나노 가공 계면을 포함합니다. 미쓰비시 화학 그룹의 탄소섬유 기반 C/SiC는 1,500℃ 노출에 적합하며 하이브리드 화학이 우주선의 온도 상한을 확장하는 방법을 보여줍니다. 직물 프리폼에 SiC 슬러리를 추가 증착하면 기존의 레이업에서 실현할 수 없는 복잡한 냉각 통로가 가능합니다. 이러한 혁신은 SiC/SiC 제품군의 리드를 유지하고 터빈 프라임으로부터의 투자를 유치합니다.

지역 분석

항공우주 및 방위 생태계가 밀집되어 있기 때문에 북미는 2024년 세라믹 매트릭스 복합재 시장 수익의 37.96%를 차지했습니다. 이 지역에는 SiC 섬유의 인출, 부품 레이업, 기계 가공, 엔진 조립에 걸친 수직 통합 공급망이 있습니다. 첨단 복합재 제조 혁신 연구소(Institute for Advanced Composites Manufacturing Innovation)와 같은 정부 이니셔티브는 파일럿 라인에 조성금을 흘려 지역의 능력을 뒷받침하고 있습니다. 롤스로이스와 GE는 수요 사이클을 원활하게 하고, 추가 공장 확장을 정당화하는 다년간 발주를 실시합니다.

아시아태평양은 중국과 일본이 전략적 재료 프로그램을 확대하고 있기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 10.84%로 성장할 전망입니다. 국가 계획은 고성능 섬유 공급 자립화를 목표로 하고 있으며, 2035년에 이정표 목표가 설정되었습니다. 자동차의 전동화는 가볍고 열에 강한 부품의 지역 수요를 자극합니다. 노동 비용 감소와 적극적인 보조금은 경쟁력 있는 수출 가격을 가능하게 하며, 이 지역은 중요한 소비자이며 세계 세라믹 매트릭스 복합재 시장 공급업체로 자리매김하고 있습니다.

유럽은 신재생에너지를 많이 사용하는 송전망을 지원하는 터빈 개수와 롤스 로이스사의 UltraFan과 같은 새로운 항공기 엔진의 실증 시험을 통해 안정적인 점유율을 유지하고 있습니다. EU의 연구 네트워크는 공업 자금과 민간 자금을 모아 산업용 노에 적합한 산화물 등급을 성숙시키기 위해 용도 범위를 넓히고 있습니다. 엄격한 배기 가스 규제는 CMC와 같은 효율성 향상 재료에 대한 바람직한 정책 환경을 만들어 유럽 수요를 강화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 방위 등급의 차열 용도 증가

- 경량 차량 플랫폼 수요

- 방위 분야에서 세라믹 매트릭스 복합재의 용도 확대

- 신재생 가스터빈 복고풍 증가

- 극초음속 차량의 연구개발 가속

- 시장 성장 억제요인

- 초합금에 비해 높은 제조 비용

- 복잡한 다단계 제조 루트

- 파이버 더스트 배출 규제 강화

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측 : 금액

- 제품 유형별

- C/C

- C/SiC

- Oxide/Oxide

- SiC/SiC

- 최종 사용자 산업별

- 자동차

- 항공우주

- 방위

- 에너지 및 전력

- 전기 및 전자

- 기타 최종 사용자 산업(의료 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 튀르키예

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 이집트

- 나이지리아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 랭킹 분석

- 기업 프로파일

- 3M

- applied thin films inc.

- CeramTec GmbH

- COIC

- CoorsTek Inc.

- General Electric Company

- KYOCERA Corporation

- LANCER SYSTEMS

- Mitsubishi Chemical Group Corporation

- Pratt & Whitney

- Rolls-Royce

- Safran

- SGL Carbon

- Starfire Systems Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

제7장 시장 기회 및 전망

AJY 25.10.27The global ceramic matrix composites market is valued at USD 6.81 billion in 2025 and is forecast to reach USD 10.45 billion by 2030, registering an 8.95% CAGR through the period.

Expansion rests on the material's ability to combine the toughness of metals with the heat resistance of ceramics, a balance that unlocks performance gains for aerospace engines, hypersonic systems, and industrial gas turbines. Investment in lightweight propulsion, stricter fuel-burning standards, adoption of variable-fuel turbines, and the search for longer-life high-temperature parts shape the current demand outlook. Cost-down progress in automated fiber placement and reactive melt infiltration is compressing cycle times and closing the cost gap with nickel super-alloys, while government grants for advanced-materials plants are de-risking capacity additions. A wider set of end users-from chemical processors to fusion-energy developers-now specify CMCs, reflecting a more diversified opportunity mix that supports long-term growth resilience.

Global Ceramic Matrix Composites Market Trends and Insights

Increasing Defense-Grade Thermal Barrier Applications

Defense agencies now treat thermal capability as a primary design filter. Hypersonic munitions programs in the United States require materials that remain structurally stable above 2,000 °C, a threshold that eliminates most super-alloys. Lockheed Martin's test series highlights the need for CMCs in electronics ruggedization and aero-shell protection. The premium prices defense contractors accept for survivability accelerate early CMC qualification, generating learning curves that benefit other sectors. Carbon-fiber reinforced silicon carbide composites have demonstrated reusable performance after multiple high-heat cycles, an advantage that shifts life-cycle cost equations.

Lightweight Vehicle Platforms Demand

Electric and autonomous vehicle programs pursue aggressive mass-reduction targets because every kilogram saved improves driving range and cooling efficiency. Ceramic matrix composites weigh up to 65% less than nickel-based alloys yet retain functional strength at exhaust temperatures. Demonstration ceramic gas turbines in Japan reached thermal efficiencies above 40% while cutting component weight by double-digit percentages. Automotive production volumes push suppliers toward near-net-shape processes such as automated fiber placement that convert hours-long layups into minute-level cycles.

High Production Cost vs. Super-Alloys

CMC parts still cost 3-5 times more than comparable metallic parts due to high-temperature fiber draw and lengthy infiltration steps. The SCANCUT project cut machining time by 70% through novel milling paths, and similar automation breakthroughs are narrowing the gap. Total cost of ownership improves as CMC lifetimes lengthen, but initial acquisition price remains a hurdle for price-sensitive power and automotive users. GE's USD 200 million Alabama facility targets cost parity at scale geaerospace.

Other drivers and restraints analyzed in the detailed report include:

- Growing Renewable Gas-Turbine Retrofits

- Hypersonic Vehicle R&D Acceleration

- Complex Multi-Step Manufacturing Routes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SiC/SiC composites held 55.19% ceramic matrix composites market share in 2024 and are projected to grow at an 11.05% CAGR to 2030. Integration of finer pitch fibers delivering strengths above 2 GPa has expanded their structural envelope. The ceramic matrix composites market size for SiC/SiC applications is forecast to rise sharply as new jet engine cores qualify shrouds, combustor liners, and nozzle extensions. Carbon/carbon systems maintain niches in rocket nozzles where oxidation can be controlled, and oxide/oxide grades gain traction in industrial heat exchangers that value inherent oxidation stability over peak temperature.

Process advances include nano-engineered interphases that mitigate fiber damage during thermal cycling. Mitsubishi Chemical Group's carbon-fiber-based C/SiC, qualified for 1,500 °C exposure, shows how hybrid chemistries extend temperature ceilings for space vehicles. The additive deposition of SiC slurry onto woven preforms makes complex cooling passages not feasible with legacy layups. Such innovations maintain the lead of the SiC/SiC family and attract investment from turbine primes.

The Ceramic Matrix Composites Market Report Segments the Industry by Product Type (C/C, C/SiC, Oxide/Oxide, and More), End-User Industry (Automotive, Aerospace, Defense, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Due to dense aerospace and defense ecosystems, North America commanded 37.96% of the ceramic matrix composites market revenue in 2024. The region houses vertically integrated supply chains that span SiC fiber draw, component layup, machining, and engine assembly. Government initiatives like the Institute for Advanced Composites Manufacturing Innovation funnel grants toward pilot lines, underpinning local capacity. Rolls-Royce and GE place multi-year orders that smooth demand cycles and justify further plant expansions.

Asia-Pacific delivers the fastest 10.84% CAGR through 2030 as China and Japan escalate strategic materials programs. National plans seek supply independence for high-performance fibers, with milestone targets set for 2035. Automotive electrification also stimulates regional demand for lightweight, thermally resilient parts. Lower labor costs and proactive subsidies enable competitive export pricing, positioning the region as a significant consumer and global ceramic matrix composites market supplier.

Europe maintains a steady share through turbine retrofits that support renewable-heavy grids and through new aircraft engine demonstrators such as Rolls-Royce UltraFan. EU research networks pool public and private funds to mature oxide-oxide grades suitable for industrial furnaces, widening application scope. Strict emission regulations create a positive policy environment for efficiency-raising materials like CMCs, reinforcing European demand.

- 3M

- applied thin films inc.

- CeramTec GmbH

- COIC

- CoorsTek Inc.

- General Electric Company

- KYOCERA Corporation

- LANCER SYSTEMS

- Mitsubishi Chemical Group Corporation

- Pratt & Whitney

- Rolls-Royce

- Safran

- SGL Carbon

- Starfire Systems Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing defense-grade thermal barrier applications

- 4.2.2 Lightweight vehicle platforms demand

- 4.2.3 Increasing Application of Ceramic Matrix Composites in Defense Sector

- 4.2.4 Growing renewable gas-turbine retrofits

- 4.2.5 Hypersonic vehicle R&D acceleration

- 4.3 Market Restraints

- 4.3.1 High production cost vs. super-alloys

- 4.3.2 Complex multi-step manufacturing routes

- 4.3.3 Stricter fibre-dust emission norms

- 4.4 ValueChain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 C/C

- 5.1.2 C/SiC

- 5.1.3 Oxide/Oxide

- 5.1.4 SiC/SiC

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace

- 5.2.3 Defense

- 5.2.4 Energy & Power

- 5.2.5 Electrical & Electronics

- 5.2.6 Other End-User Industries (Medical, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 Nordic Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 applied thin films inc.

- 6.4.3 CeramTec GmbH

- 6.4.4 COIC

- 6.4.5 CoorsTek Inc.

- 6.4.6 General Electric Company

- 6.4.7 KYOCERA Corporation

- 6.4.8 LANCER SYSTEMS

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 Pratt & Whitney

- 6.4.11 Rolls-Royce

- 6.4.12 Safran

- 6.4.13 SGL Carbon

- 6.4.14 Starfire Systems Inc.

- 6.4.15 TORAY INDUSTRIES, INC.

- 6.4.16 UBE Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment